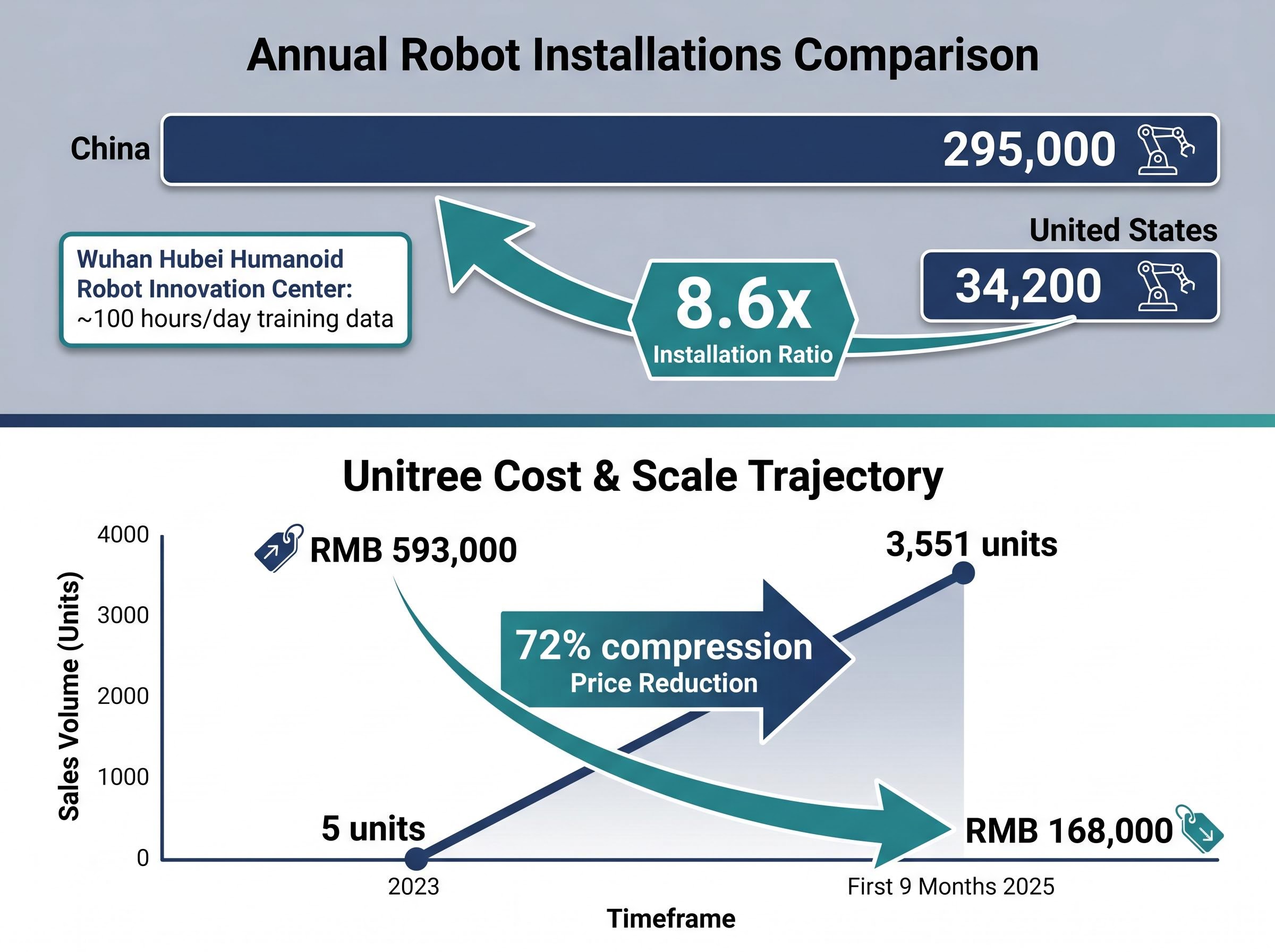

China installs 295,000 industrial robots per year. The United States installs 34,200. That ratio is not a manufacturing statistic. It is an AI training data advantage compounding in real time, and it sits at the centre of a structural problem that most US robotics stock assessments have not fully absorbed. A May 2026 report from Alpine Macro, authored by Chief Geopolitical Strategist Dan Alamariu, draws a hard line between what the US leads and what it does not control in the robotics supply chain. What follows is a breakdown of those findings, a mapping of specific supply-chain dependencies to investment risk categories, and an evaluation of whether NVIDIA’s simulation strategy represents a genuine structural offset or a workaround that leaves the core vulnerability intact.

Two separate contests: how the US-China robotics competition is actually structured

The Alpine Macro report reframes the US-China robotics competition not as a single race but as two separate contests running simultaneously. The first is the “brain layer”: semiconductor design, frontier AI model development, and high-fidelity simulation environments. The second is the “body layer”: physical manufacturing infrastructure, component supply-chain density, and deployment volume at scale.

The US leads the brain layer convincingly. NVIDIA’s simulation ecosystem, Qualcomm’s edge-AI platforms, and a deep bench of AI research institutions give American companies a measurable advantage in the intelligence that makes robots think. China leads the body layer with equal conviction. Beijing’s 15th Five-Year Plan explicitly names embodied intelligence as a national development priority, and billions of dollars have been directed into specialised robotics and embodied AI development funds.

The investment problem is that winning one contest does not guarantee winning the other.

The structural fault lines in US-China technology competition extend well beyond robotics: chip export controls grounded in national-security law carry bipartisan Congressional backing that places them outside the jurisdiction of trade negotiators, meaning diplomatic progress at the summit level leaves the deeper contest over semiconductor and AI supply chains largely untouched.

- Brain layer (US leads): Frontier AI chip design, high-fidelity simulation, reinforcement-learning model development

- Body layer (China leads): Manufacturing infrastructure, rare earth and permanent magnet supply, deployment volume generating real-world training data

- Why they matter independently: Brain-layer advantages drive semiconductor and software valuations; body-layer dependencies constrain hardware-intensive robotics plays through component sourcing risk and data disadvantage

Why the split matters for portfolio construction

Brain-layer leadership supports conviction in US semiconductor and simulation software positions. Body-layer dependency, however, introduces a category of risk that standard equity analysis frameworks do not typically surface. The two layers are not symmetrically substitutable: software advantages cannot directly replace missing physical components. An investor evaluating US robotics exposure through a pure AI-chip or software lens is assessing only half the competitive picture.

AI hardware capital expenditure concentration adds a second layer of risk for investors holding US robotics and semiconductor positions: hyperscalers have committed $635 billion to $700 billion in FY2026 infrastructure spending, and if escalating inference costs make generative AI applications structurally unprofitable, the deceleration in capital deployment would remove the demand backstop that currently underpins semiconductor valuations across the sector.

When big ASX news breaks, our subscribers know first

China’s deployment machine: the embodied AI data gap that simulation cannot easily replicate

The scale numbers deserve a moment to settle. According to the International Federation of Robotics, China installed 295,000 industrial robots in a single year. The United States installed 34,200. That is an 8.6x ratio, and every unit deployed generates operational hours that feed back into physical AI learning curves.

The IFR World Robotics 2025 data, released in September 2025, provides the primary industry benchmark for global installation volumes, confirming China’s 295,000 annual installations and setting the quantitative baseline against which the US figure of 34,200 is measured.

The mechanism is direct. The Wuhan Hubei Humanoid Robot Innovation Center produces approximately 100 hours of usable embodied training data per day. That is institutional-scale data generation running continuously, funded by state capital, with no commercial return threshold to meet. No equivalent US facility operates at comparable volume.

The cost trajectory compounds the problem. Unitree, a Chinese robotics manufacturer, sold 5 units in 2023. Across the first nine months of 2025, it sold 3,551 units.

Unitree’s average unit price declined from approximately RMB 593,000 to RMB 168,000 over the same period, a 72% compression that reflects manufacturing density translating directly into cost advantage.

| Metric | China | United States |

|---|---|---|

| Annual robot installations | 295,000 | 34,200 |

| State-funded training infrastructure | Present (e.g., Wuhan centre: ~100 hrs/day) | No equivalent identified |

| Example unit cost trajectory | Unitree: RMB 593,000 → RMB 168,000 | No comparable public data |

The cycle is self-reinforcing. More robots deployed means more training data generated, which produces better models, which drives further deployment and cost compression. For US robotics investors, this represents a durable competitive headwind rather than a temporary lag.

How China’s component grip translates into tangible risk for US robotics hardware

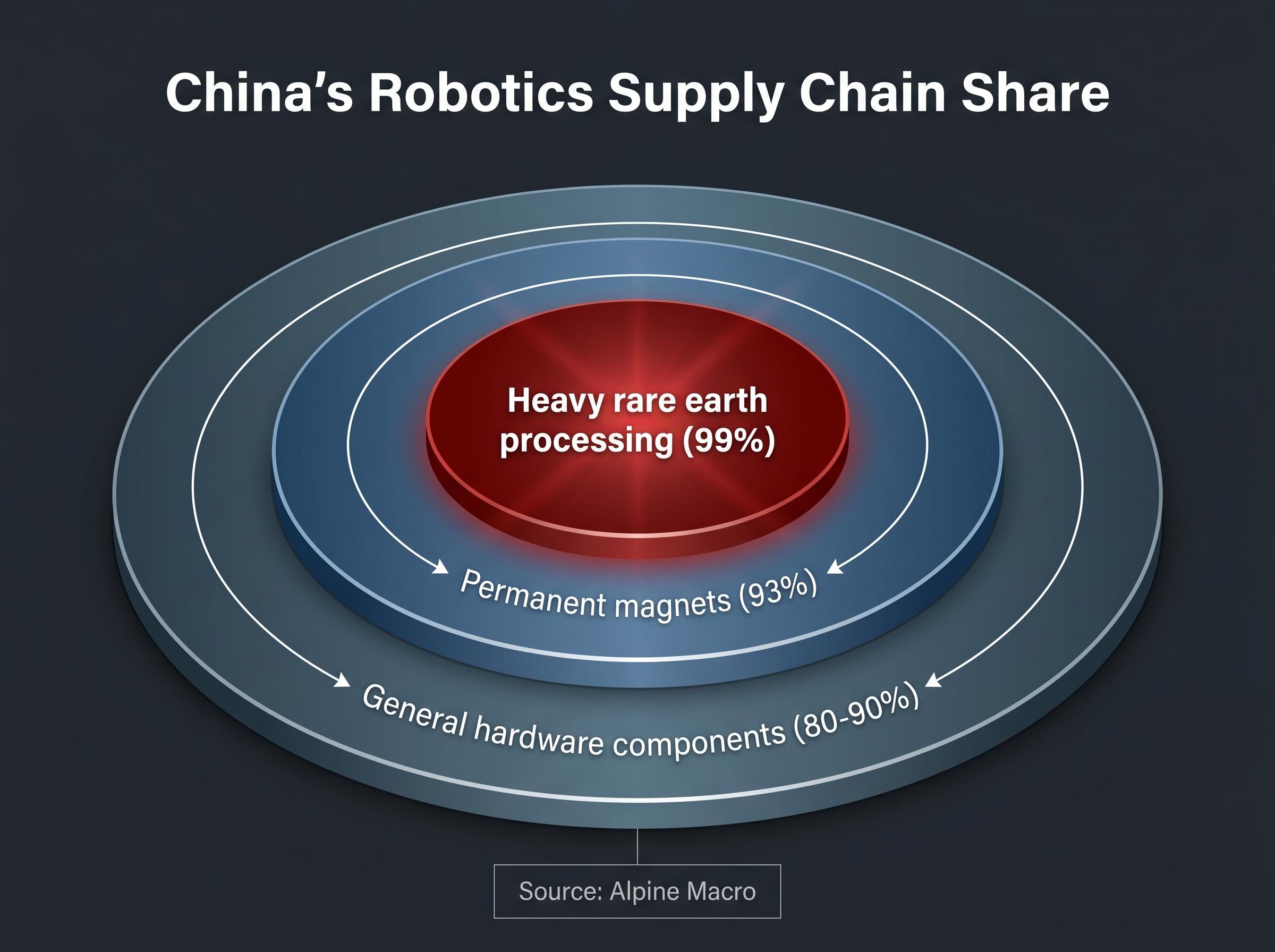

Supply-chain dependency is an abstract phrase until the specific components are named. According to the Alpine Macro report, China supplies an estimated 80-90% of the hardware components used globally in robotics. That figure alone carries weight, but two sub-categories sharpen the risk further.

- General hardware components (80-90%): Sensors, actuators, structural elements, and electronic assemblies that form the physical architecture of robotic systems

- Permanent magnets (93%): China controls an estimated 93% of the global permanent magnet market; these magnets are the core components in robotic actuator systems that convert electrical signals into physical movement

- Heavy rare earth processing (99%): China manages approximately 99% of heavy rare earth element processing, required for the high-strength motors that give robots precision and torque

China’s estimated 99% share of heavy rare earth element processing represents the single most concentrated supply-chain dependency in the entire robotics stack.

These are not hypothetical exposure points. The US Department of Defence issued a Request for Information on rare earth permanent magnet supply chains in January 2025, signalling that policymakers themselves regard the dependency as material.

The DoD rare earth metallization RFI, published through the Office of the Under Secretary of Defense for Acquisition and Sustainment, explicitly frames the conversion of rare earth oxides into metals and alloys as a national security priority, confirming that policymakers regard the permanent magnet dependency as a material vulnerability rather than a theoretical one.

The legislative response: real progress or long runway?

In February 2026, Representatives Tokuda and Dunn introduced H.R. 7563, the Rare Earth Magnet Market Revitalization Act, which would prohibit imports of certain rare earth magnets from covered nations. As of May 2026, the bill remains unenacted. Defence Production Act Title III measures continue funding upstream projects, but no legislation comparable in scale to the CHIPS and Science Act has been passed for magnets or rare earths.

MP Materials and Lynas Rare Earths have received DoD support as allied-nation alternatives. The diversification activity, however, remains concentrated at the mining and refining level. No named US robotics OEM has publicly announced non-Chinese permanent magnet sourcing for its robotic systems through mid-2026. The gap between legislative intent and enacted policy implies that this vulnerability persists as priced-in risk for the foreseeable investment horizon.

NVIDIA’s simulation strategy: genuine offset or partial workaround?

NVIDIA has built the most comprehensive simulation ecosystem available to US robotics developers. The capability is real, and it merits detailed examination before any verdict on the US position.

- Isaac Sim (built on Omniverse): Enables photorealistic, physically accurate simulation for training and testing industrial robots, with emphasis on synthetic data generation for computer-vision models and reinforcement-learning-based control policies

- Omniverse: The underlying platform providing real-time collaboration, physics simulation, and digital-twin creation across robotics workflows

- Cosmos: A foundation model integrating with robotics workflows, focused on multi-modal capabilities and digital twins that extend simulation into world-model territory

At GTC 2025, NVIDIA positioned synthetic data generation as central to its robotics strategy. The logic is sound: if real-world deployment data is scarce, generate training signal synthetically at scale. This is a genuine strategic asset, not a superficial marketing claim.

NVIDIA’s China revenue position illustrates the layered nature of the brain-layer advantage: market share fell from approximately 95% before export controls to near zero by FY2026 Q1, with domestic rivals including Huawei Ascend capturing an estimated 70-80% of China’s AI accelerator market, a dynamic that limits NVIDIA’s ability to monetise its simulation ecosystem directly inside the world’s largest robotics deployment economy.

The embodied parity question

The unresolved tension sits here: simulation can generate volume and diversity of synthetic scenarios, but 295,000 robots operating in real factories produce sensor-level physical data (environmental noise, material variance, mechanical wear patterns) that simulation environments approximate probabilistically rather than reproduce identically.

No NVIDIA executive has publicly framed the simulation ecosystem as a direct counter to China’s deployment-scale data advantage. The capability is positioned forward rather than geopolitically. More importantly, no benchmark currently exists comparing robotics model performance when trained on synthetic-only data versus real-world-plus-synthetic datasets at scale. That benchmark, when it arrives, will be the data point that clarifies whether the simulation offset thesis holds or whether the embodied data gap remains structurally significant.

What the structural gap means for investors in US robotics plays today

The preceding analysis produces a differentiated risk framework rather than a uniform signal. Not all US robotics exposure carries the same vulnerability profile.

| Investment Category | Brain-Layer Exposure | Body-Layer Exposure | Key Risk Variable |

|---|---|---|---|

| US semiconductor / simulation plays | High | Low | Synthetic vs. embodied data parity |

| Broad robotics ETFs (e.g., BOTZ) | Mixed | Mixed | Undifferentiated brain/body bundling |

| Hardware-intensive robotics manufacturers | Low | High | Component sourcing concentration |

| Allied-nation supply-chain plays | Low | Moderate | Legislative timeline and contract flow |

The Global X Robotics and AI ETF (BOTZ), with AUM of approximately $3.79 billion as of May 2026, bundles significant Japanese and European holdings alongside US positions. Broad robotics ETFs may blend brain-layer and body-layer exposure without differentiating between their structural risk profiles. All major named US humanoid robotics companies (Boston Dynamics, Apptronik, Figure AI, Sarcos) remain private as of May 2026, meaning direct public-market exposure to humanoid robotics runs primarily through semiconductor and ETF vehicles.

AI chip valuation frameworks that disaggregate GPU flywheel economics from custom ASIC contract models reveal why NVIDIA at approximately 24x forward earnings and Broadcom at 37x reflect meaningfully different risk profiles even within the same brain-layer exposure category, a distinction that becomes material when pricing in the simulation offset thesis and its dependence on continued NVIDIA market access.

Three risk categories warrant separate pricing:

- Component sourcing risk: Concentration of permanent magnet and rare earth supply in a single nation

- Deployment-scale data disadvantage: The self-reinforcing cycle of real-world training data accumulation favouring the larger installed base

- Legislative remediation timeline: The years-long gap between policy awareness and enacted supply-chain legislation

A durable asymmetry priced in for years, not quarters

The Alpine Macro report, published 12 May 2026, frames this as a structural condition rather than a cyclical one. Dan Alamariu’s analysis positions state capitalism as what he views as a prerequisite for competing in the embodied AI race, a framing that implies market forces alone will not close the body-layer gap on a short timeline.

Alamariu’s Alpine Macro analysis frames state capitalism as a prerequisite for winning the embodied AI competition, suggesting the deployment and component gaps are not market-correctable on a short investment horizon.

The policy response confirms the timeline. H.R. 7563 was introduced in February 2026 and remains unenacted. No rare earth or magnet legislation has matched the scale of the CHIPS and Science Act. The 8.6x robot installation ratio continues to compound China’s training data advantage with each operational quarter.

Three forward-looking signals warrant monitoring:

- Legislative progress on H.R. 7563 or successor bills that could create a CHIPS-scale intervention for permanent magnets

- Public benchmarking of synthetic versus real-world robotics training data, which would clarify the simulation offset thesis

- Named US robotics OEM announcements on non-Chinese component sourcing, which would signal downstream diversification beyond the mining and refining level

Understanding this dynamic now, while the legislative runway remains long and the market has not fully repriced body-layer risk, is the window in which portfolio positioning adjustments carry the most value.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding legislative outcomes, simulation capabilities, and competitive dynamics are speculative and subject to change based on market developments and policy decisions.