EOS Shares Jump 4% as MARSS Wins €102M Counter-Drone Deal

2 hrs ago

Commonwealth Bank shed more than 10% of its market value in a single session on 13 May 2026, one of the steepest single-day falls in the bank’s history, even as headline cash profit ticked upward. The March quarter trading update gave investors a broadly stable income picture, but the fine print told a different story: A$316 million in loan impairments, a deliberate A$200 million lift in collective provisions, and cautious forward language that suggested management saw darker conditions ahead. Released against the backdrop of a Federal Budget that axed negative gearing, the update landed at the worst possible moment for a stock already carrying a price-to-earnings multiple of nearly 28 times earnings. What follows decodes the specific signals inside the quarterly disclosure, explains what rising provisions actually mean for earnings trajectory, and gives retail investors a framework for evaluating whether the post-crash CBA share price reflects genuine value or a valuation correction that still has further to run.

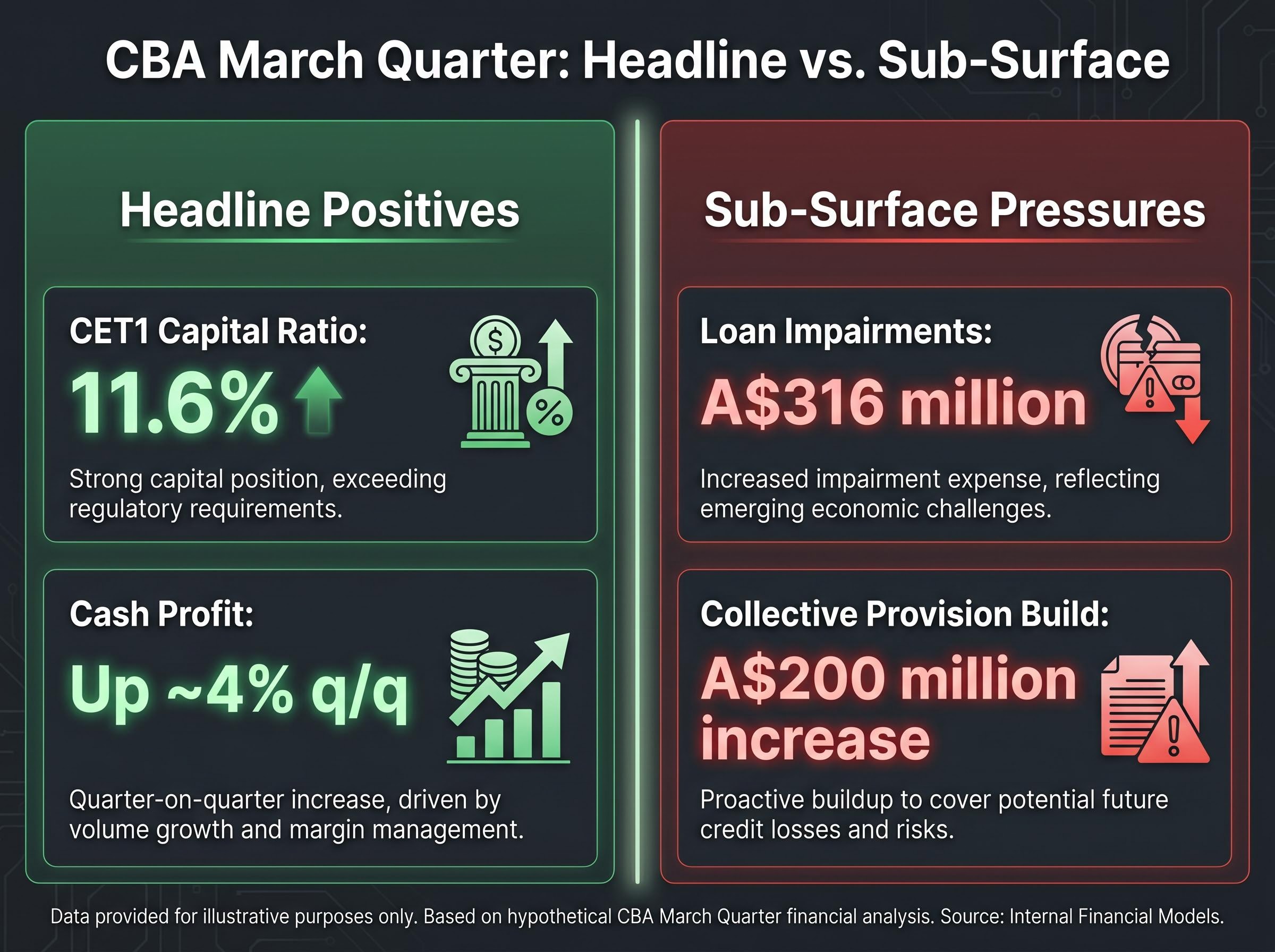

The headline figure from the March quarter looked fine. Cash profit rose approximately 4% quarter-on-quarter, and the Common Equity Tier 1 (CET1) capital ratio held at 11.6%. The market’s response was anything but fine.

CBA closed at A$153.67 on 13 May 2026, a fall of approximately 10.43% in a single session. By the close on 14 May, the stock had partially recovered to A$156.42, but the damage extended well beyond one day:

The narrative of a “12% decline over five trading sessions” circulating in some coverage is not well supported by available data. The evidence points to a concentrated single-day shock on 13 May, followed by tentative buying on 14 May.

Two catalysts compounded rather than operating independently. The Federal Budget, announced the week prior, removed negative gearing for property investors and tightened capital gains tax settings. That policy shift had already unsettled bank investors before CBA released its 3Q26 trading update and Basel III Pillar 3 disclosure via the ASX on the morning of 13 May. The quarterly numbers landed into a market already pricing structural risk to the mortgage book, and the provisioning data confirmed the anxiety rather than relieving it.

Start with what the market saw first. Operating income was stable. The CET1 ratio of 11.6% exceeded regulatory requirements comfortably. Cash profit rose approximately 4% quarter-on-quarter, according to reporting from Motley Fool Australia (the specific figure has not been confirmed from the primary ASX document).

On any other day, those figures would have prompted a flat open at worst.

Beneath the stable operating income headline, rising arrears across the loan book tell a more granular story: personal loan arrears spiked 30 basis points in a single quarter, and stress spread across every major consumer lending category, not just the mortgage segment most closely associated with the negative gearing debate.

The table below separates the headline positives from the sub-surface indicators that drove the selloff:

| Metric | Reported Figure | What It Signals |

|---|---|---|

| CET1 Capital Ratio | 11.6% | Balance sheet strength; regulatory buffer intact |

| Cash Profit (q/q) | Up ~4% | Earnings still growing, but rate of growth matters |

| Loan Impairments | A$316 million | Realised credit losses rising |

| Collective Provision Build | A$200 million increase | Management expects credit conditions to deteriorate further |

The A$200 million collective provision increase is a forward-looking management decision, not a backward-looking accounting entry. It carries more informational weight than the profit figure because it reflects where management believes credit conditions are heading, not where they have been.

That distinction is what the market priced on 13 May. A profit beat matters less when management is simultaneously building buffers against expected future losses.

Collective loan impairment provisions are money set aside today against loans that have not yet defaulted but where management sees elevated risk of future losses. They are not tied to a specific borrower who has missed payments. Instead, they represent a buffer across the broader loan book, built on probability-weighted estimates of deterioration ahead.

RBA analysis of collective provisioning explains that these buffers are held against unidentified losses and general loan book deterioration, and that how quickly a bank builds them is itself a countercyclical signal about where management believes the credit cycle is heading.

The logic works in three steps:

This is why CBA’s A$200 million collective provision build matters more than the 4% cash profit increase. The profit figure looks backward. The provision build looks forward.

CBA is not alone. Westpac increased its bad debt buffers in its April 2026 quarterly update. NAB is expected to carry collective provisions of approximately A$706 million for the half-year to March 2026, according to Morningstar and Dow Jones reporting.

The interpretive question for investors is straightforward: if peers are building at similar or higher rates, this is a sector-wide signal about the Australian credit environment. If CBA is building faster relative to its book, it may reflect CBA-specific concerns about its mortgage portfolio’s exposure to the policy changes ahead.

Sector-wide provisioning forecasts from Morgans project total Big Four provisions rising from approximately A$2.4 billion in FY25 to approximately A$5.5 billion by FY27, a trajectory that frames CBA’s single-quarter A$200 million build not as an isolated management decision but as part of a coordinated industry-wide reassessment of credit risk.

A 10% single-day fall sounds like it should create opportunity. The arithmetic says otherwise.

CBA’s trailing twelve-month P/E ratio, even after the crash, sits at approximately 25-28 times earnings depending on the data provider. NAB, by comparison, trades at approximately 19 times earnings.

Post-crash, CBA remains one of the most expensively priced major banks in the world. At roughly 25-28 times earnings, the stock still commands a significant premium over domestic peers and global banking benchmarks.

The sector-wide valuation disconnect had been building for months before the 13 May shock: all 14 analysts covering CBA held sell ratings as of late April 2026, with a consensus price target of around A$130, and yet the stock continued to trade well above that level, reflecting the momentum dynamic that made the eventual correction so severe.

That premium historically rested on three conditions:

The March quarter update places the third condition directly in question. When management is building provisions at this pace, earnings compounding is decelerating. The premium may have been justified when growth was steady. Whether it remains justified when growth is slowing and credit costs are rising is the question the market began repricing on 13 May.

Institutional research desks moved quickly. The Australian Financial Review reported on 14 May 2026 that multiple brokers slashed forecasts following the combined budget and quarterly update shock.

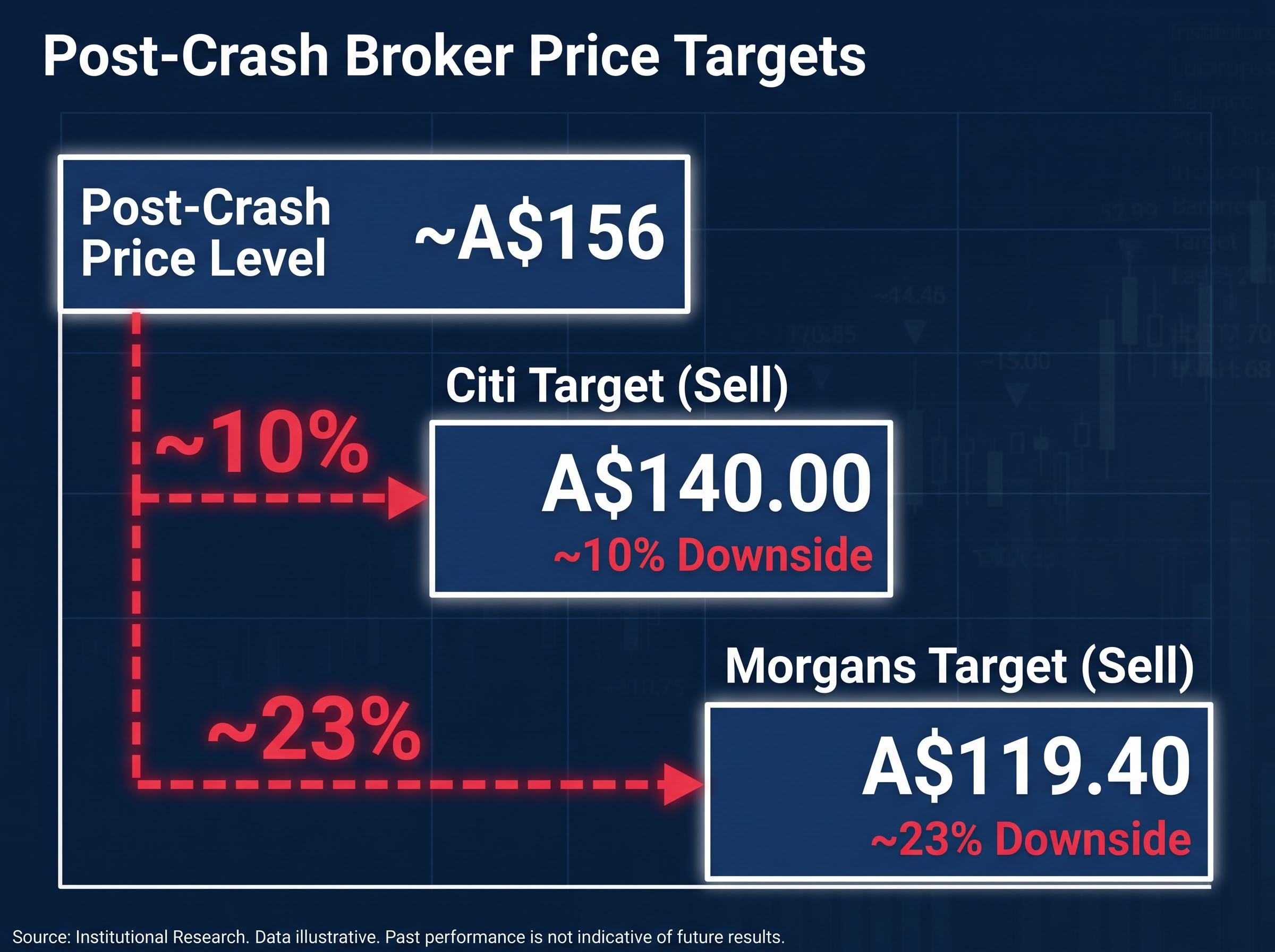

| Broker | Rating | Price Target (A$) | Implied Downside from ~A$156 |

|---|---|---|---|

| Morgans | Sell | $119.40 | ~23% |

| Citi | Sell | $140.00 | ~10% |

| JPMorgan | Not confirmed | Not confirmed | Earnings forecasts cut |

Morgans’ A$119.40 target implies approximately 23% further downside from the post-crash price level, a figure that suggests the selloff on 13 May may represent the beginning of a re-rating rather than its conclusion.

Citi maintained its Sell rating and A$140.00 target following the update. JPMorgan slashed earnings forecasts downward, though exact revised figures remain unconfirmed.

These are not fringe views. Multiple institutional desks independently see further downside of 10-23% even after the stock already lost more than a tenth of its value in a single session. For retail investors weighing a “buy the dip” decision, those targets offer a calibration point worth sitting with.

The quarterly numbers tell a one-quarter story. The Federal Budget’s removal of negative gearing tells a multi-year one.

The transmission mechanism runs through two stages:

The Federal Budget tax reform measures confirm that negative gearing will be limited to new builds from 1 July 2027 and that the 50% Capital Gains Tax discount will be replaced with inflation-based indexation, a structural shift that directly reduces the after-tax return on leveraged investment property and narrows the pool of future mortgage borrowers.

CBA’s own economics team quantified the potential impact. According to CommBank Newsroom’s May 2026 housing outlook update, the removal of negative gearing is expected to reduce established dwelling prices by approximately 25% over time. That estimate came from the bank’s own analysts, not from external critics.

Analysts have broadly described the near-term credit risk as manageable, but that assessment is contingent language. It depends on unemployment remaining stable and house prices avoiding a sharp correction. If either condition fails, manageable becomes something else.

CBA’s own A$200 million provision build suggests management is not fully persuaded conditions will remain stable. When a bank’s economics team publishes a 25% dwelling price impact estimate and its provisioning team simultaneously builds buffers, the two signals reinforce each other.

Mortgage lending is CBA’s dominant revenue source. Any structural shift in investor property demand is not a peripheral concern but a direct challenge to the earnings base that underwrites the current valuation.

The tension from 13 May has not resolved. Cash profit rose, and the stock fell, because the market looked past the backward-facing number and focused on three forward-facing pressures: a provisioning signal that management expects credit deterioration, a valuation premium that remains stretched even after a 10% correction, and a housing policy change that threatens the bank’s single largest revenue line.

The bull case is not baseless. A CET1 ratio of 11.6% is genuinely strong, and if economic conditions stabilise, some portion of the provision build could reverse in future periods. CBA retains the largest retail banking franchise in Australia, and market share does not evaporate overnight.

The question is whether those strengths justify paying 25-28 times earnings when Morgans sees fair value at A$119.40 and Citi at A$140.00.

Three forward indicators will determine who is right:

The next information triggers are the remaining peer bank results and CBA’s full-year results cycle. Until then, the data available supports caution more than conviction.

For investors wanting to build their own fair value estimate rather than relying solely on broker targets, our comprehensive walkthrough of ASX bank valuation methods covers net interest margin analysis, return on equity frameworks, CET1-adjusted dividend discount modelling, and a worked example using Westpac’s verified H1 2026 figures that shows how the same inputs produce fair value estimates ranging from A$34 to A$49 depending on assumptions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Two catalysts hit simultaneously: the Federal Budget announced the removal of negative gearing for property investors, and CBA's March quarter trading update revealed A$316 million in loan impairments and a A$200 million increase in collective provisions, signalling management expects credit conditions to deteriorate further.

A collective loan impairment provision is money a bank sets aside today against loans that have not yet defaulted but where management sees elevated risk of future losses; when a bank increases this buffer, it reduces current reported profit and signals that management expects credit conditions to worsen, making it a forward-looking indicator more meaningful than the headline profit figure.

Following the 13 May 2026 crash, Morgans set a Sell rating with a price target of A$119.40 (implying approximately 23% further downside from the post-crash price near A$156), while Citi maintained a Sell rating with a A$140.00 target, and JPMorgan cut earnings forecasts without confirming a revised target.

Removing negative gearing reduces the after-tax return on leveraged investment property, which lowers investor demand for property, slows new mortgage origination volumes, and risks eroding the collateral quality of existing loans if dwelling prices fall; CBA's own economics team estimated the policy could reduce established dwelling prices by approximately 25% over time.

Yes; even after the 13 May 2026 selloff, CBA's trailing price-to-earnings ratio remained at approximately 25-28 times earnings, compared to NAB at approximately 19 times, making it one of the most expensively priced major banks in the world and leaving a significant valuation gap relative to institutional broker price targets.