CBA’s Record 10.4% Crash: What Brokers and Charts Now Signal

1 hr ago

The May 2026 Budget did not simply adjust how capital gains are taxed. It dismantled the two-part tax advantage that made leveraged residential property investing the dominant wealth-building strategy for Australian investors for more than two decades. From 1 July 2027, the 50% CGT discount on residential property gains disappears, replaced by cost base indexation and a 30% minimum tax on real gains. Simultaneously, negative gearing deductions for established dwellings are restricted to new builds only.

These two changes, working in concert, alter the after-tax return equation for property investors and shift the relative attractiveness of ASX equities in ways that many investors have not yet fully mapped. What follows is an examination of what the combined reform package means for capital deployment decisions, whether to favour income stocks or growth equities, and how to use the 14-month transition window before 1 July 2027 runs out.

For more than 20 years, leveraged residential property investing in Australia rested on two interconnected tax advantages that no other mainstream asset class could replicate:

The 2026-27 Budget removed both pillars simultaneously for established dwellings. This is not two separate administrative adjustments. It is the structural unwinding of a compounding tax loop.

Properties held before 7:30pm AEST on 12 May 2026 retain existing negative gearing treatment under grandfathering provisions. Gains accrued to 1 July 2027 on existing holdings remain eligible for the 50% discount. New investors in established dwellings, however, lose access to both from the effective date.

The negative gearing restrictions introduced by the Budget extend beyond the property-versus-equities comparison: a 30% minimum tax on trust distributions related to property investment income also takes effect from 1 July 2027, which has significant implications for investors holding established dwellings inside family trust structures.

The replacement mechanism is cost base indexation. Under this approach, the asset’s original purchase price is adjusted upward by the Consumer Price Index (CPI) ratio between the acquisition quarter and the sale quarter. Tax then applies only to gains above that inflation-adjusted cost base.

In practical terms, purely inflationary growth is sheltered. If a property’s value rises only in line with CPI over the holding period, the taxable gain is zero. All real gains above the inflation-adjusted cost base, however, are fully assessable, subject to a 30% minimum tax rate.

As of mid-May 2026, the legislative detail underpinning the apportionment methodology and ATO calculation tools remains outstanding. The policy design is confirmed; the operational mechanics are not.

Consider the illustrative scenario published by Property Principles: a residential property purchased for $700,000 and sold 10 years later for $1,100,000, producing a $400,000 capital gain.

Under the old regime with the 50% CGT discount, the approximate tax liability came to $94,000. Property Principles modelled an indicative increase of approximately $47,000 under a reform scenario, pushing the total toward $141,000.

| Scenario | Purchase Price | Sale Price | Approximate CGT |

|---|---|---|---|

| Old regime (50% discount) | $700,000 | $1,100,000 | ~$94,000 |

| Reform scenario (indicative) | $700,000 | $1,100,000 | ~$141,000 |

The $47,000 indicative difference was modelled against a 25% discount proposal, not the confirmed 30% minimum tax with indexation. The figure is directional rather than precise under the final policy mechanics, which replace the discount mechanism entirely with cost base indexation. Actual outcomes will vary depending on inflation and holding period.

The CGT increase compounds with the negative gearing restriction. An investor in an established dwelling purchased after mid-2027 would lose the annual cash flow benefit of deducting rental losses against wage income and face a larger tax bill at exit. Both sides of the return equation compress simultaneously.

A further consequence that the tax arithmetic does not capture directly is the CGT lock-in effect: higher effective rates at exit discourage asset sales and portfolio reallocation, which may suppress turnover in both property and equities markets in ways that affect price discovery and liquidity independent of the return calculation.

The income-versus-growth distinction under the new regime follows directly from how indexation works in practice:

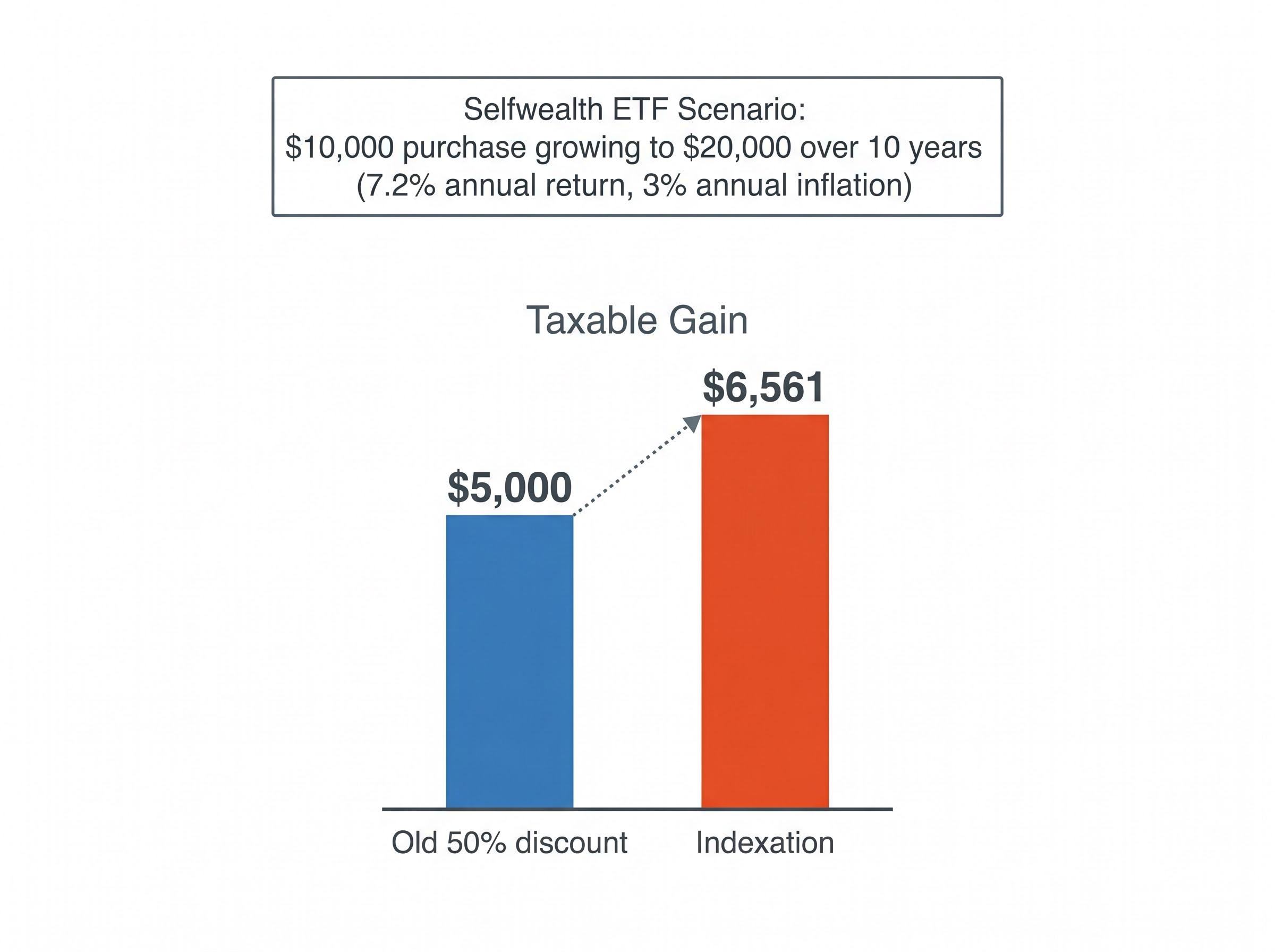

Rob Wilson, Director of Investment Strategy at Selfwealth, illustrated this with an ETF scenario: a $10,000 purchase growing to $20,000 over 10 years at 7.2% annual return, assuming 3% annual inflation. Under indexation, the taxable gain is $6,561; under the old 50% discount, it would have been $5,000. The difference reflects the portion of real gain that indexation exposes but the flat discount previously sheltered.

This is a marginal shift in relative attractiveness, not a directive to overhaul portfolio construction. Risk tolerance, return expectations, and time horizon remain the primary drivers of allocation decisions. The reform adjusts the after-tax calculus at the margin, favouring income-producing assets slightly over those relying purely on capital appreciation.

The post-reform framework creates specific asymmetries between three investment vehicles. Listed equities carry several attributes that benefit indirectly from the changes:

New-build residential property occupies a distinct position. Purchasers of newly constructed dwellings retain the option to choose between the 50% CGT discount or indexation at eventual sale, and negative gearing deductions remain available from 1 July 2027.

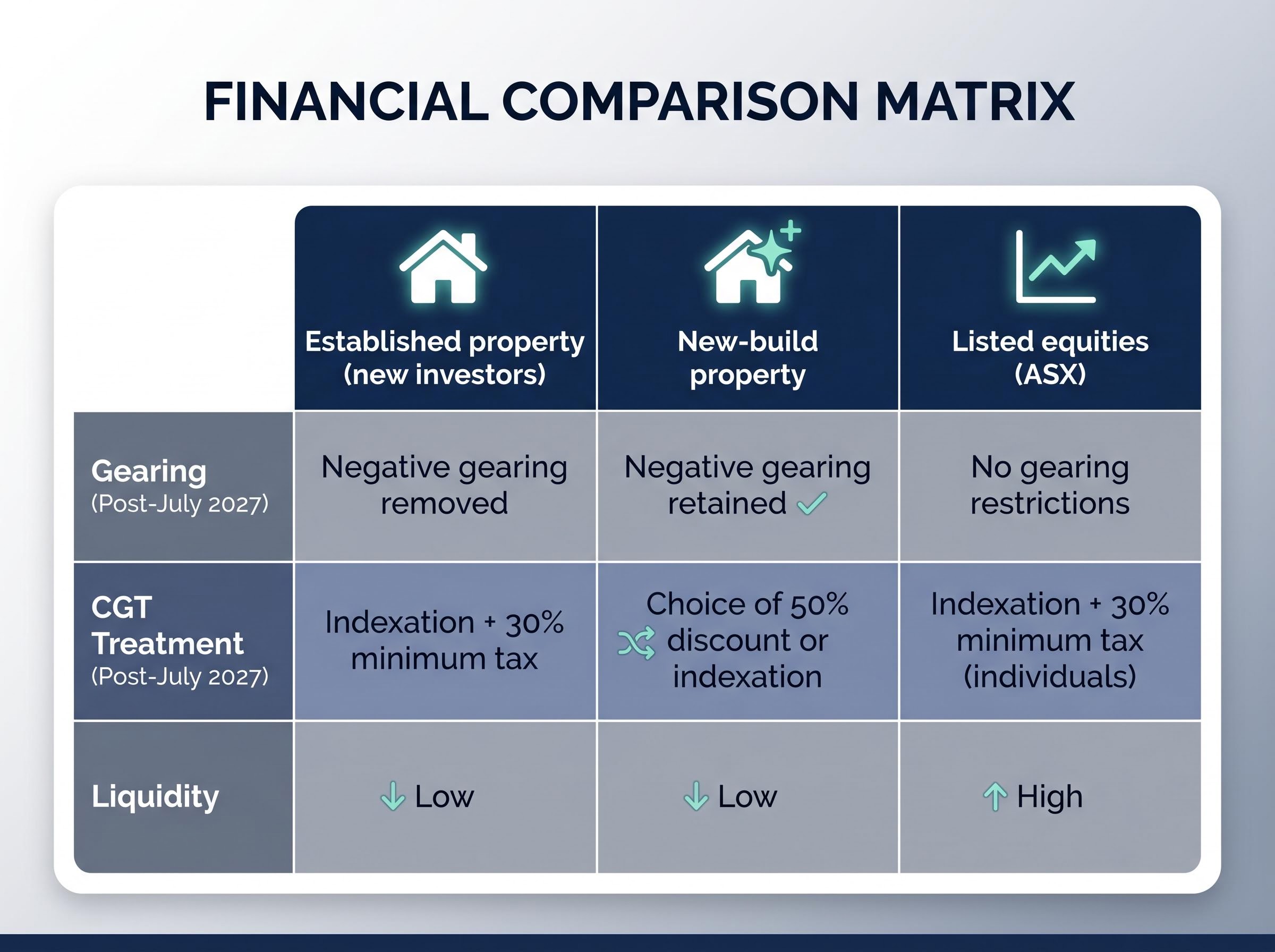

| Investment Vehicle | Gearing (Post-July 2027) | CGT Treatment (Post-July 2027) | Liquidity |

|---|---|---|---|

| Established property (new investors) | Negative gearing removed | Indexation + 30% minimum tax | Low |

| New-build property | Negative gearing retained | Choice of 50% discount or indexation | Low |

| Listed equities (ASX) | No gearing restrictions | Indexation + 30% minimum tax (individuals) | High |

A further consideration applies to investors weighing personal versus entity ownership. The standard company tax rate of 30% (or 25% for base rate entities) is now more closely aligned with the personal CGT minimum rate, which may change the calculus for some investors holding equities through company structures. Companies do not rely on the CGT discount mechanism in the same way as individuals, trusts, and partnerships.

The transition window between the Budget announcement on 12 May 2026 and the effective date of 1 July 2027 gives investors approximately 14 months to plan. That planning opportunity, however, depends on understanding the mechanics of the split.

Gains accrued on existing holdings to 1 July 2027 remain eligible for the 50% CGT discount. Gains accruing after that date fall under the indexation and 30% minimum tax framework. The 1 July 2027 market value acts as the dividing line. Investors may use either an independent valuation or an ATO-approved apportionment formula to determine the split, though ATO tools have not yet been released as of mid-May 2026.

The ATO’s negative gearing and CGT reform guidance confirms the effective dates, grandfathering provisions, and transitional apportionment framework, though the operational calculation tools and approved apportionment formula for transition-date valuations remain outstanding as of mid-May 2026.

The transition planning sequence is straightforward:

The Selfwealth analysis illustrated this with an ETF example: a $10,000 purchase that grows to $12,200 by 1 July 2027 and then to $14,400 at eventual sale, producing a total gain of $4,400 apportioned across two regimes. The pre-commencement portion receives the 50% discount; the post-commencement portion falls under indexation.

The policy design is confirmed, but parliamentary passage and ATO operational guidance remain outstanding. Three specific unknowns are worth monitoring: the ATO valuation calculator release, the precise apportionment methodology for transition-date valuations, and any amendments during the parliamentary drafting process.

Investors with complex holdings, including multiple property parcels, dividend reinvestment plan shares, or trust structures, should seek professional financial and tax advice before making structural changes.

The 2026-27 Budget has redrawn the after-tax return map for Australian investors, though the full contours depend on legislative detail still forming. Three structural shifts are now visible:

No formal investor sentiment surveys or fund flow data yet show measurable asset-class rotation, and the full mechanics await parliamentary confirmation and ATO implementation. Rob Wilson, Director of Investment Strategy at Selfwealth, has noted the Budget’s revenue-neutral design limits direct monetary policy implications, suggesting the investment calculus, rather than macro settings, is where the meaningful change sits.

The franking credit system’s unchanged status, combined with the new CGT framework, reinforces the long-standing logic of holding franked ASX dividend payers for Australian investors building wealth outside superannuation.

Franking credit mechanics become more consequential under the new CGT framework because the after-tax advantage of fully franked distributions relative to capital growth strategies widens when the exit tax on real gains rises, making the grossed-up yield calculation a more central input to stock selection for Australian investors building income-oriented positions.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Forward-looking statements regarding legislative outcomes are subject to change based on parliamentary and regulatory developments.

The May 2026 Budget has structurally altered the relative attractiveness of established property versus equities. Within the equities universe, it has incrementally favoured income stocks over pure capital growth strategies. These are real shifts in after-tax arithmetic, not speculative projections.

The 14-month transition window to 1 July 2027 is a genuine planning resource, but acting before legislative detail and ATO tools are available carries its own risks. The reform is one input into a portfolio review, not a trigger for wholesale restructuring.

The practical next steps remain calibrated: seek professional financial and tax advice tailored to individual holdings, monitor ATO guidance releases as they emerge, and treat the policy change as a structural signal worth incorporating rather than a deadline demanding immediate action.

Investors exploring which income-oriented equity positions are best positioned to capture the after-tax advantages the new CGT framework creates will find our full explainer on high yield ETFs in the current ASX cycle, which examines how the financials and materials rotation drove 22%-plus total returns over 12 months to April 2026 and what structural conditions would need to shift for that income rotation to reverse.

From 1 July 2027, the 50% CGT discount on residential property gains is replaced by cost base indexation and a 30% minimum tax on real gains. Negative gearing deductions for established dwellings are also restricted to new builds only.

Under cost base indexation, the original purchase price is adjusted upward by the CPI ratio between the acquisition quarter and the sale quarter, so only real gains above that inflation-adjusted cost base are taxable, subject to a 30% minimum tax rate.

Gains accrued on assets held before 1 July 2027 remain eligible for the 50% CGT discount, while gains accruing after that date fall under the new indexation framework; investors can use an independent valuation or an ATO-approved formula to apportion gains between the two regimes.

Income-oriented equities with modest capital appreciation have smaller residual gains at sale, meaning the shift from a flat 50% discount to indexation affects them less; investors in these stocks have already realised much of their return through tax-advantaged franked dividends, which remain unchanged by the Budget.

No, the dividend imputation system was not changed by the 2026-27 Budget, meaning the after-tax advantage of fully franked ASX distributions is preserved and becomes comparatively more valuable as the exit tax on real capital gains rises under the new framework.