EOS Shares Jump 4% as MARSS Wins €102M Counter-Drone Deal

2 hrs ago

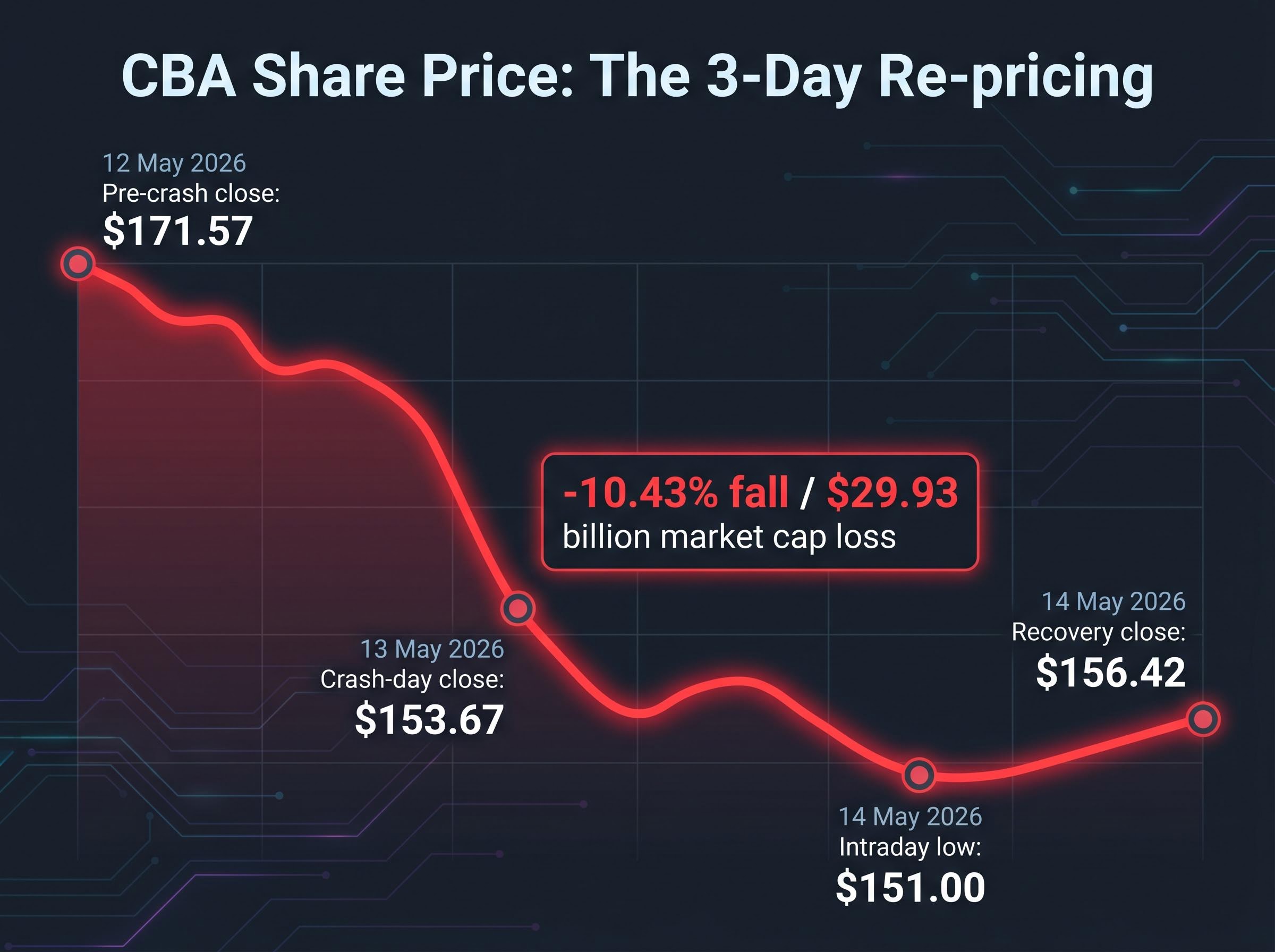

Commonwealth Bank of Australia shed 10.43% of its value in a single session on 13 May 2026, erasing approximately $29.93 billion in market capitalisation and surrendering its position as the ASX’s most valuable listed company to BHP for the first time in years. The CBA share price fall was not routine volatility. It was a repricing event triggered by a quarterly earnings update that missed consensus, a deliberate shift in credit provisioning that signalled management caution about the economy, and a federal budget that targeted the bank’s core growth engine: investor mortgages. What follows explains exactly what the Q3 FY26 numbers showed, why those numbers hit a stock priced for perfection so hard, and where brokers and analysts now see CBA heading from here.

The numbers tell the story in sequence. CBA closed at $171.57 on 12 May 2026. Twenty-four hours later, the stock closed at $153.67, a 10.43% fall that marked the bank’s worst single-session performance since COVID-19 turmoil and, by some measures, its worst day since the 1991 listing.

Approximately $29.93 billion in market capitalisation vanished in one session. CBA’s post-crash market cap of roughly $257.16 billion placed it well behind BHP, ending a period in which CBA had held the ASX’s top-cap position.

The pre-crash rally in bank shares through April 2026 had already attracted widespread institutional scepticism, with the ASX 200 Financials sector up 8.87% year to date even as unanimous sell ratings and price targets clustered 20-25% below market prices signalled that momentum and fundamentals had decoupled well before the Q3 result arrived.

The selling did not stop at the close. On the morning of 14 May, CBA hit a fresh 52-week intraday low of $151.00 before recovering through the session to close at $156.42. As of mid-May 2026, the stock remains approximately 8-10% below its pre-result level.

| Date | Event | Price | Change |

|---|---|---|---|

| 12 May 2026 | Pre-crash close | $171.57 | Baseline |

| 13 May 2026 | Crash-day close | $153.67 | -10.43% |

| 14 May 2026 (morning) | Intraday low | $151.00 | New 52-week low |

| 14 May 2026 (close) | Recovery close | $156.42 | Partial recovery |

The quarterly result was not a disaster. It was a miss, and for a stock priced the way CBA was priced, that distinction barely mattered.

CBA reported Q3 cash net profit after tax (cash NPAT) of $2.7 billion, up approximately 4% on the prior corresponding period. Statutory NPAT came in at $2.6 billion. The miss against analyst consensus was modest, approximately 1-2%, but for a stock trading at a premium to every Big Four peer, even a small shortfall carried weight.

The operational picture showed a franchise still growing:

Net interest margin (NIM) was broadly stable excluding non-recurring tailwinds. Operating income came in flat.

What unsettled the market was not the profit line. It was the provision line.

Loan impairment expense hit $316 million, including a deliberate $200 million collective provision top-up (approximately 8 basis points of gross loans). Management explicitly increased the weighting of its downside economic scenario in the provisioning model, citing “heightened geopolitical and macroeconomic uncertainty.”

Corporate troublesome and non-performing exposures rose to $6.5 billion, representing 0.94% of total committed exposure, up from 0.90%. That trajectory, combined with the provision language, signalled that CBA’s leadership sees real and rising risk in the economy, not merely accounting caution.

“We are closely monitoring the impacts of the Middle East conflict and other factors on our customers and the economy. Our actions this quarter, including strengthening provisions, reflect a prudent approach to managing emerging risks.”

Matt Comyn, CEO, Commonwealth Bank of Australia

A $2.7 billion quarterly profit does not, on its face, explain a $30 billion market cap wipeout. Valuation does.

Before the result, CBA traded at a price-to-earnings and price-to-book ratio well above its Big Four peers. That premium was the market’s bet that earnings growth would remain strong and credit conditions would stay benign. When neither condition was fully met, the premium unwound violently.

Flat operating income and a 1-2% earnings miss are inconsequential for most stocks. For CBA at $171.57, they were sufficient to trigger a significant derating because the price already reflected an outcome the quarter did not deliver.

The broker community had been signalling this vulnerability for months. Before the Q3 result, major brokers already held bearish ratings with price targets clustered well below the market price:

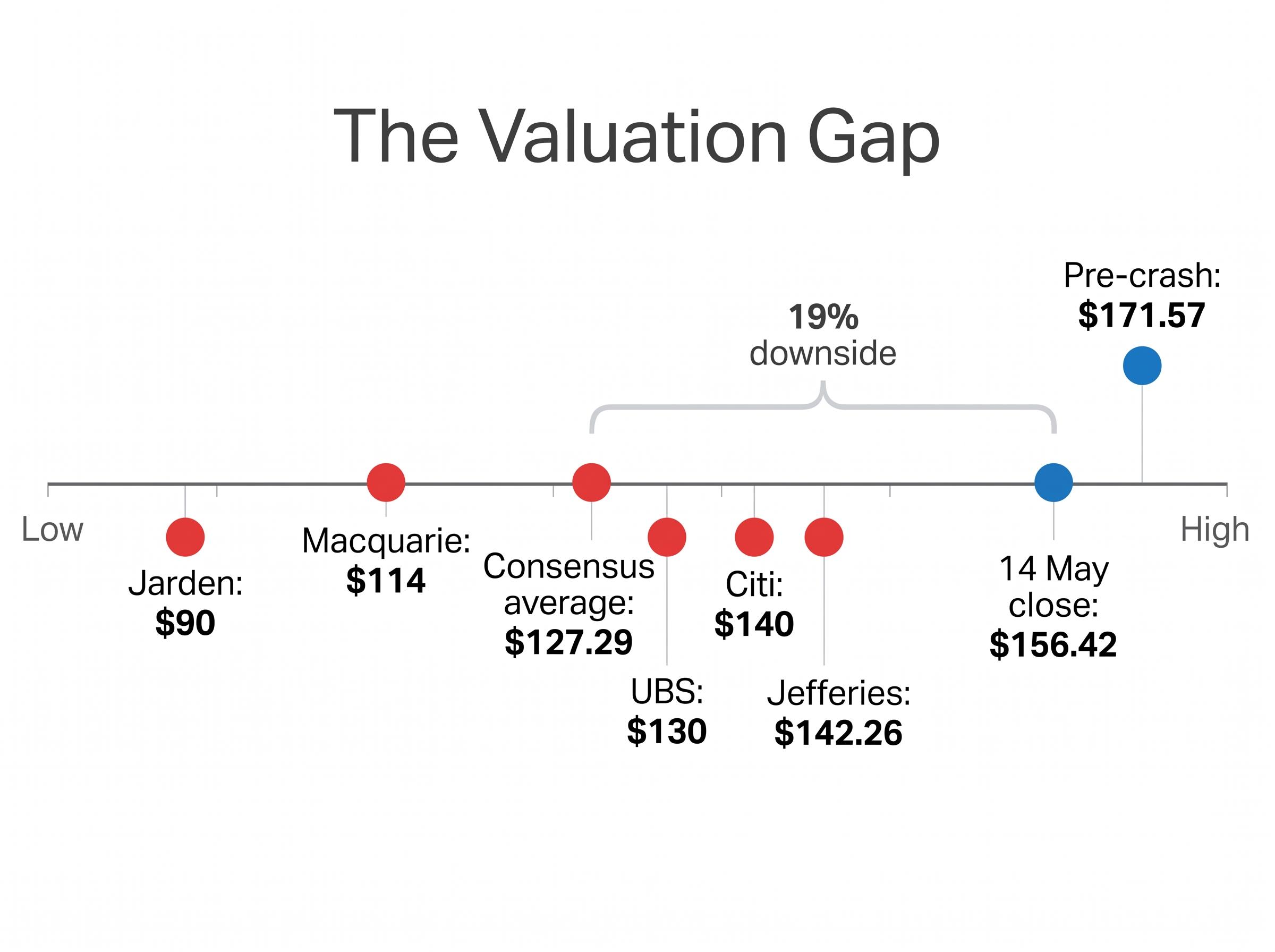

CBA’s premium valuation relative to every Big Four peer was not a secret entering the Q3 result; all 14 covering analysts held sell ratings with a consensus 12-month target of approximately $125.95, implying that the market price had been pricing in an outcome the business was structurally unlikely to deliver.

The gap between a $171.57 share price and broker targets ranging from $114 to $142.26 told investors that institutional opinion considered the valuation unsustainable. The Q3 result provided the catalyst.

The earnings miss arrived on the same day as a structural policy headwind. The 2026-27 Federal Budget announced two measures targeting investment property:

Federal Treasurer Jim Chalmers cited a greater than 400% rise in house prices since the 50% CGT discount replaced inflation-adjusted indexation in 1999.

The 2026-27 Federal Budget negative gearing and CGT reforms set out a phased reduction in the ability to offset investment property losses against other income, alongside a narrowing of the capital gains tax discount that has applied to investment properties since 1999, with the government citing housing affordability pressures as the primary policy rationale.

For CBA, these changes strike at the bank’s single most important growth engine. The bank holds approximately 30%+ market share in Australian home loans, making it the most exposed Big Four lender to any structural decline in investor lending demand.

Jarden analyst Matthew Wilson projected the changes could reduce housing credit growth by approximately 25%. Broader analyst estimates suggested a 5-10% reduction in investor lending demand. Jarden’s 12-month price target of $90 implies approximately 42% downside from the pre-crash price.

“Australia shares fall as CBA plunges 10% on earnings miss, housing tax changes.”

Reuters headline, 13 May 2026

The market read both drivers as reinforcing. A modestly disappointing quarter met a policy shift that could compress mortgage volumes for years.

No major broker upgraded its stance following the Q3 result. The numbers reinforced existing bearishness rather than prompting reassessment.

Big Four sell ratings were already a defining feature of the sector entering May 2026, with CBA carrying the most extreme consensus of any major Australian bank and ANZ the only exception, a divergence that reflects meaningfully different earnings growth expectations, capital positions, and valuation starting points across the group.

| Broker | Rating | 12-Month Price Target |

|---|---|---|

| Morgan Stanley | Underweight | $130 |

| Morgans | Sell | $119.40 |

| Macquarie | Sell | $114 |

| UBS | Sell | $130 |

| Citi | Sell | $140 |

| Jefferies | Sell | $142.26 |

| Jarden | Sell | $90 |

| Consensus average | – | ~$127.29 |

The consensus average price target of approximately $127.29 (range: $90 minimum to $149.10 maximum, per TipRanks as of mid-May 2026) implies roughly 19% further downside from the 14 May recovery close of $156.42.

Structural concerns underpin the bearish consensus. Annualised home loan growth among major banks averaged 3.7% as of February 2026, and deposit growth has slowed to 3.3%, down from rates exceeding 8% in 2024-2025. Both figures point to normalising momentum in CBA’s core businesses at a time when policy headwinds are intensifying.

The bull case and the bear case both have evidence behind them, and neither has resolved.

Investors who see opportunity point to the franchise underneath the price. Business lending grew 12.5% at 1.2x system. Capital remains strong. The $200 million provision build, on this reading, reflects management prudence rather than evidence of imminent large-scale losses.

Investors who see further risk point to the numbers the bulls cannot explain away. The consensus average target of $127.29 sits approximately 19% below the post-crash recovery price of $156.42. Rising corporate non-performing exposures (0.94% of total committed exposure and trending higher), combined with the budget’s structural headwind to investor mortgage volumes, suggest earnings compression over the medium term.

The variables that will determine which side is right:

The 10.43% fall on 13 May 2026 was driven not by a catastrophic result but by the collision of a modestly disappointing quarter with a stock priced to deliver an exceptional one, compounded by a federal budget that targeted the bank’s core growth engine.

Three forces converged in a single session: an earnings miss of 1-2% below consensus, a $200 million provision build signalling management caution about the macro environment, and negative gearing and CGT changes that threaten investor mortgage volumes for years to come.

With broker consensus targets averaging approximately $127.29 and no major broker upgrading after the result, the institutional view is that the repricing is real and may not be complete. CBA shareholders now face a decision about whether the franchise quality justifies holding above that consensus valuation, or whether the arithmetic of a normalising growth environment has further to run.

For investors who want to build their own view on where CBA trades from here, our dedicated guide to macro assumptions in bank valuations uses NAB as a live case study to show how different growth rate and discount rate inputs can produce a valuation range of $19 to $85.50 on a single stock, demonstrating why the gap between the $90 Jarden target and the $156 recovery price is not simply a matter of analytical disagreement.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

CBA fell 10.43% on 13 May 2026 because three negative forces hit simultaneously: a Q3 FY26 earnings miss of roughly 1-2% below consensus, a $200 million collective provision build signalling management caution about the economy, and a federal budget announcement phasing down negative gearing and reducing the CGT discount for investment properties, threatening CBA's core mortgage growth engine.

A collective provision top-up is a deliberate increase in funds set aside for potential future loan losses, even before specific loans turn bad. CBA's $200 million build alarmed investors because management explicitly increased the weighting of its downside economic scenario, signalling that leadership sees real and rising credit risk in the economy rather than just applying routine accounting caution.

Following the Q3 result, major brokers maintained sell ratings with price targets ranging from $90 (Jarden) to $142.26 (Jefferies), with a consensus average of approximately $127.29, implying roughly 19% further downside from the 14 May 2026 recovery close of $156.42.

The budget's phased reduction in negative gearing concessions and narrowing of the CGT discount for investment properties directly threatens investor mortgage demand, which is significant for CBA because the bank holds approximately 30% or more of the Australian home loan market, making it the most exposed Big Four lender to any structural decline in investor lending activity.

Before the crash, CBA held the position of the ASX's most valuable listed company, but the loss of approximately $29.93 billion in market cap in a single session pushed its post-crash market cap to roughly $257.16 billion, ceding the top position to BHP for the first time in years.