How Zero Commissions Changed the Maths on Thematic ETFs

2 hrs ago

A 33% single-day share price surge sounds like a buying signal. But when that surge is triggered by a multi-hundred-million-dollar contract announcement, the real question is not whether the number is large, but whether it means what it appears to mean.

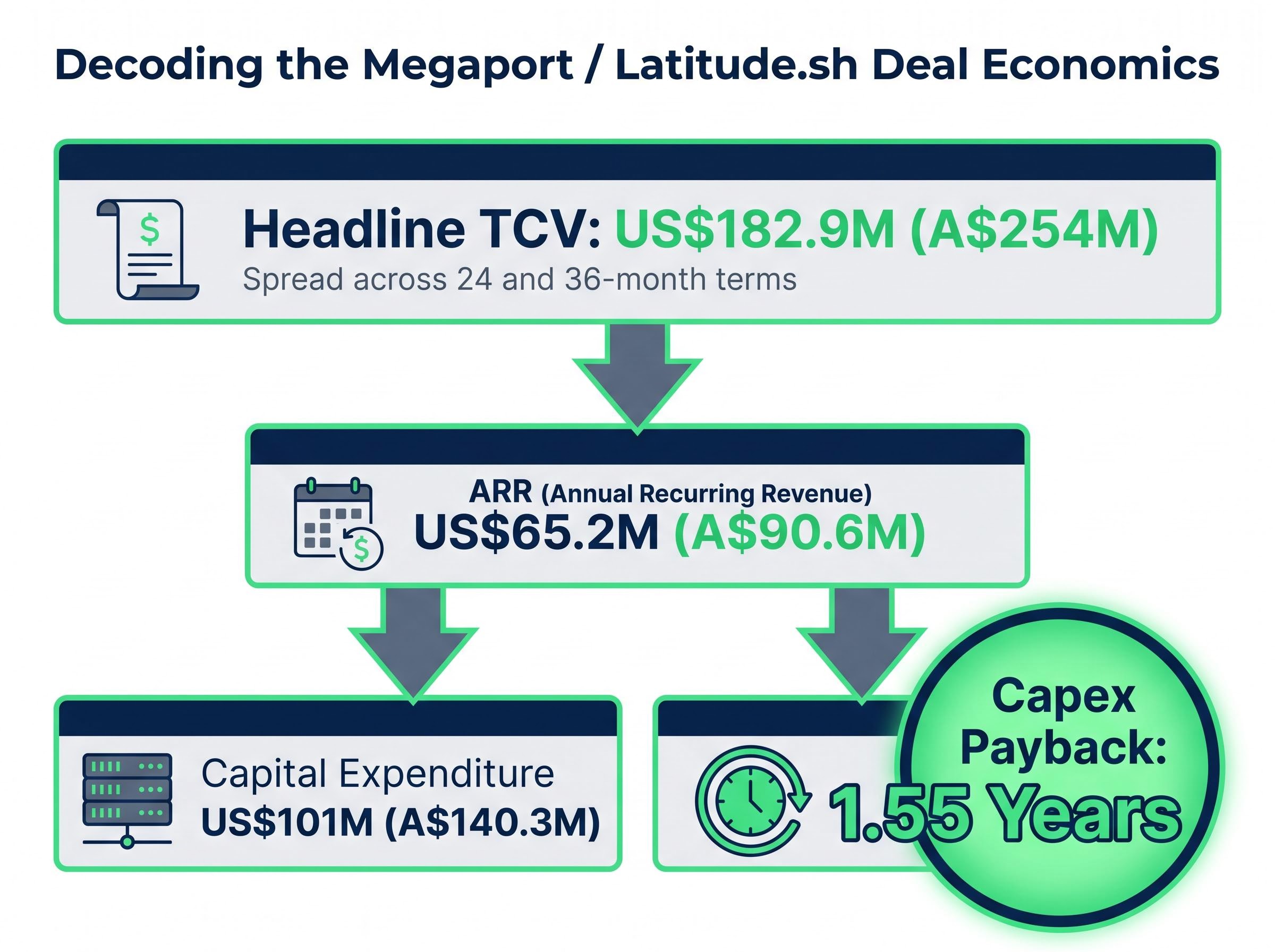

On 14 May 2026, Megaport (ASX: MP1) announced that its subsidiary Latitude.sh had secured three contracts with a combined Total Contract Value (TCV) of approximately US$182.9 million (roughly A$254 million). The market reacted immediately and enthusiastically. Yet analysts covering the stock expressed genuine uncertainty about long-term profitability, even while acknowledging the strong headline figures. That gap between a compelling announcement and honest analyst uncertainty is exactly what this article is designed to close.

What follows is a practical framework for evaluating contracted AI infrastructure deals, built around the Megaport/Latitude.sh contracts as a real-world case study. It covers what metrics like TCV, Annual Recurring Revenue (ARR), and capex payback actually tell investors, and which warning signs separate genuinely value-creating contracts from headline-grabbing announcements.

The instinct to treat a large contract number as good news is reasonable. A US$182.9 million TCV figure is material for a company of Megaport’s size, and the market’s initial reaction reflected that. The problem is that TCV, on its own, is a gross figure. It tells investors nothing about whether revenue is firmly contracted or merely expected, nothing about how that revenue arrives over time, and nothing about the certainty attached to it.

Consider the structure. Two of the three Latitude.sh contracts carry 36-month terms. The third has a 24-month term. Together, they account for all announced TCV, structured as fixed-fee revenue independent of actual usage. That structure matters enormously, but the headline number does not communicate it.

Cash received sooner is worth more than cash received later. A contract spread across three years is worth less in present-value terms than the same dollar figure over eighteen months. And contracts can change; customers can default, renegotiate, or fail to renew.

Every time a TCV figure is announced, investors should ask three questions before reacting:

Analysts treat TCV as a starting point, not value in itself.

These three questions form the foundation of a more rigorous evaluation, one that moves beyond the headline and into the economics that actually drive shareholder value.

TCV introduces the deal. ARR sizes it for comparison. Capex payback tells investors whether the economics actually work. Each metric’s limitation points directly to the next.

ARR, or Annual Recurring Revenue, is TCV standardised to a single year. It is more useful for valuation because it feeds discounted cash flow (DCF) models and allows direct comparison across deals of different durations. The three Latitude.sh contracts produce approximately US$65.2 million in ARR (roughly A$90.6 million). That figure, rather than the headline TCV, is what analysts plug into their models.

But ARR alone does not answer whether the deal creates value. The cost of delivering that revenue matters just as much.

The broader challenge of linking AI hardware spending to revenue is not unique to Megaport; capex monetisation metrics have become the central question for analysts covering hyperscalers globally, where Wall Street is demanding concrete revenue justification within a one-year timeline for investments running into the hundreds of billions.

| Metric | Definition | Megaport Example | What It Tells You |

|---|---|---|---|

| TCV | Total value of all payments over the contract’s full term | US$182.9M (A$254M) | Scale of the deal, but not its annual economics or profitability |

| ARR | TCV divided by contract term, annualised | US$65.2M (A$90.6M) | Comparable annual revenue run-rate for modelling and peer comparison |

| Capex Payback | Total capital expenditure divided by ARR | ~1.55 years | How quickly the investment is recovered through contracted revenue |

Megaport disclosed approximately US$101 million in additional capital expenditure (roughly A$140.3 million), directed primarily at NVIDIA GPU, compute, networking, and storage hardware. Dividing US$101 million by US$65.2 million in ARR produces a capex-to-ARR ratio of approximately 1.55x, implying a payback period of roughly 1.55 years.

A sub-3-year payback on AI infrastructure capex is generally considered strong by infrastructure analysts. The Megaport figure sits at what broker commentary describes as the “very attractive end of the spectrum.”

One caveat deserves attention. That payback calculation assumes the ARR figure reflects actual cash revenue, not merely booked revenue, and that operating expenses (power, cooling, maintenance, software orchestration) do not consume the margin between revenue and capex recovery. Investors should watch for per-cluster margin disclosures over time.

Power, cooling, and facility costs represent the operating expense layer sitting between contracted ARR and actual free cash flow, and physical infrastructure cost inputs including energy agreements and onsite generation are becoming a primary differentiator in whether AI GPU infrastructure margins hold across a full contract term.

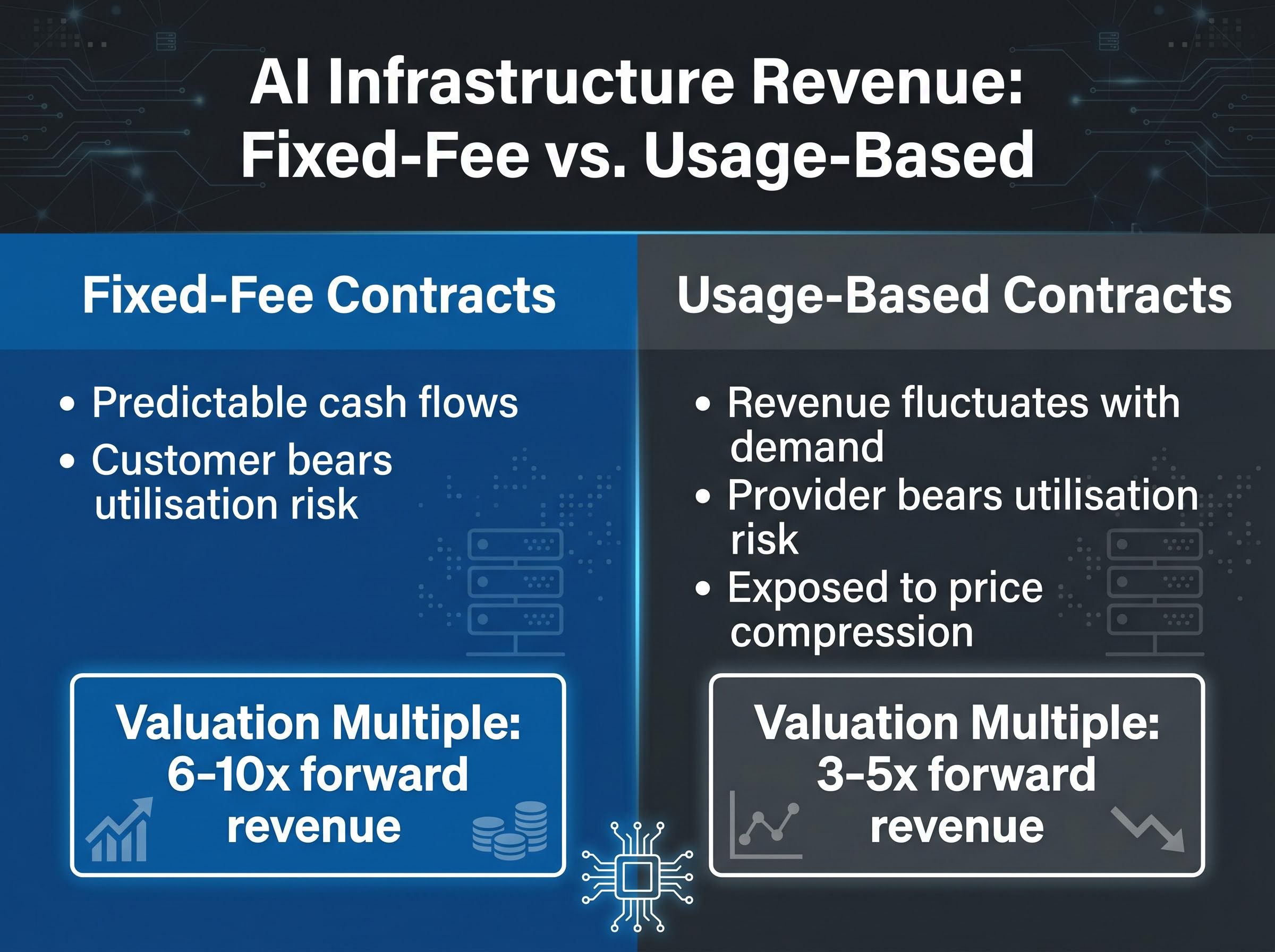

Not all revenue carries the same weight. A dollar of fixed-fee, take-or-pay revenue is valued differently from a dollar of usage-based cloud revenue, and the distinction matters more than most retail investors realise.

A take-or-pay contract obligates the customer to pay regardless of whether they consume the contracted capacity. The customer books capacity, pays for it monthly, and bears the risk of underutilisation. The infrastructure provider receives predictable cash flows that can be modelled with the same confidence applied to lease payments or infrastructure credit.

Usage-based revenue works differently. The provider bears utilisation risk: if the customer scales down workloads, revenue falls. Price compression risk compounds this; as more GPU capacity enters the market, per-unit pricing may decline.

The Latitude.sh contracts are structured as fixed-fee revenue independent of usage levels. This is what allows analysts to apply an infrastructure-style valuation framework rather than a speculative technology multiple.

According to research from Insight Investment (2025), digital infrastructure asset-backed securities (ABS) investors favour contracted, lease-like cash flows over volumetric deals. Fixed Income News Australia (2025) echoes this framing, noting that private credit investors favour “contracted, cash flow-driven returns through underwriting discipline, covenant protections and asset-backed structures.”

Fixed-fee, take-or-pay AI contracts are valued closer to infrastructure-like revenue; usage-based GPU cloud revenue is discounted more heavily due to utilisation risk.

One further detail: upon contract expiry, Latitude.sh’s hardware transfers into its broader compute pool. This recycling provision creates a residual value pathway if customers choose not to renew, partially offsetting the risk of contract non-renewal.

A perfectly structured fixed-fee contract is only as reliable as the counterparty behind it. Customer credit quality and concentration risk rank among the first factors institutional analysts examine when a deal is announced, yet they are often the last thing retail investors consider.

For the Latitude.sh contracts, the immediate analytical questions are specific. Who are the three customers? Are they profitable, well-funded organisations, or speculative AI startups dependent on continued venture capital funding? Does any single contract represent a disproportionate share of group revenue?

ASX continuous disclosure obligations under Listing Rule 3.1 require listed companies to disclose material contracts promptly, but they do not mandate the release of counterparty identity or credit quality data, which is precisely why investors must interrogate those details independently after an announcement.

According to Insight Investment (2025), institutional investors prefer established, investment-grade businesses and cloud providers over smaller “neocloud” startups when evaluating digital infrastructure counterparties. Fixed Income News Australia recommends that private credit investors check for prepayments, security deposits, or parental guarantees when counterparties are not investment-grade.

When evaluating any AI infrastructure contract announcement, investors should ask:

The broader AI infrastructure market offers cautionary examples. Analysis from Morningstar documents how OpenAI, Anthropic, and xAI have entered circular arrangements where hyperscalers or GPU vendors provide capital or equity in exchange for commitments to purchase compute from those same vendors. In these cases, TCV may be artificially inflated by vendor financing or equity kickbacks, and the underlying economics can be opaque.

Investors should also watch for “up to” volumetric revenue presented as if it were contracted TCV. A pattern has emerged across global AI infrastructure deal announcements: large TCV headlines produce an initial share price spike, followed by a second stage where investors reassess contract firmness and counterparty quality. The Sharon AI Holdings experience illustrates this directly. A roughly 30% share price surge on a US$1.25 billion cloud infrastructure deal was followed by analyst questions about the customer’s identity, credit quality, and how much pre-financing was required before cash flows commenced.

The framework above can be compressed into a six-dimension checklist. Each dimension addresses a distinct evaluation question, and the Megaport/Latitude.sh deal provides a worked example for each.

| Evaluation Dimension | Key Question | Megaport/Latitude.sh Answer |

|---|---|---|

| Contract Quality | Is revenue fixed-fee and non-cancellable? | Yes; fixed-fee, usage-independent across all three contracts (24-36 month terms) |

| Customer Risk | Are counterparties creditworthy and diversified? | Three separate customers; individual credit profiles not yet publicly disclosed |

| Economics | What is the capex payback period? | ~1.55x capex/ARR ratio; approximately two-year payback on US$101M capex |

| Residual Value | Can hardware be redeployed if contracts are not renewed? | Yes; hardware recycles into Latitude.sh’s broader compute pool |

| Balance Sheet and Funding | How is capex financed, and what is the leverage impact? | Funding structure not fully detailed; analysts flag this as a key monitoring point |

| Valuation | Does the share price reaction match only announced contracts, or assume future deals? | A$90.6M incremental ARR is material against FY26 revenue guidance of A$302M-A$317M; the 33% surge may price in further contract wins |

Megaport’s FY26 guidance (revenue A$302 million to A$317 million; EBITDA margin 21%-24%) provides the baseline. The incremental ARR of approximately A$90.6 million is significant relative to that base, which partly explains the market’s enthusiasm. The open question is whether the current share price assumes this is the beginning of a series of similar deals, or prices only what has been announced.

AI infrastructure deals earn premium multiples when companies demonstrate a 2-3 year payback on new capex, a high percentage of fixed or minimum-commitment revenue, and counterparties with strong balance sheets.

The 33% share price surge on 14 May 2026 and simultaneous analyst caution are not contradictory. They reflect the fact that several genuine unknowns persist even after a well-structured deal is announced.

Brokers have framed the Latitude.sh contracts as a shift from “networking SaaS” to “AI infrastructure,” a re-rating narrative that justifies higher multiples if execution follows. At the same time, they flag specific concerns: Megaport is moving from a relatively asset-light model into a capex-heavy segment, and Latitude.sh’s history as a smaller neocloud provider raises questions about the capacity to design, deploy, and manage infrastructure at 8,000-10,000 GPU-equivalent scale.

The unresolved questions that explain persistent analyst uncertainty include:

A structural tension sits beneath these questions. The Latitude.sh contracts run for 24-36 months, but GPU and AI infrastructure hardware typically carries an economic life of 4-6 years. The deal economics beyond the first contract term depend entirely on renewal pricing, which is unknown and may be lower if AI compute prices compress as supply expands.

Latitude.sh’s hardware recycling provision partially mitigates this risk by creating a residual value pathway. But it does not eliminate the possibility that second-term economics look materially different from first-term economics. The NEXTDC/OpenAI MoU comparison is instructive here: MoU status versus binding contract is a similar question of announced value versus contractual certainty.

Megaport’s Latitude.sh contracts sit within a broader pattern. Across multiple ASX-listed names, the same sequence is playing out: large headline TCV, strong initial market reaction, followed by analyst focus on contract firmness, capex burden, and counterparty quality.

Megaport’s move into contracted AI compute sits within a rapidly expanding ASX AI infrastructure landscape where colocation operators, property trusts, and network services companies are each capturing different layers of the same structural buildout, with Australia’s data centre capacity projected to more than double from 1,350 MW to 3,100 MW by 2030.

Australian AI data centre market projections through 2031 point to sustained hyperscaler investment and expanding GPU capacity, the same structural forces that create both the demand backdrop for Latitude.sh-style contracts and the potential for per-unit compute pricing compression that weighs on renewal economics.

| Company | Contract Structure | Contract Term | Key Analyst Focus |

|---|---|---|---|

| Megaport/Latitude.sh | Fixed-fee, take-or-pay | 24-36 months | Capex intensity, counterparty disclosure, execution at scale |

| NEXTDC (ASX: NXT) | MoU with OpenAI; $7B S7 Eastern Creek project | Long-dated (details pending) | MoU vs binding contract, equity/debt raising, power grid constraints |

| Macquarie Technology Group (ASX: MAQ) | Sovereign/government workloads with escalators | 5-10+ years | Lower headline growth but high-quality, bond-like cash flows |

The investor reaction pattern across these announcements follows a consistent three-stage arc:

Valuation benchmarks reinforce the pattern. AI-tilted data centre operators with visible contracted growth trade at EV/EBITDA multiples in the high teens to 20x-plus, compared with mid-teens for traditional operators. Fixed-fee, contract-backed revenue attracts 6-10x forward revenue multiples in private and listed transactions, while usage-based or lower-quality revenue compresses to 3-5x. The framework presented in this article applies equally to each of these names, and to any future Australian company announcing AI infrastructure contract wins.

Contracted capacity benchmarks across Australian digital infrastructure are shifting rapidly; CDC Data Centres’ 555MW deal with a US investment-grade hyperscaler, the largest data centre contract in Australian history, illustrates both the scale now available to well-capitalised operators and the counterparty quality standards institutional investors apply when assessing the sector.

Large TCV announcements are a useful starting signal, not a conclusion. The evaluation framework, covering contract quality, ARR, capex payback, customer risk, residual value, and funding impact, is the tool that converts that signal into a judgment.

The Megaport/Latitude.sh contracts show genuinely strong headline economics on several dimensions: fixed-fee structure, a sub-two-year implied payback, and material incremental ARR relative to the existing revenue base. The questions that remain open, around counterparty credit quality, renewal pricing, and capex funding, are not reasons to dismiss the deal. They are the dimensions that separate informed assessment from reflexive enthusiasm.

The next time a company on a watchlist announces a multi-hundred-million-dollar AI infrastructure deal, this framework provides the structure to evaluate it rather than simply react to it.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Total Contract Value is the gross sum of all payments over a contract's full term, representing the scale of a deal but not its annual economics or profitability. Analysts treat TCV as a starting point and convert it to ARR and capex payback ratios to assess whether a deal genuinely creates shareholder value.

Divide the total capital expenditure by the Annual Recurring Revenue (ARR) generated by the contract; a result below three years is generally considered strong by infrastructure analysts. For example, Megaport's Latitude.sh contracts produced a capex-to-ARR ratio of approximately 1.55x, implying a payback period of roughly 1.55 years on US$101 million in capex.

Fixed-fee contracts obligate the customer to pay regardless of actual usage, giving the provider predictable cash flows that can be modelled like lease payments. Usage-based contracts expose the provider to utilisation and price compression risk, meaning revenue can fall if the customer scales down workloads or per-unit compute prices decline.

Key warning signs include undisclosed counterparty identities, revenue described as 'up to' a volumetric figure rather than fixed-fee, vendor financing arrangements that may inflate TCV, and the absence of security deposits or prepayments backing the contract. Analysts also flag concentration risk when a single customer represents more than 25-30% of a provider's total revenue.

ARR standardises the TCV figure to a single year by dividing it by the contract term, making it directly comparable across deals of different durations and enabling use in discounted cash flow models. For the Latitude.sh contracts, a US$182.9 million TCV across 24-36 month terms translates to approximately US$65.2 million in ARR, which is the figure analysts actually use for valuation.