WTI Jumps 1.6% as Iran Strikes Shatter Hormuz Deal Hopes

1 hr ago

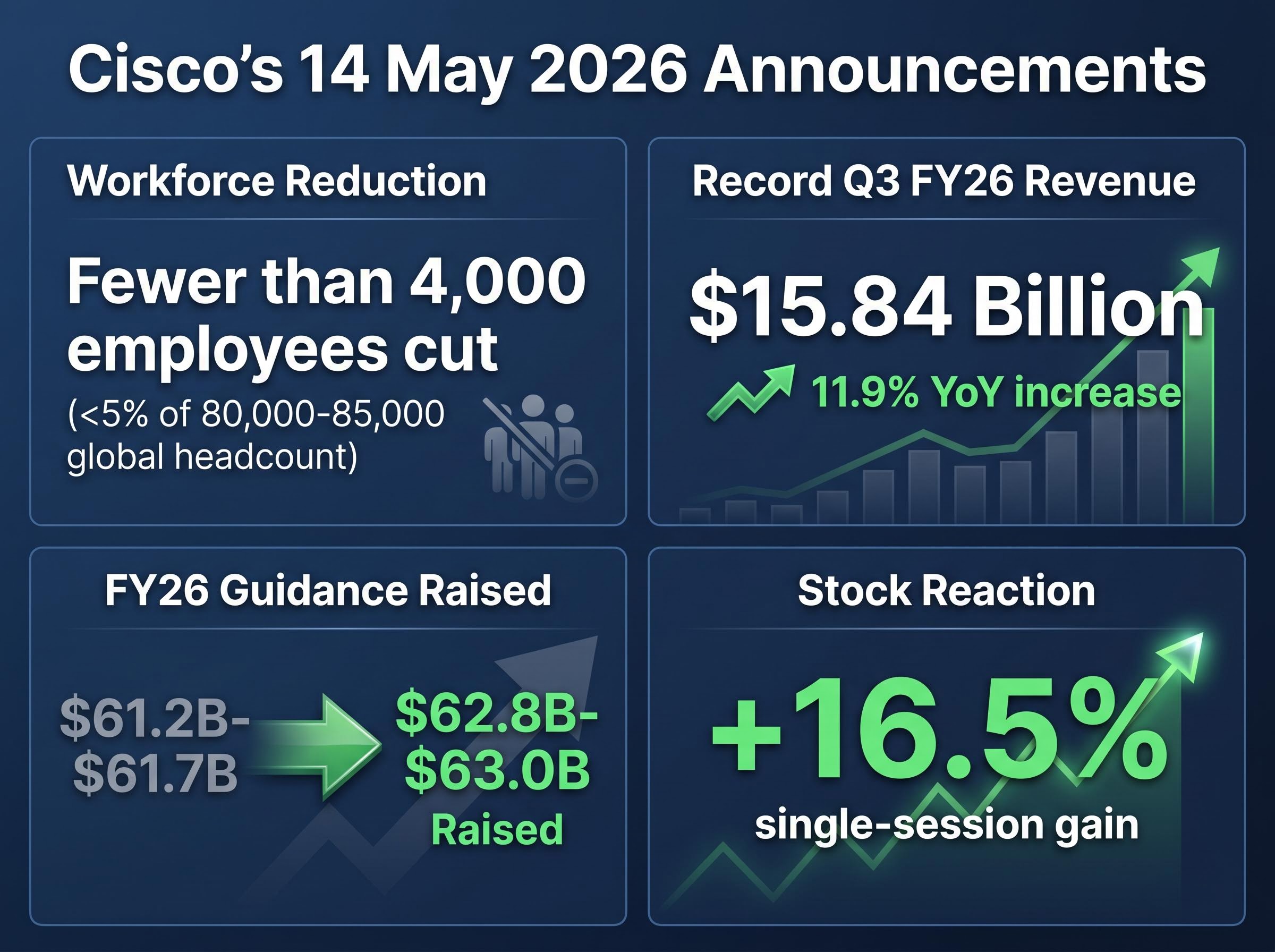

Cisco cut fewer than 4,000 jobs on 14 May 2026, the same day it posted record quarterly revenue of $15.84 billion and raised its full-year forecast by more than $1.5 billion. The stock responded with a 16.5% single-session surge, its largest in years, reaching record highs in after-hours trading. The juxtaposition is not a contradiction. It is the clearest example yet of how markets price corporate restructuring when it is paired with an AI-driven growth thesis and a guidance beat that lands well above Wall Street consensus. What follows is an explanation of the financial results behind the move, the mechanics connecting the layoffs to the raised outlook, and why the pattern now extends well beyond a single company.

Three announcements hit the wire simultaneously during Cisco’s Q3 FY26 earnings call:

Cisco ranked among the top percentage gainers in U.S. markets on the day. The reaction was not a response to the layoffs in isolation, nor to the guidance raise in isolation. It was a response to the combination, which the market read as a signal of strategic confidence rather than distress.

CEO Chuck Robbins stated: “To ensure we are capturing the significant opportunities in silicon, optics, security, and AI, we announced a restructuring plan today to reallocate resources and allow us to invest in these key growth areas.”

The distinction between a restructuring that signals weakness and one that signals reallocation is the interpretive question that shaped the entire session.

Cisco’s Q3 FY26 revenue of $15.84 billion represented an 11.9% year-over-year increase, a company record. The composition of that growth, however, tells a more specific story than the headline figure.

Product revenue reached $12.12 billion, driven by AI infrastructure and optics orders from hyperscale data centre customers. Services revenue came in at $3.74 billion, a slight decline. The divergence is a leading indicator: the growth engine sits in hardware and silicon tied to AI buildouts, not in traditional services contracts.

The semiconductor supercycle underpinning these orders has been years in the making, with hyperscaler physical hardware and data centre construction absorbing an estimated $450 billion of the roughly $700 billion in AI infrastructure capital projected for 2026, a concentration that makes networking and optics components among the most directly exposed categories in the supply chain.

Robbins expressed confidence in the forward pipeline. “Cisco will be one of those winners,” he said, referencing the company’s positioning within the AI infrastructure spending cycle.

The raised FY26 guidance landed materially above both prior company guidance and Wall Street consensus.

| Metric | New FY26 Guidance | Prior FY26 Guidance |

|---|---|---|

| Full-year revenue range | $62.8B-$63.0B | $61.2B-$61.7B |

| Change versus prior guidance | +2.5-2.9% | |

| Change versus Wall Street consensus (~$61.6B) | +2.0-2.3% | |

A 2.0-2.3% beat above consensus is a material positive surprise for a company of Cisco’s scale. The revised midpoint of approximately $62.9 billion sits roughly $1.3 billion above where the Street had modelled.

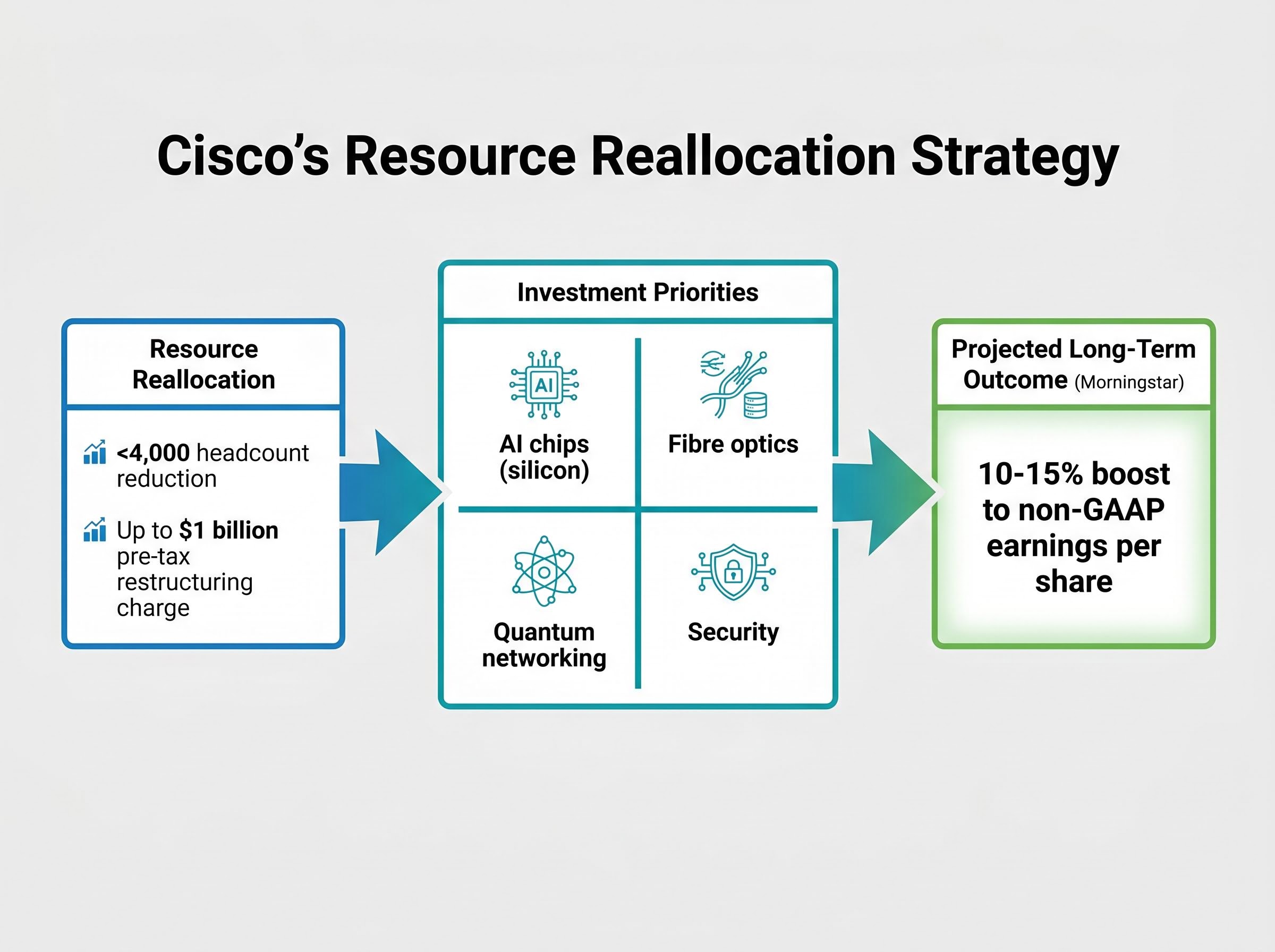

The term “restructuring” carries an immediate association with corporate distress. In Cisco’s case, the internal logic runs differently: headcount reductions in lower-growth functions fund accelerated investment in higher-margin areas where AI demand is pulling revenue forward.

Robbins’ internal memo identified four specific investment priorities:

Selective hiring in these areas is continuing alongside the cuts. Cisco also offered internal placement support to affected employees, citing a 75% historical success rate for finding new roles within the organisation. That context reframes the announcement from a pure headcount reduction to a resource reallocation with a measurable internal absorption mechanism.

The financial cost is not trivial. Cisco expects pre-tax restructuring charges of up to $1 billion, with $450 million recognised in Q4 FY26 and the remainder flowing through FY27.

Morningstar projected that AI-driven restructurings of this type could boost non-GAAP earnings per share by 10-15% over the long term, as capital shifts from lower-margin legacy operations to higher-margin AI infrastructure.

Quantum networking, in particular, differentiates Cisco’s forward investment thesis from pure-play AI infrastructure peers. It signals a bet on a technology layer that most competitors have not yet prioritised at this scale.

Cisco’s announcement is the latest entry in a pattern that has repeated across enterprise technology since late 2025. The structure is consistent: pair a workforce reduction in non-AI functions with an AI investment pivot and, where results support it, a guidance raise.

| Company | Restructuring Scale | AI Investment Focus | Stock Reaction |

|---|---|---|---|

| IBM | ~3,800 jobs, Q4 2025 | $500M+ Watsonx AI; raised FY26 revenue guide ~4% | +12% |

| HPE | ~2,500 jobs, Feb 2026 | AI servers (GreenLake); $800M charge; FY26 revenue +7% | +9% |

| Dell | ~5,000 jobs, Mar 2026 | $1.2B savings; AI revenue outlook raised 50% YoY | +10-20% |

| Cisco | ~4,000 jobs, May 2026 | Silicon, optics, quantum networking, security | +16.5% |

The stock reactions cluster in a 10-20% range. The 2025-2026 cycle has seen more than 100,000 tech layoffs industry-wide, yet AI revenue for infrastructure players has surged 30-50% year-over-year. Q1 2026 enterprise tech revenue averaged approximately +15% year-over-year across the sector.

What separates Cisco from this peer group is its quantum networking investment and its valuation. At approximately 15x forward price-to-earnings, Cisco trades at a discount to most pure-play AI infrastructure names, which may partly explain the outsized single-session move.

Infrastructure-level AI adoption, where companies embed AI at the hardware and networking layer rather than running surface-level pilots, is projected to generate 3x the ROI of shallow deployments by 2027, a gap that partly explains why markets reward companies like Cisco, IBM, and HPE for committing capital to specific hardware categories rather than announcing generic AI strategies.

The pattern across Cisco, IBM, HPE, and Dell suggests three indicators that separate strategic reallocation from distress-driven cost-cutting:

Hyperscaler AI capital expenditure, estimated at more than $200 billion annually, remains the primary demand driver underpinning these announcements. Cisco’s AI order backlog is the specific forward indicator analysts are now monitoring most closely.

Hyperscaler capital expenditure for 2026 is now tracking toward $725 billion across Amazon, Microsoft, Alphabet, and Meta, with Q1 2026 alone absorbing $130 billion, figures that translate directly into forward order demand for the networking, optics, and silicon categories where Cisco has concentrated its restructuring investment.

The $1 billion in restructuring charges will weigh on GAAP earnings through FY27, even as non-GAAP results remain strong. For investors focused on reported earnings rather than adjusted figures, the near-term picture is less clean than the stock reaction suggests.

Economists have also identified “deflationary AI pressure” on enterprise headcount as a secular trend, not a company-specific event. The efficiency gains that justify these restructurings may create a structural reduction in technology sector employment that extends beyond any individual announcement cycle. The 10-year Treasury yield stood at 4.455% on 14 May, providing a valuation comparison backdrop that makes Cisco’s 15x forward P/E appear relatively favourable, though rising yields could pressure growth stock multiples more broadly.

Analyst commentary on AI job cuts and higher returns has grown more cautious, with some researchers questioning whether workforce reductions tied to AI pivots reliably translate into the margin expansion and earnings growth that initial market reactions tend to price in.

Cisco’s 14 May announcement landed in a market already at record levels, with the S&P 500 at 7,444.25 and the Nasdaq Composite at 26,402.34. The 16.5% single-session response is now a data point about how investors price AI-driven restructuring in a risk-on environment, not merely a Cisco-specific reaction.

The raised guidance, combined with hyperscaler AI capital expenditure momentum, positions the stock within a framework that the market has now validated four times across four large-cap enterprise technology names in six months. The next time a peer announces layoffs paired with an AI pivot and a guidance upgrade, the market’s likely playbook is documented.

The forward question is which enterprise technology company runs this playbook next, and whether the market’s willingness to reward the combination holds as restructuring charges accumulate across the sector.

For investors wanting to understand how the 14 May session played out across the broader hardware stack, our full explainer on AI infrastructure stocks covers the simultaneous Nvidia catalyst, the sympathy gains in Arista, Super Micro, Marvell, and Broadcom, and the regulatory risk from Congressional opposition to the H200 China clearance that could shape the next leg of the trade.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Cisco's corporate restructuring refers to the reduction of fewer than 4,000 jobs announced on 14 May 2026, designed not to cut costs but to reallocate resources toward high-growth areas including AI silicon, fibre optics, quantum networking, and security.

The market interpreted the combination of a record quarterly revenue of $15.84 billion, a raised full-year guidance range of $62.8 billion to $63.0 billion, and a targeted AI restructuring plan as a signal of strategic confidence rather than corporate distress.

Cisco's revised full-year revenue guidance of $62.8 billion to $63.0 billion beat Wall Street consensus of approximately $61.6 billion by roughly 2.0-2.3%, placing the midpoint about $1.3 billion above where analysts had modelled.

Investors should monitor three indicators: whether the restructuring is paired with a raised guidance outlook, whether the company names specific AI technology priorities rather than using generic language, and whether the restructuring charge-to-savings ratio suggests growth funding rather than margin protection.

All four companies followed a similar playbook of pairing workforce reductions in non-AI functions with targeted AI investment pivots, with stock reactions clustering in a 10-20% range; Cisco's 16.5% single-session gain was the largest of the group.