Woolworths: Strong Sales, Shrinking Profits, Slim Upside

2 hrs ago

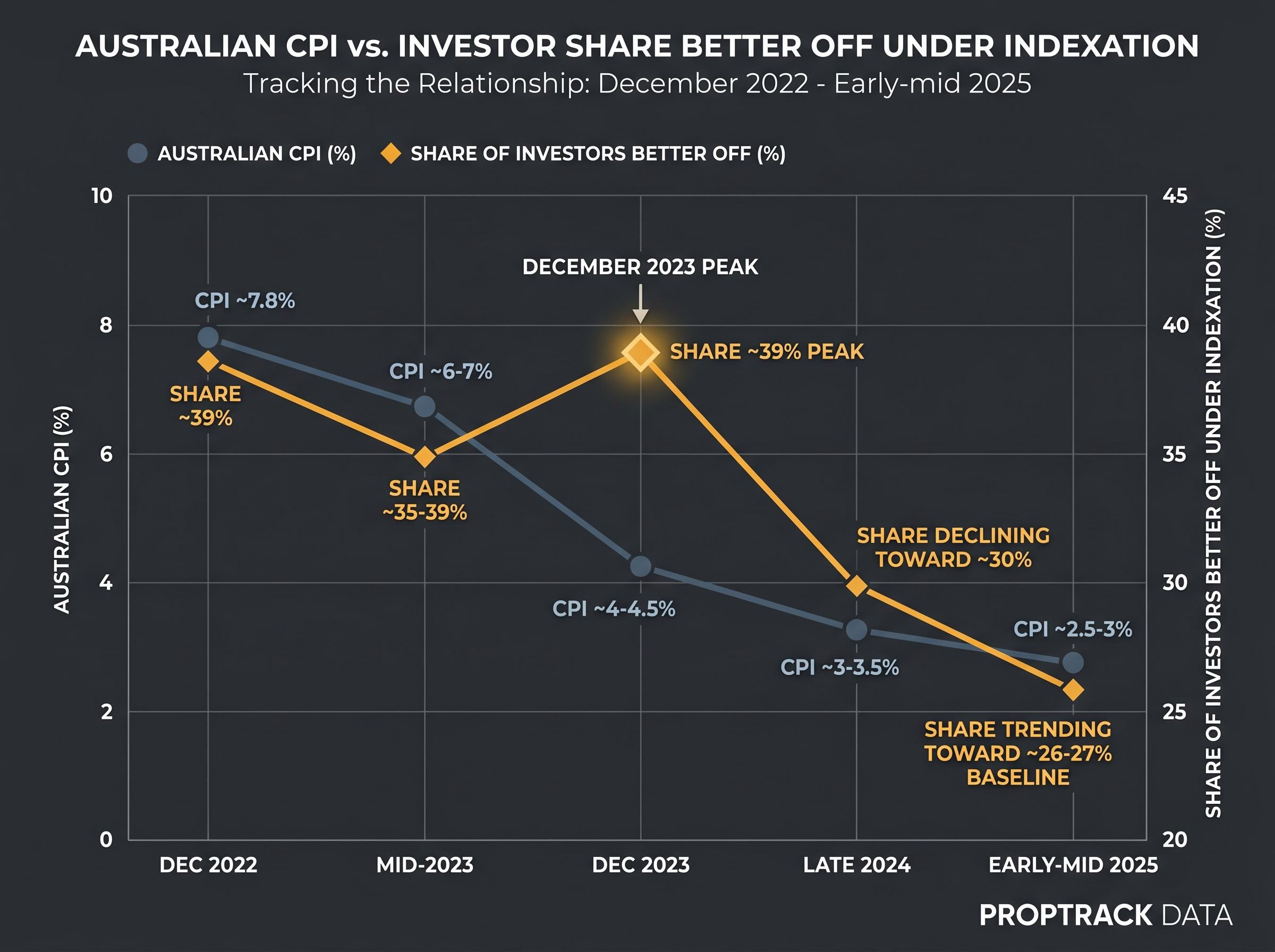

Australia’s capital gains tax regime is about to undergo its most significant structural change since 1999. From 1 July 2027, the 50% CGT discount for individuals, trusts, and partnerships on assets held longer than 12 months will be replaced by CPI indexation of the cost base, paired with a minimum 30% tax on net real gains. The reform has drawn sharp reactions from both sides. Yet the distributional reality is more nuanced than most coverage suggests. PropTrack analysis of the past decade found that roughly 27% of property investors generating capital gains would have paid less tax under indexation than under the flat discount, a share that peaked at 39% in Q4 2023, roughly 12 months after Australia’s inflation peak. This analysis maps which investor cohorts and which cities are genuinely better or worse off, using CPI trajectories and city-level price growth data to move beyond the broad headlines into the specific mechanics that determine individual outcomes.

Under the current 50% discount, half the total nominal gain is sheltered from tax regardless of how much of that gain was simply inflation eroding purchasing power. Under CPI indexation, the cost base rises with the consumer price index, meaning only the portion of the gain above cumulative inflation is taxed. That taxed portion, however, is taxed in full and subject to a 30% minimum rate.

The outcome for any individual investor reduces to one spread: nominal price growth minus CPI. Where that spread is large (strong real growth well above inflation), the 50% discount usually produces a lower tax bill. Where the spread is narrow or negative (nominal growth tracking near or below inflation), indexation wins because it can shrink the taxable gain to near zero.

The Treasury’s Budget 2026-27 factsheet illustrates the mechanics directly: an investor selling after two years of 2.5% inflation faces a taxable gain of $34,688 under indexation, compared with $30,000 under the 50% discount at a 47% marginal rate.

The 30% minimum tax is an underappreciated second lever. Investors who currently realise gains in low-income years at marginal rates well below 30% (those with taxable income below approximately $45,000 in 2028) face a hard floor under the new regime regardless of how inflation-adjusted their gain appears. Pitcher Partners identifies three transitional scenarios: assets sold entirely before 1 July 2027 (full 50% discount); assets sold entirely after (full indexation plus 30% minimum); and assets bought pre-2027 and sold after, where a split treatment uses the 1 July 2027 valuation as the dividing line.

The split-calculation rule that applies to assets bought before 2027 and sold after introduces a valuation dependency that most investors have not yet modelled: the 1 July 2027 market value becomes the dividing line between gains taxed under the old discount and gains taxed under the new indexation regime, making that single figure one of the most consequential numbers in an investor’s tax planning.

| Investor Profile | Nominal Growth | CPI Indexed Gain | Which Regime Wins |

|---|---|---|---|

| High real growth (e.g., Brisbane house, 12% annual growth) | Large nominal gain | Large taxable real gain remains after indexation | 50% discount |

| Inflation-tracking growth (e.g., Melbourne apartment, 2-3% growth) | Modest nominal gain | Near-zero real gain after indexation | CPI indexation |

| Low-income investor in any market (marginal rate below 30%) | Any level | 30% floor applies regardless | 50% discount (current low rate preserved) |

PropTrack’s decade-long analysis offers the closest available market-wide quantification. Roughly 27% of capital-gain-generating property sales over the past ten years would have produced a lower taxable gain under indexation than under the 50% discount. That is a material minority, not a rounding error.

The share was not static. Through the pre-pandemic years, it hovered around a 26% baseline, reflecting the structural floor of markets and sub-segments where real returns were genuinely flat. Then inflation moved.

CPI peaked at approximately 7.8% year-on-year in December 2022. It moderated to roughly 4-4.5% by December 2023, eased further to approximately 3-3.5% by late 2024, and has trended toward 2.5-3% in early-to-mid 2025. The spike, and its lag through holding periods, reshaped the calculus.

The ABS CPI data for the December 2022 quarter confirmed the annual inflation rate reached 7.8 per cent, the precise peak that reshaped the indexation calculus for investors who bought near that period and subsequently held into modest nominal growth conditions.

By Q4 2023, PropTrack data showed 39% of investors would have paid less tax under indexation, the highest share in the dataset.

The logic was direct. Investors who bought near or during peak inflation, held for 12-18 months, and sold into modest nominal growth found their real gain was minimal once the cost base was indexed upward. Under the 50% discount, half that inflation-driven nominal gain would still have been taxable.

Three distinct phases of the CPI cycle explain the pattern:

City-level price trajectories explain part of the picture. Two additional variables, holding period and marginal tax rate, determine the rest, yet most public commentary on this reform treats them as afterthoughts.

Indexation’s relative merit is a function of cumulative CPI over the holding period. A longer hold through a high-inflation period means more cumulative cost base adjustment; a short hold captures only a slim inflation uplift. BDO’s analysis highlights the inversion this creates.

Under the 50% discount, assets that grow strongly over short horizons can produce a lower inflation-adjusted tax liability than longer holds. Indexation reverses some of this dynamic, rewarding patience in low-real-growth environments while penalising short, high-growth bursts.

The marginal rate variable adds a second axis. A top-rate taxpayer at 47% sits well above the 30% minimum floor and experiences the reform primarily as a shift in how gains are measured. A low-income retiree or part-time worker whose marginal rate is 19% faces the floor as a binding constraint, one that eliminates the long-standing strategy of timing gains to low-income years. Treasury’s own modelling found that for top-rate taxpayers over the past 20 years, effective tax rates on nominal gains under indexation would generally have been 20-30%, sometimes higher where real returns are large.

Four investor profiles illustrate the matrix most clearly:

Pre-CGT assets (acquired before 1985) are also brought into the regime, creating an additional cohort of affected investors who had previously been entirely exempt from capital gains tax.

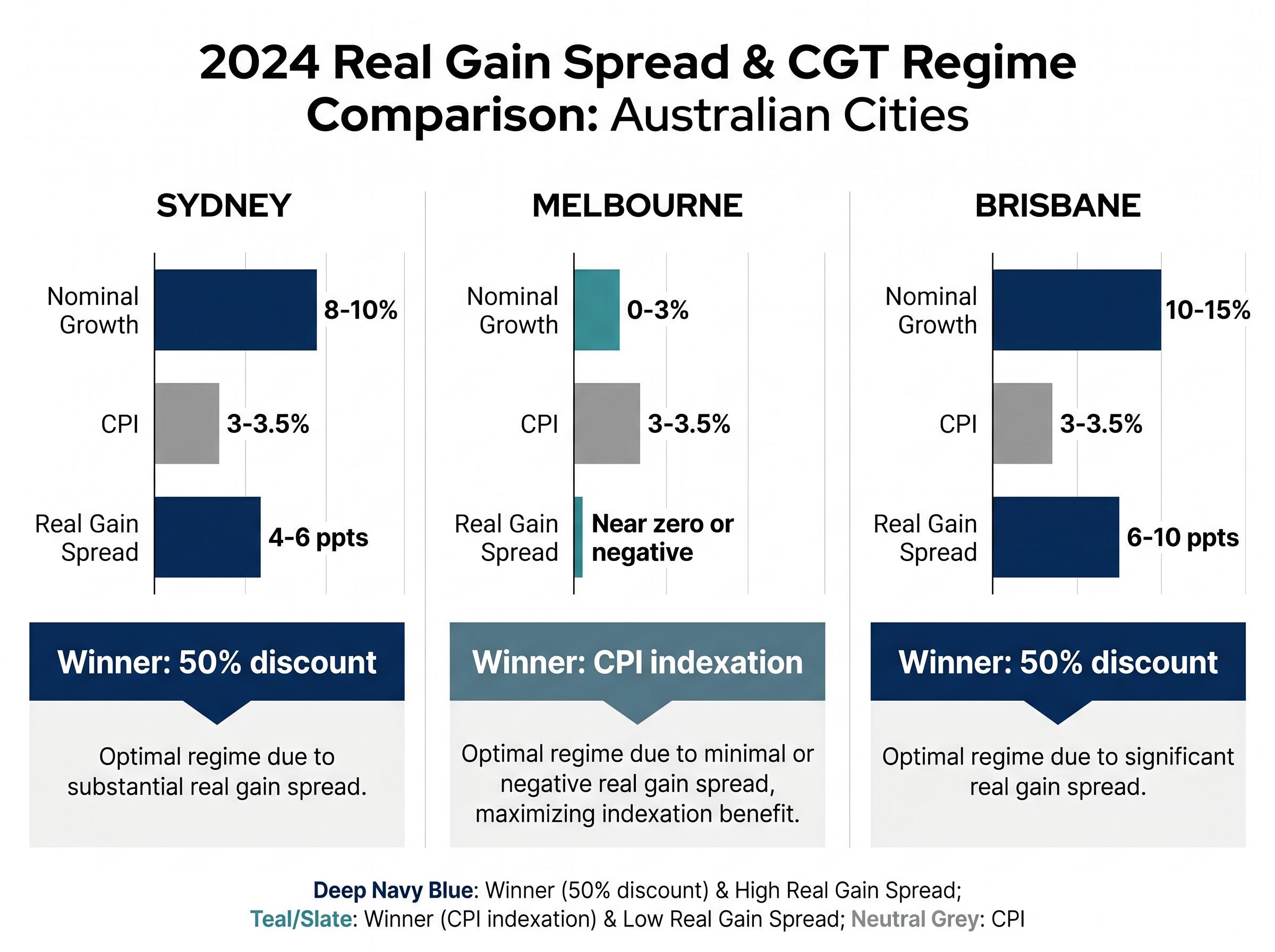

National figures mask the divergence that matters most to individual investors. The spread between nominal property growth and CPI varies dramatically across Australia’s three largest eastern seaboard markets, producing fundamentally different reform outcomes depending on where an investment property sits.

The PropTrack Home Price Index for December 2024 recorded annual growth of approximately 3.4% in Sydney, negative 2.5% in Melbourne, and 11.4% in Brisbane, figures that confirm the divergent real-gain spreads driving the city-level CGT outcome differences discussed here.

Sydney remains a high-spread market. Dwelling values rose approximately 8-10% through 2024 and were tracking roughly 6-8% on a 12-month view in early 2025. Against CPI of approximately 3-3.5%, the spread sits at roughly 4-6 percentage points. For an investor who bought in 2023 and sells post-2027, indexation offers a modest 3-4% cost base adjustment while the remaining real gain is fully taxed. The 50% discount, which halves the entire nominal gain, remains the more generous treatment for most recent Sydney investors.

Melbourne presents the strongest domestic case for indexation. Most indices show 0-3% dwelling growth through 2024, with early 2025 readings flat to slightly negative in some measures. Against CPI of 3-3.5%, the spread is near zero or negative in many sub-markets.

The implication is direct: under indexation, real gains approach zero, meaning CGT liability could be negligible. Under the 50% discount, half the inflation-driven nominal gain would still be taxed. Melbourne investors are the least urgently motivated to sell before 1 July 2027.

Brisbane sits at the opposite end. Annual dwelling growth ran at approximately 10-15% through 2024, with early 2025 still showing 8-12% gains. The spread between nominal growth and CPI stretches to 6-10 percentage points.

Indexation strips out only the 3-4% inflation component, leaving a large real gain fully taxed at the 30% minimum floor or higher. Brisbane investors who captured 2020-2024 growth are among the clearest losers under the new regime, and disproportionate pre-2027 selling pressure from this cohort is a reasonable expectation.

| City | Approx. 2024 Nominal Growth | Approx. CPI (2024) | Real Gain Spread | Likely Winning CGT Regime (2023-bought property) |

|---|---|---|---|---|

| Sydney | 8-10% | 3-3.5% | 4-6 ppts | 50% discount |

| Melbourne | 0-3% | 3-3.5% | Near zero or negative | CPI indexation |

| Brisbane | 10-15% | 3-3.5% | 6-10 ppts | 50% discount |

The transitional period between now and 1 July 2027 contains the highest-value planning window of the entire reform. Four priority actions, in sequence, give investors a concrete framework.

The lock-in effect created by higher effective CGT rates adds a second-order dimension to the sell-before-2027 calculus: investors who choose not to sell before the cutoff may subsequently find themselves reluctant to realise gains at any point under the new regime, concentrating portfolio risk in assets they would otherwise have rotated out of.

Investors whose taxable income sits below approximately $45,000 can currently realise discounted gains at marginal rates well under 30%. Under the new regime, the 30% floor eliminates this strategy entirely.

Income-support recipients (such as Age Pension recipients) may be exempt, but most part-time workers and early retirees are not. For this cohort, realising gains before 1 July 2027 while the 50% discount and their low marginal rate both apply may represent the most material tax-planning opportunity of the reform.

The political timing of this reform matters as much as its design. CPI peaked at approximately 7.8% in December 2022, the moment when indexation would have sheltered the largest number of investor cohorts. By early-to-mid 2025, inflation has eased to approximately 2.5-3%, trending toward the RBA’s 2-3% target band. The regime takes effect on 1 July 2027, in conditions that are least favourable to indexation’s own logic.

| Period | Approx. CPI (Year-on-Year) | Approx. Share of Investors Better Off Under Indexation |

|---|---|---|

| December 2022 | ~7.8% | Rising toward 39% |

| Mid-2023 | ~6-7% | ~35-39% |

| December 2023 | ~4-4.5% | ~39% (peak) |

| Late 2024 | ~3-3.5% | Declining toward ~30% |

| Early-mid 2025 | ~2.5-3% | Trending toward ~26-27% baseline |

As inflation stabilises near 2-3%, any market with nominal property growth above approximately 4-6% will likely produce a worse outcome under indexation for most marginal-rate investors. The 50% discount halves the entire nominal gain; a 2-3% CPI adjustment strips out a fraction of it.

No publicly available city-level Treasury modelling exists yet, making independent scenario analysis the primary available tool for investors assessing their specific exposure to the reform.

The longer-term picture carries genuine uncertainty. The RBA’s ability to maintain inflation at target, future supply shocks, or a sustained period of sub-inflation property growth (as Melbourne demonstrated in 2023-2024) could all shift the calculus again. The regime’s distributional effects are not fixed; they will evolve with the inflation cycle.

The empirical record, city-level trajectories, and forward CPI outlook converge on a clear, if qualified, verdict. For the majority of Australian property investors, particularly those in Sydney and Brisbane with strong real gains and those on low marginal rates facing the 30% floor, this change represents a higher effective CGT burden than the existing 50% discount. PropTrack’s 27% baseline provides the realistic measure: roughly three-quarters of investors generating a capital gain will face a higher or equivalent tax liability under indexation.

The genuine minority who benefit should not be dismissed:

The most consequential variable is not the choice of regime itself but the quality of the 1 July 2027 valuation. This single data point determines how much of an investor’s total gain is sheltered under the discounted pre-2027 rules versus exposed to the indexed post-2027 rules. Complementary state-level reforms, including zoning, planning, and stamp duty, remain unaddressed by this policy, meaning the supply-side structural constraints on Australian housing persist regardless of CGT settings.

The CGT changes sit within a broader package of three reform pillars introduced by the 2026-27 Federal Budget, with the negative gearing ring-fence and a 30% minimum tax on discretionary trust distributions operating alongside the CGT discount replacement to reshape the after-tax calculus for every structure through which Australians currently hold investment property.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections discussed in this article are subject to market conditions and various risk factors.

—

From 1 July 2027, the existing 50% CGT discount for individuals, trusts, and partnerships on assets held longer than 12 months will be replaced by CPI indexation of the cost base, paired with a 30% minimum tax on net real gains.

Investors in flat-growth markets like Melbourne, those who held property during the 2022-2023 inflation spike, and investors with near-zero real gains are most likely to pay less tax under indexation compared to the 50% discount.

Investors whose taxable income falls below approximately $45,000 currently benefit from realising discounted gains at marginal rates well below 30%, but the new 30% minimum floor eliminates this strategy entirely after 1 July 2027.

For assets bought before 2027 and sold after, the 1 July 2027 market value acts as the dividing line between gains taxed under the old 50% discount and gains taxed under the new CPI indexation regime, making it one of the most consequential figures in an investor's tax planning.

Brisbane and Sydney investors with strong real gains above CPI are likely worse off under indexation, while Melbourne investors facing near-zero or negative real growth relative to CPI could see their taxable gain reduced to near zero under the new regime.