VAS vs VHY: Why the Lower-Yield ETF Wins in Retirement

2 hrs ago

Most ETFs take the simplest possible approach: buy every stock in an index and weight by market capitalisation. The VanEck Morningstar Wide Moat ETF (ASX: MOAT) operates on a fundamentally different premise. It buys only US-listed companies that Morningstar analysts judge to have durable competitive advantages, and only when those companies are trading below what those analysts estimate they are worth. The result is a concentrated, equal-weighted portfolio of approximately 40-50 stocks that looks nothing like the S&P 500.

With nearly $900 million in assets under management, the MOAT ETF has become one of the larger factor-based ETFs available on the ASX. Yet its methodology sits well outside what most investors encounter when they first explore ETFs, blending a quality screen with a valuation discipline that sets it apart from both broad index funds and simpler quality-factor products. What follows explains exactly how the fund works: what an economic moat is, how stocks are selected, what the current portfolio holds, what it costs, and how it compares to other US equity ETF options available to Australian investors.

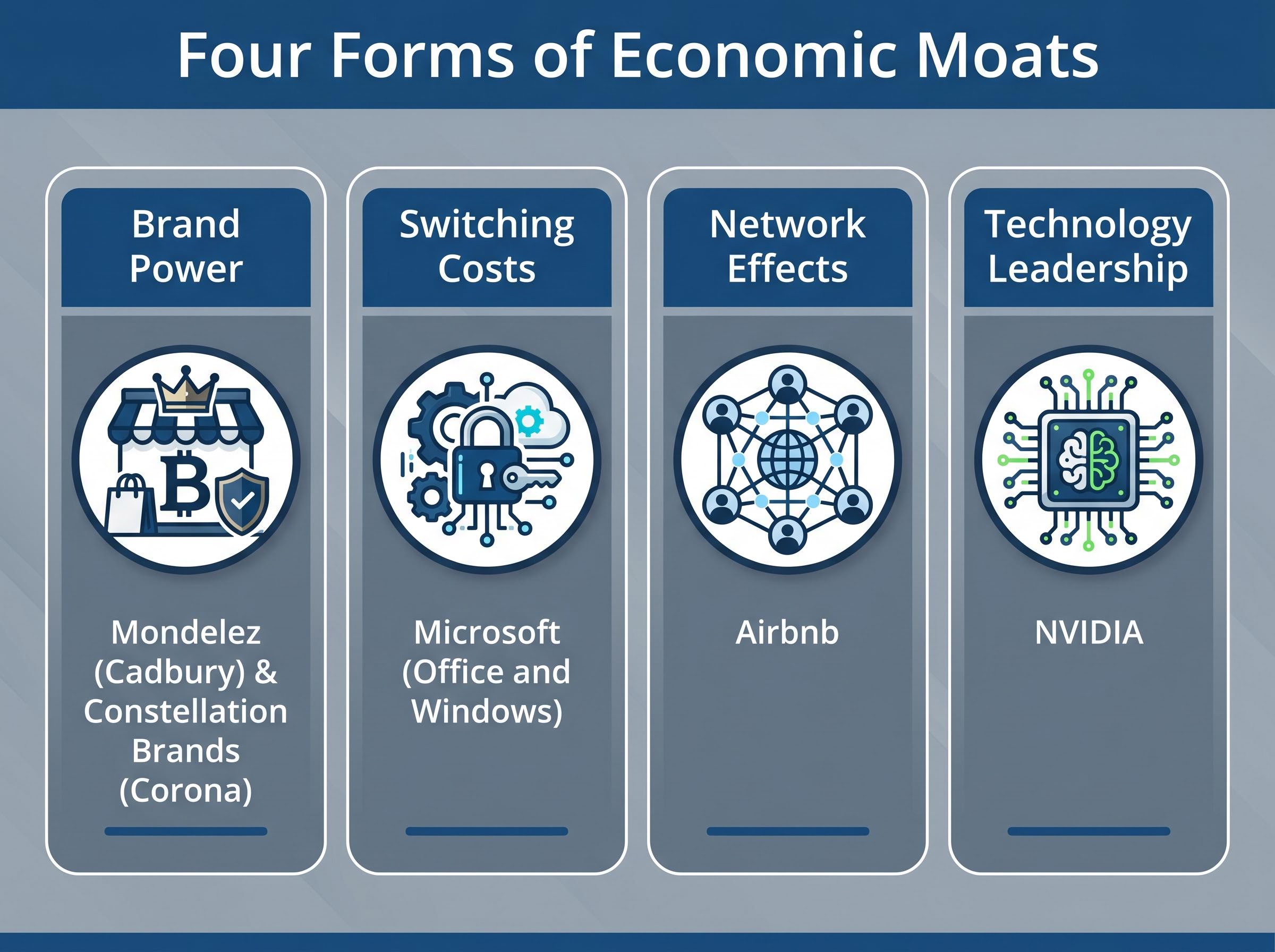

The term “economic moat” was popularised by Warren Buffett to describe a structural, durable advantage that protects a business from competitive erosion over time. A company with a wide moat can sustain higher returns on capital than its competitors, not because of a single quarter’s results, but because something about its position is genuinely difficult to replicate.

Warren Buffett described an economic moat as a business’s ability to maintain competitive advantages over its rivals in order to protect its long-term profits and market share.

Moats take several forms, and each operates differently:

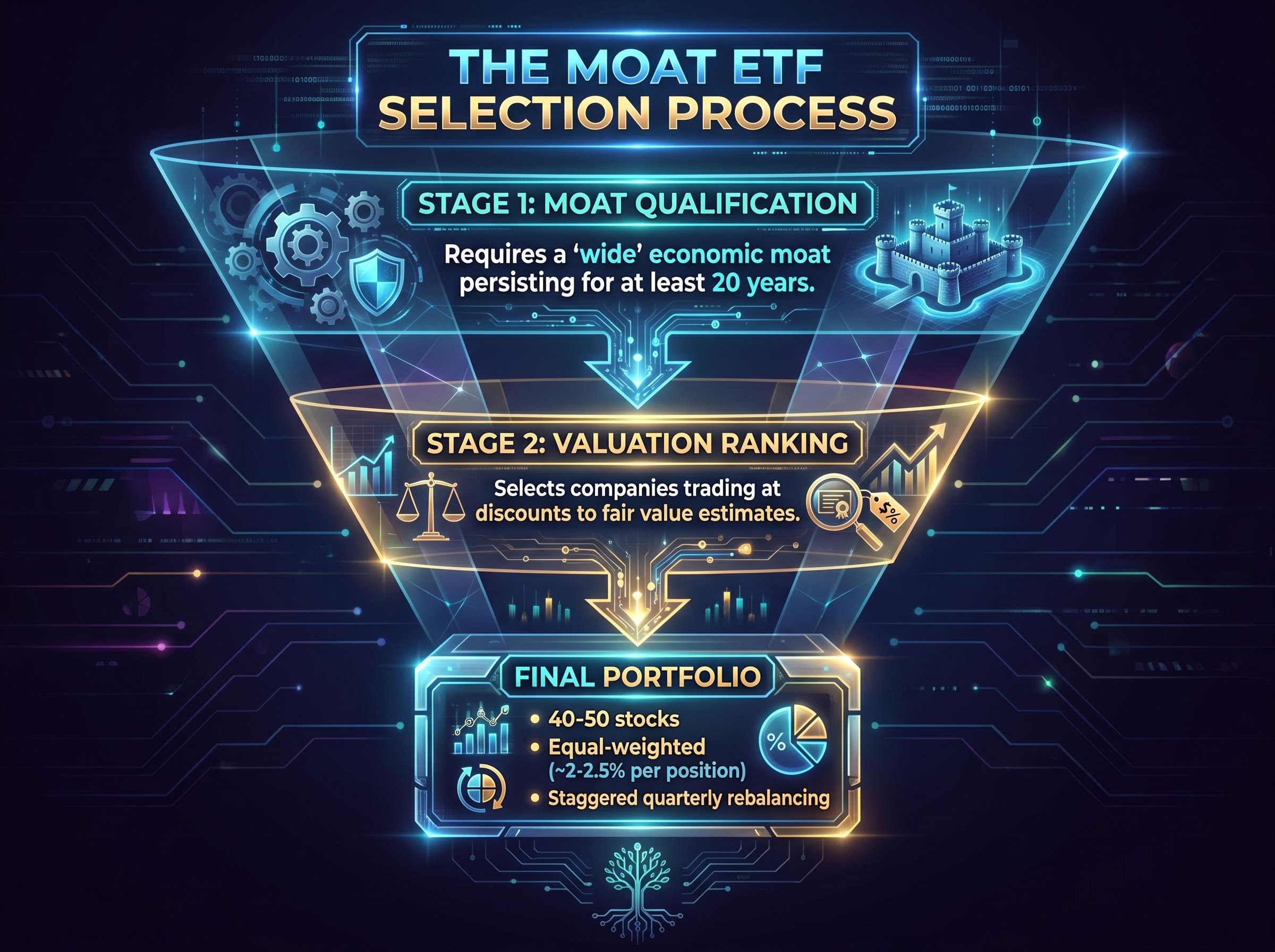

Understanding these categories matters because the MOAT ETF does not simply buy large companies. It buys companies whose competitive positions Morningstar analysts believe will persist for at least 20 years, a much higher bar than most quality screens apply.

The fund tracks the Morningstar Wide Moat Focus Index, which applies a two-stage selection process rather than a single quality filter. The distinction between these stages is what separates the MOAT ETF from simpler quality-factor products.

The selection works sequentially:

This is a rules-based, algorithmic methodology, not discretionary stock-picking. No portfolio manager is choosing favourites. The index applies both filters systematically and reconstitutes through a staggered quarterly rebalancing schedule.

The resulting portfolio of approximately 40-50 stocks is equal-weighted, meaning each holding receives roughly the same allocation at rebalance, typically around 2-2.5% per position. This produces a meaningfully different risk profile from market-cap-weighted funds, where the largest companies by size receive the largest allocations.

In a market-cap-weighted index like the S&P 500, a handful of mega-cap technology stocks can represent 25-30% of total exposure. Equal weighting removes that concentration, giving mid-cap wide-moat companies the same portfolio influence as their larger peers.

Equal-weight construction produces a structurally different return profile over time because it forces quarterly trimming of outperformers and topping up of underperformers, a mechanical discipline that contrasts with cap-weighted indexes where winning stocks accumulate an ever-larger share of the portfolio until a correction corrects the imbalance.

The fund’s top ten holdings as of 15 May 2026 illustrate how the dual screen produces a portfolio that diverges substantially from a standard US equity index.

| Rank | Company |

|---|---|

| 1 | Fortinet Inc |

| 2 | NXP Semiconductors N.V. |

| 3 | NVIDIA Corporation |

| 4 | Mondelez International Inc |

| 5 | Airbnb Inc |

| 6 | Masco Corp |

| 7 | Bristol-Myers Squibb Co |

| 8 | Kenvue Inc |

| 9 | Constellation Brands |

| 10 | Microsoft Corporation |

The spread across sectors is notable. Technology (NVIDIA, Microsoft, Fortinet), semiconductors (NXP), consumer goods (Mondelez, Constellation Brands, Kenvue), healthcare (Bristol-Myers Squibb), accommodation (Airbnb), and building products (Masco) all appear in the top ten. Durable competitive advantages are not confined to one corner of the market.

Wide-moat AI positions like NVIDIA and Broadcom have attracted particular scrutiny in 2026 because their structural advantages in proprietary silicon platforms and switching-cost lock-in are now being tested against sustained hyperscaler capital expenditure commitments, with Morningstar assigning both 4-star ratings and wide-moat designations as of May 2026 even after significant share price recoveries.

Because of equal weighting, Fortinet holds the same portfolio allocation as Microsoft, regardless of Microsoft’s vastly larger market capitalisation. This is by design: the methodology weights conviction in the moat-plus-valuation signal, not company size.

Beyond the top ten, the broader portfolio also includes:

The MOAT ETF charges an annual management fee of 0.49% per annum. That sits higher than broad-market passive ETFs, which typically charge between 0.03% and 0.07%, but remains in line with or below many actively managed fund options. The premium reflects the cost of Morningstar’s proprietary research and the more complex index construction methodology.

Performance across multiple time horizons provides context for evaluating that fee.

| Period | Total Return | Notes |

|---|---|---|

| 1-year | ~1.27%-4.82% | Range reflects different measurement dates to approximately May 2026 |

| 3-year annualised | ~8.36%-8.59% | Annualised total return |

| 5-year annualised | ~9.43% | Annualised total return |

The fund manages approximately $887.6 million in assets, according to Morningstar Australia data, making it one of the larger factor-based ETFs on the ASX.

The three-year and five-year annualised figures indicate meaningful compound returns over the medium to long term. The wider range in the one-year figure reflects the sensitivity of shorter measurement windows to prevailing market conditions at any given date.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Australian investors considering US equity exposure through the ASX typically encounter three distinct approaches, each serving a different investment priority.

ASIC’s regulatory framework for ETFs listed on the ASX requires foreign equity products to meet specific Product Disclosure Statement obligations under the AQUA rules, a standard that applies to funds like MOAT and shapes what information Australian retail investors can access before allocating capital.

| ETF | ASX Ticker | Approach | Holdings (approx.) | Management Fee |

|---|---|---|---|---|

| VanEck Morningstar Wide Moat | MOAT | Quality + valuation dual screen, equal-weighted | 40-50 | 0.49% p.a. |

| iShares Core S&P 500 | IVV | Broad passive, market-cap weighted, no factor screen | ~500 | Lower than MOAT |

| Betashares S&P 500 Quality | QUAL | Quality-factor screen, no valuation overlay | Varies | Below MOAT’s 0.49% |

The differences are structural, not just fee-related. IVV provides the broadest possible US equity exposure at the lowest cost, making it the natural default for investors who want market returns without active selection. It applies no quality or valuation filter.

QUAL adds a quality screen, selecting companies with stronger balance sheets and more consistent earnings. However, it does not apply a valuation overlay; a stock can be expensive and still qualify if it meets the quality criteria.

MOAT layers both screens, requiring companies to demonstrate a durable competitive advantage and trade below Morningstar’s fair value estimate before inclusion. The trade-off is a higher fee and a concentrated portfolio with fewer holdings than either alternative.

The right choice depends on whether an investor values broad diversification and low cost (IVV), quality-factor exposure at a moderate fee (QUAL), or a more targeted quality-plus-valuation conviction approach (MOAT).

Investors who want international moat exposure beyond US-listed equities can access the same dual-screen methodology through ASX: GOAT, which applies Morningstar’s wide-moat and valuation filters to 67 companies across developed markets excluding Australia, at a management expense ratio of 0.55% per annum.

The methodology is clear. The performance data is available. The remaining question is whether the fund’s specific characteristics align with an individual investor’s circumstances.

Considerations that may favour MOAT:

Considerations that may give pause:

VanEck Australia has announced no methodology changes in 2025-2026, providing continuity for investors evaluating the fund’s approach against its track record. The fund’s nearly $900 million in assets under management indicates meaningful adoption among both institutional and retail investors on the ASX.

Investors should review the current holdings list and compare MOAT’s sector exposures with their existing portfolio allocations before making a decision.

For investors ready to think through how MOAT would interact with their existing superannuation, domestic equity, and international equity holdings, our dedicated guide to structuring an ETF portfolio for Australian investors covers asset allocation frameworks, the impact of cap-weighted concentration in common super defaults, fee compounding over long horizons, and practical guidance on keeping a portfolio to the 2-6 fund range that minimises tax and administrative complexity.

The MOAT ETF offers Australian investors exposure to US equities filtered by two of the most enduring principles in long-term investing: quality and valuation discipline. The Morningstar Wide Moat Focus Index methodology, equal-weighted portfolio construction, and 0.49% annual fee represent a deliberate trade-off, paying more for a more selective process.

Nearly $900 million in assets under management signals established market acceptance. The fund’s dual-screen approach remains distinct from both broad passive options like IVV and single-factor products like QUAL.

Investors considering an allocation should compare the fund’s current holdings and sector exposures against their existing portfolios and consult a financial adviser for guidance tailored to their individual circumstances.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The MOAT ETF (ASX: MOAT) is a VanEck fund that tracks the Morningstar Wide Moat Focus Index, selecting approximately 40-50 US-listed companies with durable competitive advantages that are also trading below Morningstar's fair value estimates, with each holding equally weighted at rebalance.

An economic moat is a structural, durable competitive advantage that protects a business from rivals over time, such as brand power, switching costs, network effects, or technology leadership. The MOAT ETF only holds companies Morningstar analysts believe can sustain these advantages for at least 20 years.

The MOAT ETF charges an annual management fee of 0.49% per annum, which is higher than broad-market passive ETFs that typically charge between 0.03% and 0.07%, but reflects the cost of Morningstar's proprietary research and the dual-screen index methodology.

IVV provides broad passive exposure to around 500 US stocks at a lower cost with no quality or valuation filter, QUAL adds a quality screen but no valuation overlay, while MOAT applies both screens and uses equal weighting across a concentrated portfolio of 40-50 stocks at a 0.49% fee.

As of May 2026, the top ten holdings include Fortinet, NXP Semiconductors, NVIDIA, Mondelez, Airbnb, Masco, Bristol-Myers Squibb, Kenvue, Constellation Brands, and Microsoft, with each holding an approximately equal portfolio allocation regardless of market capitalisation.