On the same day Kevin Warsh was confirmed as Federal Reserve Chair, the Bureau of Labor Statistics reported headline CPI running at 3.8% annually, with core services inflation at 4.1% and Brent crude above $107 a barrel. The inflation problem Warsh inherits is not one thing. It is several: shelter costs grinding higher, services prices accelerating, goods inflation re-emerging, and an oil shock driven by military escalation in the Middle East layered on top of all of it.

Warsh’s Senate confirmation on 13 May 2026, by a 51-45 vote, closes a months-long political and procedural saga and opens a new chapter in U.S. monetary policy at one of the most complex inflationary junctures since the post-pandemic surge. Fed officials are openly debating rate hikes. Markets are re-pricing the rate path. And the question of Fed independence is live again.

What follows explains what the confirmation means, why inflation is spreading beyond tariffs and energy, what the Fed’s internal debate looks like right now, and what investors in equities, bonds, and the dollar should be watching.

How Warsh got confirmed, and what the vote revealed

The path to the chair was not smooth. President Trump announced the nomination on 30 January 2026, framing the pick in Oval Office remarks that emphasised Warsh’s independence and hawkish credentials. Then the process stalled.

Senator Thom Tillis placed a hold on the nomination. It stayed in place until the Department of Justice closed its criminal investigation into Jerome Powell over Fed building renovation cost overruns. Once that investigation ended, the hold lifted, and the procedural timeline accelerated:

- 30 January 2026: Trump nominates Warsh as Fed Chair

- 11 May 2026: Senate advances the nomination

- 12 May 2026: Senate confirms Warsh to the Board of Governors (seven-member body), 51-45

- 13 May 2026: Senate confirms Warsh as Chair

- 15 May 2026: Powell’s term as Chair ends; Powell remains on the Board through 2028

The margin itself carried a message. Multiple Senate Democrats cited concerns that Warsh, who advised Trump’s 2024 campaign, would not protect the Fed from White House pressure. That opposition was not partisan reflex alone; it was a policy argument about institutional independence that will shadow every rate decision Warsh makes.

When big ASX news breaks, our subscribers know first

Inflation in May 2026 is not the story policymakers expected

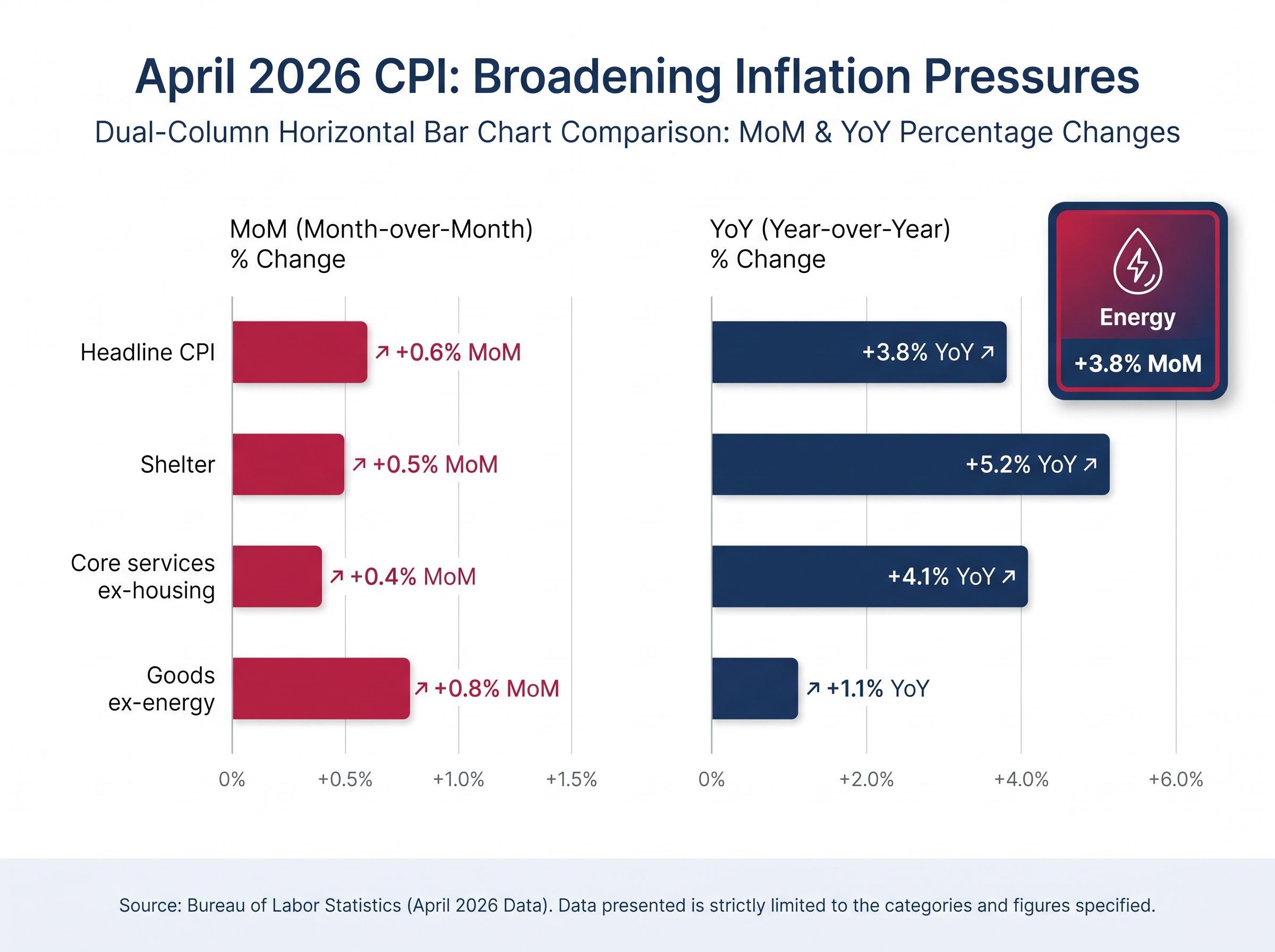

The April CPI report, released 12 May 2026, showed headline inflation rising +0.6% month-on-month and +3.8% year-on-year. Core CPI, which strips out food and energy, came in at +0.4% month-on-month and +2.8% year-on-year.

The April CPI print arrived at double the consensus forecast, a +0.6% monthly reading against the +0.3% expectation, and the immediate market reaction included a sharp repricing of rate-cut probabilities that pushed first-cut forecasts toward 2027 at major Wall Street banks.

Those headline numbers only tell part of the story. The component-level data reveals inflation spreading across nearly every major category simultaneously.

| CPI Component | April MoM Change | April YoY Change |

|---|---|---|

| Shelter (rent, OER) | +0.5% | +5.2% |

| Core services ex-housing | +0.4% | +4.1% |

| Goods ex-energy | +0.8% (apparel) | +1.1% (used vehicles) |

| Food | +0.3% | Eggs +12.5% |

| Energy | +3.8% | Oil-driven surge |

Shelter remains the single largest contributor, running at +5.2% year-on-year with rent rising +0.6% and owners’ equivalent rent up +0.4% in the month. Auto insurance climbed +1.2% and medical care services gained +0.7%, pushing core services excluding housing higher.

The Fed’s preferred gauge tells a similar story. March core PCE, released 3 May 2026 by the Bureau of Economic Analysis, printed at +3.2% year-on-year. The Atlanta Fed’s April tracker estimate came in at +0.32% month-on-month, suggesting no relief in the forthcoming release.

The BEA March 2026 PCE release confirmed core personal consumption expenditures inflation at 3.2% year-on-year, a reading that sits well above the Fed’s 2% target and reinforces the case that price pressures have not been contained to the energy and tariff channels alone.

The Wall Street Journal reported on 11 May that “sticky” core services inflation was running at +4.1% year-on-year, with auto insurance and healthcare leading the persistence.

When inflation broadens across shelter, services, goods, and food simultaneously, it becomes harder for the Fed to characterise it as transitory or sector-specific. For investors, multi-sector inflation persistence changes the rate calculus more than a single energy or tariff spike would.

What the Iran conflict and oil prices add to the problem

The energy component of April CPI, up +3.8% month-on-month, traces directly to the escalation between Israel and Iran. The conflict’s transmission into oil markets followed a specific sequence:

- 8 May 2026: Israeli strikes hit Iranian oil facilities

- 10 May 2026: Iran launched retaliatory drone attacks on Gulf shipping

- 11 May 2026: The U.S. deployed a carrier group to the region

- 13 May 2026: Ceasefire talks stalled, per the UN

No full blockade of the Strait of Hormuz has materialised, but the threat has been enough. Brent crude traded between approximately $107.74 and $110.43 per barrel as of 13 May 2026. WTI crude sat at approximately $102.93. Shipping and freight costs rose an estimated 5% from conflict-related disruption alone, independent of tariff effects.

The forward implication is direct: Brent above $107 during the survey period for May CPI (releasing June 2026) means energy pressure likely intensifies in the next data print.

This is where the policy bind sharpens. Rate hikes are a tool for demand-side inflation, not supply-side energy shocks. The oil component complicates the Fed’s toolkit precisely because raising rates cannot bring the price of crude down. Warsh may be forced into tightening demand at a moment when a supply shock is already weighing on economic activity.

What the Federal Reserve actually is, and why its leadership matters so much right now

The Federal Reserve operates under a dual mandate from Congress: price stability and maximum employment. When those two objectives conflict, as they do now with inflation elevated and economic growth persisting, the Chair’s judgment about which to prioritise shapes the direction of policy for millions of households and businesses.

The Federal Reserve dual mandate framework, as established by Congress, assigns the central bank the twin objectives of price stability and maximum employment, a pairing that places the Chair in the position of arbitrating between competing priorities whenever inflation and labor market conditions pull in opposite directions.

The Board of Governors comprises seven members, and the Chair sets the agenda for Federal Open Market Committee (FOMC) deliberations. The Chair does not hold a formal veto over rate decisions, but the role carries outsized influence over the pace, tone, and communication of monetary policy.

The two tools at the centre of the inflation debate

The federal funds rate is the interest rate at which banks lend to each other overnight. The current target range is 3.50-3.75%. Raising it makes borrowing more expensive across the economy, cooling demand but also slowing growth. Lowering it does the reverse.

The balance sheet is the Fed’s portfolio of bonds and other assets, currently valued at approximately $6.7 trillion. Warsh has characterised the bond portfolio as “fiscal policy rather than monetary policy.” Bloomberg reported on 13 May that Warsh is expected to target $100 billion per month in balance sheet runoff, an acceleration from the current pace that would amount to additional tightening beyond any rate increases.

Accelerated balance sheet reduction, targeting $100 billion per month in runoff, functions as a form of tightening that operates in parallel with rate changes, steepening the yield curve even in periods when short-term rates are held steady, and Warsh has signalled this tool will be deployed independently of the rate path.

Powell’s departure as Chair on 15 May does not remove him from the institution. He remains on the Board through 2028, a potential source of internal divergence if Warsh’s policy direction departs significantly from his predecessor’s preferences.

Inside the Fed, the rate hike debate is already happening

The pressure to raise rates is not coming from one voice. Three regional Fed presidents have made the case publicly, each citing specific data:

- Neel Kashkari, Minneapolis Fed President (12 May, Reuters): “Core services and shelter inflation warrants 25bp hike at June meeting.” He cited core CPI running at +3.9% year-on-year as evidence of persistence beyond the energy shock.

- Lorie Logan, Dallas Fed President (10 May, Bloomberg): Called for “two hikes needed by Q3,” pointing to PCE services at +0.4% month-on-month as a signal of a wage-price spiral forming.

- Raphael Bostic, Atlanta Fed President (9 May, Financial Times): Supported “higher for longer” with a potential 50 basis points in total hikes, citing GDPNow tracking at +2.8% for the second quarter as evidence that the economy can absorb tighter policy.

The FOMC minutes from the April meeting, released 8 May, noted “upside risks to inflation” from services and wages, providing institutional framing that aligns with the hawkish voices.

Yet markets are not fully convinced. CME FedWatch data from 13 May showed 97-98% probability of no change at the June meeting and only approximately 37% probability of any hike before year-end. Goldman Sachs, in a 11 May note, forecast two 25 basis point hikes in June and September, a view meaningfully more aggressive than what futures pricing reflects.

That gap between hawkish Fed rhetoric and restrained market pricing is itself a source of risk. If Warsh’s leadership accelerates the pace toward Goldman’s forecast, the re-pricing in Treasuries and equities could be abrupt.

The fracture across the FOMC has a direct consequence for forward guidance reliability: when dissenters span both hawkish and dovish directions simultaneously, official statements carry less market-calming authority than they did during more unified committee periods, leaving investors to parse individual Fed president remarks for directional signals rather than relying on consensus language.

What broadening inflation and a hawkish new Chair mean for portfolios right now

Moody’s Analytics warned on 12 May that core inflation is broadening toward 4% by summer, a level that would leave the Fed further behind its 2% target than at any point since early 2024.

Equities

The S&P 500 traded at approximately 7,447 on 13 May, with an intraday high of 7,450.94. Sticky inflation and rising rate hike expectations compress equity valuations, particularly for long-duration growth stocks whose future cash flows are discounted at higher rates. Goldman Sachs characterised Warsh as “less dovish than Powell” with a focus on reaching 2% PCE “via demand curbs,” a framework that implies sustained pressure on the multiple investors are willing to pay.

Bonds

The 2-year Treasury yield stood at approximately 4.01%, and the 10-year yield at approximately 4.49%. A materialised hike cycle, even of 50 basis points total, would push the short end higher and steepen or flatten the curve depending on how long-term growth expectations adjust. No cuts are expected until at least Q1 2027 per market median forecasts.

Investors managing fixed-income exposure across multiple markets will find our full explainer on global rate repricing from the oil shock covers Morningstar’s three scenario framework for bond portfolios, the simultaneous policy shifts at the Fed, ECB, and Bank of England, and the emerging market sovereign spread widening of approximately 150 basis points that has accompanied the crude surge since February 2026.

The dollar

The DXY index sat at approximately 98.50, caught between competing forces. A hawkish Fed is dollar-positive, as higher U.S. rates attract capital inflows. Geopolitical uncertainty and fiscal concerns are dollar-negative. The net effect has been modest, but a decisive move toward hikes could tilt the balance.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Warsh starts with a mandate, a debate, and a complication he cannot rate-hike away

Kevin Warsh takes the chair with a confirmed mandate, a growing internal consensus that rates may need to rise, and an oil-driven inflation component that monetary policy cannot directly address. Three signals will clarify the trajectory in the weeks ahead: the pace of balance sheet runoff announcements, the language in the June FOMC statement, and the May PCE data releasing in June.

Markets are pricing restraint. Three Fed presidents are calling for action. Goldman Sachs is forecasting two hikes by September. The distance between those positions will close, one way or the other, during Warsh’s first months.

Powell, still on the Board through 2028, adds an unusual internal dynamic. Whether it becomes a source of friction or continuity will not be resolved quickly.

—