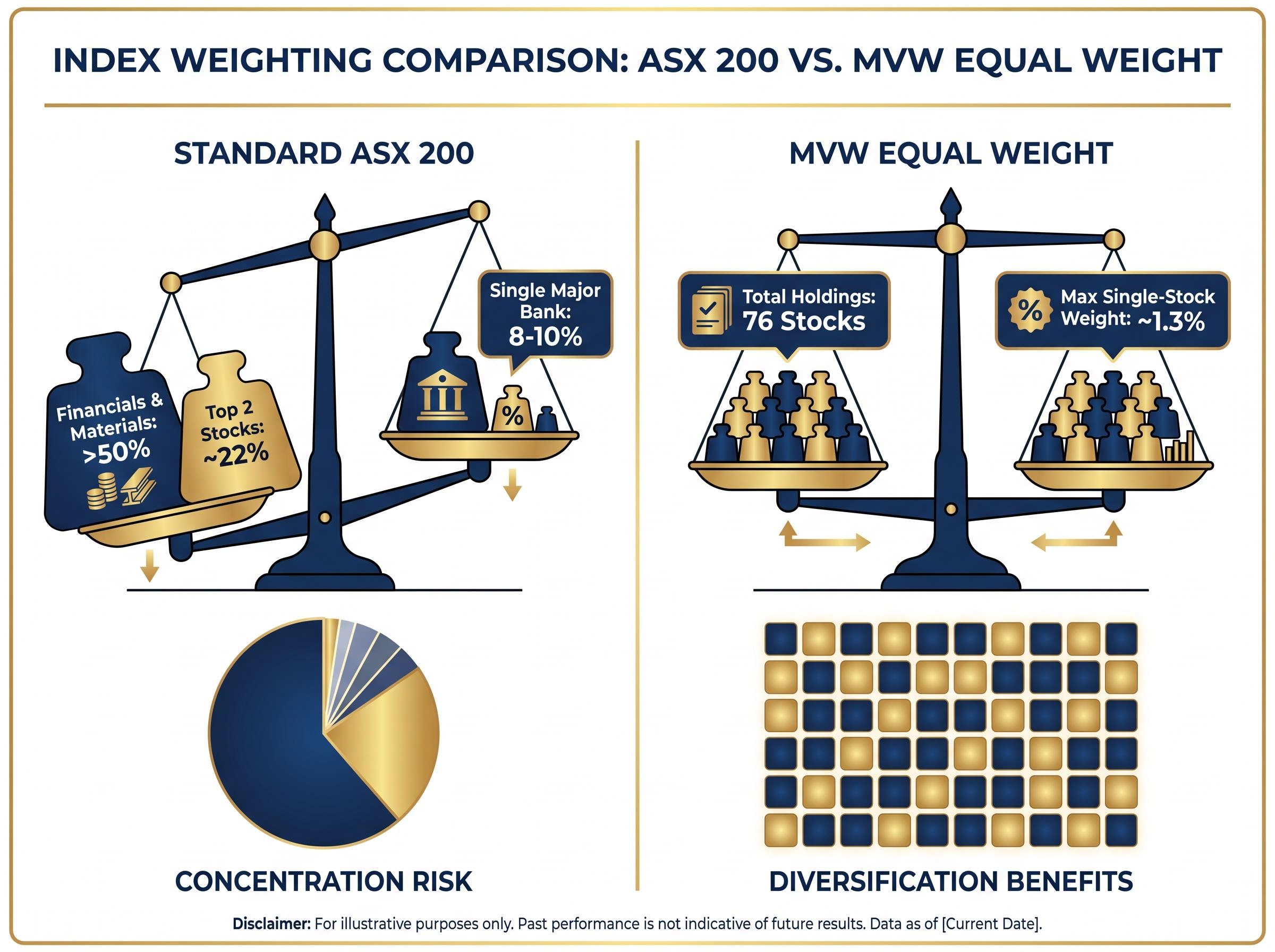

Australian investors who hold an ASX 200 index fund often assume they own a diversified slice of the market. The reality is less comfortable. Two sectors, Financials and Materials, account for more than half the index weight, and just two individual stocks represent roughly 22% of a typical market-cap-weighted portfolio, according to VanEck research. When Commonwealth Bank of Australia shed more than 10% following the May 2026 federal budget, holders of standard ASX 200 ETFs felt the damage directly, not because they owned CBA specifically, but because their “diversified” fund did. Three alternative ETFs attack this concentration problem through structurally different mechanisms: VanEck Australian Equal Weight ETF (MVW), BetaShares FTSE RAFI Australia 200 ETF (QOZ), and BetaShares Australian Ex-20 Portfolio Diversifier ETF (EX20). What follows is a comparison of how each redefines diversification, what risks each eliminates versus retains, and which portfolio situation each best suits.

Why your ASX 200 index fund may be less diversified than you think

Market-cap weighting sounds intuitive: a company’s weight in the index is proportional to its market value. The larger the company, the larger the slice it occupies. But in the Australian context, this mechanism produces a portfolio that leans heavily on a narrow band of mega-caps rather than distributing risk across the broader economy.

The concentration numbers tell the story:

- Two sectors (Financials and Materials) represent more than 50% of the market-cap-weighted Australian equity index

- Two individual stocks account for roughly 22% of a typical cap-weighted portfolio

- A single major bank can represent 8-10% of a standard ASX 200 index fund on its own

More than 50% of a market-cap-weighted Australian equity index sits in just two sectors: Financials and Materials, according to VanEck research.

The CBA post-budget decline of more than 10% in May 2026 illustrated the risk in practice. That loss did not affect only direct CBA shareholders. Every investor holding a standard ASX 200 index fund absorbed a meaningful drawdown from a single stock’s move, precisely because the index’s construction handed that stock an outsized weighting. The problem is not CBA itself. The problem is a weighting methodology that concentrates risk in whatever happens to be the largest company on any given day.

Single-stock concentration risk behaves differently depending on whether the exposure arrives through direct ownership or through an index fund: a 10% CBA position held directly is a deliberate choice, but the same effective weight embedded inside a market-cap ETF is invisible until a drawdown makes it visible.

When big ASX news breaks, our subscribers know first

What “smart beta” actually means for Australian investors

Smart beta is index-based investing that replaces market-cap weighting with a rules-based alternative weighting scheme. It is not active stock picking. A smart beta ETF still follows an index; it simply follows one that defines constituent weights differently from the standard approach.

The three methodologies covered in this article each represent a distinct lever for addressing the concentration problem:

- Equal weighting (MVW): Every stock in the portfolio receives the same weight, regardless of its market capitalisation, spreading risk evenly across all constituents

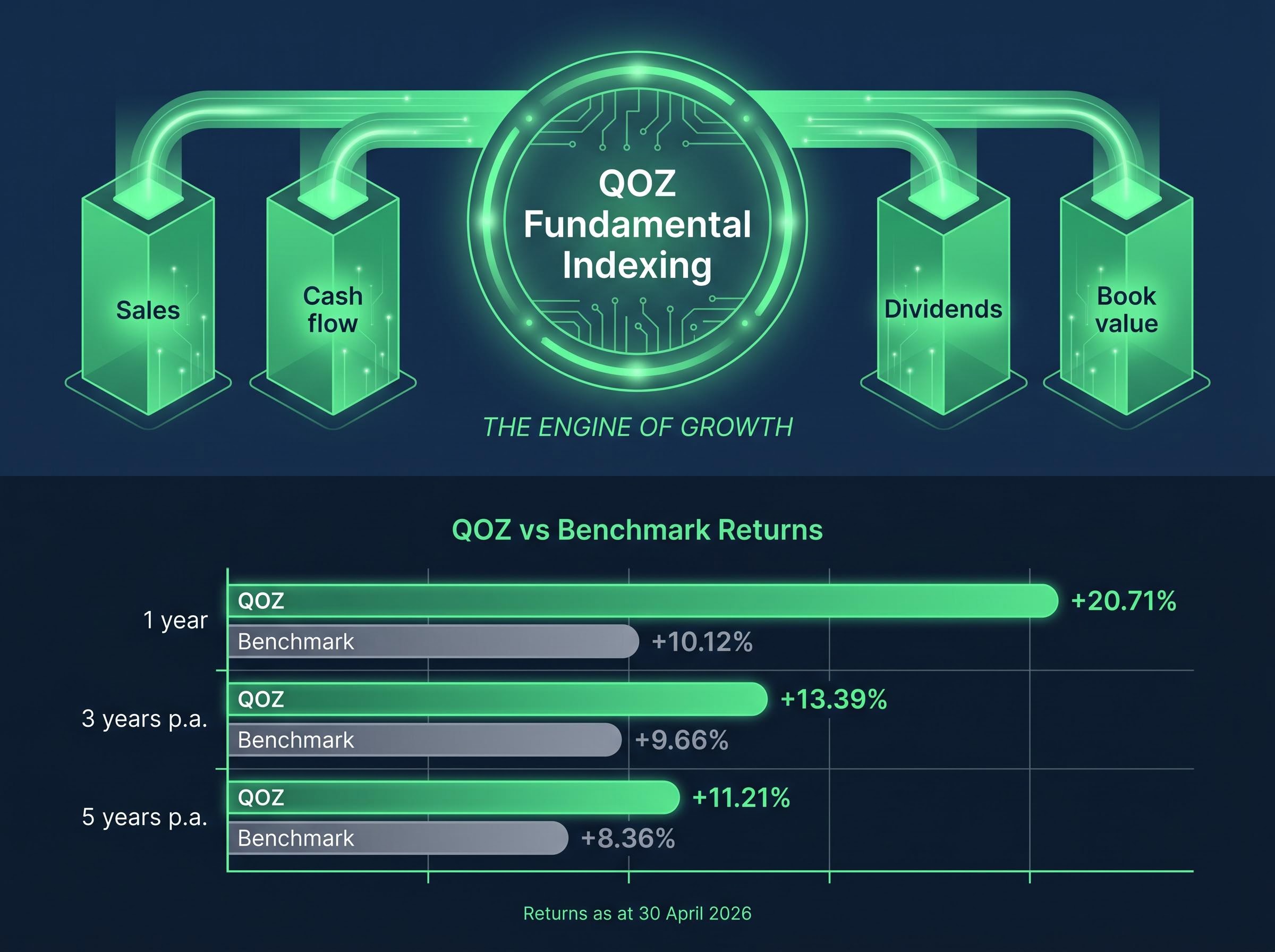

- Fundamental indexing (QOZ): Stocks are weighted by economic metrics (sales, cash flow, dividends, book value) rather than share price, tilting the portfolio toward companies with larger real-world economic footprints

- Deliberate large-cap exclusion (EX20): The top 20 stocks by market capitalisation are removed entirely, eliminating the source of concentration rather than reweighting around it

All three carry meaningful tracking error versus the standard ASX 200. Periods where they diverge from the headline benchmark, both outperforming and underperforming, are built into the design. That divergence is the mechanism, not a sign of failure.

US index fund concentration mirrors the Australian problem at an even more extreme scale: five mega-cap technology stocks controlled roughly 23% of the broad US market index as of mid-April 2026, a structural parallel that shows cap-weighted concentration is a global feature of market-cap indexing rather than a quirk of the Australian market.

The ASIC RG 282 guidance for ETF issuers sets out the disclosure and compliance obligations that govern how exchange-traded products listed on the ASX must report holdings, fees, and index methodology to retail investors, making it the regulatory framework underpinning the product disclosure statements for all three funds discussed here.

MVW: equal weighting spreads the risk across 76 stocks

MVW holds 76 ASX-listed stocks, each at approximately equal weight. The fund rebalances quarterly, resetting allocations so that no single stock exceeds roughly 1.3% of the portfolio at each rebalance date. Compare that to a standard ASX 200 index fund, where a single major bank can command 8-10%.

| Feature | MVW | Standard ASX 200 Index |

|---|---|---|

| Number of holdings | 76 | ~200 |

| Max single-stock weight | ~1.3% (at rebalance) | 8-10% (largest constituent) |

| MER | 0.35% p.a. | ~0.07-0.10% p.a. (typical) |

| Rebalancing frequency | Quarterly | As needed (market-cap driven) |

The fund had A$3.18 billion in funds under management as at 15 May 2026. Note that MVW performance figures require direct verification at the VanEck product page, as the most recent publicly available data could not be independently corroborated at the time of writing.

The trade-offs follow directly from the mechanism:

- Advantages: Reduced single-stock concentration, broader sector diversification, and a structural mid-cap and value tilt that gives greater representation to companies outside the mega-cap tier

- Disadvantages: Higher portfolio turnover from quarterly rebalancing, and meaningful tracking error against the ASX 200 when large caps lead the market; the fund will diverge most sharply precisely when the big banks and miners are performing strongest

MVW suits investors who want broad Australian equities exposure without mega-cap concentration, particularly those building model portfolios aimed at reducing bank and miner dominance.

QOZ: fundamental indexing weights companies by economic substance, not share price

QOZ tracks the FTSE RAFI Australia 200 Index, which weights companies using four fundamental factors:

- Sales

- Cash flow

- Dividends

- Book value

By anchoring weights to these economic metrics rather than share price, the methodology reduces the distortion caused by high-multiple growth stocks inflating their own index representation. In the Australian market, this produces a portfolio where Financials (32.3%) and Materials (26.7%) are the largest sectors (as at 30 April 2026), reflecting that Australia’s economically largest companies by fundamental output remain banks and miners, not growth technology firms.

The top 10 holdings as at 30 April 2026 were BHP, CBA, Westpac, NAB, ANZ, Woodside, Rio Tinto, Wesfarmers, Woolworths, and Telstra.

The performance data, reported by BetaShares as at 30 April 2026, is where the methodology’s impact becomes most visible:

| Period | QOZ Return | Benchmark Return |

|---|---|---|

| 1 year | +20.71% | +10.12% |

| 3 years p.a. | +13.39% | +9.66% |

| 5 years p.a. | +11.21% | +8.36% |

QOZ delivered +11.21% p.a. over five years to 30 April 2026, compared with +8.36% p.a. for the benchmark, a period that reflected a strong value and income environment.

Those returns demand context. The outperformance reflects a period where value, income, and quality factors were rewarded. Past performance does not guarantee future results. QOZ will underperform when growth and momentum stocks lead the market, and its “active-like” behaviour means it can look significantly different from the benchmark for extended periods.

The fund had A$1.14 billion in FUM as at 15 May 2026, with a management cost of 0.40% p.a. Investors considering QOZ are accepting a value tilt, not simply buying a better index.

Constructing an inflation-aware ETF portfolio adds another dimension to the fund selection decision covered here: in an environment where the RBA cash rate sits at 4.10% and annual CPI reached 4.6% in March 2026, the income and sector characteristics of a fund like QOZ, with its fundamental tilt toward cash flow and dividend-paying companies, carry different real-return implications than a purely equal-weighted structure.

EX20: cutting out the top 20 to solve concentration at its source

EX20 takes the most direct approach. The fund tracks the 180 largest ASX-listed companies after removing the top 20 by market capitalisation. There is no reweighting mechanism. The source of concentration is simply excluded.

The resulting portfolio is mid-to-large cap Australian equities with no exposure to the mega-bank and mega-miner tier. Representative holdings as at 30 April 2026 include:

- Fortescue

- Goodman Group

- Transurban

- QBE Insurance

- Scentre Group

- Coles Group

- Origin Energy

The sector profile (as at 30 April 2026) reflects this construction: Materials sits at 30.7%, Financials (excluding big-four banks) at 14.3%, Industrials at 11.9%, and Real Estate at approximately 11%. Materials remains the largest sector because significant mid-tier resources companies sit outside the top 20.

The fund had A$644 million in FUM as at 15 May 2026, with the lowest management cost of the three at 0.25% p.a. Performance to 30 April 2026: one-year +4.97%, three-year p.a. +6.61%, five-year p.a. +5.56%.

The trade-offs are the most explicit of the three:

- Ideal use cases: Investors who already hold direct ASX 20 positions (bank shares, BHP, Telstra) and want Australian equities exposure without doubling up; also useful as a satellite diversifier alongside a core ASX 200 holding

- Key risks: Greater mid-cap volatility from removing the market’s most liquid names; the fund is explicitly designed to underperform in periods when mega-cap resources and financials drive returns, as the five-year trailing return demonstrates

EX20 is the most specialist of the three products. It functions as a complement or satellite vehicle, not a replacement for core broad-market exposure.

Choosing between MVW, QOZ, and EX20: what each fund is actually solving for

The selection decision starts with the investor’s existing portfolio problem, not the product features:

- Reducing single-stock concentration within a diversified Australian equities holding: MVW spreads risk across 76 equally weighted names, directly diluting mega-cap dominance

- Gaining a value and income tilt within Australian equities: QOZ weights by fundamental economic metrics, producing a portfolio that favours companies with strong cash flows, dividends, and book value

- Avoiding doubling up on names already held directly: EX20 removes the top 20 entirely, serving investors who own CBA, BHP, or other mega-caps directly and want exposure to the rest of the market

| Fund | Strategy Type | MER | Best Suited For |

|---|---|---|---|

| MVW | Equal weight | 0.35% p.a. | Reducing mega-cap concentration |

| QOZ | Fundamental (RAFI) | 0.40% p.a. | Value and income tilt |

| EX20 | Ex-top-20 | 0.25% p.a. | Satellite diversifier; avoiding overlap with direct holdings |

FUM as at 15 May 2026: MVW A$3.18 billion, QOZ A$1.14 billion, EX20 A$644 million. All three carry meaningful tracking error versus the ASX 200, and investors must be comfortable with divergence from the headline benchmark as the cost of the diversification they are purchasing. Fee is one input among several; the methodology’s fit with the investor’s specific concentration problem matters more.

The diversification you choose depends on the concentration you are trying to escape

A standard ASX 200 index fund is not inherently well-diversified. It is market-cap-weighted, which in the Australian context means it is a concentrated bet on a handful of banks and miners wrapped in the language of broad market exposure. The alternative is not simply “any non-cap-weighted ETF” but the specific methodology that addresses the specific concentration problem present in the investor’s portfolio.

Readers considering any of these three funds should verify current data, including fees, performance, and holdings, directly on the issuer product pages before acting: VanEck MVW, BetaShares QOZ, BetaShares EX20. Fund metrics update continuously, and the figures cited in this article reflect specific reporting dates.

This article is for informational purposes only and should not be considered financial advice. Past performance does not guarantee future results. Investors should conduct their own research and consult with financial professionals before making investment decisions.