Foxconn Beats Q2 Estimates by 6% as AI Server Demand Surges

16 hrs ago

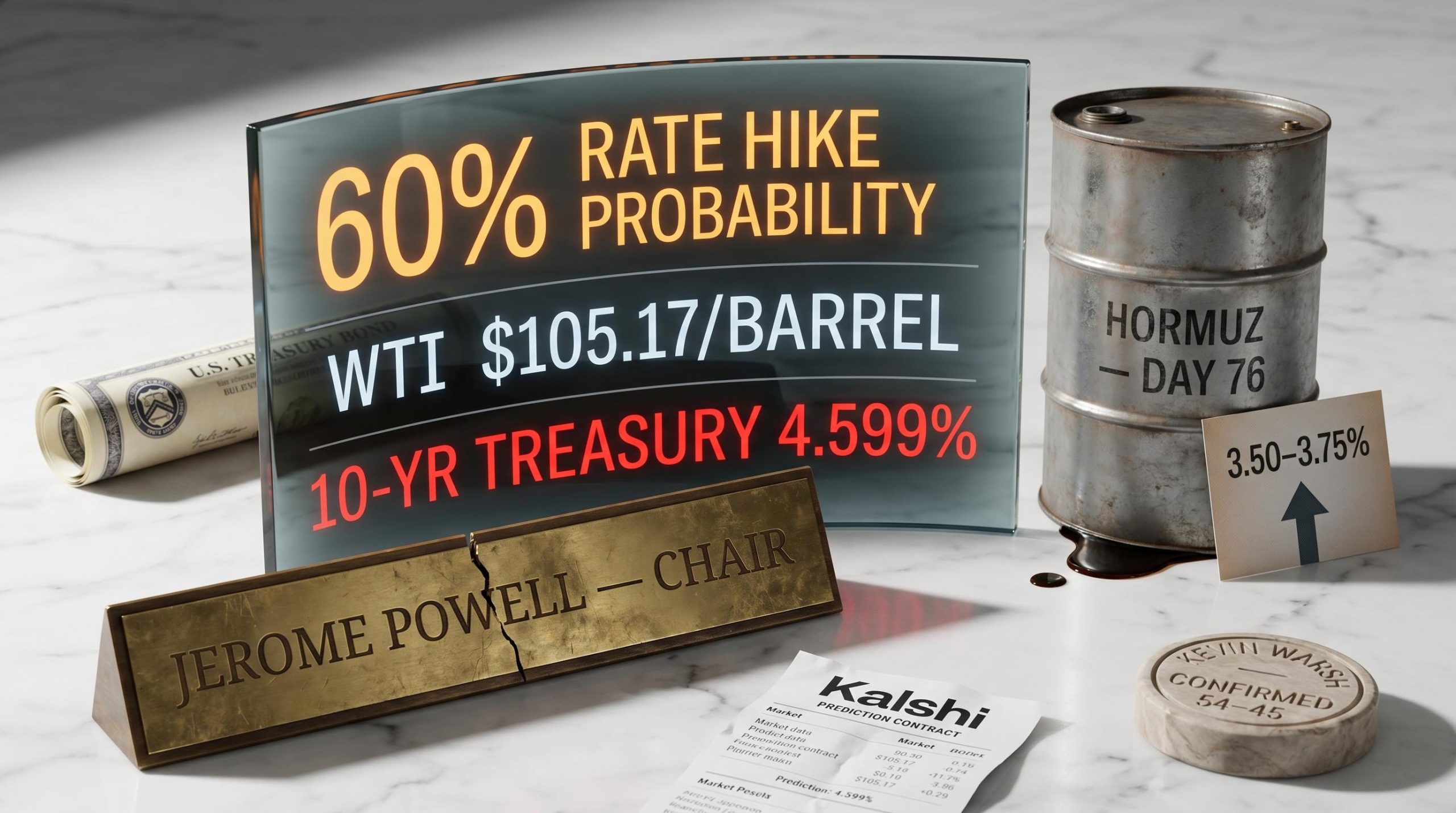

On 15 May 2026, the same day Jerome Powell walked out of the Federal Reserve for the last time as chair, prediction markets put the probability of a rate hike before July 2027 at 60 percent. That number, drawn from Kalshi, would have been almost unthinkable six months ago.

Three forces converged this week. April CPI and PPI data came in hotter than expected, driven by war-related energy prices. The Strait of Hormuz remained effectively closed for the 76th consecutive day. And Kevin Warsh, a Trump-aligned nominee, was confirmed as the next Fed chair. Together, these developments have forced a sharp reassessment of the Federal Reserve rate hike probability, shifting the consensus from “when will they cut?” to “could they hike?”

What follows explains how the Iran conflict is feeding directly into U.S. prices, what the Warsh appointment means for the institution’s independence, and why the market has repriced the rate path entirely.

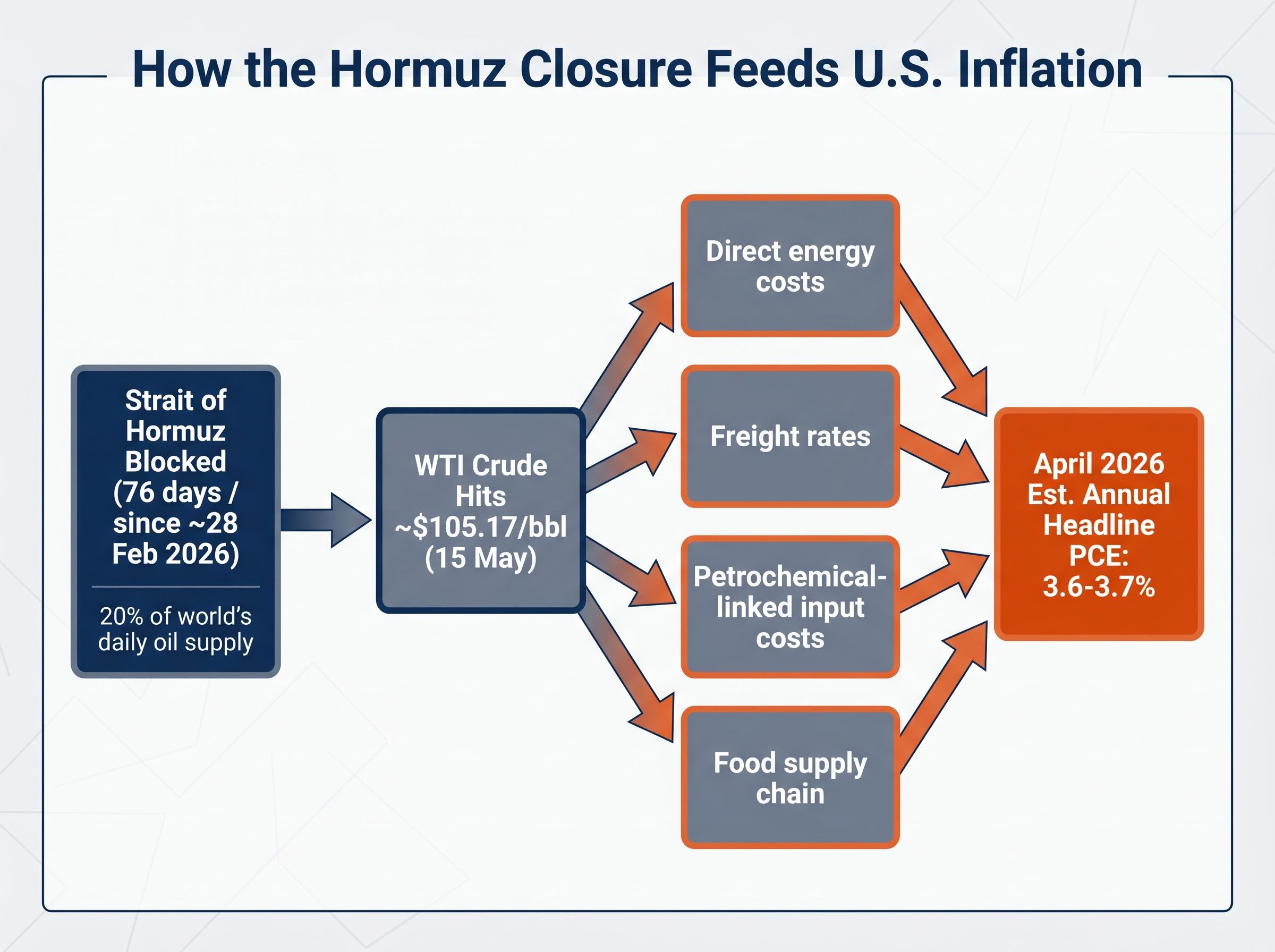

The mechanism is physical before it is financial. The Strait of Hormuz, through which roughly 20 percent of the world’s daily oil supply passes, has been effectively blocked since approximately 28 February 2026. A waterway 7,000 miles from the United States has reached directly into what Americans pay at the pump, at the grocery checkout, and on shipping invoices.

The Hormuz triple lock, combining active U.S. naval blockade operations, Iranian toll enforcement on non-aligned vessels, and the near-total withdrawal of commercial war risk insurance, means the waterway has remained effectively closed even on days when physical passage was theoretically possible.

WTI crude oil closed at approximately ~$105.17 per barrel on 15 May, up roughly 4.2 percent on the day and approximately 8 percent on the week. That price filters into the domestic economy through multiple channels:

April 2026 CPI and PPI both came in above market expectations, with energy as the primary driver. PCE-relevant components from both reports point to a monthly headline Personal Consumption Expenditures (PCE) advance of slightly above 0.6 percent for April, implying an annual headline PCE rate of 3.6-3.7 percent, according to analyst estimates.

This is a supply-side shock, not a demand-driven one. That distinction matters enormously for how the Fed can respond.

KPMG U.S. chief economist Diane Swonk has projected that inflationary effects from the Iran war would intensify before improving, a view consistent with the Hormuz closure’s ongoing nature and the Congressional Research Service’s March 2026 risk assessment of the waterway.

A Fed official reviewing the incoming data this week would see the picture build in stages.

Core PCE for March 2026 rose 0.3 percent month-over-month, according to Bureau of Economic Analysis data. That was already uncomfortable. The April estimate, informed by this week’s CPI and PPI releases, sits at approximately 0.3 percent monthly for core, placing the annual core PCE rate at roughly 3.0-3.1 percent, per KPMG U.S. analysis.

The headline figure is worse. Annual headline PCE is projected at 3.6-3.7 percent for April, which would mark the highest reading since May 2023.

| Inflation Metric | March 2026 Reading | April 2026 Estimate | Fed Target |

|---|---|---|---|

| Headline PCE (MoM) | — | ~0.6%+ | Consistent with 2.0% annual |

| Core PCE (MoM) | 0.3% | ~0.3% | Consistent with 2.0% annual |

| Annual Headline PCE | — | 3.6-3.7% | 2.0% |

| Annual Core PCE | — | ~3.0-3.1% | 2.0% |

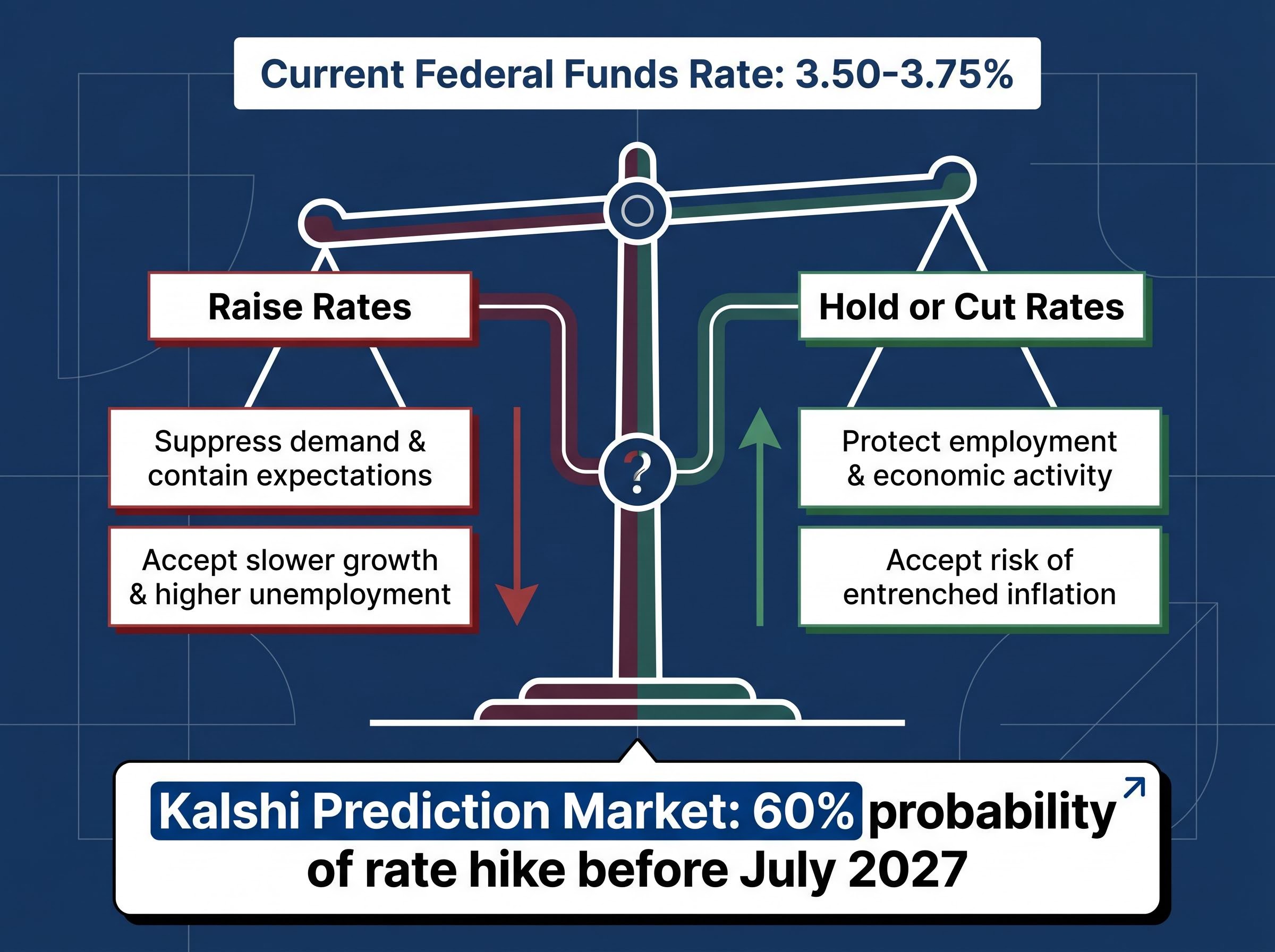

The federal funds rate currently sits at 3.50-3.75 percent, held steady at the 29 April FOMC meeting. At least some committee members at that meeting favoured a rate hike, per available reporting. The data arriving since has only strengthened their case.

The April 2026 FOMC statement confirmed the federal funds rate target range at 3.50-3.75 percent while explicitly acknowledging that inflation was elevated in part due to rising global energy prices, a formulation that left the door open for tightening if incoming data continued to deteriorate.

Kalshi, a regulated U.S. prediction market where participants stake real money on outcome contracts, placed the probability of a Fed rate hike before July 2027 at 60 percent following this week’s inflation releases. That figure is derived from actual capital committed to positions, not survey responses.

Six months ago, the consensus expectation was rate cuts. The 60 percent hike probability represents a near-complete inversion of where markets stood at the start of 2026.

The Fed’s standard tool is the interest rate. Raise rates and borrowing becomes more expensive, which slows spending, which reduces demand, which eases price pressure. That mechanism works when inflation is demand-driven: too much money chasing too few goods.

An oil supply shock creates a different problem. Prices rise not because demand is excessive but because supply has been physically removed. The Hormuz closure has taken barrels off the market. No interest rate setting can put them back.

This forces the Fed into a genuine trade-off, not a clean policy choice:

The dual mandate (price stability and maximum employment) offers no escape from this tension. It requires the Fed to balance both objectives simultaneously, and a supply shock makes them directly opposed.

The 1973-74 OPEC oil embargo offers a cautionary precedent. The Arthur Burns-led Fed responded to that supply shock with politically accommodative monetary policy rather than tightening. The result was a decade of entrenched inflation that required the severe Volcker tightening of the early 1980s to break. The 1951 Treasury-Fed Accord, which restored the Fed’s independence from Treasury control after wartime yield-curve pegging, established the institutional principle now under scrutiny: that central bank credibility depends on resisting political pressure precisely when that pressure is most intense.

The Federal Reserve History analysis of the 1973 oil shock details how Burns-era accommodation of a supply-driven price surge allowed inflation expectations to become unanchored, a process that unfolded gradually enough that policymakers repeatedly underestimated its severity until correction required extreme tightening.

The April FOMC statement acknowledged elevated inflation risks from Middle East developments. How the new chair interprets that language will define the institution’s direction.

The Senate confirmed Kevin Warsh as the next Federal Reserve chair on 13 May 2026, by a vote of 54-45. As of 15 May, the formal transition from Powell remains pending.

The fractured FOMC that Warsh inherits is a legacy of the 29 April decision, where a historic four-way dissent split the committee between hawks pushing for hike signalling and a lone dove seeking accommodation, leaving official guidance language that three of four dissenters publicly opposed.

The confirmation did not arrive in a vacuum. President Trump has publicly advocated for lower interest rates throughout his second term. The administration has launched an investigation into the Federal Reserve itself. These actions create background pressure on any incoming chair, regardless of stated intentions.

During confirmation proceedings, Warsh committed to maintaining the Fed’s independence, though with qualifications that drew scrutiny from economists and senators. Reuters reported on 21 April 2026 that Warsh framed his independence commitment in terms that left room for interpretation, a distinction that matters when the institution’s credibility is the variable markets are pricing.

Bond markets registered the tension immediately. The 10-year Treasury yield reached 4.599 percent on 15 May, up 14 basis points on the day and 24 basis points on the week. The 30-year Treasury yield hit 5.125 percent, breaching 5 percent for the first time since 2007.

The question is not whether Warsh will face pressure to cut. He will. The question is whether the institution’s independence framework survives the combination of political demand and an inflation environment that argues against accommodation.

The repricing is not confined to the United States. On 15 May 2026, long-dated government bonds sold off across the world’s largest sovereign debt markets simultaneously.

| Country | Instrument | Yield (15 May 2026) | Weekly Change | Last at This Level |

|---|---|---|---|---|

| United States | 10-year Treasury | 4.599% | +24 bps | — |

| United States | 30-year Treasury | 5.125% | — | June 2007 |

| United Kingdom | 10-year gilt | Highest since 2007 | — | 2007 |

| United Kingdom | 30-year gilt | Highest since 1998 | — | 1998 |

| Japan | 30-year JGB | All-time record | — | Never |

Carson Group chief macro strategist Sonu Varghese framed the signal directly: bond markets are pricing in the Hormuz closure as an extended condition, not a short-term disruption, and China as unlikely to act to reopen it.

“Bond markets are signalling that Hormuz remains closed and China is unlikely to act to reopen it,” Varghese noted, a reading consistent with the outcome of President Trump’s visit to China this week, the first by a sitting U.S. president since 2017, which concluded without a significant perceived breakthrough on either trade or the Middle East.

When U.S., UK, and Japanese long bonds all sell off in the same week for the same underlying reason, the signal is structural. Positioning built on 2025-era cut expectations requires reassessment.

Three unresolved variables will determine whether the Fed hikes, holds, or eventually cuts:

Reuters reported on 11 May 2026 that Wall Street brokerages have already revised rate cut timing projections in response to persistent inflation and the leadership transition. The consensus position has consolidated: no 2026 cuts are expected, and the distribution of the next move is skewed toward hold or hike.

Any hike from the current 3.50-3.75 percent range would push the top of the band to at least 4.00 percent. Diane Swonk of KPMG U.S. has warned that inflationary effects from the Iran war will intensify before improving, a projection that argues the pressure on the Fed only increases from here.

Wolfe Research’s yield decomposition places only 19 basis points of the roughly 40-basis-point surge in attributable geopolitical risk premium, meaning a structural yield floor will persist even if the Strait of Hormuz reopens fully, as the remaining movement reflects growth repricing and fiscal dynamics that no peace agreement can reverse.

For investors, the asymmetric risk in U.S. rate policy has flipped. Portfolios positioned for cuts are exposed to a hiking cycle that prediction markets now consider the more likely scenario.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

The confluence is what makes this moment different. War-driven inflation, a leadership transition under political pressure, and a genuine market repricing toward hikes do not represent a temporary dislocation. They represent a structural break in the assumptions that governed rate expectations through 2025 and into early 2026.

In the weeks ahead, three developments will determine the trajectory: the BEA’s official April PCE release, Warsh’s first public statements as chair, and any shift in the Iran conflict or Strait of Hormuz situation. Each carries the weight to move markets independently. Together, they will define the new rate cycle.

The Fed’s credibility as an inflation-fighting institution, hard-won through the post-pandemic tightening cycle, is now being tested by a set of forces no single policy lever can fully resolve. How Warsh navigates that constraint will determine whether the Burns parallel remains a historical reference or becomes a real-time replay.

As of 15 May 2026, Kalshi prediction markets placed the probability of a Federal Reserve rate hike before July 2027 at 60 percent, a near-complete reversal from the rate-cut consensus that prevailed at the start of 2026.

The Strait of Hormuz carries roughly 20 percent of the world's daily oil supply, and its closure since approximately 28 February 2026 has pushed WTI crude above $105 per barrel, feeding directly into US energy, freight, food, and petrochemical costs and complicating the Fed's ability to cut rates.

Kevin Warsh is a Trump-aligned nominee confirmed as the next Federal Reserve chair on 13 May 2026; his appointment has raised questions about the institution's independence given the administration's public advocacy for lower interest rates during a period of elevated inflation.

A supply-side shock, like an oil supply disruption, raises prices because physical supply has been removed rather than because demand is excessive, which means the Fed cannot resolve the inflation by cutting rates and instead faces a painful trade-off between fighting inflation and protecting economic growth.

The three most consequential variables are the Bureau of Economic Analysis's official April PCE release, Kevin Warsh's first public statements as Fed chair, and any change in the status of the Strait of Hormuz closure, each of which carries enough weight to independently shift market rate expectations.