Morgan Stanley’s S&P 500 Target: What Q1 Earnings Justify

3 hrs ago

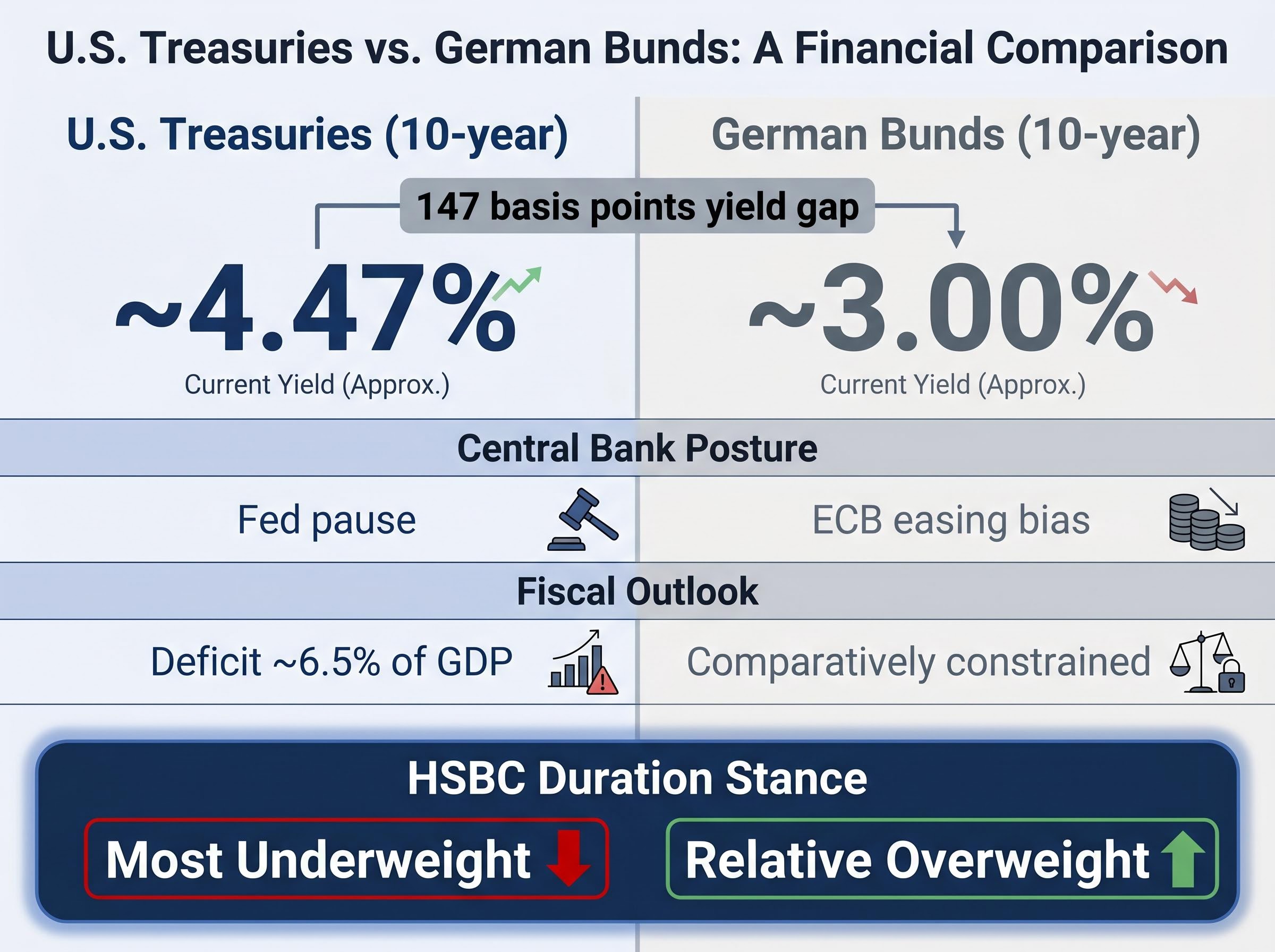

HSBC holds a maximum overweight in global equities and simultaneously treats U.S. Treasuries as its most underweight fixed income position, preferring European sovereign bonds instead. That combination, published by chief multi-asset strategist Max Kettner as of mid-May 2026, sits at the heart of a regional divergence thesis that is more coherent than it first appears. U.S. 10-year Treasury yields sit roughly 147 basis points above German Bund yields. U.S. equities are outperforming European peers year-to-date. European business surveys signal contraction. Yet HSBC’s market outlook favours European duration, European financials, and U.S. consumer discretionary as its three highest-conviction relative value calls.

Understanding why requires unpacking a framework that most surface-level commentary misses: a bank bullish on U.S. equities can simultaneously underweight U.S. bonds and underweight European consumer stocks if the macro divergence between the two regions creates asymmetric return profiles across different asset classes. What follows is a three-part examination of how that logic works, where it is vulnerable, and what data would confirm or disconfirm it through the second half of 2026.

The raw yield gap is unambiguous. The 10-year U.S. Treasury yields approximately 4.47%. The 10-year German Bund yields approximately 3.00%. On an income basis, Treasuries offer 147 basis points more annual carry.

HSBC designates U.S. Treasuries as the bank’s most underweight fixed income position, a stance that prioritises forward price appreciation over current yield.

The logic behind that call is not an income argument. It is a term premium and directional argument. The U.S. fiscal deficit, projected at approximately 6.5% of GDP, introduces structural upward pressure on longer-duration Treasury yields as supply grows. The European Central Bank (ECB), by contrast, has cut rates by a cumulative 25-50 basis points since late 2025, with market pricing reflecting elevated odds of a further cut in June 2026. That easing trajectory supports Bund price appreciation even at lower absolute yield levels, because bond prices rise when yields fall.

Adding to this upward pressure on yields, the increasingly fractured Federal Open Market Committee faces deep internal divisions over sticky inflation that could keep U.S. borrowing costs elevated for an extended period.

The ECB April 2026 monetary policy statement confirmed the Governing Council held rates steady while explicitly declining to pre-commit to a particular easing path, leaving market pricing for a June 2026 cut dependent on incoming inflation and growth data rather than formal forward guidance.

| Metric | U.S. Treasuries (10-year) | German Bunds (10-year) |

|---|---|---|

| Yield (mid-May 2026) | ~4.47% | ~3.00% |

| Central bank posture | Fed pause | ECB easing bias |

| Fiscal outlook | Deficit ~6.5% of GDP | Comparatively constrained |

| HSBC duration stance | Most underweight | Relative overweight |

The distinction matters for readers accustomed to comparing bonds by yield alone. A lower-yielding bond with a falling yield trajectory can deliver superior total returns over a holding period if the price appreciation from declining yields exceeds the income sacrificed. That is the bet HSBC is making.

The European economic data paints a bleak picture. The German ifo Business Climate Index fell to 84.4 in April 2026, down from a revised 86.3 in March, its lowest reading since May 2020. The Eurozone Composite PMI registered 48.6 in April, below the 50 threshold that separates expansion from contraction. Eurozone growth consensus for 2026 sits at approximately 1.0%, compared with U.S. growth tracking approximately 2.5%.

The headwinds are broad:

None of this sounds like a reason to own European bonds. The counterintuitive connection runs through monetary policy.

When survey data deteriorates, the ECB’s easing bias strengthens. Rate cuts reduce short-term yields directly, and expectations of further easing pull longer-duration yields down as markets price in the forward trajectory. That dynamic creates conditions for price appreciation in longer-duration Bunds.

The return profile is asymmetric. If the European economy recovers faster than expected, Bunds give back some gains, but the downside is cushioned by carry. If weakness persists or deepens, Bunds could outperform significantly as the ECB delivers more easing than currently priced. This mechanism operates regardless of whether U.S. yields remain higher in absolute terms; relative directional moves, not absolute levels, drive cross-regional duration preferences.

A contracting European economy and a thriving financial sector seem contradictory. Yet HSBC identifies European financials as its top tactical overweight within European equities, a call echoed by PIMCO, Bank of America, UBS, and Amundi.

The resolution lies in the sector’s earnings drivers, which are less correlated with aggregate GDP growth than headline PMI readings suggest. European banks and insurers benefit from elevated bond yields (which boost insurer investment income), strong capital positions, and shareholder return programmes that deliver value irrespective of whether the broader economy expands.

While broader European equity valuations have compressed under the weight of high energy costs, financial institutions remain uniquely positioned to capture income from the same elevated yield environment that pressures industrial margins.

| Metric | European Financials | STOXX 600 Broad Index |

|---|---|---|

| CET1 ratio (Q4 2025) | 16.18% | N/A |

| Dividend yield | ~5-6% | Lower average |

| YTD performance (mid-May 2026) | Approximately flat to slightly negative | ~-0.07% (MSCI Europe, 30 April) |

| HSBC stance | Top tactical overweight | Neutral |

The 5-6% dividend yield across European banks represents the income anchor of the sector thesis, delivering shareholder returns even in the absence of meaningful price appreciation.

The CET1 ratio (a measure of a bank’s core capital relative to its risk-weighted assets) stands at 16.18% for significant ECB-supervised institutions as of Q4 2025, indicating well-capitalised balance sheets. European Stoxx 600 companies have announced approximately €85.7 billion in buybacks in early 2026, according to Bloomberg, further supporting shareholder returns.

The thesis rests primarily on income return and forward earnings rather than price appreciation already realised. Year-to-date, STOXX Europe 600 Banks have delivered approximately flat to slightly negative returns, broadly in line with the wider MSCI Europe index.

For investors examining the specific profit drivers across the region, our detailed coverage of STOXX 600 earnings forecasts breaks down how commodity tailwinds and financial sector margins are masking flat profitability in other non-cyclical sectors.

The fixed income positioning favours Europe. The equity positioning splits: European financials on one side, U.S. consumer discretionary on the other. The two calls are complementary expressions of the same regional divergence.

Three structural factors underpin U.S. consumer resilience:

Estimated EPS growth for U.S. consumer discretionary sits at approximately 12% for 2026, compared with approximately 5% for European peers.

However, these optimistic full-year projections contrast sharply with recent corporate earnings reports from major consumer brands, which show a marked contraction in demand for big-ticket durables and discretionary services.

European consumer discretionary faces a different set of conditions:

The valuation debate is real. European consumer discretionary trades at approximately 14x forward price-to-earnings, versus approximately 22x for U.S. peers. Morgan Stanley has noted the European discount as a potential mean-reversion opportunity, yet still ranks U.S. consumer discretionary higher on earnings growth grounds. Full-year 2026 S&P 500 estimates continue to move higher, a pattern contrary to the typical seasonal revision pattern where estimates drift lower through the year.

Whether HSBC’s call is a momentum trade or a fundamentals trade depends on whether the earnings growth differential persists. At current estimates, the premium multiple attached to U.S. names reflects superior growth, not speculative excess.

HSBC’s maximum overweight in global equities, published as of 13 May 2026, is the broad stance. The regional divergence calls are the specific expressions within that envelope: European bonds for duration, European financials for income, U.S. consumer discretionary for earnings growth.

Kettner’s framework rests partly on sentiment and positioning indicators. HSBC assesses systematic strategies as having additional buying capacity remaining, a signal the bank uses to gauge whether a rally is crowded. By that measure, the current equity rally is not yet at sell-signal territory.

The credible counterarguments are specific:

PIMCO’s framing of “no duration without yield” represents the clearest institutional counterpoint to the Bund duration thesis, arguing that sub-3% Bund yields do not adequately compensate investors for the price risk of holding longer-duration European sovereigns.

MSCI USA returned approximately +6.9% year-to-date as of 30 April 2026, reinforcing the U.S. equity outperformance that makes the European duration call appear contrarian. The question is whether that outperformance is already priced into relative valuations.

The three HSBC calls will be tested by specific data over the coming months. Rather than offering a vague “markets remain uncertain” closing, the framework produces identifiable signposts.

HSBC’s own internal early warning system, the sentiment and positioning indicators Kettner emphasises, would signal when systematic investors have fully deployed their capacity and the equity overweight becomes crowded. That threshold has not been reached. The bank also holds a more-than-double overweight in local emerging market debt, reinforcing the broader pro-risk positioning stack.

HSBC’s regional divergence thesis is not a bet against the United States. The bank maintains a maximum overweight in global equities, including U.S. equities. The thesis is a set of relative value calls that express where within the global opportunity set the best risk-adjusted returns are likely to emerge: European bonds over Treasuries for duration and term premium reasons, European financials as the continent’s strongest equity exposure on income and capital strength, and U.S. consumer discretionary over European equivalents on earnings growth and labour market fundamentals.

The durability of these calls through the second half of 2026 depends most critically on the ECB’s easing trajectory and whether Eurozone PMI data produces any convincing stabilisation signal. Readers looking to track the thesis in real time should monitor ECB policy decisions, monthly PMI releases, and the U.S.-Europe earnings growth differential as each reporting season arrives.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

As of mid-May 2026, HSBC holds a maximum overweight in global equities, with chief multi-asset strategist Max Kettner identifying European financials and U.S. consumer discretionary as the bank's highest-conviction equity calls within that broader bullish stance.

HSBC's preference for European sovereign bonds over U.S. Treasuries is based on a forward price appreciation argument: the ECB's easing trajectory is expected to push Bund yields lower and prices higher, while the U.S. fiscal deficit (projected at around 6.5% of GDP) creates structural upward pressure on Treasury yields that limits price upside.

European banks and insurers derive earnings from elevated bond yields boosting investment income, strong capital positions (CET1 ratio of 16.18% as of Q4 2025), and shareholder return programmes including approximately 85.7 billion euros in buybacks, all of which are less dependent on broad GDP growth than headline economic surveys suggest.

The thesis would be confirmed by an ECB rate cut in June 2026, Eurozone PMI stabilising near or above 50, and a widening U.S. fiscal deficit; it would be challenged if sticky Eurozone services inflation blocks further ECB easing, the Fed pivots to rate cuts, or a China demand recovery lifts European consumer discretionary above U.S. peers.

Estimated EPS growth for U.S. consumer discretionary stands at approximately 12% for 2026, more than double the roughly 5% forecast for European peers, with U.S. names also supported by a stable labour market and a wealth effect among high-income households driving spending.