Samsung Rout Anchors Global Selloff as Bonds and Stocks Fall Together

4 mins ago

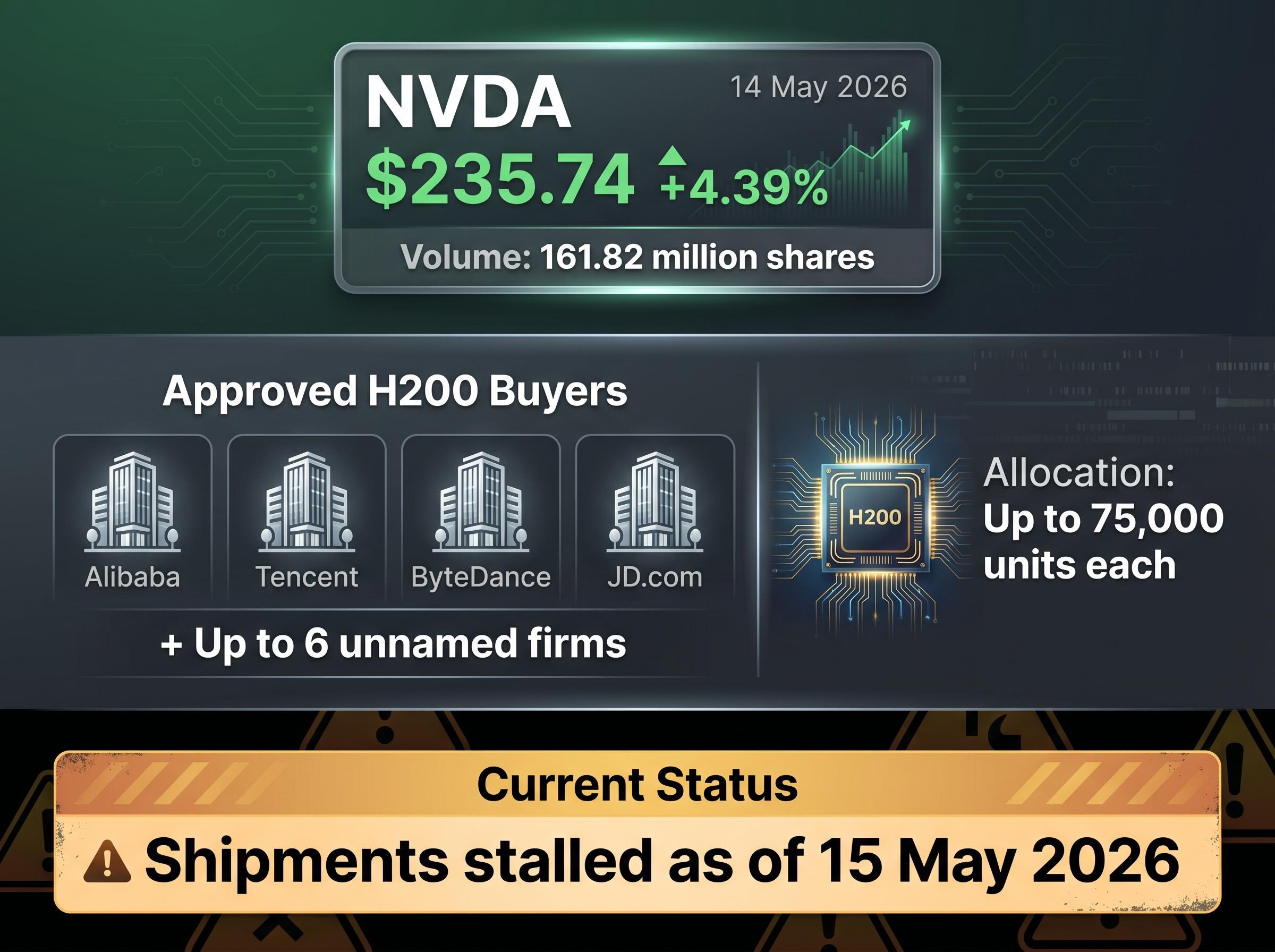

Nvidia closed at an all-time high of $235.74 on 14 May 2026, surging more than 4% after reports that US regulators had approved sales of H200 AI chips to up to 10 Chinese companies, including Alibaba, Tencent, and ByteDance. The clearance arrived the same week Jensen Huang travelled to China alongside President Trump, with a formal Trump-Xi summit unfolding in Beijing on 15 May, making this simultaneously a corporate, regulatory, and geopolitical development with direct implications for Nvidia’s revenue trajectory. What follows covers what the H200 clearance actually means for Nvidia’s financials, how the diplomatic backdrop shaped the policy shift, and whether the record rally reflects durable fundamentals or a sentiment spike that could reverse.

Nvidia shares closed at $235.74 on 14 May 2026, up 4.39% on trading volume of approximately 161.82 million shares. The catalyst was immediate: reports confirmed that US regulators had cleared up to 10 Chinese companies to purchase H200 chips, Nvidia’s second-most capable AI accelerator, with per-company allocations of up to 75,000 units each.

Record close: NVDA $235.74, up 4.39% on 14 May 2026, the highest closing price in the company’s history.

The approved buyers include some of the largest technology companies in China:

The distinction between clearance and delivery, however, is where the headline starts to fracture. As of 15 May 2026, actual shipments of H200 chips to these companies remain stalled despite the regulatory approvals. The stock has already repriced on the approval news, meaning any revenue realisation depends on shipment execution that has not yet occurred. For investors, the gap between “approved” and “shipped” is the load-bearing detail the headline does not carry.

The H200 approvals did not arrive in a regulatory vacuum. They arrived the same week as a formal Trump-Xi summit in Beijing on 15 May 2026, where semiconductor export controls featured directly on the agenda alongside China’s commitments on rare earth exports.

Jensen Huang’s presence in China during the same week as President Trump underscored the corporate-diplomatic alignment behind the clearance. AI chip restrictions and rare earth supply were negotiated as part of a broader trade framework, not as standalone technology-sector decisions. The summit framing suggests the H200 approvals were a concession within a reciprocal deal structure, not a permanent policy reset.

Several flashpoints from the summit remain live, and any one of them could narrow the same diplomatic channel that opened chip sales:

Investors reading the clearance as a permanent regulatory shift should note it is embedded in a negotiation that includes unresolved geopolitical tensions; the same framework that opened access could restrict it again.

The summit agenda risks that remain live, including unresolved Taiwan arms sales, Iran energy disruption, and conditional rare earth commitments, carry very different probability distributions; analysts at Fidelity International flagged low expectations for comprehensive agreement before Day 1 readouts even emerged.

Cantor Fitzgerald raised its Nvidia price target to $350 following the clearance news, the most directly catalyst-linked analyst revision to emerge from the event. Other major brokers, including Goldman Sachs, Morgan Stanley, and Bank of America, have issued upgrades in recent weeks tied to broader AI data-centre demand, though those revisions were not explicitly linked to the H200 China clearance.

The forward-looking revenue case rests on specific numbers. Analyst estimates suggest the H200 clearance could open a China market worth up to $50 billion for Nvidia, with potential chip-sale revenue of approximately $8 billion if deliveries proceed.

China market opportunity: Analysts estimate the H200 clearance could open a market worth up to $50 billion for Nvidia, contingent on shipment execution.

For context, China previously accounted for roughly 20-25% of Nvidia’s data-centre revenue before the 2023-2024 export control tightening. The clearance represents a meaningful shift back toward that revenue base, but the qualifier “if deliveries proceed” is load-bearing. These are forward-looking projections contingent on actual shipment execution, not booked revenue.

Institutional investors at BlackRock and Goldman Sachs have largely reframed China upside as a call option on geopolitical resolution, building their base-case price targets entirely on US and allied market demand while treating any China revenue recovery as an asymmetric bonus rather than a modelled input.

| Analyst / Source | Key Figure | Condition Required |

|---|---|---|

| Cantor Fitzgerald | Price target raised to $350 | Sustained China market access |

| China market estimate | Up to $50 billion | Full clearance execution and delivery |

| Chip-sale revenue upside | Approximately $8 billion | H200 shipments proceed as approved |

AI chip export controls are US government licensing requirements, administered by the Commerce Department, that govern which semiconductor products can be sold to foreign entities. For investors unfamiliar with this regulatory layer, the mechanics are straightforward: companies like Nvidia must obtain clearance before shipping high-performance chips to restricted markets, and that clearance can be granted, modified, or revoked depending on policy priorities.

The Bureau of Industry and Security licensing review policy governs how clearances like the H200 approval are granted on a case-by-case basis, with specific security requirements that companies and foreign buyers must satisfy before shipments can proceed.

The current cycle began with the 2023-2024 tightening, which blocked sales of Nvidia’s A800, H800, and other reduced-performance GPU variants designed specifically for the Chinese market. The sequence has followed a pattern:

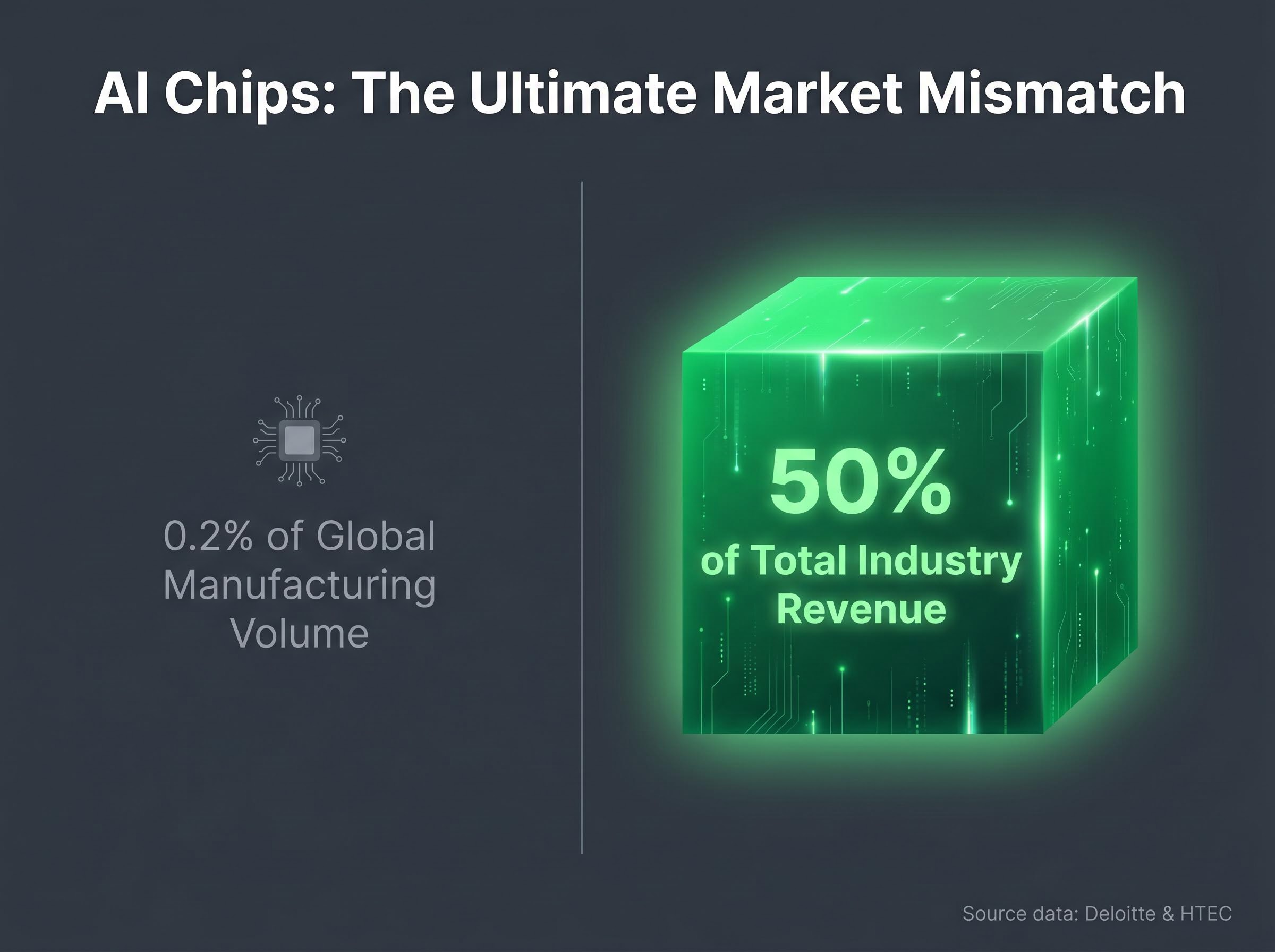

The outsized market impact stems from concentration. AI chips represent just 0.2% of all chips manufactured globally but account for approximately 50% of total semiconductor industry revenue, according to data from Deloitte and HTEC. When China accounted for 20-25% of Nvidia’s data-centre revenue, a policy shift in either direction could directly alter top-line estimates and forward valuation multiples. Thursday’s 4.39% move on a single clearance headline illustrates the scale of repricing these decisions can trigger.

The bull case has measurable foundations. TSMC forecasts the global semiconductor market will exceed $1.5 trillion by 2030; TSMC shares themselves gained 4.5% on 14 May. Deloitte projects global semiconductor sales will reach $975 billion in 2026, representing a 26% growth rate. KPMG’s Semiconductor Industry Confidence Index stands at 63, its third-highest reading in two decades, and 93% of industry leaders surveyed expect revenue growth in 2026.

AI infrastructure spending is approaching $650 billion, and the demand visibility from hyperscaler capital expenditure programmes provides genuine earnings support for the sector’s premium valuations.

A capex-to-revenue lag of 18-24 months sits at the centre of the bear case for premium semiconductor valuations; Morningstar analyst Dennis Li has identified this timing gap as the mechanism by which hyperscaler spending commitments translate into recognised earnings far later than current multiples assume.

Revenue concentration: AI chips account for approximately 0.2% of all chips manufactured but generate roughly 50% of total semiconductor industry revenue.

The counter-case carries equal weight. HTEC argues the “hardware boom is slowing” and the next phase is a software, power, and inference problem rather than a chip-volume story. PwC flags overbuild risk, warning that capital inflows and industrial policy could create margin compression even when top-line demand remains strong. The 0.2% volume to 50% revenue ratio is historically rare, and multiple industry forecasters flag it as a concentration risk rather than a baseline assumption.

| Source | Bullish Indicator | Key Risk Flagged |

|---|---|---|

| Deloitte | $975 billion in 2026 sales, 26% growth | Cyclicality and capex intensity remain high |

| KPMG | Confidence Index at 63; 93% expect growth | Tariffs, trade policy, and energy availability |

| PwC | AI and government subsidies as structural drivers | Overbuild risk and margin compression |

| HTEC | AI chips generate 50% of industry revenue | Hardware boom slowing; software and power phase next |

The stock moved on clearance. The next repricing event is shipment confirmation or denial.

As of 15 May 2026, regulatory approval has been granted but actual H200 deliveries to the 10 approved Chinese companies remain stalled. The gap between approval and execution is the single most actionable near-term variable for investors holding or considering Nvidia at these levels. The $8 billion revenue upside estimate, Cantor Fitzgerald’s $350 price target, and the broader China re-entry narrative all depend on chips physically reaching buyers.

Beijing’s customs block adds a second layer to the approval-versus-delivery gap: even where US licences exist, Chinese buyers face domestic pressure not to act on them, meaning the controlling barrier has shifted from Washington to Beijing rather than disappearing.

The investment thesis from this point forward hinges on three forward-looking factors:

The policy environment that created Thursday’s upside is the same environment that could reverse it. Ongoing monitoring of trade policy developments is now a core component of the Nvidia investment case.

Thursday’s record close is supported by a real regulatory development, real analyst upgrades, and a genuine sector growth backdrop. The fundamentals are not fiction. Yet the upside case, up to $8 billion in China revenue and Cantor Fitzgerald’s $350 target, is contingent on execution variables that have not yet resolved. The downside includes a policy reversal that the same diplomatic channel could produce.

Investors who entered on the clearance news should track the three forward variables identified above: shipment execution, diplomatic continuity, and hyperscaler capex. These are the catalysts that will determine whether the all-time high was a starting point or a peak.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced are forward-looking estimates subject to market conditions and various risk factors.

The H200 is Nvidia's second-most capable AI accelerator, and regulatory clearance for its sale to up to 10 Chinese companies could open a market worth up to $50 billion for Nvidia, representing a meaningful reversal of the 2023-2024 export control tightening that had blocked access to China's AI chip market.

As of 15 May 2026, US regulatory approvals have been granted but actual deliveries remain stalled, with Beijing's customs processes adding a second layer of delay, meaning the controlling barrier has effectively shifted from Washington to Beijing rather than disappearing entirely.

The H200 approvals arrived during the same week as a formal Trump-Xi summit in Beijing on 15 May 2026, where AI chip restrictions and rare earth exports were negotiated as part of a broader trade framework, suggesting the clearance was a concession within a reciprocal deal structure rather than a permanent policy reset.

Cantor Fitzgerald raised its Nvidia price target to $350 as the most directly catalyst-linked analyst revision following the clearance news, while the broader analyst community including Goldman Sachs, Morgan Stanley, and Bank of America have issued upgrades tied to AI data-centre demand more generally.

The three primary risks are failure to execute H200 shipments to approved Chinese buyers, a breakdown in the Trump-Xi diplomatic framework due to unresolved tensions over Taiwan or energy flows, and a deceleration in hyperscaler AI data-centre capital expenditure, all of which could erode the revenue upside currently priced into the stock.