Why FOS Capital’s $10M Order Book Is Not $10M in Revenue

42 mins ago

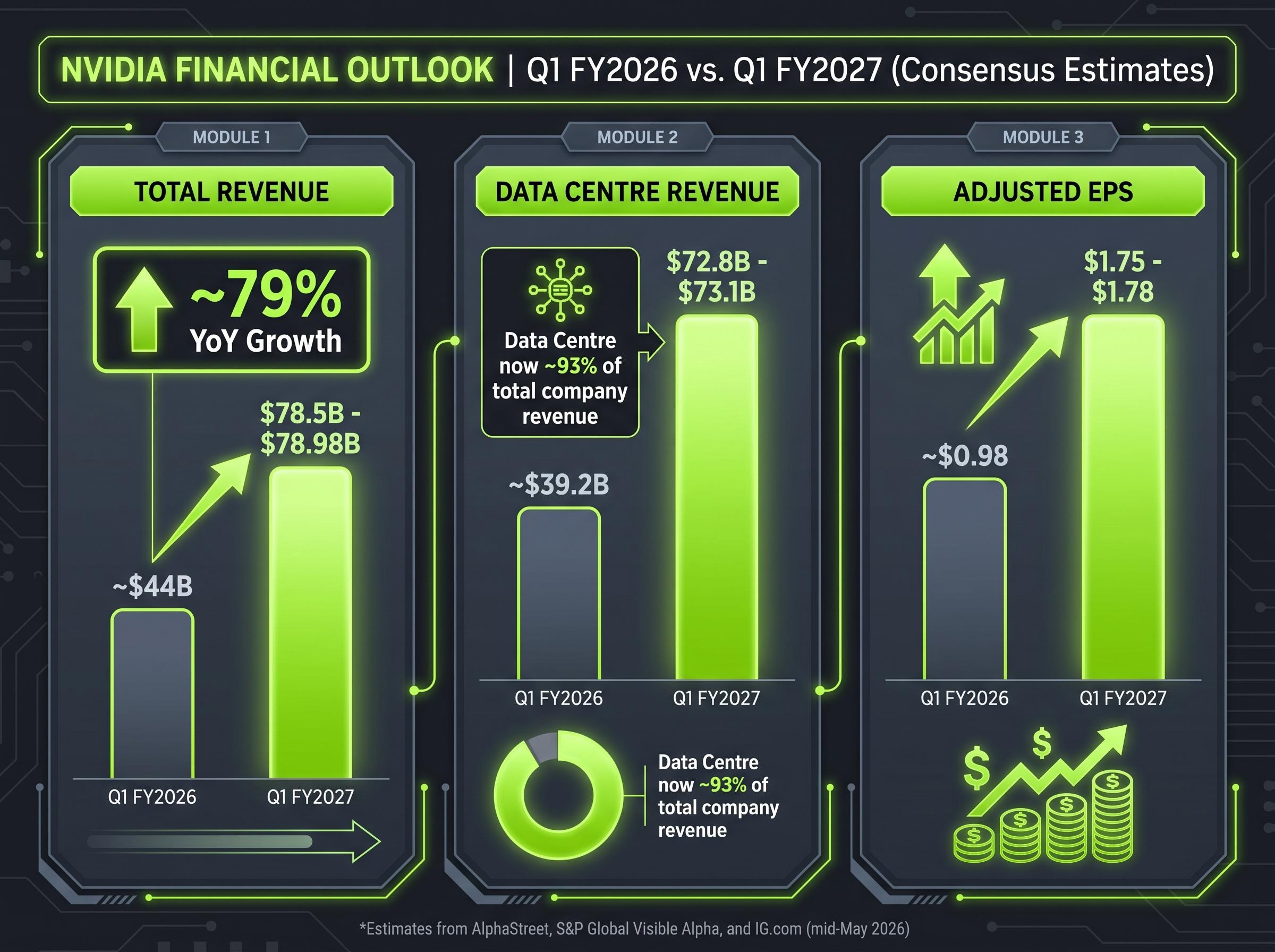

Nvidia enters its Q1 FY2027 earnings week having already climbed 36% from its March 2026 low and more than 1,800% since October 2022, making its upcoming results one of the most consequential data points in the current market cycle. The results, expected the week of 19 May 2026, arrive at a moment when AI infrastructure spending has become the central organising force in large-cap technology investing. Wall Street consensus calls for approximately $78.5 billion in quarterly revenue, with data centre alone expected to account for roughly $73 billion of that total. These are not incremental figures; they represent a 79% year-over-year revenue growth rate at a company already operating at hyperscale. At the same time, a stock pullback on 17 May and rising Treasury yields signal that investors are not writing the bull case without conditions. This analysis examines what Nvidia’s earnings are likely to reveal about AI infrastructure investment health, where the competitive risks are actually concentrated, and what the results will mean for the broader semiconductor sector.

The numbers that matter this week are specific, and they leave little room for ambiguity. Consensus revenue sits at $78.5-$78.98 billion, adjusted earnings per share at $1.75-$1.78, and data centre revenue at $72.8-$73.1 billion, according to estimates compiled by AlphaStreet, S&P Global Visible Alpha, and IG.com as of mid-May 2026.

| Metric | Consensus Estimate | Prior Year Comparison | Implied YoY Growth |

|---|---|---|---|

| Total Revenue | $78.5-$78.98B | ~$44B (Q1 FY2026) | ~79% |

| Adjusted EPS | $1.75-$1.78 | ~$0.98 (Q1 FY2026) | ~79-82% |

| Data Centre Revenue | $72.8-$73.1B | ~$39.2B (Q1 FY2026) | ~86% |

Data centre revenue alone now accounts for roughly 93% of the total company figure, illustrating how completely Nvidia’s financials track AI infrastructure spending.

79% year-over-year revenue growth at a company already generating nearly $80 billion per quarter is a remarkable achievement and an extraordinarily high bar. Even a modest shortfall at this scale carries outsize implications for sentiment.

That growth rate is both the bull case and the vulnerability. A beat confirms the AI infrastructure thesis. An in-line print may disappoint a market conditioned to expect upside surprises. A miss, even a narrow one, would force a reassessment of the demand trajectory at the precise moment valuations assume it continues.

The revenue estimates above do not exist in isolation. They sit on top of a capital expenditure cycle that has no modern precedent in technology infrastructure.

Combined 2026 hyperscaler capex guidance totals $600-$725 billion, representing 60-77% year-over-year growth across the four largest cloud infrastructure operators, according to data compiled by Yahoo Finance and the Financial Times through April and May 2026. The company-level commitments are substantial:

The current AI investment cycle has already surpassed every prior technology spending peak in US history, with IT hardware and software reaching 4.9% of GDP in Q1 2026, a figure that eclipses both the dot-com era peak of approximately 4.2% and the cloud buildout peak of approximately 3.8%, placing the current infrastructure buildout in genuinely uncharted macroeconomic territory.

This capex wave has not decelerated despite macroeconomic uncertainty and the emergence of more capital-efficient AI architectures, which is itself a signal worth noting. These are not speculative allocations; they are board-approved capital plans backed by balance sheets that can absorb them.

AI data centre builds are GPU-intensive by design. The compute layer of a modern AI training cluster requires thousands of high-end accelerators per facility, meaning capital committed to infrastructure converts to GPU procurement at scale. Data centre revenue at roughly $73 billion for a single quarter illustrates how tight the link has become between hyperscaler budgets and Nvidia’s income statement.

The near-term revenue visibility this provides is genuinely unusual by any historical measure. When the customers publicly commit to $600-$725 billion in annual spending and the primary bottleneck is GPU supply rather than demand, the order book writes itself, at least for the next several quarters.

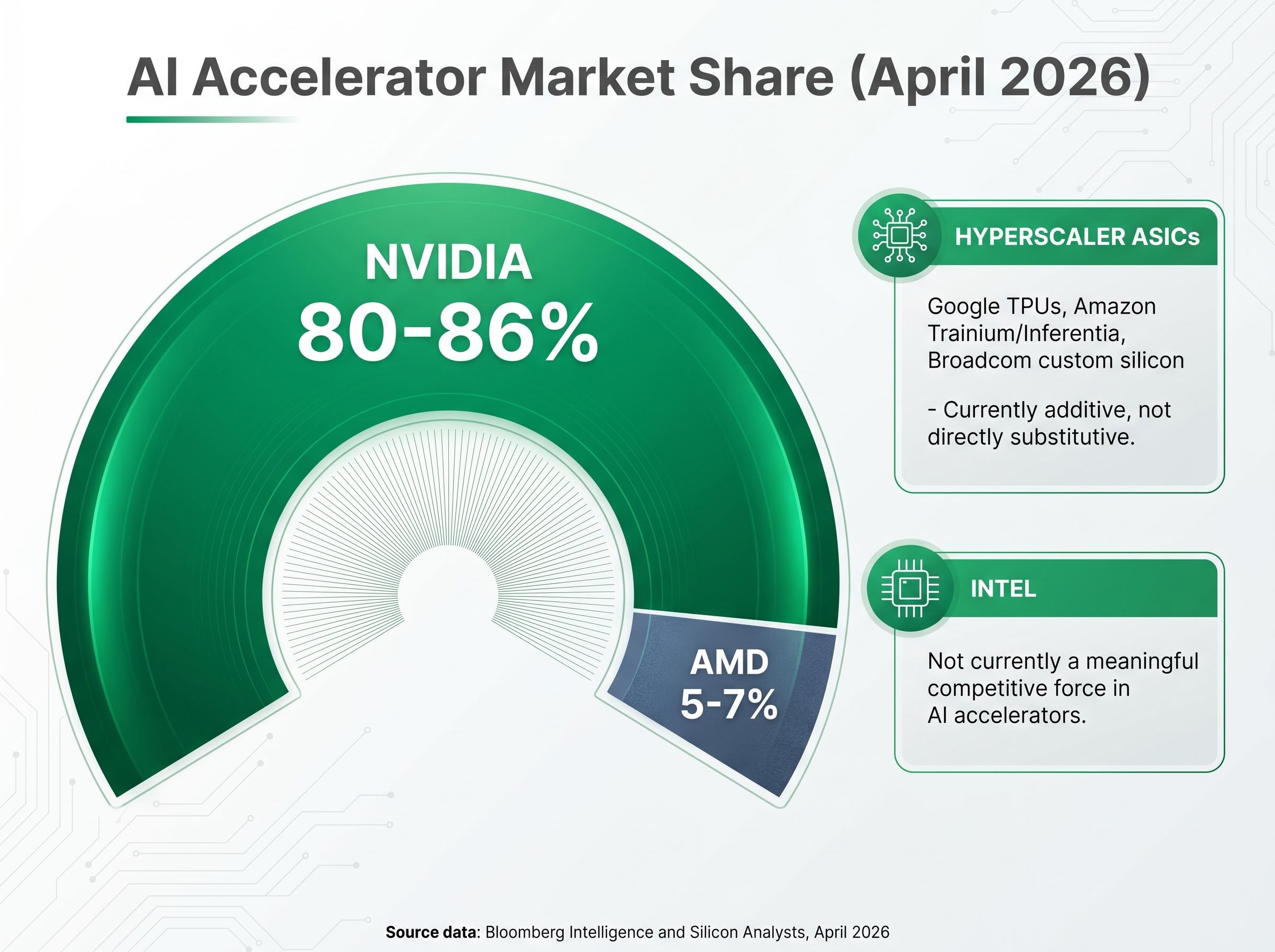

Nvidia holds approximately 80-86% of the AI accelerator market, according to Bloomberg Intelligence and Silicon Analysts data from April 2026. That dominance is the starting point for assessing competitive risk, not the conclusion.

80-86% market share in AI accelerators as of April 2026, with no analyst reports documenting large-scale erosion.

Three distinct competitive vectors warrant individual assessment:

No analyst reports as of mid-May 2026 document large-scale Nvidia GPU market share erosion. The competitive threat is real in trajectory but not yet in magnitude, and confusing the two produces either complacency or misplaced alarm.

For investors who want to act on the competitive landscape analysis rather than simply monitor it, our dedicated guide to Nvidia versus Broadcom positioning examines how the GPU flywheel and the custom ASIC contract model each generate AI infrastructure revenue, compares forward earnings multiples, and explains why the two companies frequently coexist within the same hyperscaler data centre rather than competing for the same procurement budget.

Not all risks carry equal weight at current valuations. The analytical task is distinguishing headwinds already reflected in analyst models from vulnerabilities the market has not fully absorbed.

A risk being “priced in” means analysts have adjusted revenue models to account for the impact, not that the stock price already reflects a worst-case scenario. Premium multiples price in future growth, so a known headwind that reduces that growth trajectory still carries downside even when it is not a surprise. The distinction matters: investors who treat “priced in” as “no longer relevant” misread how valuation compression works at the high end.

Nvidia’s earnings report this week functions as more than a company-specific event. It operates as a leading indicator for the semiconductor sector and for AI capital allocation broadly.

The Philadelphia SE Semiconductor Index has risen more than 60% from its March 2026 low, a surge partly anchored in expectations for Nvidia’s results. When the largest component of a sector index reports, the outcome reads through to the entire cohort. A beat from Nvidia confirms the AI infrastructure thesis for every semiconductor name exposed to data centre spending. A miss or cautious guidance deflates sentiment across the group.

Assessing AI bull market runway requires separating the demand evidence, which remains compelling at $130 billion in Q1 2026 hyperscaler spending alone, from the valuation evidence, where Arm Holdings trades at 85x forward P/E and the S&P 500 Shiller CAPE sits at its second-highest reading in 155 years of market data, a divergence that Paul Tudor Jones framed in May 2026 as a one-to-two year risk horizon rather than an immediate exit signal.

| Index / Stock | Gain from March 2026 Low | Additional Context |

|---|---|---|

| Nvidia (NVDA) | ~36% | Up 1,800%+ since October 2022 |

| Philadelphia SE Semiconductor Index | 60%+ | Broad sector rally anchored in AI capex expectations |

| S&P 500 | ~17% | Up over 8% year-to-date; rally breadth concerns persist |

The broader market context adds a layer of consequence. The S&P 500 is up approximately 17% from its March low and over 8% year-to-date as of mid-May 2026. Beneath those headline figures, rally breadth remains narrow.

According to LSEG data, approximately 20% of S&P 500 constituent stocks have outperformed the index since the 30 March trough. A rally carried by so few names makes Nvidia’s earnings particularly consequential for market health narratives.

That concentration means a disappointing result from Nvidia would not simply affect one stock. It would challenge the thesis underpinning the broader market advance.

The reported figures will matter. What management says about the future will matter more.

Three forward signals deserve close attention when results land:

Analyst 12-month price targets range from $245 to $320, with a consensus average of approximately $274. That $75 spread reflects a wide distribution of views on whether the current growth rate is sustainable. The earnings call will narrow that distribution in one direction.

Recent rating actions underscore the range of conviction. TD Cowen raised its target to $275 with a Buy rating. Wells Fargo moved to $315. Citi and Bernstein both maintain Buy ratings at $300, according to analyst notes compiled by TheStreet and Yahoo Finance. The 17 May pullback is a reminder that ahead of a binary event at this valuation, sentiment can pivot on a single data point.

The results will function as a verdict on whether AI infrastructure investment is still in its acceleration phase or beginning a more measured plateau, with implications reaching well beyond Nvidia’s own share price.

Nvidia’s Q1 FY2027 results will function simultaneously as a company-specific earnings event and as the most direct available read on the health of the AI infrastructure investment cycle. The analytical framework for interpreting them is now clear: consensus expectations set the bar at $78.5 billion in revenue; hyperscaler capex commitments of $600-$725 billion provide the demand backstory; competitive share remains above 80% but warrants monitoring; and the distinction between priced-in and unpriced risks determines which headlines should move an investment thesis and which should not.

How Nvidia’s management characterises demand sustainability, supply chain conditions, and geographic constraints will matter as much as the reported numbers themselves. The headline will arrive within days. The signal it carries will shape technology sector positioning for months.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Wall Street consensus estimates call for approximately $78.5-$78.98 billion in total revenue, adjusted earnings per share of $1.75-$1.78, and data centre revenue of $72.8-$73.1 billion, representing roughly 79% year-over-year revenue growth.

AI data centre builds are GPU-intensive, meaning the combined $600-$725 billion in 2026 capex guidance from the four largest cloud operators converts almost directly into GPU procurement, giving Nvidia unusual near-term revenue visibility.

Nvidia holds approximately 80-86% of the AI accelerator market as of April 2026, with AMD at roughly 5-7% and hyperscaler custom silicon growing but largely additive to total AI compute spend rather than directly substitutive.

The $5.5 billion charge related to U.S.-China export restrictions is considered a known, priced-in headwind, with analysts having already adjusted revenue models to exclude the affected segment; less-discussed risks include customer concentration and valuation compression from any guidance miss.

Because Nvidia is the largest component of the Philadelphia SE Semiconductor Index, which has risen more than 60% from its March 2026 low, a beat or miss from Nvidia reads through to sentiment across all semiconductor names exposed to data centre spending.