Why a Rising AUD Is Quietly Eroding Your International ETF Returns

13 hrs ago

Most investors understand that buying quality companies matters. Far fewer can explain what makes that quality durable for 20 years or more, and fewer still know that a single ASX-listed ETF applies a 100-plus analyst research framework to answer exactly that question.

The VanEck Morningstar International Wide Moat ETF (ASX: GOAT) brings Morningstar’s economic moat framework to Australian investors as a passive, low-cost vehicle. With A$55.5 million in assets under management and 67 holdings across developed international markets (excluding Australia), GOAT occupies a distinctive corner of the ETF landscape. It is neither a pure quality fund nor a passive index replicator, but a dual-filtered strategy that demands both competitive durability and price attractiveness before a company earns a place in the portfolio.

This article explains what an economic moat is, where moats come from, how Morningstar identifies and classifies them, and why GOAT’s combination of moat screening with valuation discipline produces a portfolio construction logic that differs meaningfully from comparable ETFs like ASX: QLTY.

In competitive markets, high profits attract competitors. Capital flows toward returns, margins compress, and yesterday’s market leader becomes tomorrow’s cautionary tale. That is the default. Yet a small category of businesses sustains elevated returns on capital for remarkably long periods, not because competitors are unaware of the opportunity, but because structural defences make it genuinely difficult to replicate their position.

Warren Buffett introduced the term “economic moat” to describe these defences, borrowing the image of a castle’s protective perimeter. The concept is not about size or brand familiarity alone. It refers to specific structural characteristics, built into a company’s business model, that make competitive erosion slow, expensive, or both.

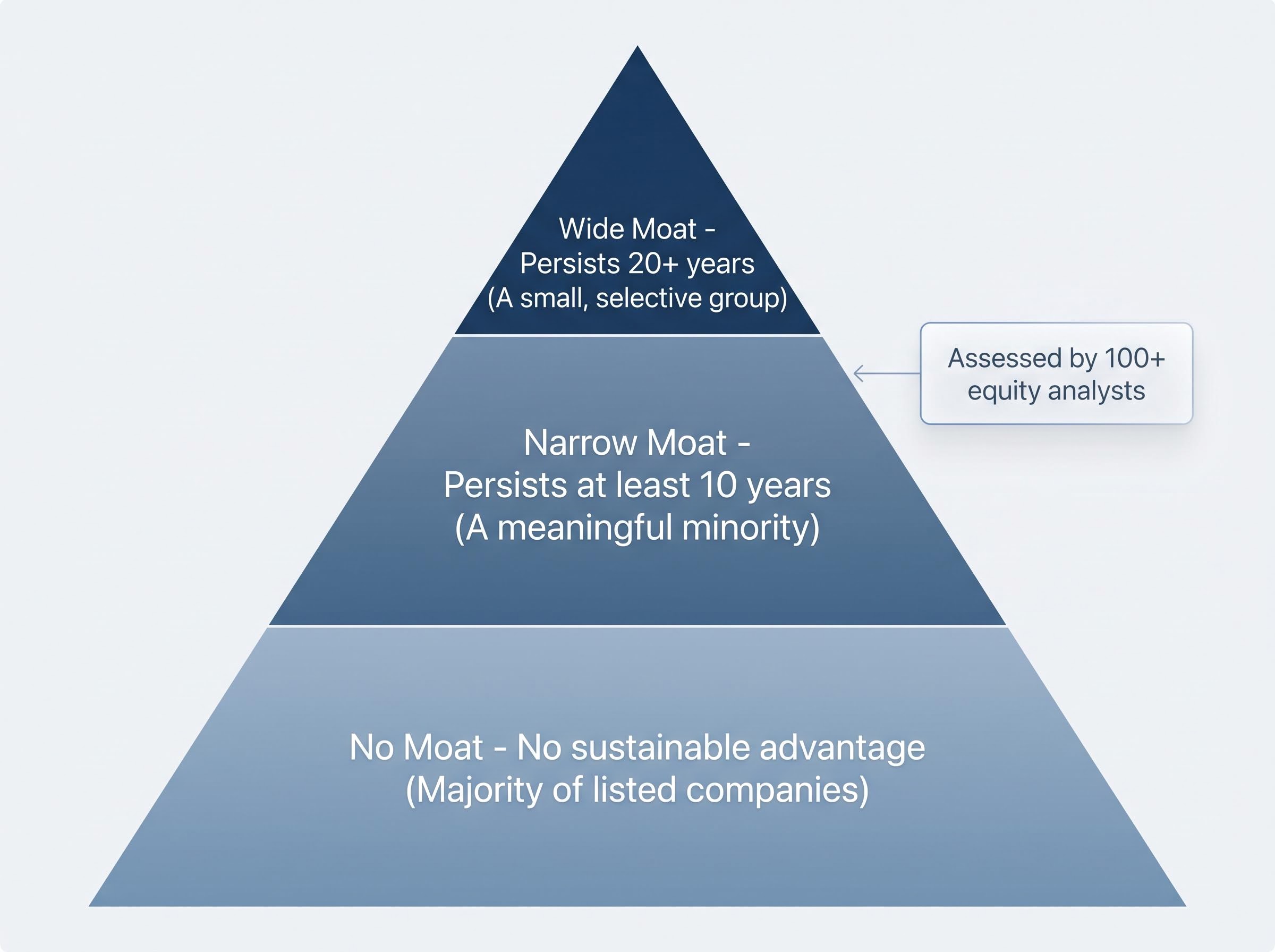

Morningstar formalised Buffett’s concept into an analytical framework, deploying more than 100 equity analysts to assess whether a company’s competitive advantage qualifies as durable.

Morningstar defines a “wide moat” as a competitive advantage expected to persist for 20 years or more, a threshold that excludes the vast majority of listed companies globally.

For Australian investors evaluating international ETFs, understanding this concept is the prerequisite for assessing whether GOAT’s screening logic is genuinely differentiated, or simply another quality label.

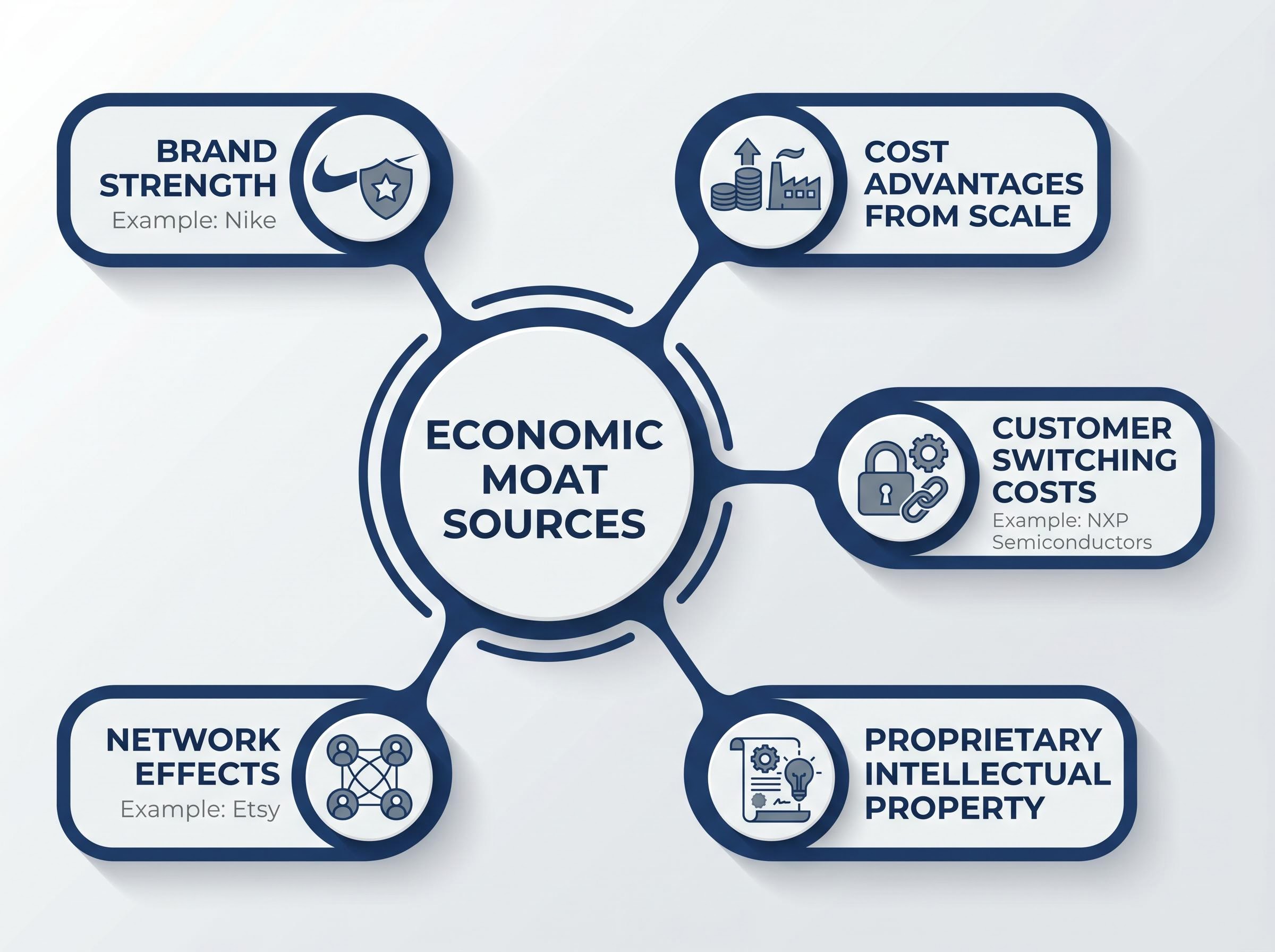

Morningstar’s analysts assess moats by identifying specific structural mechanisms that protect a company’s earnings. Five recognised sources form the taxonomy:

Return on equity is one of the five core fundamental analysis metrics that helps investors assess how efficiently a company converts shareholder capital into profit, a figure that wide moat companies tend to sustain at elevated levels precisely because their structural advantages limit competitive erosion of margins.

Morningstar recorded 14 moat upgrades in technology and 12 in industrials during 2024, a reminder that moat assessments are not fixed labels but evolving judgements tied to shifting competitive dynamics.

The strongest moats rarely rely on a single source. Companies holding multiple simultaneous advantages, such as brand strength plus switching costs, or intellectual property plus scale, receive stronger and more durable moat ratings.

Morningstar’s analyst team assesses the interaction of these sources, not merely the presence of any single one. A semiconductor company with both proprietary IP and deep customer switching costs, for instance, presents a materially higher barrier to competition than one relying on patents alone.

Morningstar’s moat framework operates as a three-tier classification system, structured as a progression of confidence levels rather than a simple pass or fail.

| Moat Rating | Durability Expectation | Selectivity |

|---|---|---|

| No Moat | No sustainable competitive advantage identified | Majority of listed companies |

| Narrow Moat | Competitive advantage expected to persist for at least 10 years | A meaningful minority |

| Wide Moat | Competitive advantage expected to persist for 20 years or more | A small, selective group |

“Wide” is deliberately set as a high bar. Morningstar’s team of more than 100 equity analysts must be confident, based on forward-looking fundamental research, that a company’s competitive advantage will endure for two decades or longer.

The 20-year threshold is not a forecast of future profitability. It is an analyst confidence assessment that the structural defences protecting a company’s market position will remain intact over that horizon.

These ratings are not permanent. Morningstar revises classifications as competitive conditions evolve. The 14 technology upgrades and 12 industrials upgrades during 2024 reflect this ongoing reassessment. In 2025, Morningstar Indexes introduced the Morningstar Global Wide Moat VC 7 Index, and the GOAT index underwent methodology simplifications effective April 2026, signalling continued development of the framework.

Understanding what “wide moat” means in practice helps investors calibrate how selective GOAT actually is. Its 67-holding portfolio is considerably more concentrated than broad international ETFs precisely because the classification threshold excludes most listed companies.

A wide moat identifies which businesses are worth owning over the long term. GOAT adds a second question: is the market offering them at an attractive price right now?

Morningstar’s proprietary fair value estimate serves as the second filter. Wide moat companies only enter the GOAT portfolio when they are also trading at a discount to that fair value estimate. The index reconstitutes periodically to rotate toward wide moat companies that have moved to more attractive valuations and remove those that have re-rated or lost moat status.

GOAT’s dual-filter logic: a company must possess a wide moat (competitive advantage expected to last 20 years or more) and trade at an attractive valuation relative to Morningstar’s fair value estimate. Both conditions must be met simultaneously.

This architecture separates GOAT from pure quality strategies. Buying a great company at the wrong price is a different risk from buying a mediocre company at any price, and GOAT’s construction explicitly accounts for that distinction.

The trade-off is worth acknowledging honestly. Valuation discipline can cause GOAT to exclude expensive quality stocks that continue rising, which may produce periods of near-term underperformance versus pure quality peers that carry no price filter.

Key fund metrics for GOAT:

Australian investors comparing GOAT and QLTY are choosing between quality philosophies, not simply shopping on fees. The two funds start from different premises, and those premises logically produce different portfolios, different return profiles, and different risk characteristics.

GOAT applies an analyst-driven, dual-filter approach: wide moat classification plus attractive valuation. QLTY, issued by BetaShares, uses a quantitative quality factor screen based on return on equity, earnings stability, and low leverage, with no explicit valuation screen.

A quality factor screen based on return on equity, earnings stability, and low leverage identifies financially disciplined businesses, but without a valuation overlay it can systematically overweight expensive sectors during momentum-driven cycles, which is the structural mechanism behind QLTY’s stronger recent returns relative to GOAT.

| Metric | ASX: GOAT | ASX: QLTY |

|---|---|---|

| Issuer | VanEck Australia | BetaShares |

| Selection methodology | Morningstar wide moat + attractive valuation | Quality factor screen (ROE, earnings stability, leverage) |

| Valuation discipline | Yes, must trade below fair value estimate | No explicit valuation screen |

| Analyst input | 100+ Morningstar analysts | Quantitative/rules-based |

| MER | 0.55% p.a. | 0.35% p.a. |

| AUM | A$55.5M | A$926M |

| Holdings | 67 | 150 |

| 1Y return | 0.38% | 4.70% |

| 3Y return (p.a.) | 5.56% | 13.18% |

| Geographic scope | Developed markets ex-Australia | Global (including US) |

The performance gap reflects structural design, not simply stock selection. QLTY’s quantitative quality screen captured the US technology re-rating cycle more fully because it does not exclude stocks on valuation grounds. Holdings such as Visa, Uber, and Lam Research illustrate that quality factor exposure without a price filter naturally tilts toward momentum in expensive sectors. GOAT’s valuation discipline caused it to underweight expensive US tech during the same period, explaining much of the return divergence.

QLTY suits investors who want rules-based quality exposure at lower cost and are comfortable accepting valuation risk in exchange for broader market participation. GOAT suits investors who want analyst-backed conviction and accept valuation discipline as a feature, understanding that near-term underperformance is the cost of that discipline.

Both funds exclude Australian equities, making them complementary to an ASX-focused core holding rather than substitutes for it.

The moat framework is an abstraction until applied to actual companies. GOAT’s top holdings as at 31 March 2026 illustrate how the dual filter produces a genuinely differentiated portfolio.

| Company | Sector / Country | Weight |

|---|---|---|

| Symrise AG | Speciality Chemicals / Germany | 2.27% |

| Thales | Defence & Aerospace / France | 2.24% |

| Unicharm Corp | Consumer Goods / Japan | 2.22% |

| Constellation Brands | Beverages / United States | 2.19% |

German speciality chemicals, French defence technology, Japanese consumer goods, American beverages. This is not a portfolio that resembles any market-cap-weighted index. The geographic and sector diversity reflects the moat filter’s sector-agnostic application: competitive advantages exist across industries, not only in technology.

The reconstitution dynamic is worth understanding for long-term holders:

The economic moat concept extends well beyond ETF selection. It is a fundamental business analysis lens that retail investors can apply when evaluating any company, domestic or international.

Morningstar deploys more than 100 equity analysts using forward-looking fundamental research to assess moat classifications, a level of analytical resource that distinguishes this approach from quantitative screening.

Commentary from Motley Fool Australia in December 2025 highlighted wide moat strategies, including GOAT, as well-suited to long-term retail investors seeking international exposure, precisely because the moat framework rewards patience rather than timing.

An honest limitation deserves acknowledgement. Moat investing can underperform in momentum-driven market environments where valuation discipline causes a strategy to miss expensive rallies. GOAT’s 3Y annualised return of 5.56% reflects this characteristic. For context, VanEck’s related US-focused moat ETF (MOAT) is YTD -1.91% as of 8 May 2026, while the global variant (MOTG) is YTD +1.49%, illustrating that moat strategy returns vary meaningfully by geographic exposure. Neither figure invalidates the framework; both reflect the interaction between moat quality, valuation entry points, and regional market conditions.

The transferable insight is this: investors who learn to identify moat sources (brand, scale, switching costs, IP, network effects) and layer valuation awareness on top possess a mental model that applies to any equity analysis, not just GOAT’s holdings.

For investors who want to see how Morningstar’s moat classifications play out in the Australian domestic market, our deep-dive into ASX network-effect moats examines how platforms like Seek and REA Group hold participation-based advantages that proved resilient across Morningstar’s 2026 review of 132 companies, with Seek trading at a significant discount to its Morningstar fair value estimate despite positive AI-driven financial results.

The economic moat concept provides a durable analytical framework for identifying businesses worth owning for decades. GOAT operationalises that framework for ASX investors through a dual filter of competitive advantage and valuation discipline, producing a concentrated, analyst-driven 67-stock portfolio that looks nothing like a broad international index.

The trade-offs are real. GOAT carries a higher MER (0.55%) and smaller AUM (A$55.5 million) than QLTY, and its valuation screen has produced lower returns over recent periods when expensive quality stocks continued to re-rate. Each of these characteristics has a philosophically coherent basis: concentration reflects selectivity, the fee reflects analyst input, and underperformance reflects price discipline.

ETF fee compounding over a 30-year horizon can convert a seemingly modest management expense ratio difference into a six-figure terminal wealth divergence, which is why GOAT’s 0.55% MER deserves honest scrutiny relative to QLTY’s 0.35%, even when the higher fee reflects genuine analyst input rather than administrative overhead.

In markets where valuations are stretched and competitive advantages can erode quickly, the combination of moat depth and price discipline is the kind of structural logic that tends to reward patient investors over full market cycles.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Investors considering GOAT should review the current VanEck product disclosure statement (PDS) and compare the fund’s live holdings and return data on the VanEck Australia website before investing, as holdings and performance figures reflect data as at 31 March 2026 and will have changed.

ASIC Regulatory Guide 168 sets out the disclosure obligations that govern product disclosure statements for ASX-listed ETFs, including the content standards that issuers such as VanEck must satisfy when describing fund methodology, fees, and risk factors to retail investors.

ASX: GOAT is an ETF issued by VanEck Australia that tracks a Morningstar index of wide moat companies trading at attractive valuations, giving investors access to 67 international businesses with competitive advantages expected to last 20 years or more.

Morningstar defines a wide moat as a competitive advantage expected to persist for 20 years or more, based on forward-looking research from over 100 equity analysts who assess five sources: brand strength, cost advantages, switching costs, intellectual property, and network effects.

GOAT uses a dual filter requiring both a wide moat classification and an attractive valuation relative to Morningstar's fair value estimate, while QLTY applies a quantitative quality screen based on return on equity, earnings stability, and low leverage with no explicit valuation screen, which contributed to QLTY's stronger recent returns during the US technology re-rating cycle.

GOAT charges a management expense ratio of 0.55% per annum, holds 67 companies across developed international markets excluding Australia, and had approximately A$55.5 million in assets under management as at 31 March 2026.

GOAT's valuation discipline caused it to underweight expensive US technology stocks during a period when those stocks continued to re-rate higher, whereas QLTY's quantitative quality screen has no price filter and therefore captured more of that momentum-driven rally.