How Zero Commissions Changed the Maths on Thematic ETFs

2 hrs ago

Australia’s approach to taxing capital gains is about to change in a way it has not changed since 1999. The federal government’s 2026-27 Budget has replaced the long-standing 50% flat CGT discount with a CPI-based indexation model, effective 1 July 2027, restoring a method last used in the era before the Howard government simplified the system more than a quarter of a century ago. For Australians holding investment properties, shares, and other CGT assets, the shift rewrites the calculation that determines what they owe when they sell. This article explains, in plain terms, how the new calculation works, which assets fall under the new rules, what the transitional provisions mean for holdings purchased before 2027, and who is likely to pay more or less tax under the reformed regime. It also covers what remains unresolved and what investors can do before the start date arrives.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Under the current system, any individual or trust that holds a CGT asset for more than 12 months receives a 50% reduction in the taxable gain before their marginal tax rate is applied. The mechanism is simple: sell an asset for $200,000 more than the purchase price, and only $100,000 is taxable. The discount applies regardless of how much of that gain was driven by inflation and how much represented a genuine real return.

That simplicity is exactly what the government argues is the problem. Treasury has framed the reform as restoring CGT to its “original intent”: taxing real gains only. Under the existing discount, an investor whose property rose in value purely because of inflation still pays tax on half of a nominal gain that delivered no real purchasing power increase.

The 2026-27 Budget announcement also introduced a parallel restriction on negative gearing for established residential properties acquired after 12 May 2026, meaning property investors face a compounding structural deterioration in after-tax returns rather than a single CGT change in isolation.

The replacement is not a new idea. CPI-based cost base indexation was the standard method from 1985 to 1999, when Australia first introduced CGT. The government is returning to that earlier approach rather than inventing a new one.

Pitcher Partners has described the change as a “seismic shift” in the CGT landscape, reflecting the breadth of what has been announced.

The core structural changes include:

The concept is straightforward. Instead of discounting the gain by a flat 50%, the new system adjusts the original purchase price upward to reflect inflation over the holding period. Only the difference between this inflation-adjusted cost base and the sale price is taxable.

The formula works as follows: the indexed cost base equals the original cost base multiplied by the ratio of the Consumer Price Index (CPI) at the time of sale to the CPI at the time of purchase. If inflation has been significant over the holding period, the indexed cost base rises substantially, and the taxable gain shrinks. If real price growth has been strong relative to inflation, the taxable gain may actually be larger than it would have been under the old discount.

Budget documentation confirms that indexation will use CPI “in a similar manner” to the pre-1999 rules. A 30% minimum tax rate applies to the resulting net capital gain, meaning sellers pay either their marginal rate or 30%, whichever is higher. The indexation benefit is available only for assets held more than 12 months, preserving the existing threshold for concessional treatment. Newly constructed residential properties are excluded from the revised treatment.

The step-by-step calculation runs as follows:

| Method | What is taxed | Rate applied | New builds included? |

|---|---|---|---|

| Old 50% discount | 50% of the nominal capital gain | Seller’s marginal tax rate | Yes |

| New CPI indexation | Gain above the inflation-adjusted cost base (real gain only) | Marginal rate or 30%, whichever is higher | No (excluded from revised treatment) |

CGT was introduced in Australia on 20 September 1985. From that date until 1999, the standard method for calculating a capital gain was CPI-based indexation. Investors tracked a cost base for each asset and applied published CPI ratios, available from the ATO for each quarter, to determine the inflation-adjusted purchase price at the time of sale. The taxable gain was the difference between the sale price and the indexed cost base.

The system worked, but it was administratively heavier than what replaced it. In 1999, the Howard government introduced the 50% flat discount as a simpler alternative, and indexation was frozen. Assets acquired before that date retained the option to use either method, but all new acquisitions fell under the discount.

The ATO’s existing pre-1999 indexation guidance is now being cited by tax practitioners as the likely template for the post-2027 regime. Budget documentation confirms the ATO will develop guidance and calculators drawing on those earlier methods. However, no dedicated ATO practical guide or calculator for the new system has been published as of mid-May 2026.

The ATO indexation method guidance for pre-1999 assets sets out the precise CPI ratio calculation that practitioners are treating as the operational template for the post-2027 regime, given that Budget documentation confirms the new system will work in a similar manner to those earlier rules.

Despite the policy announcement, no draft legislation or explanatory memorandum has been released for consultation or introduced into Parliament. Both KPMG and Pitcher Partners have explicitly flagged this absence and are calling for early consultation. The following questions remain open:

Until implementing legislation is released, each of these questions represents a genuine gap in the framework that advisers and investors cannot plan around with confidence.

Whether an investor pays more or less tax under indexation depends on two variables: how much of the asset’s price growth was real (above inflation) and how much was nominal (driven by inflation). Investors can locate themselves in this framework relatively quickly.

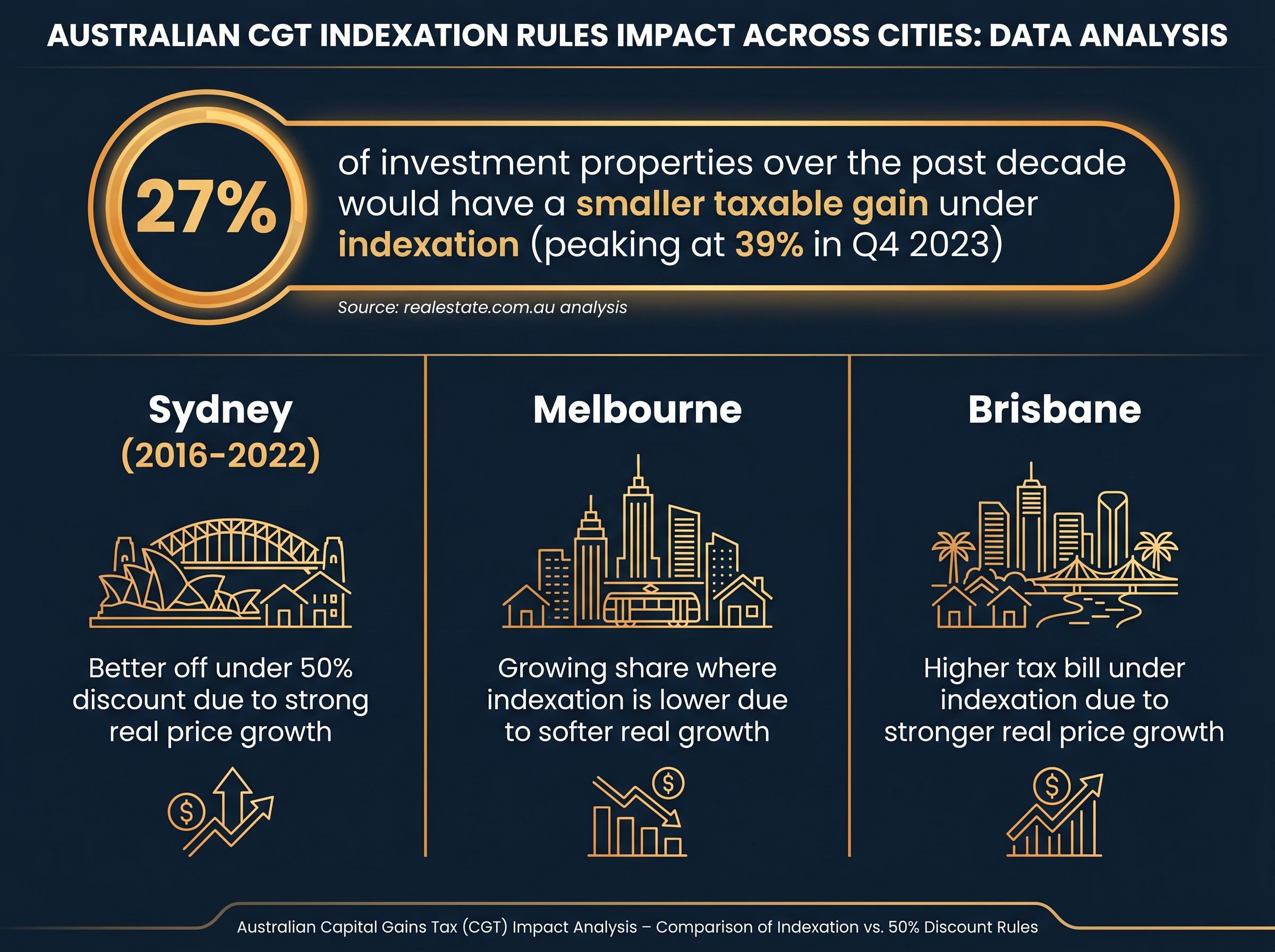

According to analysis from realestate.com.au, roughly 27% of investment properties that generated a capital gain over approximately the past decade would have had a smaller taxable gain under indexation than under the 50% discount.

That figure peaked at 39% in Q4 2023, approximately 12 months after Australia’s headline inflation peaked, illustrating how the balance between the two methods shifts with the inflation cycle.

City-level data sharpens the picture. Sydney sellers from 2016 to 2022 would generally have been better off under the old flat discount, reflecting strong real price growth that outpaced inflation. Melbourne has seen a growing share of sales where indexation would have produced a lower taxable gain, consistent with softer real growth in recent years. Brisbane sellers are more likely to face a higher tax bill under indexation, given that city’s stronger real price growth over the period.

Perpetual frames the logic simply: high real growth means a higher taxable gain under indexation; high inflation relative to real growth favours indexation.

Higher effective rates also create a lock-in effect on portfolio reallocation: investors with large unrealised gains are incentivised to hold rather than sell and reinvest into more productive assets, which cuts against the government’s stated goal of redirecting capital toward new construction and productive investment.

| Investor profile | Likely outcome under indexation vs 50% discount | Key driver |

|---|---|---|

| High-growth city property (strong real gains) | Higher taxable gain under indexation | Real growth exceeds inflation adjustment |

| Inflation-tracking, low-growth property | Lower taxable gain under indexation | Inflation adjustment absorbs most of the nominal gain |

| Complying super fund holder | Retains one-third discount (outside new regime) | Structural carve-out for super funds |

| Pre-CGT long-held asset (pre-1985) | New tax liability from 1 July 2027 onward | Loss of full CGT exemption; gains measured from 2027 deemed cost base |

Past performance does not guarantee future results. The relationship between inflation and real growth varies across markets, holding periods, and economic cycles. Individual outcomes will differ.

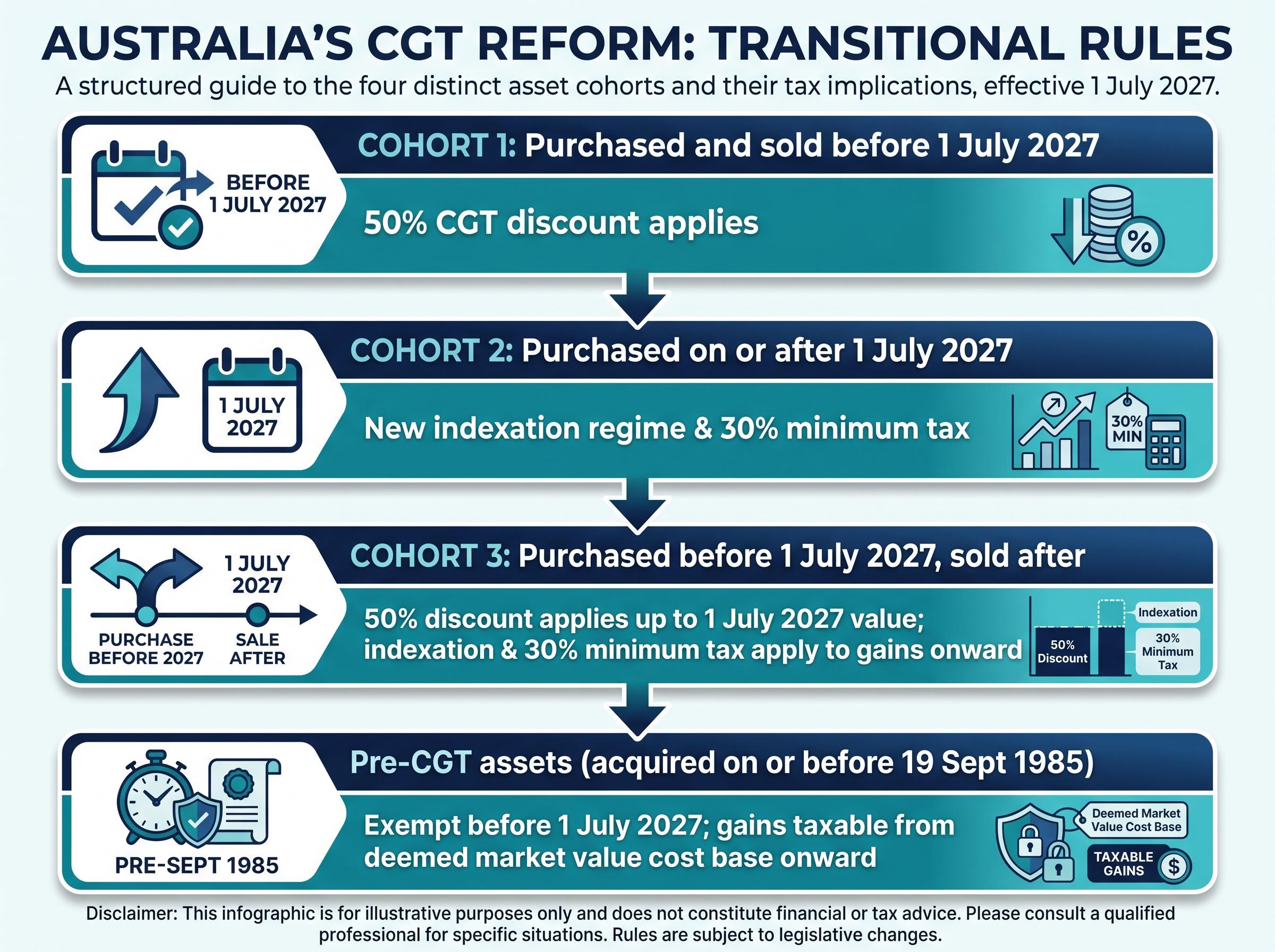

The Budget outlines a three-period framework that determines which rules apply to any given asset:

For transitional assets, the calculation effectively splits the gain into two periods. Treasury’s examples reference a “specified formula method” as an alternative to full market valuation for determining the 2027 value, but practitioners have raised concerns that formula methods may lock in unfavourable cost bases for some investors.

Assets acquired on or before 19 September 1985 have been fully exempt from CGT since the tax was introduced. That exemption ends on 1 July 2027.

KPMG has described this aspect of the reform as “remarkable”, reflecting the scale of the change for long-held family properties, farms, and inherited investment assets.

From 1 July 2027, gains on pre-CGT assets become taxable, measured from a deemed cost base equal to the asset’s market value at that date. Gains accrued before 1 July 2027 remain exempt.

The valuation chosen on that date becomes the permanent cost base for all future taxable gains, creating significant valuation risk. Pitcher Partners has warned about the potential for ATO disputes if valuations are challenged, particularly for illiquid assets such as family businesses and rural properties. Advisers are urging pre-CGT asset holders to consider whether crystallising tax-free gains before 2027 (by selling) is preferable to accepting the new regime and the valuation burden it imposes.

Pitcher Partners CGT reform analysis identifies the absence of draft legislation as the central implementation risk, noting that without a formal explanatory memorandum, advisers and investors cannot plan with confidence around the transitional valuation requirements for pre-CGT assets.

The core decision facing investors now is whether to sell before 1 July 2027 under the 50% discount or hold into the new regime. That calculation depends entirely on individual asset profiles, marginal tax rates, and expected future growth. There is no universal answer.

One structural consideration stands out. Complying superannuation funds retain the one-third CGT discount for holdings over 12 months and sit outside the 30% minimum tax that applies to individuals and most trusts. This creates a structural incentive to hold long-term growth assets inside super where possible.

The structural incentive to hold assets inside superannuation extends to listed equities as well, where ASX sectoral rotation toward income stocks with franked dividends is gaining traction as investors recalibrate their portfolios around the removal of the CGT discount and the relative appeal of fully franked yield over capital growth strategies.

Stockspot has observed that some investors will bring forward disposals into the pre-2027 window, particularly where assets have already realised most of their expected capital growth.

Budget projections anticipate that overall investment in established property will moderate, with the exclusion of new residential builds from the revised treatment likely redirecting some capital toward new construction. The Property Council of Australia has described the package as a “mixed bag”, recognising the principle behind indexation while flagging concern about combined effects with tighter negative gearing rules.

Key actions practitioners are recommending investors consider before 1 July 2027 include:

The professional tax community has reached a broad consensus on one point: indexation is more principled than the flat discount as a method for taxing capital gains. Taxing real gains rather than nominal ones aligns CGT with its stated purpose. Most practitioners accept the intellectual foundation of the reform.

The consensus fractures on implementation. The Tax Institute of Australia has called for draft legislation and explanatory memoranda to be released well ahead of 1 July 2027. Both KPMG and Pitcher Partners have explicitly stated that implementing legislation has not been released, and the eight key questions identified by the profession remain unanswered. The ATO has confirmed it will develop guidance and calculators drawing on pre-1999 methods, but no timeline for draft legislation has been confirmed as of mid-May 2026.

The practical impact of this reform will vary dramatically depending on individual circumstances. No general rule applies across all investors or all asset types. The period between now and 1 July 2027 is the window in which investors, advisers, and the ATO must resolve the details that will determine whether this reform achieves its stated intent. Policy is announced. Legislation is not. That gap is where the real work remains.

From 1 July 2027, Australia replaces the 50% flat CGT discount with CPI-based cost base indexation, meaning only the real gain above inflation is taxable, and a 30% minimum tax rate applies to net capital gains for individuals and most trusts.

The indexed cost base is calculated by multiplying the original purchase price by the ratio of the CPI at the time of sale to the CPI at the time of purchase, with only the difference between this inflation-adjusted cost base and the sale price being taxable.

Assets purchased before 1 July 2027 but sold after that date are subject to transitional rules: the 50% discount applies to gains accrued up to the 1 July 2027 value, while indexation and the 30% minimum tax apply only to gains accrued from that date onward.

The full CGT exemption for assets acquired before 20 September 1985 ends on 1 July 2027, and gains from that date onward become taxable using the asset's market value on 1 July 2027 as the permanent cost base.

Practitioners recommend modelling tax outcomes under both the current discount and the new indexation method for each asset, obtaining independent valuations for pre-CGT assets, reviewing whether superannuation structures offer a more tax-efficient vehicle, and monitoring ATO guidance as draft legislation is released.