Even after shedding more than $17 per share in a single session, Commonwealth Bank of Australia still trades above every broker price target on the market. The most bearish analyst on the panel places fair value at $90, implying the stock would need to fall a further 42% from its current level to reach that estimate. CBA shares collapsed 10.4% on 13 May 2026, the steepest single-day decline since the bank’s 1991 listing, yet the sell-off has not resolved the valuation question that preceded it. The Federal Budget’s proposed overhaul of negative gearing and the capital gains tax (CGT) discount has added a structural headwind that most brokers believe the share price has not yet absorbed. One event exposed how much premium CBA was carrying; the other threatens the lending segment that has long been used to justify it. What follows is an examination of why the broker consensus remains overwhelmingly bearish despite the correction, what the property tax reforms mean mechanically for CBA’s mortgage book, and what retail investors reassessing their exposure should weigh before concluding the dip represents a buying opportunity.

What the 3Q FY26 update actually revealed about CBA’s earnings quality

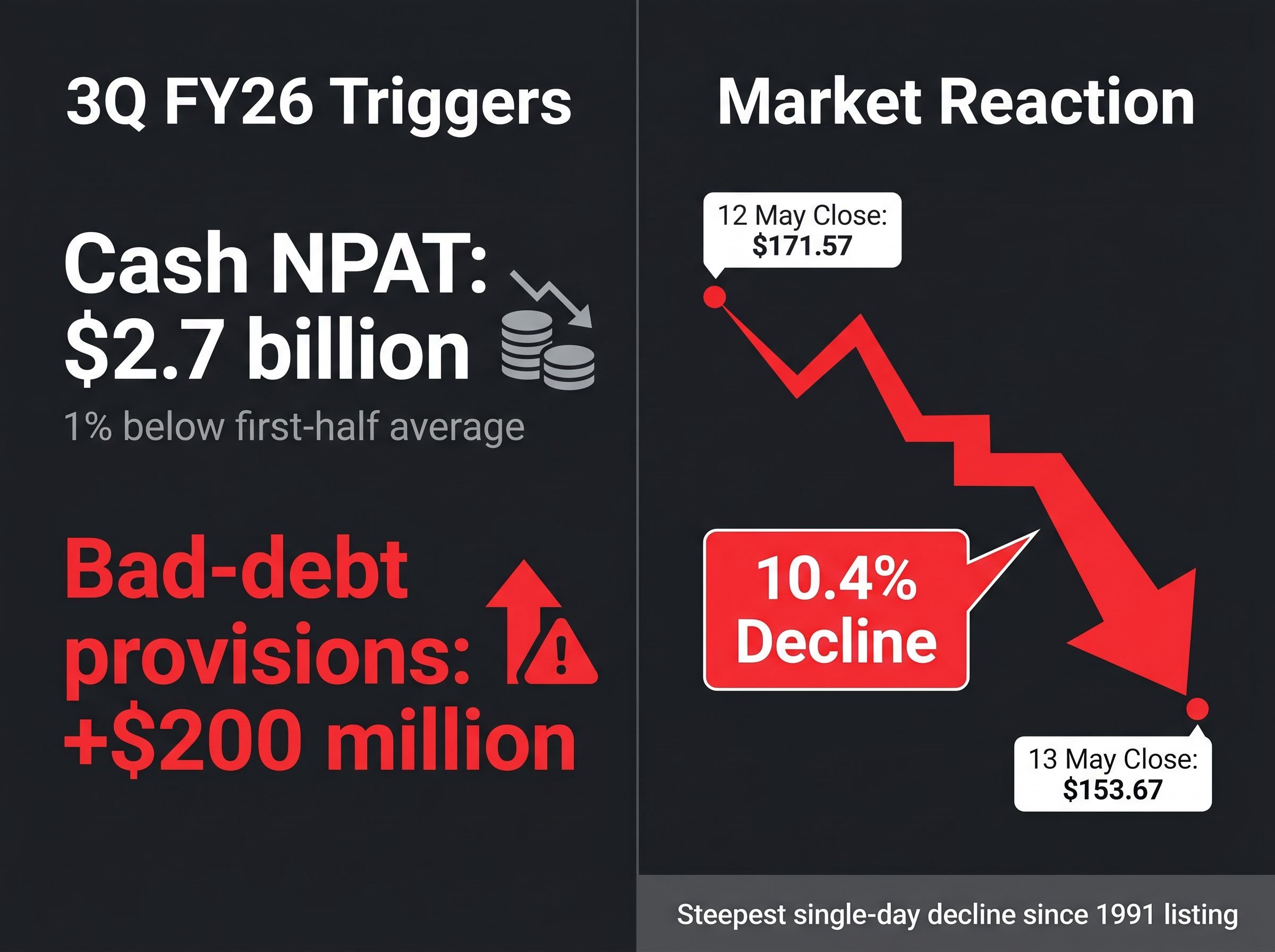

On the surface, CBA’s third-quarter result was a modest miss. Unaudited cash net profit after tax (NPAT) of $2.7 billion came in roughly 1% below the first-half quarterly average. For most banks, that would barely register. For a stock priced at the level CBA had reached, it was enough to trigger a reckoning.

The more telling detail sat further down the update: a $200 million increase in bad-debt provisions. This was not a backward-looking write-off on a soured loan book. It reflected management’s forward-looking caution, with CEO Matt Comyn citing geopolitical tensions and supply chain disruptions without offering specific guidance on the loan-loss trajectory. That combination, a provision build paired with vague macro commentary, signalled that CBA’s own leadership sees earnings risk ahead.

- Cash NPAT: $2.7 billion for 3Q FY26 (approximately 1% below first-half average)

- Bad-debt provisions: Increased by $200 million

- Management commentary themes: Geopolitical risk, supply chain disruption, no specific loan-loss guidance

The price reaction told its own story.

Two-session price movement: CBA closed at $171.57 on 12 May, opened at $163.00 on 13 May, hit an intraday low of $152.71, and closed at $153.67, a 10.4% single-day decline. The following session saw a partial recovery to $156.42.

A 10.4% sell-off on a 1% earnings miss suggests the market was already uncomfortable with what it was being asked to pay for CBA’s earnings stream. The provision increase is the forward signal that matters most.

The ASX bank sector dynamics that carried CBA to its pre-sell-off highs reflected a broader Big Four rally that analysts had flagged as momentum-driven rather than earnings-driven, with the ASX 200 Financials sector gaining nearly 9% year to date through late April 2026 even as sell ratings across all four banks remained unanimous.

When big ASX news breaks, our subscribers know first

How negative gearing and the CGT discount actually work, and what changes from July 2027

To understand what the Budget reforms mean for CBA, it helps to understand the mechanics they are dismantling.

Under existing rules, an investor who borrows to purchase a rental property can offset the annual loss (where interest and expenses exceed rental income) against their wage and salary income. A surgeon earning $400,000 who runs a $30,000 annual loss on an investment property reduces their taxable income to $370,000, effectively subsidising the cost of holding leveraged property through a lower personal tax bill. This is negative gearing.

The 50% CGT discount, introduced in 1999, turbocharges the exit. An investor who holds a property for more than 12 months pays capital gains tax on only half the gain. Treasurer Jim Chalmers has linked this concession to a greater than 400% rise in Australian house prices since its introduction. Australia’s residential property market is now ranked second most expensive globally, behind only Hong Kong.

The Grattan Institute housing affordability research has long documented the role of tax concessions in amplifying investor demand for established dwellings, providing the academic foundation for the argument that removing negative gearing and reducing the CGT discount would materially alter the after-tax return profile that has historically driven leveraged property investment.

The proposed reforms alter both mechanisms from 1 July 2027:

| Feature | Current treatment | Post-reform treatment (from 1 July 2027) |

|---|---|---|

| Negative gearing | Losses on all investment properties deductible against wage/salary income | Restricted to newly built dwellings only; losses on other investment properties quarantined to investment income |

| CGT discount | 50% discount on capital gains for assets held longer than 12 months | Substantially reduced or scrapped for residential investment properties |

| Grandfathering | N/A | Properties acquired before the cut-off date retain current treatment |

The combined effect is straightforward: the after-tax return on leveraged property investment falls materially for new purchases of established housing. Investors who previously relied on the tax system to subsidise negative cash flows while waiting for capital appreciation will face a fundamentally different equation. That change in investor economics feeds directly into the demand for the type of lending CBA provides.

Why a 25% credit growth slowdown is the number CBA investors need to understand

The transmission mechanism from tax reform to bank earnings runs through credit demand, and one broker has put a number on it.

Matthew Wilson at Jarden forecasts an approximately 25% reduction in housing credit growth as a direct result of the Budget reforms. The logic builds in stages:

- Weaker after-tax returns on leveraged property reduce the economics of high loan-to-value ratio (LVR) interest-only investor loans

- Reduced incentive to hold negatively geared properties pulls demand out of the investor lending category

- Lower investor credit demand compresses both volume and margins for lenders with heavy exposure to this segment

- CBA, which holds the largest investor home loan book among the major Australian banks, absorbs a disproportionate share of the slowdown

Interest-only investor loans have historically delivered wider margins and stronger asset quality for banks. Losing volume in this segment represents both a revenue headwind and a deterioration in the mix quality of the remaining book.

Jarden’s price target for CBA: $90, the most bearish on the broker panel, implying approximately 42% downside from the pre-sell-off price and with the current share price sitting roughly 74% above this target. This target reflects Wilson’s view that the market has not yet priced in the structural credit growth headwind.

Context from Morgan Stanley adds further texture: annualised home loan growth among the major banks averaged 3.7% as of February 2026, while deposit growth had slowed to 3.3%, down from above 8% in 2024-2025. The lending environment was already decelerating before the Budget introduced a structural drag.

Australia’s broader credit environment was already deteriorating before the Budget introduced a structural drag on investor lending, with corporate insolvencies at their highest level since 1991, real wages declining, and the RBA cash rate sitting at 4.10% after consecutive hikes that had materially slowed loan demand across all segments.

The full broker panel: seven sell ratings and what each one is really saying

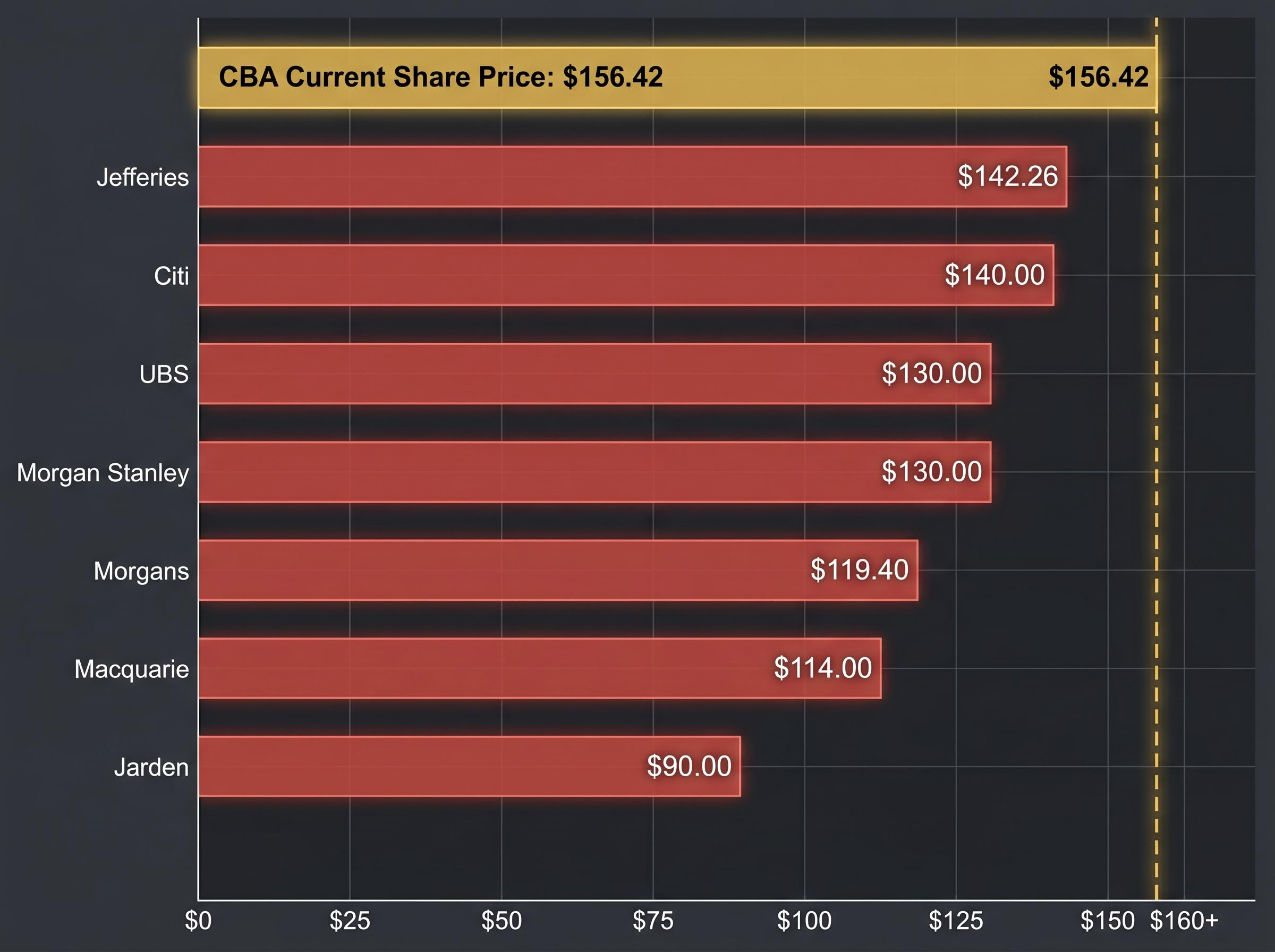

The broker panel tells a story not through any single target, but through the range. Seven analysts covering CBA hold bearish ratings. Not one has a buy or hold recommendation.

| Broker | Rating | Price target | Implied downside from $156.42 |

|---|---|---|---|

| Jarden | Underweight | $90.00 | ~42% |

| Macquarie | Underperform | $114.00 | ~27% |

| Morgans | Sell | $119.40 | ~24% |

| Morgan Stanley | Sell | $130.00 | ~17% |

| UBS | Sell | $130.00 | ~17% |

| Citi | Sell | $140.00 | ~10% |

| Jefferies | Underperform | $142.26 | ~9% |

The spread from $90 to $142.26 reflects differing assumptions about the severity of the credit slowdown, the trajectory of provisions, and the durability of CBA’s premium multiple. What unites them is the conclusion that the multiple is too high for the earnings outlook.

CBA’s price-to-book ratio sits at approximately 2.0-2.5x its major bank peers, a premium historically justified by superior returns on equity and the strength of its retail mortgage franchise. With earnings per share (EPS) growth expected in the low single digits and provisions rising, the case for paying that premium has weakened.

CBA’s premium multiple has persisted for years despite unanimous broker scepticism, sustained partly by mechanical buying from superannuation inflows and ASX 200 index replication that income-based valuation models are structurally unable to capture.

Even after the steepest single-day fall since CBA’s 1991 listing, the share price remains above every broker target. The most optimistic estimate, Jefferies at $142.26, still implies approximately 9% further downside from the 14 May close of $156.42.

What investors reassessing CBA exposure should actually weigh up now

Rather than anchoring to a single price target, investors reassessing CBA can monitor three variables that will determine whether the sell-off created genuine value or merely trimmed an extreme premium:

- Investor credit growth trajectory post-reform. Jarden’s 25% contraction forecast is the bear case. The actual outcome will depend on how property investors respond behaviourally to the changed tax treatment, and whether the 1 July 2027 effective date triggers a pre-deadline borrowing surge or an early pullback.

- Bad-debt provision trajectory over the next two quarters. The $200 million provision increase in 3Q FY26 may prove conservative or may be the beginning of a sustained build. Quarterly disclosures from CBA and RBA credit data will provide the clearest signal.

- Political durability of the property tax reforms. Any legislative weakening in the Senate before July 2027 would reduce the mortgage book headwind but would not resolve the underlying valuation concern.

One additional structural shift warrants attention. CBA’s post-sell-off market capitalisation of approximately $257.16 billion now sits well below BHP’s approximately $312.6 billion, removing the passive index-flow tailwind that came with being the ASX’s largest company by market value.

The political wildcard: what happens if reforms are wound back

The Opposition has framed the negative gearing and CGT changes as an attack on “mum-and-dad investors,” creating a credible path to partial legislative reversal in the Senate, particularly if rent increases materialise and are attributed to the policy in media coverage.

A partial backtrack would reduce the mortgage book headwind for CBA. It would not, however, resolve the valuation premium concern that predates the Budget. It would also confirm that Australia’s political system cannot sustain structural tax reform, an uncertainty that itself warrants a discount on any earnings forecast extending beyond a single electoral cycle.

CBA at $156 is still a valuation story, not a recovery story

The consensus bearish view is not primarily a reaction to the quarterly miss. It reflects a long-standing concern about CBA’s premium multiple in a low-growth environment, a concern that predates both the 13 May update and the Budget. Two compounding forces now work against the bull case: deteriorating lending fundamentals visible in the quarterly result, and a forward-looking credit growth headwind from the property tax reforms that will not materialise until July 2027 but is already reshaping broker models.

At $156.42, CBA trades above every sell-rated broker target, even after its worst day in 35 years. The target range of $90 to $142.26 suggests the burden of proof sits with the bull case, not the bear case.

The macro assumptions embedded in bank valuations explain why analysts covering the same stock can produce price targets ranging from $90 to $142, since small changes to the RBA rate path, employment trajectory, and property price outlook compound into vastly different fair value outputs without any of the modellers making an arithmetic error.

For a stock where seven brokers hold bearish ratings and the most optimistic still implies further downside, concluding that the dip represents value requires a specific thesis about what the market is getting wrong. Without one, the price has moved; the investment case has not.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.