Why AI Disruption Risk Is Mispriced Across Financial Data Stocks

50 mins ago

ResMed reported US$1.431 billion in quarterly revenue on 30 April 2026, an 11% year-on-year increase. Non-GAAP diluted earnings per share came in at US$2.86, up 21% on the prior corresponding period. The business, by every operational measure available in its most recent results, continued to grow.

The share price tells a different story. RMD.AX closed at A$28.33 on 15 May 2026, down roughly 21.7% from its January 2025 highs. The gap between operating performance and market pricing is one of the more visible disconnects on the ASX, and it has produced a genuine, unsettled debate: is this a mispricing of a high-quality compounder, or has the market correctly identified a structural risk that the earnings have not yet absorbed?

What follows is not a buy recommendation. It is a structured framework covering what ResMed does, how it has grown, why the price fell, what the GLP-1 drug concern actually involves, and what the current valuation implies. Readers will leave with the analytical tools to form their own view.

Before assessing whether the sell-off is warranted, investors need a clear picture of what exactly is being discounted. ResMed operates across two distinct segments, each with its own growth profile and margin structure.

The core business designs and manufactures continuous positive airway pressure (CPAP) devices, masks, accessories, and non-invasive ventilators for patients with obstructive sleep apnoea (OSA) and other respiratory conditions. This segment has continued to gain market share following the Philips recall, which removed a major competitor’s devices from circulation. Devices have been growing at mid-single-digit rates year-on-year, while masks and accessories deliver high-single-digit growth.

Brightree and MatrixCare serve durable medical equipment (DME) providers and post-acute care coordination outside hospital settings. SaaS revenue has been growing at low-double-digit rates, reaching approximately US$135 million per quarter by Q3 FY2025, with the run-rate higher through FY2026.

The cloud-connected device ecosystem is the competitive moat that separates ResMed from pure hardware rivals. Data flowing from millions of connected devices strengthens relationships with payers and providers, creating switching costs that deepen over time. Founded in Australia in 1989 by Peter Farrell and now headquartered in San Diego, the company carries a dual listing: CHESS Depositary Interests (CDIs) on the ASX and a primary listing on the NYSE.

The economic moat framework formalised by Morningstar identifies five structural sources of competitive advantage: brand strength, cost advantages from scale, customer switching costs, proprietary intellectual property, and network effects; ResMed’s cloud-connected device ecosystem scores on at least two of these dimensions, which explains why Morningstar’s DCF-based fair value sits above the prevailing market price even after the 2025 de-rating.

The numbers require minimal editorialising.

| Period | Revenue (US$ million) | Net Profit (US$ million) | Notes |

|---|---|---|---|

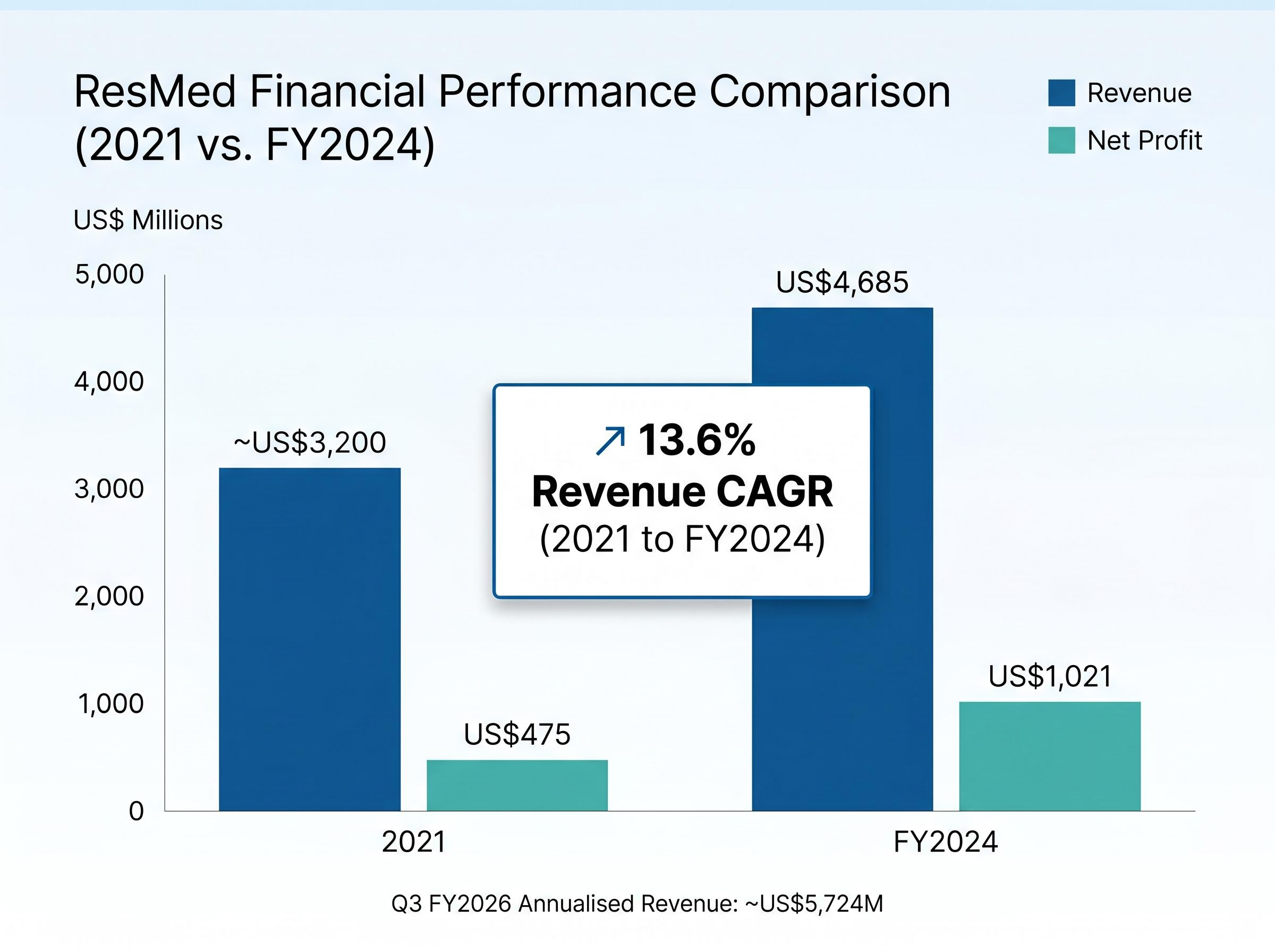

| 2021 | ~3,200 | 475 | Pre-Philips recall baseline |

| FY2024 | 4,685 | 1,021 | ~13.6% revenue CAGR from 2021 |

| Q3 FY2026 (annualised) | ~5,724 | N/A (non-GAAP EPS: US$2.86/qtr) | +11% YoY revenue; +21% EPS |

Revenue grew from approximately US$3.2 billion in 2021 to US$4,685 million in FY2024, a compound annual growth rate of roughly 13.6%. Net profit more than doubled over the same period. The most recent quarter, Q3 FY2026 (three months ended 31 March 2026), delivered US$1.431 billion in revenue against US$1.327 billion in the prior corresponding period, with non-GAAP EPS of US$2.86 versus US$1.60 a year earlier.

ResMed’s return on equity of 22.7% sits well above the 10% threshold analysts typically consider a baseline indicator of capital efficiency for established businesses.

A 21% increase in earnings per share, delivered on top of years of double-digit growth, is the single most important data point for any investor attempting to reconcile the sell-off with the operating reality.

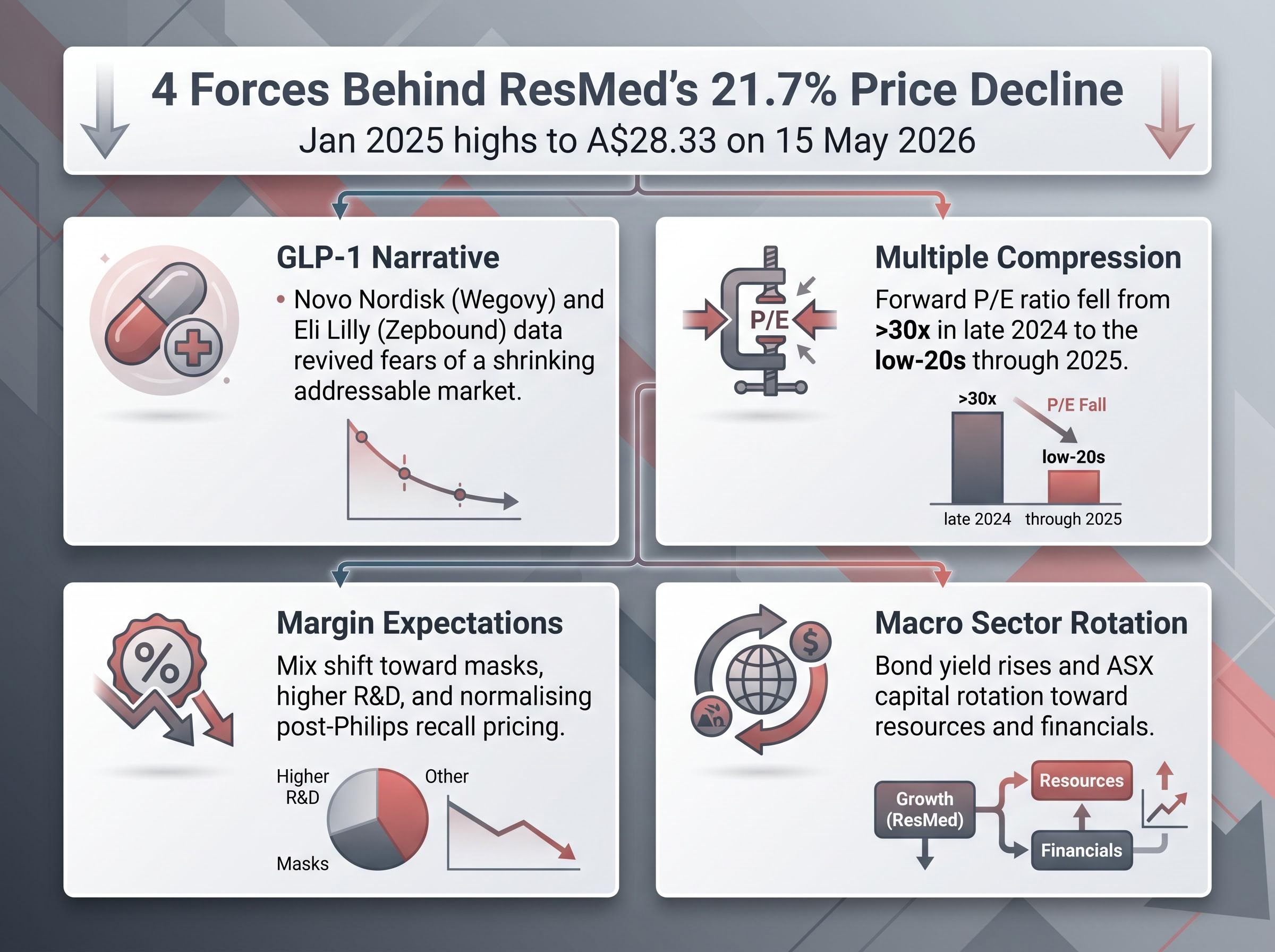

The 21.7% decline from January 2025 highs did not arrive from a single cause. Four distinct forces compressed the price, and distinguishing between them matters because they carry different implications for durability.

Australian broker commentary from Macquarie, Morgans, and Ord Minnett consistently framed the pullback as valuation de-rating, not an earnings collapse. The business kept growing. The multiple contracted. That distinction is the most important analytical step for any investor weighing whether the current price represents an entry point or a value trap.

The ASX healthcare de-rating over the past five years was driven primarily by the unwinding of COVID-era valuation distortions rather than a collapse in underlying earnings, with institutional investors including AustralianSuper and Hostplus characterising the multi-year selloff as a valuation reset and quietly building positions in global earners like CSL, Cochlear, and ResMed throughout the period.

The concern deserves to be taken seriously. GLP-1 receptor agonist drugs, primarily Wegovy from Novo Nordisk and Zepbound from Eli Lilly, promote significant weight loss in obese patients. Because obesity is a known contributor to obstructive sleep apnoea, investors reasonably asked: if millions of patients lose weight through medication, could the number of people who need CPAP devices decline?

The analyst consensus, reflected in ResMed’s Moderate Buy rating, treats this as a long-term partial mitigant rather than a near-term substitute for CPAP therapy. Four structural reasons underpin that view:

CEO Michael Farrell has consistently stated in earnings calls through 2024-2026 that GLP-1 adoption may increase OSA diagnosis rates by bringing patients into more regular contact with the healthcare system, positioning the drugs as potentially additive to CPAP demand rather than substitutive for the majority of patients.

ResMed’s management tone on this subject has been calm and data-driven. The company acknowledges GLP-1s as meaningful innovation in obesity care but maintains that real-world evidence does not support a thesis of dramatic near-term CPAP volume cannibalisation.

The consensus across 15-22 covering analysts is a Moderate Buy, with a 12-month price target of US$286 on the NYSE and a range spanning US$225 to US$345.

| Broker / Source | Rating | Target (USD) | Rationale |

|---|---|---|---|

| Morgan Stanley | Overweight | Trimmed modestly | GLP-1 multiple compression temporary |

| UBS | Buy | Reduced marginally | GLP-1 risk overstated; mid-teens EPS growth |

| Macquarie | Outperform | Above market | Not yet cheap on short-term earnings |

| Morningstar | Fair value above market | DCF-based | Strong moat; GLP-1 a scenario, not base case |

At prevailing AUD/USD exchange rates, the US$286 consensus implies material upside from the A$28-32 range where the CDIs have traded through May 2026. The annualised non-GAAP EPS run-rate from Q3 FY2026 is approximately US$11.44, which provides a current basis for investors computing their own forward P/E.

Mid-teens EPS growth trading at a low-20s forward P/E, a Moderate Buy consensus, and a Morningstar DCF fair value above market all point toward undervaluation if GLP-1 impact proves modest and delayed. The under-diagnosis runway and SaaS growth add optionality beyond the core CPAP market.

For investors wanting to stress-test whether ResMed’s cloud-connected platform qualifies as a structurally durable competitive advantage, our deep-dive into network-effect moat durability on the ASX examines Morningstar’s 2026 review of 132 companies and identifies the specific conditions under which participation-based platform moats hold, narrow, or disappear, providing a directly applicable analytical lens for evaluating the ResMed ecosystem thesis.

The multiple may remain permanently compressed if GLP-1 clinical evidence accumulates more quickly than currently anticipated. Margin expansion has disappointed, and the fading Philips-recall tailwind reduces near-term earnings upgrade catalysts. The wide target range (US$225 to US$345) reflects genuine disagreement, not consensus confidence.

The question the valuation hinges on is specific: does GLP-1 uncertainty justify a permanently lower multiple relative to ResMed’s historical averages and med-tech peers, or is the de-rating a time-limited opportunity that resolves as real-world clinical evidence clarifies the actual impact on OSA prevalence?

The analytical thread through this article points in a consistent direction without reaching a neat conclusion. ResMed’s business has a 13.6% revenue CAGR from 2021 to FY2024, a 22.7% return on equity, and 21% non-GAAP EPS growth in its most recent quarter. The sell-off was driven by sentiment, valuation de-rating, and a specific drug-class threat that the analyst consensus treats as overstated. The current price reflects a forward P/E in the low-20s against a mid-teens growth profile.

None of that tells an investor what to do. Broker price targets are not guarantees. The AUD/USD exchange rate affects CDI returns independently of the underlying business. And personal risk tolerance shapes how much weight any individual places on a long-tail risk like GLP-1 cannibalisation.

For ASX CDI holders specifically, several due diligence considerations apply:

The ASX Guidance Note on CHESS Depositary Interests sets out the entitlements and operational mechanics that apply to CDI holders in foreign-listed companies, including voting rights, dividend handling, and the conversion process between CDIs and underlying shares that affects how ASX investors access the ResMed position.

The question investors are being asked to answer is precise. Do the real-world clinical outcomes for GLP-1 drugs in OSA patients justify a permanent multiple discount? Or will the evidence accumulate in favour of the CPAP market’s durability, closing the gap between operating performance and market pricing?

The data to resolve that question does not yet exist. What exists is a framework for monitoring it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The RMD share price fell roughly 21.7% from its January 2025 highs due to four main forces: renewed GLP-1 drug fears, forward price-to-earnings multiple compression from above 30x to the low-20s, below-expectation margin expansion, and broader ASX healthcare sector rotation driven by rising bond yields.

GLP-1 weight-loss drugs like Wegovy and Zepbound raise concerns that fewer obese patients will develop sleep apnoea and need CPAP devices; however, analyst consensus treats this as a long-term partial mitigant rather than a near-term threat, because OSA has multiple non-obesity causes, many OSA patients are not obese, and the condition remains substantially under-diagnosed globally.

For Q3 FY2026 (three months ended 31 March 2026), ResMed reported US$1.431 billion in revenue, up 11% year-on-year, with non-GAAP diluted EPS of US$2.86, representing a 21% increase on the prior corresponding period.

A consensus of 15-22 covering analysts rates ResMed a Moderate Buy with a 12-month NYSE price target of US$286, spanning a range of US$225 to US$345; Morningstar's DCF-based fair value also sits above the prevailing market price, with brokers including Morgan Stanley, UBS, and Macquarie maintaining positive ratings.

ASX investors hold CHESS Depositary Interests (CDIs) in ResMed rather than direct NYSE shares, meaning they carry AUD/USD currency translation risk on top of underlying business risk, face materially lower trading liquidity than the NYSE, and must convert broker price targets (quoted in USD) at current exchange rates to assess their actual position.