Starbucks Builds AI Tools to Drop Microsoft, IBM and Oracle Apps

2 hrs ago

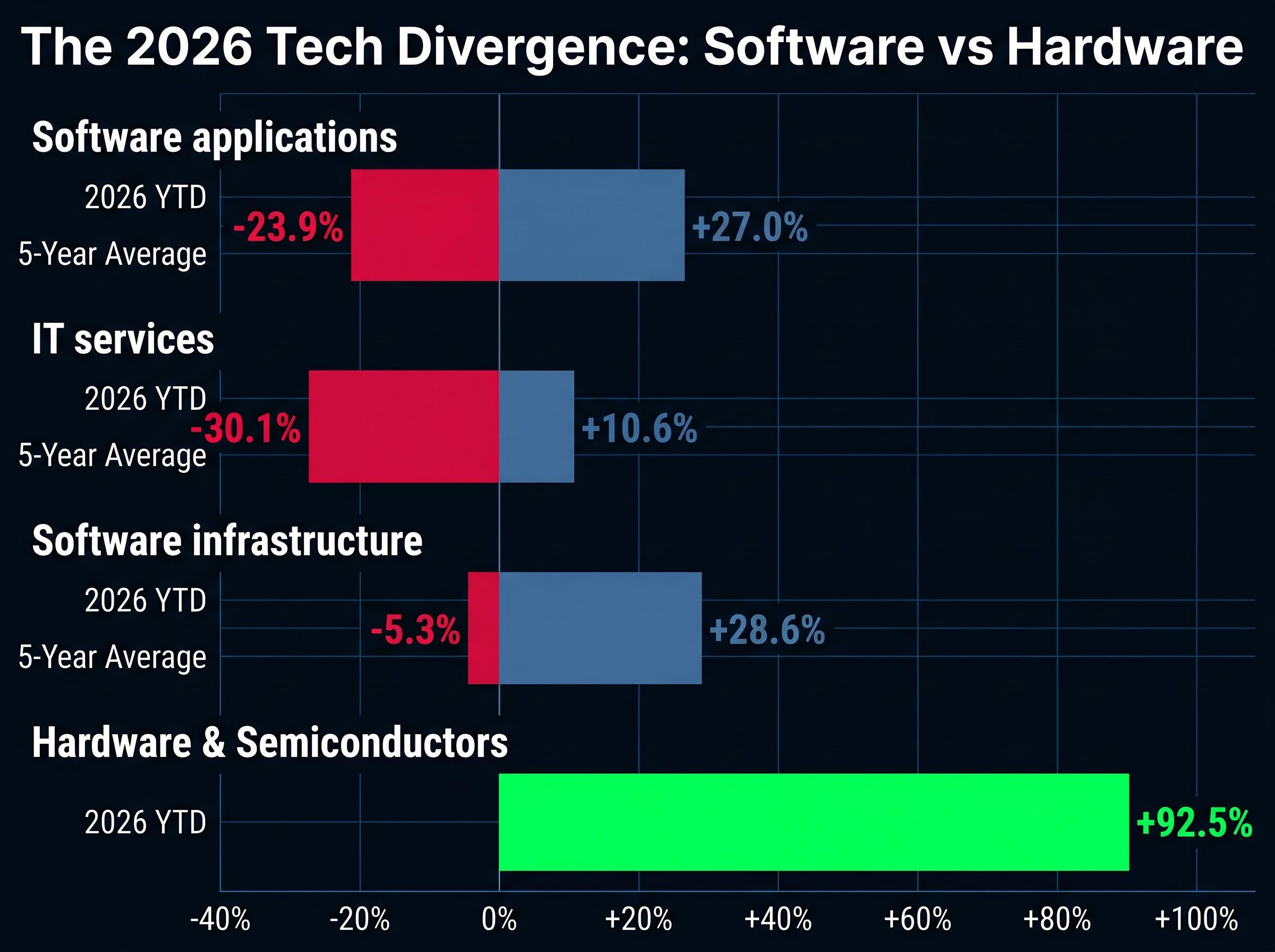

More than 75% of software application and infrastructure companies in the Morningstar US Technology Index are in negative territory year-to-date in 2026. Hardware and semiconductor stocks, by contrast, are up an average of 92.5% over the same period. That 133-percentage-point spread between technology’s winners and losers is the widest on record.

The software stocks selloff is not random noise. It reflects a specific investor thesis: that artificial intelligence will displace traditional software business models before those companies can adapt. AI coding tools, autonomous agents, and AI-native platforms are repricing the market’s expectations for legacy software revenue, and the result has been the most concentrated destruction of software equity value since 2022.

The question facing investors is whether that thesis is being priced accurately or dramatically overpriced. What follows examines the data behind the decline, the strongest evidence on each side of the debate, and the analytical framework needed to separate genuine value from a value trap.

The numbers are stark, and they predate any single catalyst. The weakness began in Q4 2025, making this a multi-quarter decline rather than a reaction to one event.

Software application stocks have fallen an average of 23.9% year-to-date in 2026, according to Morningstar data as of 11 May 2026. Over the prior five years, the same cohort averaged annual gains of 27%. IT services stocks have fared worse: down 30.1% year-to-date against a five-year average gain of 10.6%. Even software infrastructure, the most resilient sub-sector, is down 5.3% versus a five-year average of 28.6%.

| Sub-sector | 2026 YTD return | Five-year average return |

|---|---|---|

| Software applications | -23.9% | +27.0% |

| IT services | -30.1% | +10.6% |

| Software infrastructure | -5.3% | +28.6% |

The individual-stock declines are sharper still. As of 12 May 2026, Morningstar data shows:

The bottom decile of technology stocks has posted an average decline of 39.3% year-to-date, the worst result for that cohort since 2022, when the same group fell 63.7%.

This is not a routine pullback. The magnitude, breadth, and duration place it among the most severe software drawdowns in recent market history.

The scale of the shift becomes clearer when viewed alongside the broader capital reallocation: the legacy software repricing that began in early 2026 erased an estimated $2 trillion in US software market value while simultaneously triggering $1.2 trillion in M&A activity, as incumbents rushed to acquire AI capabilities they could not build fast enough organically.

The bear case rests on a specific and internally coherent thesis. AI coding tools, autonomous software agents, and AI-native platforms threaten to reduce enterprise demand for legacy software workflows and the seat-based licensing models that underpin them. If an AI agent can perform tasks that previously required a Salesforce subscription or an Adobe Creative Cloud licence, the addressable market for those products contracts permanently.

Credentialed analysts are acting on this thesis, not merely discussing it. In April 2026, Morningstar downgraded the economic moats of three major software franchises:

Morningstar’s moat downgrade rationale covers the specific fair value estimate reductions applied to Adobe, Salesforce, and ServiceNow, with each company’s wide moat rating revised to narrow on the basis that generative AI is eroding the switching costs and pricing power that previously justified premium valuations.

The performance gap between software and hardware reinforces the directional verdict. Approximately 7% of computer hardware and semiconductor stocks are negative year-to-date, compared to more than 75% of software names. Investors are not leaving technology; they are rotating within it, and the rotation has a clear thesis behind it.

AI displacement is not the only pressure. Forrester’s 2026 predictions document an environment of tighter enterprise technology budgets and elevated volatility for technology leaders, with demand concentrated on investments that deliver measurable return on investment.

This budget scrutiny affects software companies regardless of direct AI exposure. Even platforms not immediately threatened by AI substitution face procurement headwinds when enterprise buyers demand demonstrable returns before renewing or expanding contracts. The result is a compounding effect: AI fears drive multiple compression at the same time that spending caution slows revenue growth, making it difficult to isolate which factor is responsible for any single stock’s decline.

The dispersion within technology stocks tells a story the headline selloff numbers obscure.

As of 13 May 2026, the spread between the top and bottom deciles of Morningstar’s US technology stock universe stands at approximately 133 percentage points, according to Morningstar’s Dave Sekera. The top decile has returned an average of 93.3% year-to-date. The bottom decile has returned an average of negative 39.3%. That gap is the widest in the recorded dataset, roughly double the dispersion observed three years earlier.

Dispersion of this magnitude (the gap between the best and worst performers within a single sector) is a signal that investors are making sharp distinctions within technology rather than selling the sector broadly. Capital has migrated from software toward hardware and semiconductors, and it has done so with conviction.

The hardware and software divergence inside US technology in 2026 has produced a spread of more than 70 percentage points between the best and worst industry groups, with SanDisk alone returning more than 348% year-to-date on an AI-induced NAND flash memory squeeze that illustrates how precisely capital has repriced AI infrastructure beneficiaries relative to legacy incumbents.

Morningstar’s Dave Sekera has characterised the 133-percentage-point spread between the top and bottom deciles as the widest on record, reflecting a market that is repricing software risk while simultaneously bidding up AI infrastructure beneficiaries.

Historical context for the bottom decile helps calibrate where 2026 ranks:

| Year | Bottom-decile average return |

|---|---|

| 2026 (YTD) | -39.3% |

| 2025 | -32.28% |

| 2024 | -22.38% |

| 2023 | -6.67% |

| 2022 | -63.72% |

| 2021 | -17.83% |

The 2026 bottom decile is the second-worst reading in six years, trailing only the broad technology rout of 2022. Hardware stocks, meanwhile, have averaged gains of 92.5% year-to-date versus a five-year average of 82.7%, suggesting hardware returns are elevated but not dramatically above their recent trend.

The implication: investors who understand the rotation dynamic can begin distinguishing between software stocks that are collateral damage in a sentiment-driven selloff and those facing genuine structural pressure on their business models.

Morningstar’s Dave Sekera has characterised the market’s reaction to software stocks as an overreaction, arguing that software companies are more likely to embed AI into their existing offerings than to be displaced by it entirely.

Sekera’s view, as articulated in April 2026 Morningstar commentary, is that the market has moved ahead of fundamentals for certain software names, and that the adaptation cycle has more time to play out than current valuations imply, with demand for AI infrastructure products projected to reach its peak around 2028.

Enterprise AI adoption is far less uniform than the market’s rotation thesis implies: an estimated 70-80% of AI pilots fail or stall at the proof-of-concept stage, with poor data integration as the primary cause, which means the software companies most exposed to displacement are those whose customers are also the least likely to have successfully deployed AI-native alternatives.

The strongest direct evidence for the adaptation thesis comes from Microsoft’s FY26 Q1 results, reported on 29 October 2025 for the quarter ended 30 September 2025:

Microsoft (MSFT) shares are still down 15.5% year-to-date despite those results, an illustration of how broadly the software sentiment selloff has swept even companies where AI is demonstrably additive to revenue.

Databricks has earned leader recognition from Gartner, Forrester, and IDC in data platforms and lakehouses during 2025-2026, reflecting growing enterprise demand for AI-integrated data infrastructure tools. The recognition pattern indicates that AI-native product positioning is attracting enterprise spend, not displacing it.

Mendix, a low-code platform, has received continued analyst validation from Gartner and Forrester as an accelerator in AI-transformed enterprise environments. The positioning frames AI as a tool that extends the platform’s capabilities rather than one that renders it obsolete.

Neither example carries the quantitative weight of Microsoft’s earnings data. Together, however, they suggest a pattern: software companies that position AI as a product feature rather than a competitive threat are finding traction with enterprise buyers.

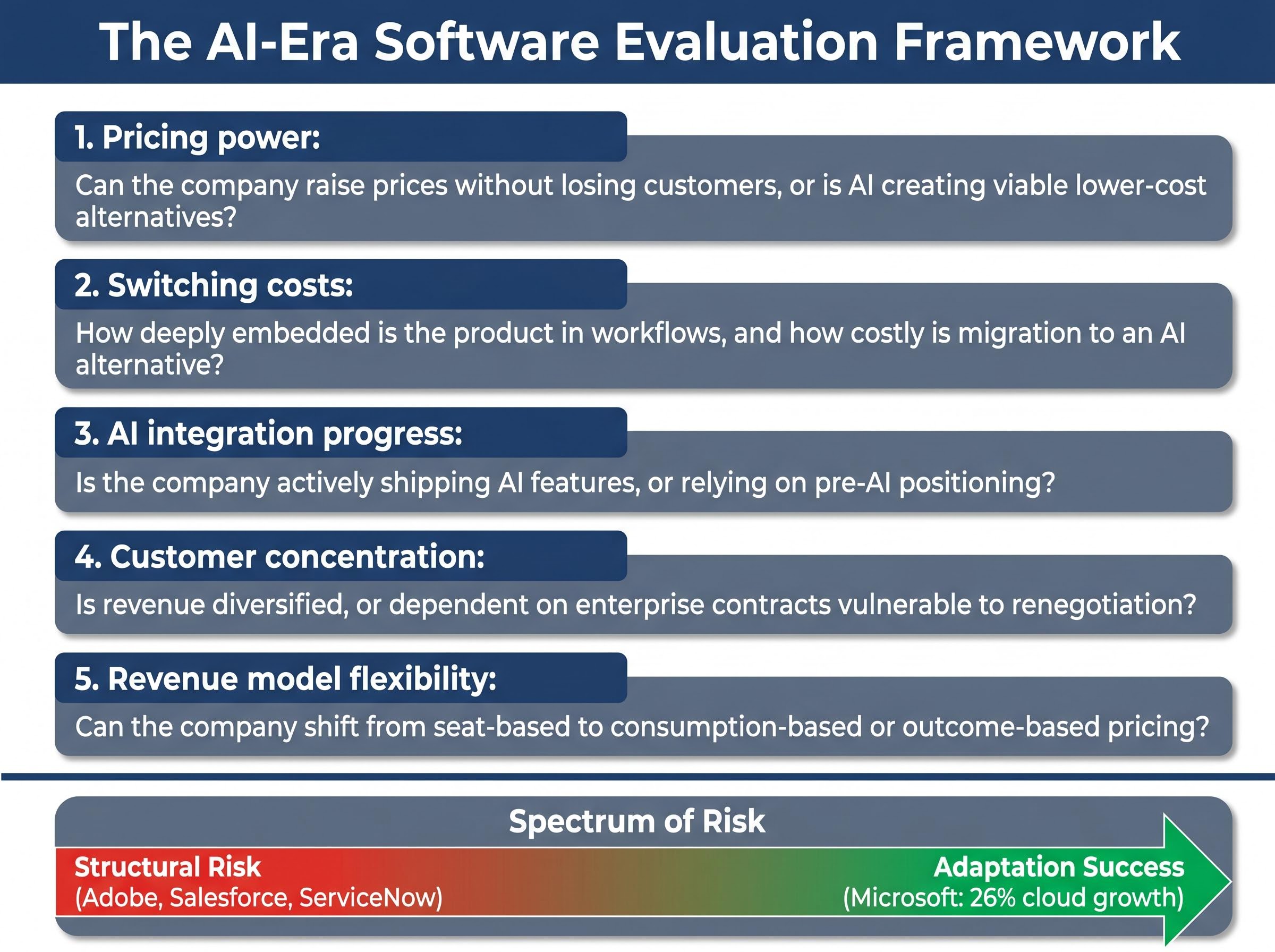

The analytical question is not whether to buy or avoid software as a category. Record dispersion within technology makes sector-level index exposure a blunt instrument. The question is which individual software companies possess moats durable enough to survive an AI-accelerated adaptation cycle.

Five variables distinguish software companies with defensible positions from those most exposed to structural disruption:

McKinsey’s analysis of AI-era software pricing shifts identifies consumption-based and outcome-based models as the structures most likely to survive the seat-licensing erosion that AI agents are accelerating, a finding that maps directly onto the revenue model flexibility variable that separates structurally resilient software companies from those most exposed to displacement.

Applying this framework produces different conclusions for different names. Adobe, Salesforce, and ServiceNow, with their Morningstar moat downgrades, sit on the identified-structural-risk side of the ledger. Microsoft, with 26% cloud revenue growth driven by AI, sits on the adaptation-success side. Most software companies fall somewhere between those poles, and that middle ground is where the selectivity test matters most.

Sekera has flagged a risk on the opposite side of the trade that may not be receiving sufficient attention. Commodity-oriented hardware companies face significant downside once AI infrastructure supply normalises, with demand for AI hardware projected to peak around 2028.

The recent hardware winners are striking: Sandisk up approximately 511.4%, Intel up more than 225%, Seagate up 194.2%, and Western Digital up 183.8% year-to-date. Those gains may carry as much mean-reversion risk on the upside as software stocks carry on the downside, and investors rotating out of software into hardware could be exchanging one timing risk for another.

The market is pricing AI disruption as if its effects will be uniform across software. The evidence from Microsoft, Databricks, and the broader adaptation cases suggests the outcome will be highly company-specific.

The 133-percentage-point spread between technology’s winners and losers is likely to persist through the AI infrastructure demand cycle. It is the defining feature of the 2026 technology investment environment, and it rewards company-level analysis while penalising passive sector exposure. For context, the current bottom-decile reading is the second-worst in six years, trailing only 2022’s broad rout.

US equity market concentration adds another layer of complexity to the selectivity argument: five companies now control roughly 30% of total US market capitalisation, a level with no historical precedent, which means passive index exposure to technology carries a structural mega-cap tilt that can obscure the company-specific analysis the current environment actually demands.

Morningstar’s assessment, as of May 2026, is that AI disruption fears are real but that pricing has moved ahead of demonstrated fundamental deterioration for certain software names, the clearest analyst verdict currently available on the selloff’s severity.

The orienting question for investors is not “should I buy software?” It is which specific software companies have the moat quality and AI integration progress to survive and benefit from this cycle, and which do not. That distinction is where returns will be made or lost.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results, and financial projections are subject to market conditions and various risk factors.

The selloff is driven by investor fears that AI coding tools, autonomous agents, and AI-native platforms will permanently reduce enterprise demand for legacy software and the seat-based licensing models that underpin them. Tighter enterprise technology budgets and Morningstar moat downgrades for Adobe, Salesforce, and ServiceNow have compounded the pressure.

Software application stocks are down an average of 23.9% year-to-date as of May 2026, and the bottom decile of technology stocks has fallen an average of 39.3%, making it the second-worst reading in six years and trailing only the broad technology rout of 2022, when the same group fell 63.7%.

According to Morningstar data as of 12 May 2026, the hardest-hit names include HubSpot down approximately 55.3%, Via Transportation down approximately 51.3%, Atlassian down 47.6%, Workday down 44.8%, SailPoint down 42.6%, and Zscaler down 35%.

Investors should assess five variables: pricing power, switching costs, AI integration progress, customer concentration, and revenue model flexibility, particularly whether a company can shift from seat-based to consumption-based or outcome-based pricing as AI changes how customers use software.

No, hardware and semiconductor stocks have moved sharply in the opposite direction, averaging gains of 92.5% year-to-date, creating a 133-percentage-point spread between technology's top and bottom deciles that Morningstar's Dave Sekera has described as the widest on record.