Vanguard VIHY Declares First Distribution at 49.49 Cents per Unit

1 hr ago

The Australian ETF industry crossed $346 billion in funds under management at the end of April 2026, setting a record high in a month when global markets were still absorbing the aftershocks of an active conflict in the Middle East. The milestone is more than a round number. It reflects a structural shift in how Australian retail investors, advisers, and self-managed super fund (SMSF) trustees are building portfolios, with international equities now capturing close to half of all new inflows and thematic technology plays delivering some of the sharpest single-month returns on record.

This analysis unpacks what drove the April record, which asset classes and individual ETFs attracted the most capital, what the macro environment made possible, and what the trajectory toward $400 billion by year-end means for investors evaluating their own allocations.

The headline is the number. The story is how it got there.

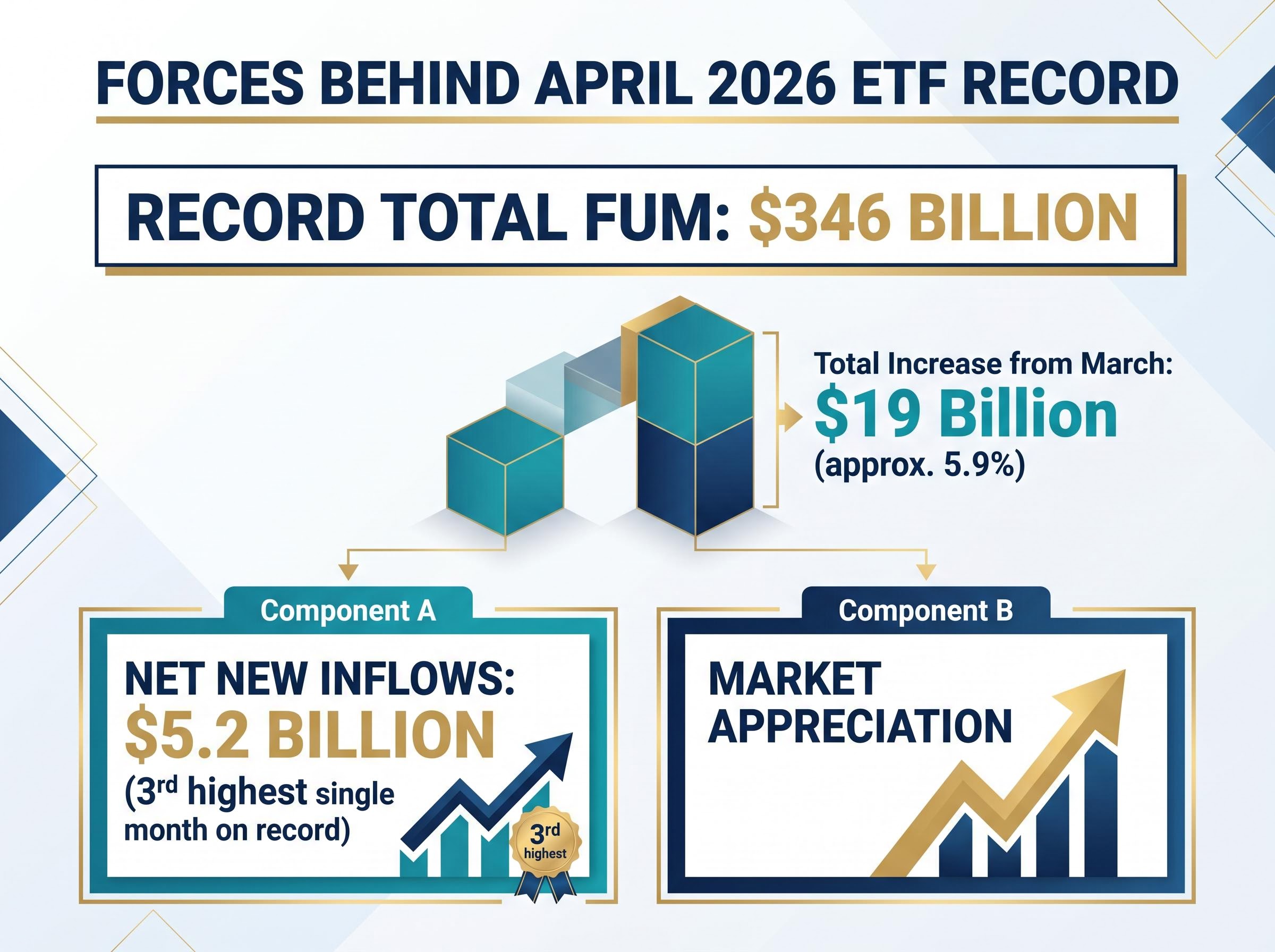

Two distinct forces converged in April 2026 to push industry funds under management (FUM) to $346 billion, an increase of approximately $19 billion (roughly 5.9%) from March. The first was market appreciation: rising equity markets, particularly in international indices, lifted the value of existing holdings across the industry. The second was genuine new capital.

April 2026 at a glance: Net inflows of approximately $5.2 billion made it the third-highest single month on record for the Australian ETF industry, according to BetaShares’ April 2026 review.

That distinction matters. A FUM record driven purely by market appreciation tells investors that index prices rose. A record driven by both appreciation and net new investment signals something broader: conviction. The two drivers broke down as follows:

That this inflow volume arrived during a period of geopolitical volatility, not after it subsided, is the analytically significant detail. Investors were not waiting for clarity. They were allocating through uncertainty.

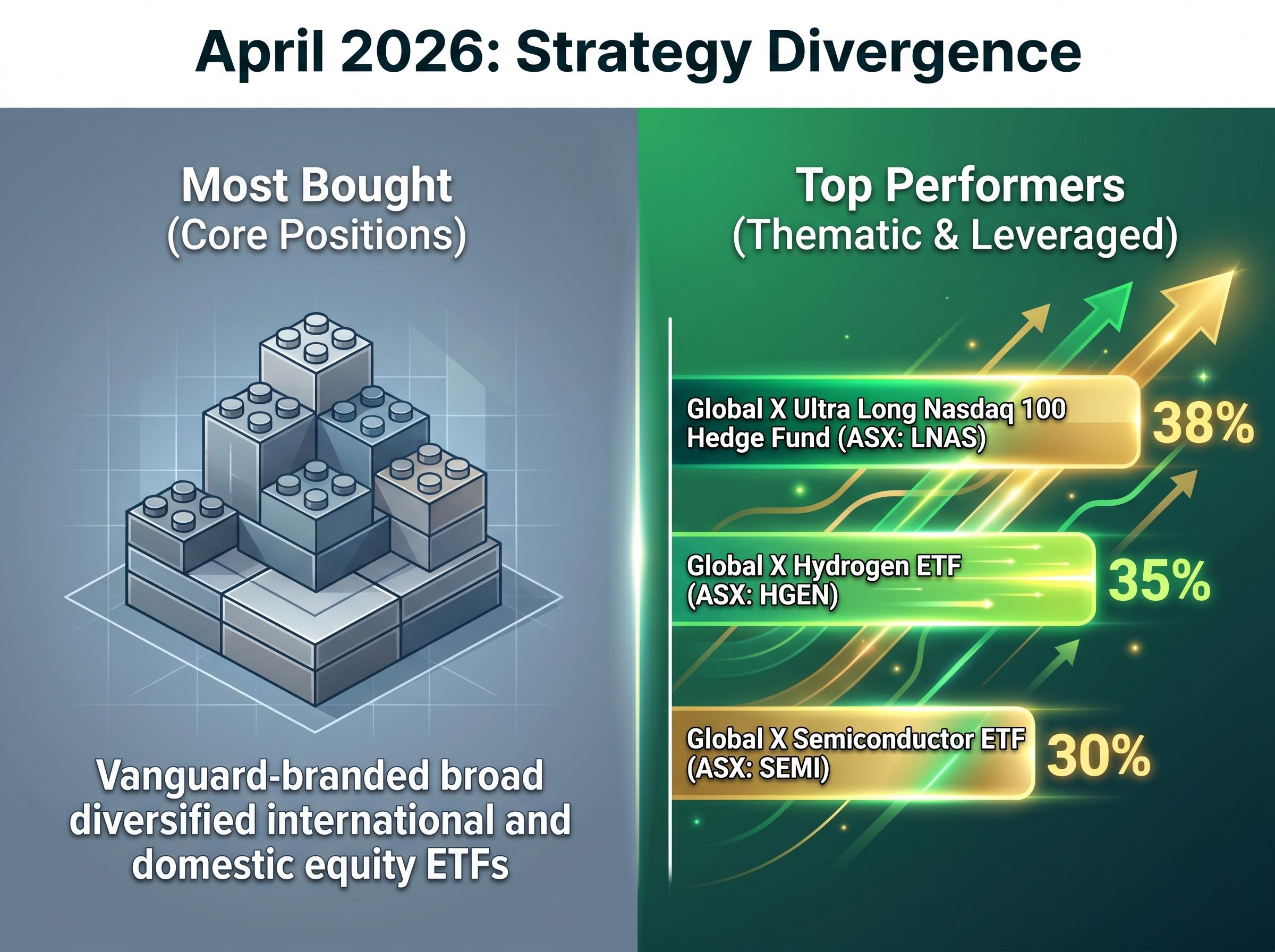

The aggregate flow picture reveals conviction. The product-level data reveals where that conviction is pointed, and the answer splits cleanly into two categories: what investors bought most, and what performed best.

On the inflows side, broad diversified international and domestic equity ETFs led the month. Vanguard-branded products dominated category-level inflows across both segments, consistent with a pattern of investors building core portfolio positions rather than chasing thematic momentum.

On the performance side, the picture looked very different. The top three ETFs by April 2026 return were all leveraged or thematic products:

The divergence between the most-bought and the best-performing products is a meaningful observation. It suggests an investor base that is allocating its largest positions to diversified, low-cost international equity ETFs for structural portfolio construction, while smaller thematic allocations capture momentum in AI hardware, clean energy, and semiconductors.

The thematic categories that dominated performance clustered around three structural themes:

That pattern points to a disciplined investor base, one that separates its core holdings from its thematic tilts and sizes them accordingly.

International equities attracted approximately $2.6 billion in April 2026, representing close to half of total industry inflows for the month, according to BetaShares’ review. This was not an anomaly. Rainmaker data from February 2026 showed international equities already accounting for approximately 43% of total ETF allocations, placing the April result squarely within a sustained directional trend.

| Asset Class | Approximate April 2026 Inflows | Rank |

|---|---|---|

| International equities | ~$2.6B | 1st |

| Australian equities | Significant (second-ranked) | 2nd |

| Fixed income | Meaningful (third-ranked) | 3rd |

The fact that Australian equities and fixed income ranked second and third, respectively, reinforces that this is a portfolio construction story. Investors are not abandoning domestic exposure; they are rebalancing away from a longstanding home bias toward a more globally diversified allocation, and ETFs are the vehicle of choice for executing that shift.

Several converging conditions reinforced international equity flows in April. The Iran conflict, while generating short-term volatility, paradoxically strengthened the case for AI hardware and defence-adjacent technology themes rather than suppressing risk appetite. US mega-cap hyperscalers collectively projected approximately US$755 billion in 2026 capital expenditure, per Q1 2026 earnings analysis by Hugh Lam at BetaShares, anchoring the AI hardware demand narrative.

US dollar weakness following the conflict made emerging market and commodity ETFs more attractive in Australian dollar terms, complementing the developed market AI story. South Korea’s KOSPI, which Hugh Lam at BetaShares described as tripling over the prior year on the back of Samsung and SK Hynix weighting, offered a single-country example of how the semiconductor theme translated into index-level performance.

The industry-level data describes a market. The more practical question is what these trends mean for individual investors reviewing their own portfolios.

Exchange-traded funds are investment products that trade on a stock exchange like individual shares but hold a diversified basket of assets, such as shares, bonds, or commodities. Their structural characteristics have made them the default vehicle for a growing share of Australian investors:

The growing use of ETFs across multiple asset classes, from equities and fixed income to thematic and sector-specific products, points to portfolio maturation. Australian investors are increasingly using ETFs as multi-purpose building blocks rather than treating them as equity-only tools. Fixed income ETFs, in particular, have been described as becoming “an ETP staple” in 2026, according to Financial Standard and Rainmaker reporting.

For SMSF trustees, the structural case for ETFs remains intact, though the regulatory environment deserves attention. The Australian Taxation Office (ATO) has identified SMSF compliance as a top superannuation priority for 2026, with increased surveillance activity focused on governance, coercive control issues, and broader trustee obligations, according to a March 2026 analysis by Dentons.

Division 296 tax, relevant to high-balance SMSF trustees, adds a portfolio construction consideration that may influence how trustees allocate between growth and income positions. The transparency and documentation clarity of ETFs align well with trustee obligations under heightened scrutiny, reinforcing rather than diminishing the case for ETF usage within self-managed funds.

High-dividend domestic equity ETFs continue to attract demand from income-focused SMSF trustees, sitting alongside growth-oriented international positions in what increasingly resembles a core-satellite portfolio approach executed entirely through exchange-traded products.

The industry consensus, supported by BetaShares and MoneyManagement.com.au, places Australian ETF industry FUM at $400 billion or above by the end of 2026.

Industry projection: BetaShares and MoneyManagement.com.au both support a $400 billion year-end FUM target for the Australian ETF industry, implying approximately 16% growth from the April 2026 level.

The structural tailwinds that make this projection plausible are well identified:

The primary downside scenario is also identifiable. General market consensus suggests that a full Strait of Hormuz blockade triggering an oil price spike above 20% could moderate ETF flows by 10-15%. To date, the Iran conflict has functioned more as a volatility source than a structural break, with AI hardware and defence-adjacent themes partially insulating technology-heavy ETF strategies from the geopolitical risk premium.

The adviser-side demand picture reinforces the growth case. According to Advisor Perspectives (May 2026), top adviser concerns this year, including AI integration, downside risk management, and geopolitical navigation, are reshaping portfolio construction toward diversified international ETF exposures. That shift adds a demand-side structural support that exists independently of retail sentiment cycles.

The risk factors that could moderate the trajectory include:

Past performance does not guarantee future results. Industry projections are subject to market conditions, geopolitical developments, and regulatory changes that may alter the growth trajectory.

April 2026’s record was not a single-factor event. It was the convergence of macro recovery, structural AI demand, declining home bias, and maturing ETF usage across asset classes, all arriving in the same month to push industry FUM past $346 billion on verified Q1 inflows of $15.2 billion and estimated April inflows of approximately $5.2 billion, the third-highest monthly figure on record.

The trajectory toward $400 billion means more product choice, continued fee compression, and a deepening secondary market that benefits all participants. Those are structural shifts, not cyclical ones.

The forward signal: The data from April 2026 is most useful not as a celebration of a number but as a directional indicator for where Australian investors are placing conviction, and why examining international and thematic ETF allocations deserves attention in any portfolio review.

For investors and SMSF trustees evaluating their own positions, the question raised by April’s data is not whether Australian ETF adoption will continue growing. The question is whether their own portfolios reflect the structural reorientation the flows describe.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The dominant ETF trends in Australia for 2026 include surging international equity allocations (nearly half of all new inflows), growing fixed income ETF adoption, and strong thematic demand in AI hardware and semiconductor products, with industry FUM reaching a record $346 billion in April 2026.

An ETF (exchange-traded fund) is an investment product that trades on a stock exchange like an individual share but holds a diversified basket of assets such as shares, bonds, or commodities, offering transparency, liquidity, low costs, and broad diversification in a single trade.

The top three performing ETFs in April 2026 were the Global X Ultra Long Nasdaq 100 Hedge Fund (LNAS) with approximately 38% return, the Global X Hydrogen ETF (HGEN) with approximately 35%, and the Global X Semiconductor ETF (SEMI) with approximately 30%.

Both BetaShares and MoneyManagement.com.au project the Australian ETF industry will reach $400 billion or above in funds under management by the end of 2026, implying approximately 16% growth from the April 2026 level of $346 billion.

ETFs are widely used by SMSF trustees due to their transparency, low costs, and documentation clarity, which align well with trustee obligations under increased ATO scrutiny; high-dividend domestic ETFs remain popular for income, while international ETFs support growth-oriented positions in a core-satellite approach.