Why Barclays Sees 56% Upside in a Beaten-Down Automation Stock

7 mins ago

Morningstar reviewed 132 companies worldwide in February 2026 and arrived at a conclusion that cuts against the prevailing AI narrative: the businesses least disrupted by artificial intelligence were not the ones building it, but the ones whose value is rooted in human participation at scale. As AI dominates investor discourse in 2026, a widespread assumption has taken hold that platform businesses, particularly job boards and marketplaces, face existential disruption. Morningstar’s global moat reassessment, extended to Australian names in April 2026, challenges this assumption directly. What follows is the analytical framework behind network-effect moat resilience, the evidence from a systematic 132-company review, and a worked example using Seek (ASX: SEK), so investors evaluating platform and marketplace stocks can assess AI risk with a structured lens rather than intuition.

The intuitive version of the AI disruption argument is straightforward: a sufficiently capable AI model could replicate what any digital platform does, faster and cheaper, rendering the incumbent’s market position irrelevant. Applied to job boards, the logic runs that generative AI tools will allow employers and candidates to find each other directly, bypassing the platform entirely.

The argument sounds compelling. It is also built on a misidentification of what makes a platform valuable.

The analytical error is treating all platform businesses as technology businesses. When AI improves, it threatens competitive advantages built on technology. It does not, however, replicate competitive advantages built on the accumulated behaviour of millions of participants.

Morningstar’s February 2026 review drew a clear distinction between these two moat categories:

Network-effect businesses represented the least downgraded cohort across the 132 companies Morningstar reviewed globally. The moat is not a feature. It is the weight of participation itself.

The scale of the exercise matters. Morningstar’s February 2026 reassessment was not a thematic opinion piece; it was a systematic stress test of competitive advantages across 132 companies worldwide, applying AI disruption scenarios to each firm’s moat source.

The pattern that emerged was consistent. Roughly half of wide-moat firms derived their advantages from network effects, and this cohort was the most intact after the AI stress test. Moat downgrades clustered in a specific category: workflow-dependent software companies, particularly those in design and productivity software where generative AI tools could directly substitute the core product.

The contrast with technology-dependent moats is striking: the legacy software repricing that erased approximately $2 trillion in US software market value in early 2026 was concentrated precisely in per-user licensing models where AI could directly substitute the core product function, the same vulnerability profile that Morningstar’s review flagged as the primary downgrade driver across workflow-dependent software firms.

Several companies received moat upgrades. Airbnb was upgraded to a wide moat based on network effects and proprietary data, a recognition that its long-tail supply aggregation cannot be replicated by AI alone. Cloudflare and CrowdStrike were among a small number of upgrades, both tied to cybersecurity network effects amplified by AI-driven demand. Booking Holdings received no moat downgrade, with Morningstar citing network effects as superseding technology advantages.

The stated conclusion was direct: network effects are “the most resilient moat source in the face of AI.”

| Company | Moat Rating Outcome | Moat Source | AI Impact Assessment |

|---|---|---|---|

| Airbnb | Upgraded to wide moat | Network effects, proprietary data | AI enhances discovery; network intact |

| Booking Holdings | No downgrade | Network effects | Network supersedes technology advantage |

| CrowdStrike | Upgraded | Network effects, data scale | AI demand amplifies moat |

| Cloudflare | Upgraded | Network effects, data scale | AI demand amplifies moat |

| Workflow software firms | Downgraded (cohort) | Technology-dependent | AI replicates core product functionality |

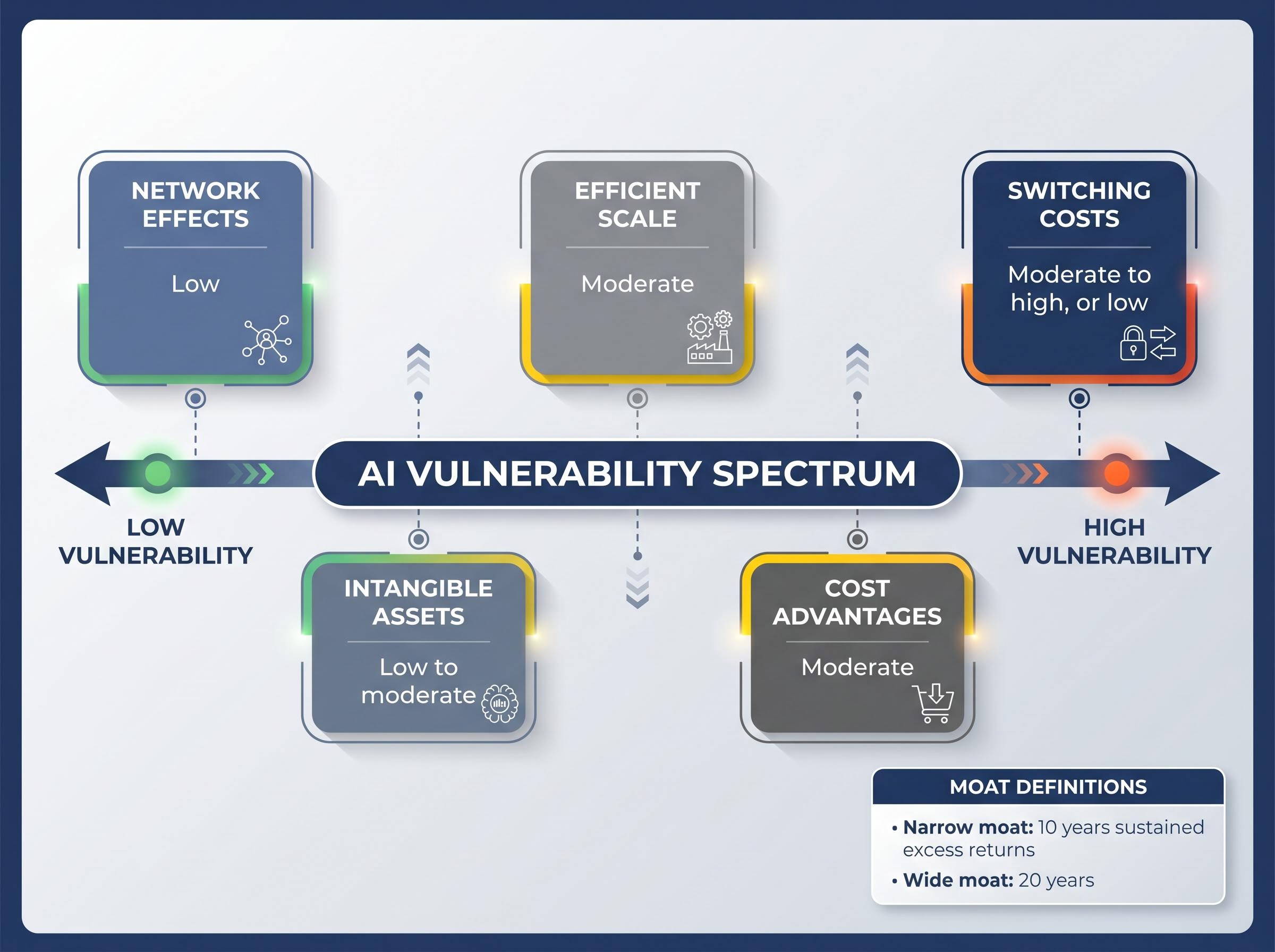

An economic moat is a structural competitive advantage that allows a company to earn returns above its cost of capital for an extended period. A narrow moat implies at least 10 years of sustained excess returns; a wide moat implies at least 20 years with high confidence. The moat concept matters for AI risk assessment because the durability of a business’s advantage determines whether a new technology erodes it or reinforces it.

Morningstar’s economic moat ratings methodology assigns wide moat status only when a firm can sustain excess returns above its cost of capital for at least 20 years with high confidence, a threshold that anchors the AI stress testing applied across all 132 companies in the February 2026 global review.

Morningstar’s framework identifies five moat sources, each with a different vulnerability profile under AI disruption:

Beyond the five sources, Morningstar’s AI review identified additional resilience criteria: ownership of key infrastructure, proprietary data, deep platform ecosystems, regulatory barriers, and unique domain-specific logic.

Morningstar, February 2026: Network effects are “the most resilient moat source in the face of AI.”

The distinction that matters most is structural. In a network platform, switching costs are implicit: they arise from the loss of access to the network’s liquidity, not from any technology lock-in a company controls.

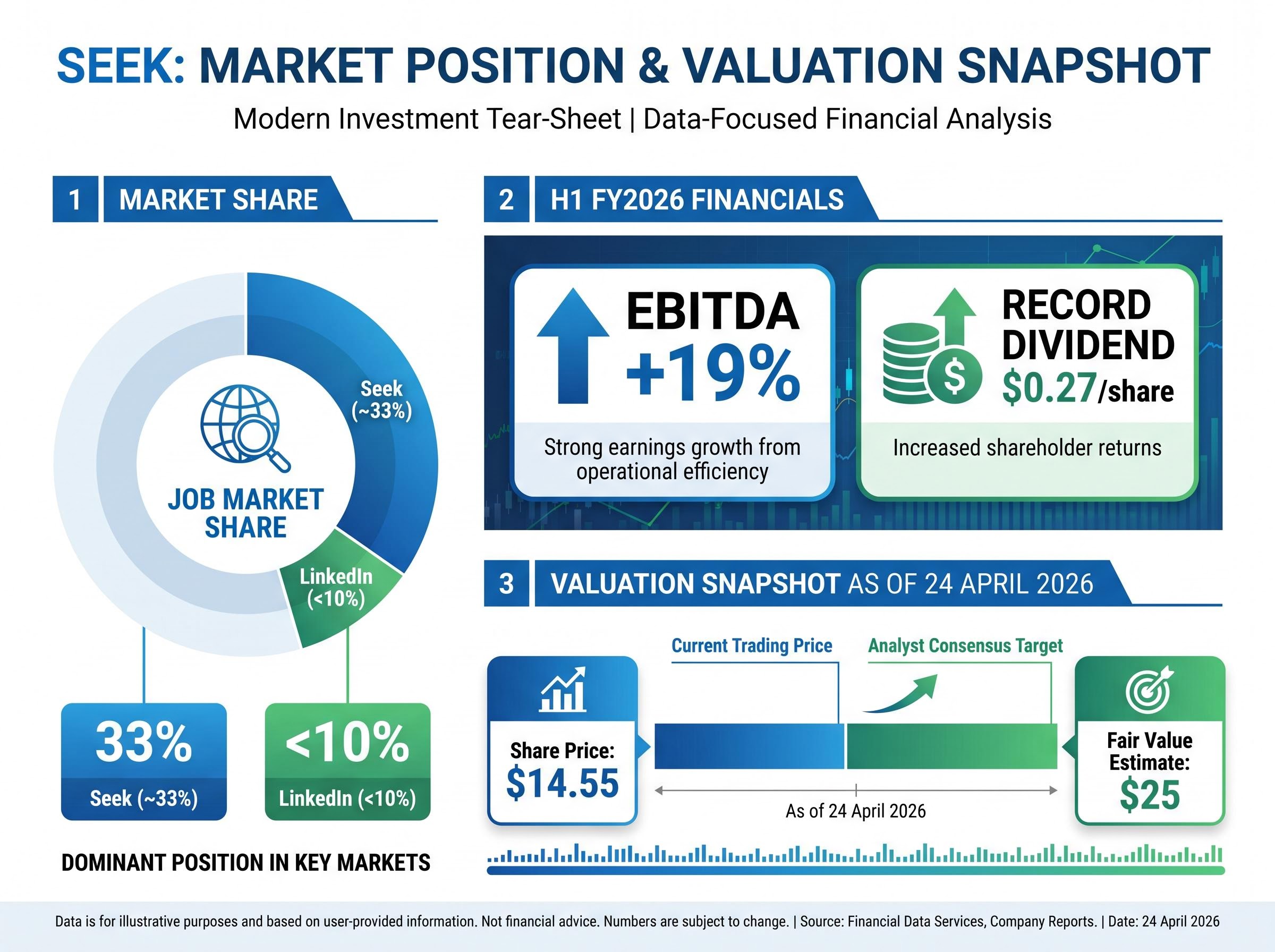

Seek holds approximately one-third of all Australian job placements, according to Morningstar’s April 2026 analysis. LinkedIn accounts for fewer than 10% in the same market. That gap is not a technology gap; it is a network gap. Seek’s matching intelligence is built on proprietary historical data spanning vacancies, CVs, applications, and hiring outcomes accumulated over years. A new entrant with superior AI but no history of Australian hiring behaviour cannot replicate this data flywheel.

The platform’s shift from active job search to a passive, feed-based discovery model, resembling social media in format, further deepens engagement and data capture. Each interaction refines the matching algorithm, which attracts more employers, which attracts more candidates. The cycle is self-reinforcing and participation-dependent.

The counterintuitive element is that generative AI strengthens the cycle rather than disrupting it. AI tools lower the barrier for job seekers to tailor CVs and apply in volume, which increases application flow onto platforms with the greatest visibility.

Seek’s H1 FY2026 results (period ending 31 December 2025) reflected this dynamic directly. EBITDA grew 19% and advertising yield rose 17%, driven by AI-enabled advertising that improved targeting and employer willingness to pay for premium placements.

According to the Deloitte Australian Employer Survey (Q1 2026), 68% of more than 500 Australian employers reported 20-30% higher application volumes on platforms like Seek since generative AI tools proliferated from mid-2025. Management’s confidence is visible in a record dividend of $0.27 per share and updated FY2026 adjusted profit guidance of $195-$250 million.

Morningstar, April 2026: Narrow moat rating confirmed for Seek, with a fair value estimate of $25 per share versus a share price of $14.55 as of 24 April 2026, implying a price-to-fair-value ratio of 0.58.

A $178 million impairment loss on China operations in the period was treated by most analysts as a one-off rather than a structural concern.

The most specific challenge to the Seek moat thesis came from Jefferies in March 2026. The analyst note argued that AI tools may lower the cost of direct hiring workflows, enabling employers to source candidates without platform dependency. Jefferies flagged Seek’s divestiture of Employment Hero as reducing an integrated hiring ecosystem, potentially opening a gap competitors could exploit.

This is a legitimate concern worth stress-testing. Its weakness lies in one assumption: that employers and candidates have a viable alternative network with comparable liquidity. They currently do not. Seek’s 33% placement share versus LinkedIn’s sub-10% share in the Australian market means that bypassing Seek requires either building a new network from zero or relying on fragmented channels with lower match quality.

Retail investor sentiment appeared to reflect this assessment. Approximately 70% or more of participants in Stockhead polls (April 2026) expressed positive sentiment toward Seek, suggesting the Jefferies concern had limited uptake.

Genuine near-term risks do exist, and they should not be conflated with the structural AI question:

Bank of America’s estimate that 838 million jobs carry meaningful AI job exposure, roughly one in four globally, adds an important dimension to the Seek thesis: if generative AI reshapes labour markets at scale, the volume of hiring activity on which job platforms depend could shift structurally, even as those platforms retain their network position within a changed market.

Morningstar assigns Seek a High uncertainty rating, which is relevant context for position sizing regardless of the moat assessment.

The same moat diagnostic applied to Seek extends naturally to other ASX-listed marketplace platforms, and the pattern holds.

REA Group (ASX: REA) received a wide moat confirmation from Morningstar Australia in April 2026. Its real estate listings network creates a self-reinforcing cycle between sellers, buyers, and agents. AI tools boosted advertising yields approximately 15% in H1 FY2026, functioning as a revenue accelerator rather than a competitive threat.

Carsales (ASX: CAR) maintained its narrow moat rating (Morningstar and Kalkine, March 2026). EBITDA grew 12% in H1 FY2026, aided by AI-powered pricing intelligence tools that enhanced buyer and seller matching.

No ASX-listed network platform or marketplace company received an AI-driven moat downgrade in 2025-2026 across coverage from Macquarie, UBS, Morningstar, and Kalkine.

| Company | Morningstar Moat Rating | AI Impact on Financials (H1 FY2026) | Primary Moat Source |

|---|---|---|---|

| Seek (SEK) | Narrow moat confirmed | EBITDA +19%, yield +17% | Network effects, proprietary hiring data |

| REA Group (REA) | Wide moat upheld | Ad yields +~15% | Network effects, listing liquidity |

| Carsales (CAR) | Narrow moat maintained | EBITDA +12% | Network effects, pricing data |

The screening question investors can carry forward: does the platform’s value derive primarily from the size and engagement of its network, or from the proprietary technology it uses to serve that network? Where the answer is participation, the AI disruption thesis weakens materially.

AI is not a universal moat destroyer. Investors who treat it as one risk systematically mispricing network-effect platforms whose competitive advantages are participation-based rather than technology-based. Morningstar’s 132-company review, the ASX moat rating record in 2025-2026, and Seek’s H1 FY2026 financial performance all point in the same direction.

The thesis has clear limits. It applies to platforms where network participation is the primary value driver. It does not extend to all technology companies, and it does not eliminate cyclical or execution risk.

Investors can apply this framework to existing holdings through a straightforward diagnostic:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

For investors wanting to situate the moat-resilience thesis within the broader question of AI equity pricing, our full explainer on AI equity valuation frameworks applies four distinct analytical lenses, including Minsky, Kindleberger, Sharma, and Shiller CAPE, to the current market environment and delivers a split verdict on whether AI-driven gains reflect genuine revenue or speculative excess.

AI proof stocks are companies whose competitive advantages are not easily replicated or eroded by artificial intelligence. Network-effect platforms qualify because their moats are built on the accumulated behaviour of millions of participants, not on proprietary technology that AI can substitute.

Morningstar's February 2026 review found that network-effect businesses were the least downgraded cohort across all 132 companies assessed, while workflow-dependent software firms saw the most moat downgrades because AI could directly replicate their core product functionality.

Seek's H1 FY2026 results showed EBITDA growth of 19% and advertising yield growth of 17%, with AI-enabled tools increasing application volumes and employer willingness to pay for premium placements, making AI a financial tailwind rather than a threat.

Investors should determine whether the platform's primary value comes from the size and engagement of its network (participation-based) or from the technology it uses to serve that network; where the answer is participation, the AI disruption thesis weakens materially.

A technology-dependent moat relies on proprietary software or algorithms that AI can replicate or surpass, while a participation-dependent moat is rooted in network effects and accumulated user behaviour that require time and mass adoption to build and cannot be copied by a new entrant with superior AI alone.