WTI Jumps 1.6% as Iran Strikes Shatter Hormuz Deal Hopes

26 mins ago

Nvidia crossed approximately $5.53 trillion in market capitalisation on 14 May 2026 after U.S. authorities quietly handed roughly ten Chinese technology firms permission to purchase the H200, an AI chip that had been locked out of China for months. The approvals arrived on the opening day of the Xi-Trump summit in Beijing, framing the move as both a commercial milestone and a diplomatic signal. For investors who have watched Nvidia navigate a maze of export restrictions since early 2025, the licenses represent a measurable shift in the geopolitical calculus around AI hardware.

What follows breaks down exactly which companies were approved, what the licenses are worth in revenue terms, what Wall Street’s named analysts are saying today, and what the continuing restrictions on next-generation chips mean for how long this tailwind lasts.

The U.S. Department of Commerce has authorised the following ten firms to purchase Nvidia’s H200 AI chips under the case-by-case licensing regime, with initial orders capped at 50,000 H200 units per company for Q2-Q3 2026:

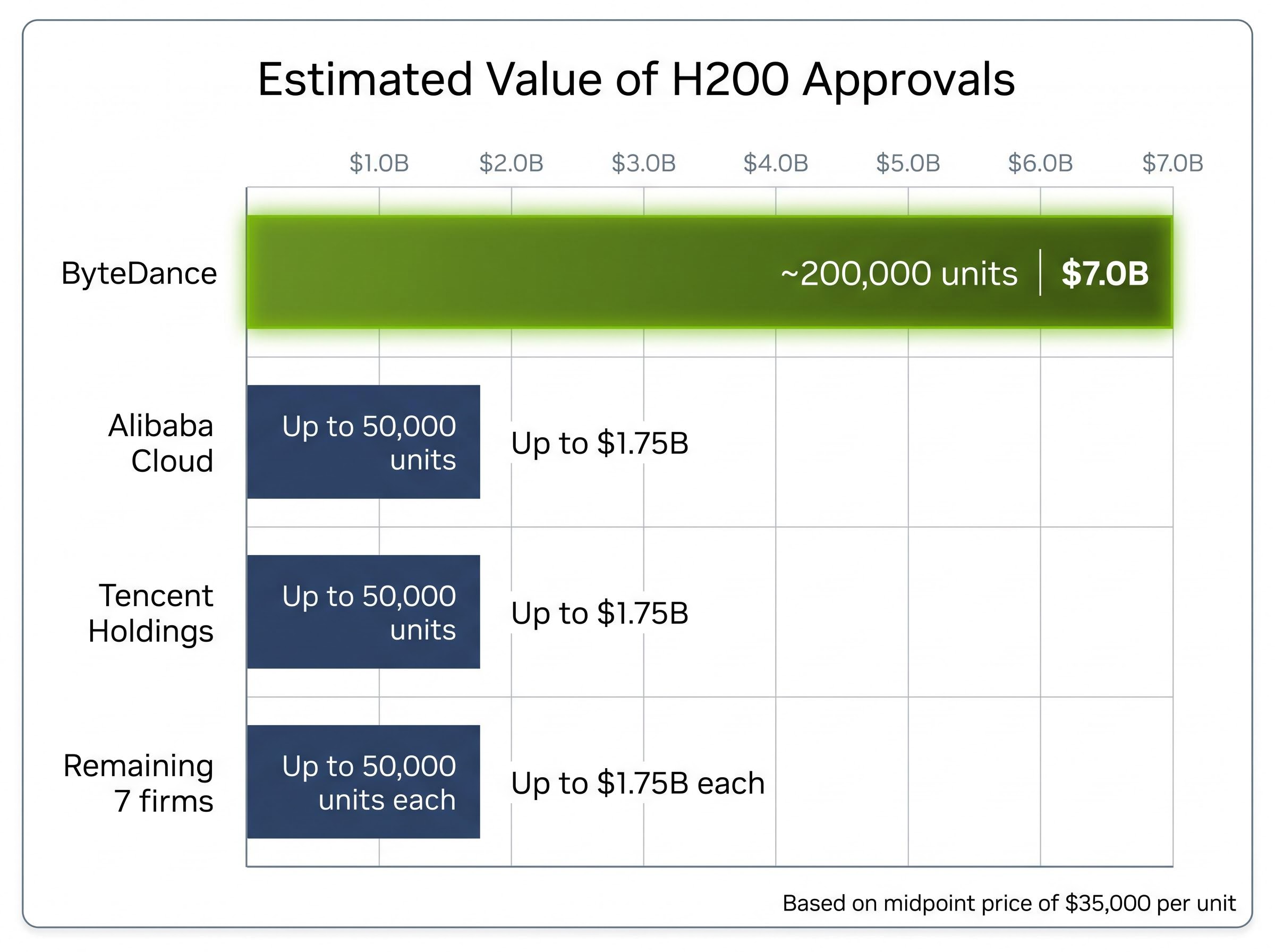

ByteDance reportedly requested approximately 450,000 units, with roughly 200,000 approved in the initial tranche.

Disputed: Pending official clarification. The scope of Huawei’s approval remains contested. Some reports indicate the licence is limited to the HiSilicon semiconductor design unit only, not the broader Huawei corporate entity. The precise terms have not been officially resolved.

At a midpoint price of $35,000 per unit, the estimated hardware value for known approved volumes is as follows:

| Company | Business Type | Approx. Units Approved | Est. Value ($35K/unit) |

|---|---|---|---|

| ByteDance | AI platform / social media | ~200,000 | $7.0B |

| Alibaba Cloud | Cloud computing | Up to 50,000 | Up to $1.75B |

| Tencent Holdings | Cloud / gaming / AI | Up to 50,000 | Up to $1.75B |

| Remaining 7 firms | Various AI / chip design | Up to 50,000 each | Up to $1.75B each |

Alibaba (BABA) gained 8.18% on 14 May, reflecting the market’s reading of which Chinese equities benefit most from restored chip access.

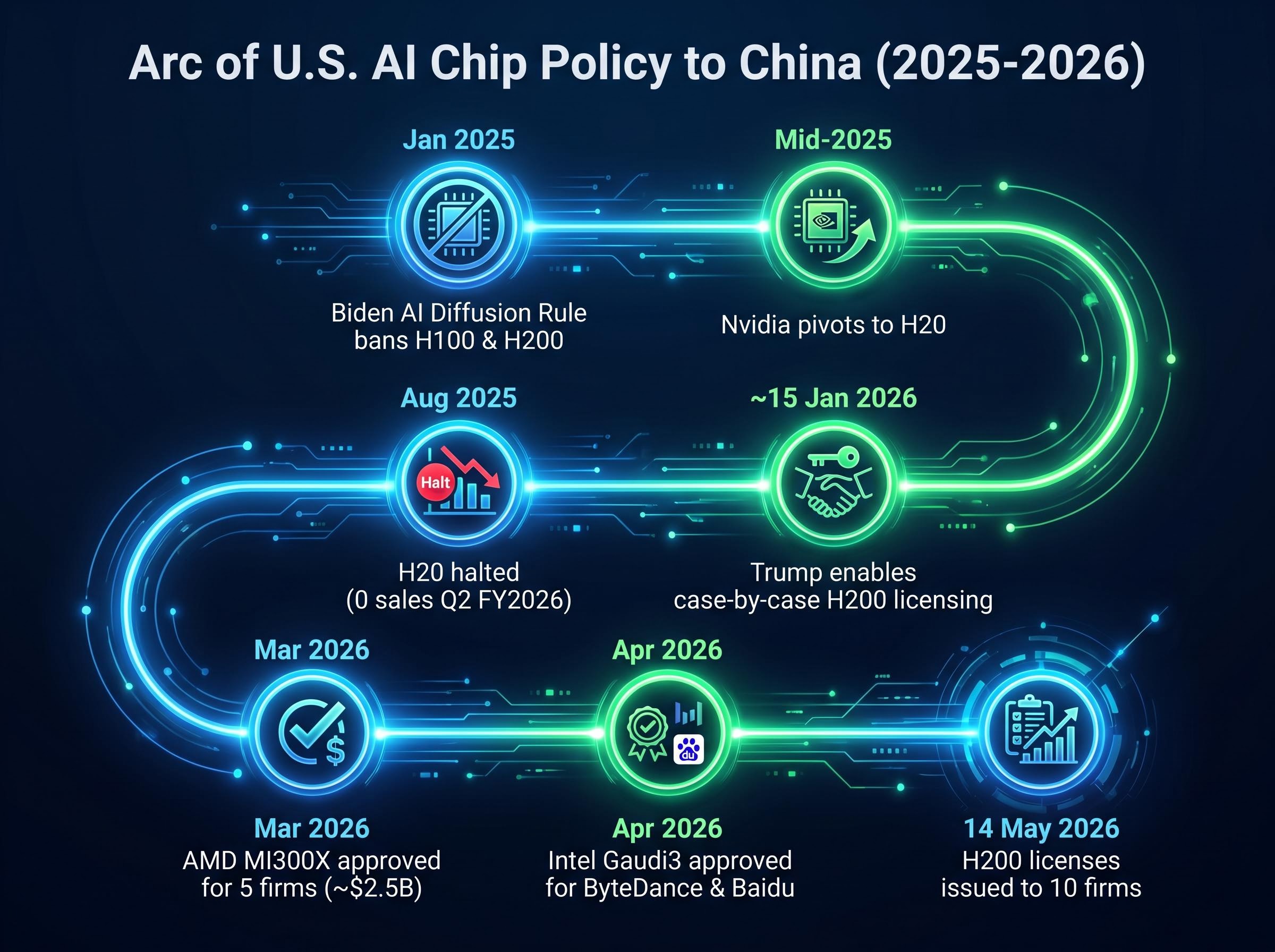

Today’s approvals are the product of a specific chain of policy reversals, not a sudden shift. The arc from outright ban to licensed access unfolded in six stages:

The asymmetric risk profile facing semiconductor stocks at the summit was quantified before the session opened: Bloomberg Intelligence placed a 70% probability on partial de-escalation while projecting only 8-12% upside for that scenario, against a 25% probability hardening case carrying 10-20% downside for the SOXX and SMH.

The BIS revised licensing policy for semiconductor exports to China, published on 13 January 2026, established the case-by-case review framework under which today’s H200 approvals were processed, including the performance caps, domestic supply priority requirements, and end-use compliance conditions that define each licence’s scope.

The B200/Blackwell architecture remains fully banned for export to China as of May 2026. The H200 sits approximately two generations behind Nvidia’s current leading-edge product. That context matters: the commercial upside from these approvals is real, but it is bounded. Washington is calibrating access, not abandoning controls, and that distinction sets a ceiling on how much China revenue Nvidia can recover through this licensing regime.

The H200 is Nvidia’s second-most capable AI processor available for commercial sale, positioned between the older H100 and the banned Blackwell B200 in performance terms. Priced at $30,000-$40,000 per unit, it is designed for large-scale model training and inference at data centre scale.

The demand from ByteDance, Alibaba, Baidu, and Tencent is business-driven. Each firm is competing in a domestic large language model (LLM) and generative AI market that is expanding rapidly, and each needs GPU-class hardware to train and deploy models at competitive scale. A large language model is an AI system trained on vast amounts of text data to generate and understand language. Without access to chips at the H200’s performance tier, these companies face a hardware bottleneck that slows development timelines.

The approved performance caps constrain what buyers actually receive:

Chinese buyers receive a deliberately constrained version of the chip’s full capability, making the demand structural (driven by competitive necessity) rather than opportunistic.

The analyst consensus is genuinely bullish. Three named strategists raised price targets within hours of the approval news.

| Analyst / Firm | Previous Target | New Target | Rating |

|---|---|---|---|

| Joseph Moore, Morgan Stanley | $245 | $260 | Buy |

| Harlan Sur, JPMorgan | N/A | $275 | Overweight |

| Vivek Arya, Bank of America | N/A | $265 | Buy |

Moore cited the H200 clearance as adding meaningful FY2027 revenue runway. Sur forecast substantial China H200 revenue in H2 2026, with meaningful earnings-per-share uplift. Arya revised Nvidia’s FY2027 revenue estimate upward, with China contributing roughly 12% of the revenue mix.

Goldman Sachs characterised the approval as “risk-on for semis,” flagging Nvidia as leading a broader sector rotation.

Across approximately 28 tracked analysts, the average price target sits at roughly $258, with approximately 95% carrying Buy ratings. NVDA traded at $230.24 in premarket as of 7:59 a.m. EDT on 14 May.

The revenue arithmetic requires care. ByteDance’s 200,000 approved units at $30,000-$40,000 per unit represent $6 billion-$8 billion in hardware value for that single buyer. No confirmed consensus figure for all ten companies has been independently verified, and estimates range widely. The direction of the revenue uplift is clear; the magnitude is still being calculated.

Beijing’s import barrier adds a layer of uncertainty that the approved-unit figures alone do not capture: customs blocks have prevented any commercial H200 shipments from completing to date, meaning the gap between U.S. licensing approvals and actual revenue recognition may be wider than the hardware value estimates suggest.

The H200 approvals were not a standalone commercial event. They landed on the opening day of the Xi-Trump summit in Beijing (14-15 May 2026), a summit covering trade normalisation and broader strategic stability. The timing is widely interpreted as a diplomatic goodwill gesture accompanying the talks.

The backdrop adds urgency. U.S. strikes on Iran on 7 May 2026 and ongoing ceasefire negotiations in mid-May have elevated energy costs (WTI crude at $101.04 per barrel on 14 May) and increased Washington’s incentive to stabilise the China relationship. Trump is reported to be seeking Beijing’s involvement in ending the conflict.

The broader summit agenda risks extend well beyond chip licences: analysts at Fidelity International flagged that markets are simultaneously pricing optimism on trade purchase commitments, AI security talks, and Iran energy negotiations, each carrying materially different probability distributions that investors should disaggregate before taking positions.

Not everyone in Washington is on board. Three categories of risk to the licensing regime are already visible:

The Commerce Department confirmed all ten firms were vetted for non-military end-use with ongoing compliance monitoring. Investors who treat this purely as a commercial catalyst miss the political scaffolding holding it up.

Nvidia’s market capitalisation reached approximately $5.53 trillion in premarket on 14 May 2026, with shares up roughly 1.9% following a prior close of $225.83 on 13 May (up 2.29% that session). The move sits within a broader risk-on environment: the S&P 500 reached 7,444.25 (up approximately 0.58%) and the Nasdaq Composite hit 26,402.34 (up approximately 1.20%) on 14 May.

A genuine counterweight exists beneath the euphoria. The probability of a rate hike by year-end 2026 has risen above 28% on CME FedWatch, up from 20.7% one week earlier. The 10-year Treasury yield stood at 4.455% on 14 May. These conditions create headwinds for growth equity valuations that investors should factor into position sizing.

AI chip valuation comparisons across Nvidia and Broadcom reveal a market that is pricing very different risk profiles into each name: Nvidia’s forward multiple of approximately 24x reflects de-rating on competitive concerns despite strong execution, while Broadcom’s 37x reflects contract-backed revenue certainty from locked-in hyperscaler deals extending through at least 2029.

Three watch points going forward:

The H200 approval is real and revenue-generating. But Blackwell remains banned, and the policy window is tied to geopolitical conditions outside Nvidia’s control.

U.S. authorities have authorised ten Chinese firms to purchase the H200, creating a concrete near-term revenue pathway for Nvidia for the first time since the H20 was halted in August 2025. The approvals are material: billions of dollars in hardware demand from named buyers, backed by a diplomatic summit that gave Washington reason to open the door.

The constraints remain equally material. Blackwell stays banned. Performance caps limit what Chinese buyers can extract from the hardware they receive. And the entire licensing regime rests on a geopolitical foundation that could shift with one failed summit session or one congressional vote.

The next testable catalyst is specific: whether the 14-15 May summit communiqué contains any language revisiting next-generation chip restrictions, and whether Nvidia’s Q2 earnings reflect initial H200 order bookings. Both are trackable. Both will determine whether this approval is a one-time concession or the beginning of a broader reopening.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These statements regarding revenue estimates and policy outcomes are speculative and subject to change based on market developments and geopolitical conditions.

The H200 is Nvidia's second-most capable AI processor available for commercial sale, priced at $30,000-$40,000 per unit and designed for large-scale model training and inference at data centre scale. Chinese AI firms need it to compete in the rapidly expanding domestic large language model and generative AI market, making demand structural rather than opportunistic.

The ten firms authorised by the U.S. Department of Commerce to purchase H200 chips are ByteDance, Alibaba Cloud, Tencent Holdings, Baidu, Huawei (scope disputed), SenseTime, iFlytek, Cambricon Technologies, Biren Technology, and Moore Threads, with initial orders capped at 50,000 units per company for Q2-Q3 2026.

ByteDance alone had approximately 200,000 units approved, representing $6 billion-$8 billion in hardware value at $30,000-$40,000 per unit. Estimates for all ten approved companies range widely and have not been independently verified, though Wall Street analysts project China contributing roughly 12% of Nvidia's FY2027 revenue mix.

The Blackwell B200 architecture remains fully banned for export to China as of May 2026, and approved H200 units are subject to performance caps: Total Processing Performance below 21,000 and memory bandwidth below 6,500 GB/s. A 25% tariff, 50% domestic supply priority, and U.S. testing mandates also apply under each licence.

Three key risks have already emerged: congressional opposition, including a bipartisan letter urging Commerce Secretary Lutnick to review the approvals; the unresolved scope of Huawei's licence, which is a pressure point for lawmakers; and the possibility that deterioration of the Xi-Trump summit or escalation of the Iran situation could prompt a policy reversal before approved units ship.