Sonic Healthcare’s P/S Halved: What the SHL Price Drop Signals

2 mins ago

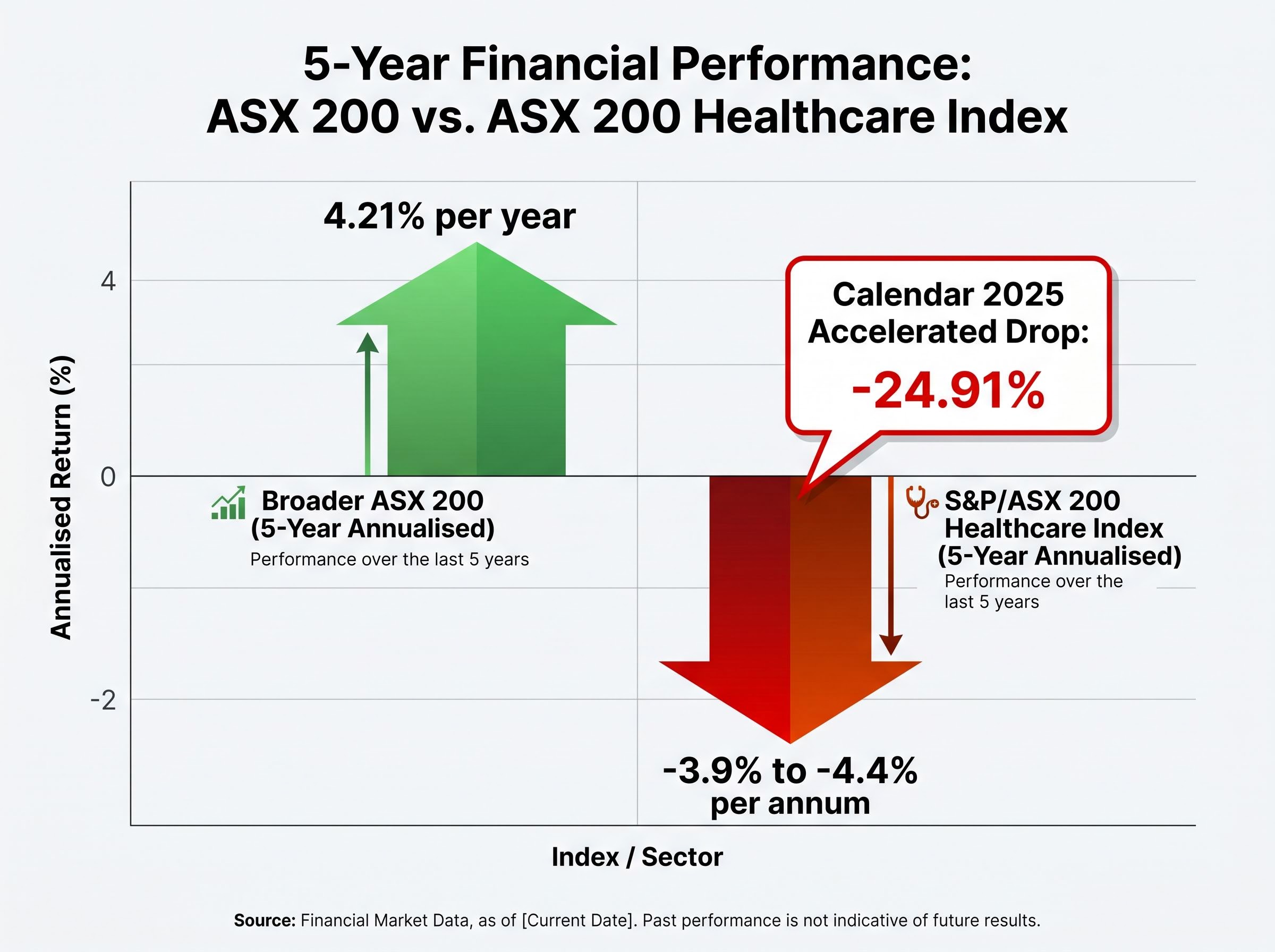

The S&P/ASX 200 Healthcare Index has delivered an annualised return of approximately -3.9% to -4.4% per annum over the past five years, destroying wealth even as the broader ASX 200 returned approximately 4.21% per year over the same period. For a sector long marketed as defensive and recession-resilient, that gap demands an explanation.

As of May 2026, institutional investors including AustralianSuper and Hostplus have quietly been adding to healthcare positions, framing the sector’s prolonged de-rating as a valuation reset rather than structural collapse. The tension between the performance record and the emerging conviction trade is the central question this analysis addresses. What follows is a diagnosis of exactly what drove the sector’s decline, which ASX healthcare sub-segments carry genuine recovery potential and which remain structurally challenged, and what global tailwinds in spending and technology could serve as the catalyst.

The headline figures are stark. The XHJ returned approximately -3.9% to -4.4% per annum annualised over five years and fell -24.91% across calendar 2025 alone, confirming the deterioration was accelerating rather than stabilising. Against a broader ASX 200 delivering roughly 4.21% per year, the sector’s cumulative underperformance over the period is among the most severe for any major index sub-sector.

The ten-year track record, however, remains modestly positive, which matters. The long-run growth thesis is not structurally broken. What happened was a sequence of overlapping pressures, each compounding the next.

CSL’s index weighting of approximately 45% in the XHJ means the mechanics of the sector selloff are less diversified than they appear: a single stock’s currency exposure, CEO departure, and demerger announcement in early 2026 transmitted directly to the headline index number, compressing the apparent breadth of the sector’s problems.

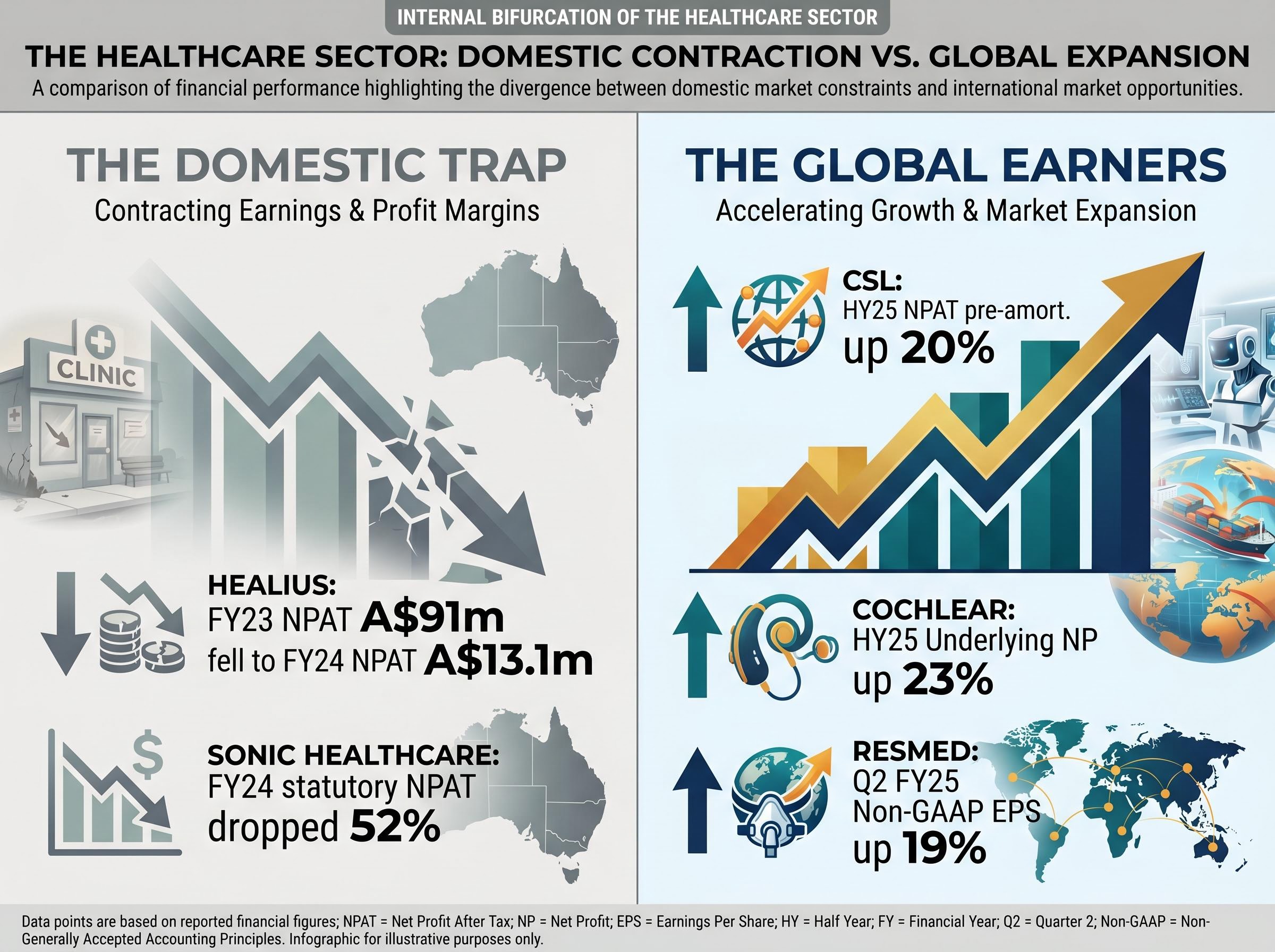

The first and most significant was the COVID valuation cycle. Pathology and diagnostics businesses saw revenues spike on pandemic testing demand, and multiples expanded to price that demand as durable. When it rolled off, both revenues and the premiums attached to them collapsed simultaneously. Sonic Healthcare’s FY24 results captured the distortion precisely: revenue fell 10%, EBITDA declined 25%, and statutory net profit after tax dropped 52%, yet core non-COVID pathology volumes were growing in the mid-single digits throughout.

Morgan Stanley characterised the underperformance in early 2025 as “largely multiple compression from elevated COVID valuations rather than structural impairment.”

That multiple compression was then accelerated by a set of secondary pressures:

The gap between Medicare rebate adjustments and actual wage growth has created a structural margin trap for domestic pathology providers. Healius is the sharpest illustration: underlying net profit after tax fell to A$13.1 million in FY24 from A$91 million in FY23, a decline driven not by volume loss but by the inability to pass through rising costs under constrained reimbursement settings. The ACCC’s decision to block the Australian Clinical Labs bid for Healius removed a consolidation pathway that might have delivered cost efficiencies, adding regulatory constraint to an already pressured operating model.

The ACCC decision to block the acquisition was grounded in concerns about a substantial lessening of competition across Australian pathology services markets, a regulatory outcome that effectively closed off the most plausible route to cost efficiency for an operator already squeezed by reimbursement constraints.

The aggregate index performance conceals a bifurcation that institutional managers have identified as the single most important selection principle within the sector. The global earners are not just outperforming the domestic operators; they are delivering earnings growth that contradicts the narrative of a broken sector entirely.

| Company | Revenue Growth | Earnings Growth | FY Guidance | Broker Sentiment |

|---|---|---|---|---|

| CSL (HY25) | 12% (US$8.0bn) | NPAT pre-amort. up 20% | Upper half of 13-17% range | Outperform (Macquarie) |

| Cochlear (HY25) | 15% (A$1.08bn) | Underlying NP up 23% | Upgraded to 18-22% growth | Increased exposure (Alphinity) |

| ResMed (Q2 FY25) | 11% (US$1.31bn) | Non-GAAP EPS up 19% | Stable US reimbursement | Buy (UBS) |

These are not marginal beats. CSL grew net profit 20% in the half. Cochlear upgraded full-year guidance to 18-22% profit growth on the back of stronger-than-expected surgery volumes in North America and Europe. ResMed delivered 19% earnings-per-share growth in a single quarter. The underperformance was valuation-driven; the earnings were not broken.

The institutional consensus has crystallised around this distinction. Alphinity Investment Management increased exposure to both CSL and Cochlear in its March 2025 quarterly update, while stating it remained “underweight pure domestic healthcare providers where regulatory and labour cost risks are elevated.”

QVG Capital’s Chris Prunty described the sector as “de-rated, but earnings are not broken,” with his funds gradually adding to select names where earnings visibility was improving. Ophir Asset Management’s Andrew Mitchell noted several healthcare names were trading at multi-year valuation lows, building positions in businesses with global earnings and low balance-sheet risk while remaining cautious on domestic pathology players.

AustralianSuper characterised the sector’s multi-year underperformance as a “valuation reset” opportunity, naming CSL, ResMed and Cochlear as key holdings. Hostplus described its active portfolios as “remaining overweight healthcare,” focused on CSL, Sonic Healthcare and ResMed.

The “defensive” label attached to healthcare is neither marketing invention nor unconditional truth. Healthcare spending is among the last areas that consumers and governments reduce during economic downturns, making revenue streams genuinely stickier than those of most sectors. During the Global Financial Crisis, the evidence was direct.

The healthcare sector was the top-performing sector on the ASX during the Global Financial Crisis, providing the strongest empirical evidence for its defensive properties.

That defensive characteristic, however, does not immunise the sector against valuation compression. A sector can have stable underlying demand while its share prices fall sharply, which is precisely what occurred when growth premiums built during COVID were repriced as interest rates rose. The defensive label describes revenue resilience, not share price resilience under all conditions.

The defensive label in ASX healthcare obscures a critical distinction: revenue resilience across economic cycles does not translate to share price resilience when the same stocks carry growth-rate multiples that reprice sharply as interest rates rise and consumer confidence falls.

Investors re-entering the sector should also recognise that ASX healthcare is not a single business model. The index spans fundamentally different sub-segments:

The private health insurance premium increase of 3.6% effective 1 April 2025, following 3.03% in 2024, illustrates one of the policy mechanisms that underpin private hospital and device utilisation, indirectly supporting companies like Cochlear.

Private health insurance premium increases provide one of the clearest policy mechanisms linking regulatory settings to device utilisation: when approved increases exceed claims inflation, fund margins recover and capacity for benefits expansion improves, creating a secondary support for procedure volumes at companies like Cochlear that depend on insured surgical demand.

The scale of global healthcare expenditure reframes what ASX healthcare exposure actually represents. According to World Health Organization data published in 2024, global health spending reached US$9.8 trillion in 2022 and continues to grow faster than global GDP in high- and middle-income regions.

| Category | Current Size | Growth Rate / Projection |

|---|---|---|

| Total Global Health Spending (2022) | US$9.8 trillion | Growing faster than global GDP |

| US Healthcare Expenditure | Over 40% of global total | ~7% annually (2022-2027) |

| Global Healthcare IT Market (2023) | US$168.9bn | CAGR ~17.9% to 2030 |

| Global Healthcare SaaS Market (2023) | US$39.4bn | ~US$147bn by 2032 (CAGR ~15.9%) |

The United States accounts for over 40% of global healthcare expenditure, with spending estimated to grow at approximately 7% annually through 2027. This is directly relevant because the three largest ASX healthcare names generate the majority of their revenues offshore, particularly in the US and European markets.

The connection is specific, not abstract:

Morgan Stanley identified ResMed’s connected device fleet and SaaS platforms in August 2024 as drivers of recurring, high-margin revenue. According to Grand View Research (2024), the global healthcare IT market was valued at US$168.9 billion in 2023 with a projected compound annual growth rate of approximately 17.9% through to 2030. Precedence Research (2024) estimated the healthcare SaaS market at US$39.4 billion, forecast to reach approximately US$147 billion by 2032.

For Australian retail investors, the practical implication is that these ASX-listed companies function as a vehicle for accessing US and European healthcare growth without direct foreign exchange conversion, changing the investment thesis from a domestic defensive play to a global structural growth exposure.

Institutional capital allocation toward environmental, social and governance (ESG) frameworks provides a separate demand-side support for healthcare valuations, operating independently of the earnings recovery cycle.

According to a Morgan Stanley survey, more than half of investors indicated plans to raise their allocation toward sustainable investments in 2024.

Healthcare’s role in delivering services that address fundamental human needs creates a natural alignment with the social pillar of ESG frameworks. This alignment is most direct in specific sub-segments:

AustralianSuper and Hostplus, two of Australia’s largest superannuation funds, have both increased healthcare exposure on rationale that is compatible with their published ESG and responsible investment frameworks. This is not incidental. As institutional mandates increasingly require ESG alignment in portfolio construction, healthcare’s essential-services nature positions it as a natural destination for capital that might otherwise be excluded from sectors with higher social or environmental controversy.

The ESG tailwind is not universal across the sector, however, and investors should distinguish between companies where the alignment is clean and those where it is more nuanced.

The recovery thesis has substance, but several risks remain unresolved and demand the same analytical precision as the tailwind arguments.

The multiple compression that has occurred means some of these risks are partially priced in. Sonic Healthcare was trading at approximately 1.0x forward sales in March 2025 versus its five-year average of approximately 1.9x, according to Goldman Sachs, reflecting significant market scepticism. That discount, however, is not on its own a signal of imminent re-rating.

Three observable developments would help confirm whether the recovery thesis is gaining traction:

These are leading indicators rather than buy signals, offering a monitoring framework for investors assessing the timing and conviction of any re-entry.

Investors wanting to stress-test the recovery thesis against risks that may not reverse cyclically will find our deep-dive into US structural policy risks for ASX healthcare, which examines FDA approval instability, RFK Jr.-led HHS policy changes affecting CSL’s vaccine franchise, and why these headwinds carry no automatic correction mechanism of the kind that rate normalisation provides.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The analytical evidence points in a consistent direction. The sector’s underperformance was real but diagnosably cyclical in its primary mechanism, driven by the unwinding of COVID-era valuation distortions rather than the collapse of an earnings base. The structural tailwinds, from global healthcare spending growth to ESG-driven capital allocation, operate independently of that cycle and are already drawing institutional capital back into select names.

The bifurcation between global earners and domestic operators is the most practical insight for investors evaluating the sector. CSL, Cochlear and ResMed carry the strongest earnings trajectories, innovation cycles and global revenue exposure. Domestic operators such as Healius require a separate and higher evidence threshold before conviction is warranted.

The conditions for sector re-engagement are forming. They reward selectivity, not index-level exposure to the XHJ.

The XHJ, or S&P/ASX 200 Healthcare Index, tracks the performance of healthcare companies listed on the ASX. It has delivered an annualised return of approximately -3.9% to -4.4% per year over the past five years and fell nearly 25% in calendar 2025 alone, significantly underperforming the broader ASX 200.

The underperformance was primarily driven by the unwinding of inflated COVID-era valuations across pathology and diagnostics businesses, compounded by rising interest rates compressing growth stock multiples, labour cost inflation, and Medicare rebate indexation failing to keep pace with wage growth for domestic operators.

Global earners like CSL, Cochlear and ResMed generate the majority of their revenue from US and European markets, delivering strong earnings growth largely insulated from Australian reimbursement constraints, while domestic operators like Healius and Sonic Healthcare rely heavily on Medicare rebates and face a structural margin squeeze from labour cost inflation.

Global health spending reached US$9.8 trillion in 2022 and continues to grow faster than global GDP, with the US alone accounting for over 40% of that total and projected growth of around 7% annually through 2027. ASX healthcare companies like CSL, Cochlear and ResMed earn the majority of their revenues from these markets, making them direct beneficiaries of this structural spending growth.

Three key indicators to monitor are: any stabilisation in Healius's underlying profitability signalling relief in the domestic operator trap, CSL's FY25 earnings landing at or above the upper half of its 13-17% NPAT growth guidance range, and any material changes to US reimbursement policy from the Centers for Medicare and Medicaid Services that would directly affect CSL and ResMed revenues.