How Comcast’s Split Ends a Decade of Conglomerate Discount

43 mins ago

The traditional assumption that a globally diversified portfolio is inherently safe is being tested by two forces arriving simultaneously: one as old as nation-states and one as new as generative AI. In May 2026, Bridgewater Co-CIO Bob Prince appeared at the HSBC Global Investment Summit in Hong Kong, in conversation with Ida Liu, CEO of HSBC Private Bank, and identified modern mercantilism and artificial intelligence as the twin structural forces now reshaping global macro investing. His framing reflects a broader shift in institutional thinking. The era of passive, set-and-forget global allocation is giving way to an environment that demands active macro navigation. What follows unpacks both forces, examines what they mean for regional divergence (with particular focus on Asia), and provides a framework for thinking about portfolio construction in a world that no longer rewards the old defaults.

Prince’s framing at the HSBC summit was not a sector call or a trade recommendation. It was a diagnosis aimed at sophisticated institutional participants: the investment regime itself has shifted, and two forces are driving that shift in ways that interact and amplify each other.

What makes their simultaneous emergence unusual is the tension between them. Mercantilism fragments trade and capital flows, splitting the global economy into competing blocs. AI concentrates them, pulling capital toward a narrow set of enablers (semiconductors, power infrastructure, data centres) at the expense of traditional diversification. The result is divergence at every level of portfolio construction, from geography to sector to currency.

This is not a new idea, but its current form is. US tariffs on Chinese electric vehicles reached 100% in 2024. The White House added semiconductor import restrictions in 2026. The EU moved to block Chinese solar panels from publicly funded projects through procurement rules rather than a traditional tariff mechanism. Each measure uses a different tool, but the strategic logic is the same: trade policy as an instrument of national competitive positioning.

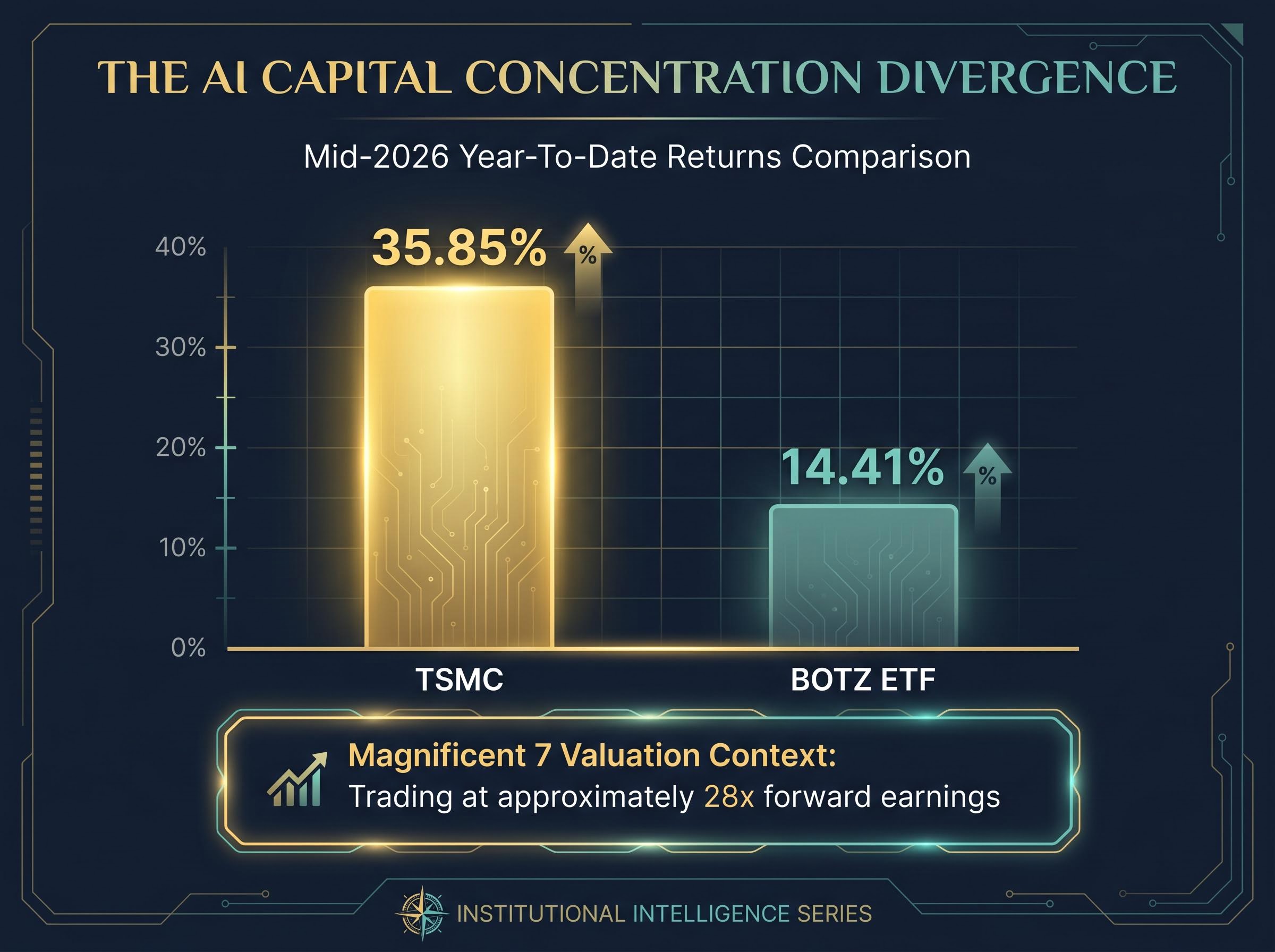

AI’s portfolio impact extends well beyond owning semiconductor stocks. It functions as a macro capital allocation force, drawing institutional spending toward chips, power generation, and data centre real estate. TSMC posted a year-to-date total return of approximately 35.85% through mid-2026. The Magnificent 7 trade at roughly 28x forward earnings, a meaningful premium to the broader market. The concentration is already underway; the question is whether it deepens or corrects.

The mercantilist escalation did not arrive as a single shock. It followed a pattern: tariffs first, then industrial policy, then procurement rules, then friendshoring. Each step raised the cost of cross-border commerce in a targeted sector, and each step made the next one easier to justify politically.

The sequence matters for investors. 100% US tariffs on Chinese EVs in 2024 were followed by semiconductor import restrictions in 2026. The EU’s decision to ban Chinese solar from publicly funded projects used regulatory rules rather than tariffs, a different mechanism producing a similar outcome. The “splinternet” thesis, the fragmentation of trade, technology, and financial systems into US-aligned and China-aligned blocs, is no longer a theoretical framework. It is observable in policy.

The legal underpinning of US tariff authority is itself in flux: two federal courts struck down the broadest statutory pillars of executive tariff power within three months of each other in early 2026, shifting trade policy risk from a binary executive shock model to an extended legislative uncertainty model that analysts at Goldman Sachs and Brookings describe as slower and more priceable for diversified portfolios.

| Policy Action | Jurisdiction | Target Sector | Mechanism | Year |

|---|---|---|---|---|

| 100% EV tariffs | United States | Electric vehicles | Import tariff | 2024 |

| Semiconductor import restrictions | United States | Semiconductors and equipment | Presidential action | 2026 |

| Solar procurement ban | European Union | Solar panels | Public procurement rules | 2026 |

Currency dynamics add a layer of complexity. The renminbi’s share of global payments stood at approximately 3.1% as of March 2026, according to SWIFT data.

At roughly 3.1% of global payments, RMB internationalisation remains a medium-term trend rather than a near-term structural shift. USD dominance is more durable than aggressive de-dollarisation narratives suggest.

The USD/JPY pair moved approximately +0.74% year-to-date, meaning yen depreciation, not the safe-haven strengthening sometimes assumed. Investors who understand the escalation logic can anticipate where the next friction points will emerge, whether in battery materials, pharmaceutical supply chains, or critical mineral processing, before they are priced into markets.

The signal is already visible in market data. TSMC returned approximately 35.85% year-to-date through mid-2026. The BOTZ ETF, a widely tracked robotics and AI basket, returned approximately 14.41% over the same period.

The gap between TSMC’s 35.85% return and the BOTZ ETF’s 14.41% illustrates the divergence between concentrated AI winners and broader AI-themed baskets. The narrative of uniform AI euphoria does not match the data.

That divergence is the first clue that AI’s portfolio impact is not a simple sector trade. It is a macro-level capital flow force that is reshaping sector weightings, energy demand, and infrastructure spending across the entire investment universe.

The distinction matters. Owning AI stocks is a sector bet. Understanding how AI investment reshapes capital allocation is a macro insight. Hyperscaler capital expenditure (from Microsoft, Google, Amazon, and Meta) has concentrated in data centres, power infrastructure, and semiconductor orders, making AI the dominant capex theme of 2024-2026. TSMC’s ongoing Arizona fabrication expansion reflects both commercial demand and geopolitical supply chain hedging.

The productivity supercycle versus bubble risk debate remains genuinely unresolved. Magnificent 7 forward price-to-earnings ratios sit at approximately 28x, a significant premium to the broader market but less extreme than the 45x sometimes cited. The valuation is elevated, not absurd; the risk is concentration and correlation, not necessarily overvaluation in isolation.

US equity market concentration has reached a level with no modern precedent: five companies now control roughly 30% of total US equity market capitalisation, a figure that Goldman Sachs and Morgan Stanley describe as extreme, and one that means passive S&P 500 holders are carrying the AI capital concentration risk the article describes by default, regardless of their stated portfolio intent.

AI’s material requirements have created derivative trades that extend well beyond semiconductor exposure:

Investors who treat AI only as a sector bet miss the broader implication: AI is already reshaping portfolio construction even for those who own no AI stocks directly.

“Asia” is not one investment decision. It is four distinct cases that happen to share a geography, each shaped differently by mercantilism and AI.

Japan’s investment thesis centres on corporate governance reform (cross-shareholding unwinding, improved shareholder returns), robotics leadership, and AI-adjacent semiconductor equipment exposure through names like Tokyo Electron and Shin-Etsu Chemical. The Nikkei returned approximately +17.71% year-to-date. The catch: yen depreciation erodes those returns for unhedged foreign investors, a risk the headline number obscures.

India’s case rests on geopolitically neutral positioning, manufacturing shift beneficiary status through Production-Linked Incentive (PLI) schemes, and domestic AI and data centre investment from conglomerates including Reliance Industries. The NIFTY 50 sat at approximately 23,722 in mid-May 2026, with recent volatility noted. Power grid reliability remains a near-term constraint on data centre expansion timelines.

Southeast Asia, particularly Vietnam and Indonesia, benefits from supply chain diversification. Vietnam has captured Apple and Foxconn manufacturing shifts, while Indonesia’s nickel reserves and battery material processing position it within the EV supply chain.

| Market | Key Theme | Mercantilism Impact | AI Exposure | Key Risk |

|---|---|---|---|---|

| Japan | Governance reform, robotics | Export competitiveness gains | Semiconductor equipment | Yen depreciation for unhedged investors |

| India | Manufacturing shift, PLI schemes | Geopolitically neutral beneficiary | Data centre build-out | Power grid constraints |

| China | Stimulus-driven rallies | Direct tariff headwinds | Domestic AI investment | Policy uncertainty, foreign outflows |

| Vietnam / Indonesia | Supply chain diversification | FDI beneficiary from reshoring | Electronics manufacturing | Infrastructure capacity |

China defies simple categorisation. The bull case is real: fiscal stimulus produced an approximately 10% bounce in the CSI 300 during Q1 2026, and domestic consumption and AI investment continue at scale. The bear case is equally real: 100% US EV tariffs, semiconductor export restrictions, property sector deleveraging, and persistent foreign investor caution create structural headwinds.

The honest assessment is that China warrants selective, hedged positioning rather than binary inclusion or exclusion. The investment case is contested, not closed.

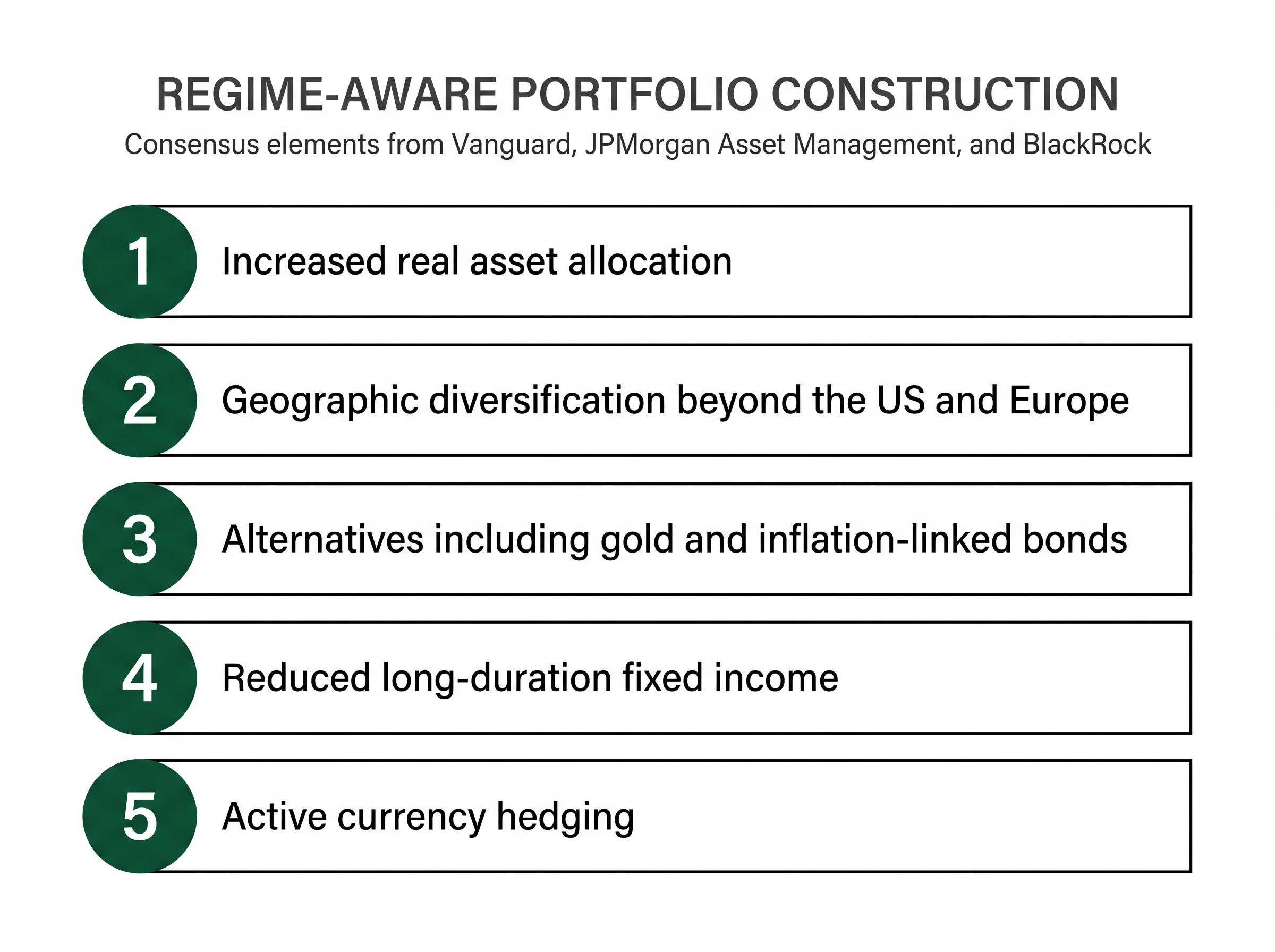

The traditional 60/40 framework faces structural challenges in this environment. Sticky inflation from tariffs, positive equity-bond correlation during inflationary episodes (both asset classes falling simultaneously), and geopolitical risk premia that conventional diversification does not capture all argue for a structural rethink.

The institutional response, observable across research from Vanguard, JPMorgan Asset Management, and BlackRock, has coalesced around what might be called “regime-aware” portfolio construction: adjusting factor exposures based on the macroeconomic regime (inflationary versus deflationary, growth versus recessionary) rather than holding fixed allocations. The five key elements of the emerging consensus, in order of structural priority:

BlackRock Investment Institute’s 2026 outlook identifies the reduced effectiveness of long-dated bonds as portfolio diversifiers as a central challenge, framing the breakdown of the traditional 60/40 as a structural regime shift rather than a cyclical anomaly.

An optimistic multipolar allocation framework can mask specific tail risks that require explicit assessment:

The breadth beneath the index tells a more nuanced story about AI-driven concentration risk: fewer than 60% of S&P 500 constituents are trading above their 200-day moving average despite index-level gains of approximately 14% over 23 trading days, a divergence between narrow headline performance and broad market participation that has historically preceded rotations into segments the concentration trade has left behind.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Both forces Prince identified at the HSBC summit point in the same direction. Mercantilism increases the number of differentiated return outcomes across geographies. AI concentrates capital toward a narrow set of enablers. Together, they mean that passive, market-cap-weighted global allocation increasingly concentrates risk in yesterday’s winners rather than positioning for tomorrow’s opportunities.

According to Bob Prince, speaking at the HSBC Global Investment Summit 2026, the current environment requires active navigation rather than passive positioning, a structural shift in how portfolios should be built and monitored.

Agility does not mean short-term trading. It means building portfolios with the flexibility to shift exposures as regimes evolve, across geographies (US, China, India, Japan) and asset classes (equities, real assets, inflation-linked bonds, currency-hedged positions). The observable data supports the diagnosis: US semiconductor restrictions, EU procurement bans, TSMC’s geographic diversification, the Nikkei’s corporate reform performance, and hyperscaler AI capex as the dominant institutional spending theme all confirm that the forces are real and the divergence is measurable.

The open question every investor faces is not whether the playbook has changed. It is which assumptions need replacing first.

For investors ready to translate the regime-aware framework into specific allocation decisions, our comprehensive walkthrough of geopolitical portfolio resilience covers gold allocation sizing at current price levels, bond duration positioning under stagflationary conditions, rebalancing cadence, and defence sector exposure across a five-component checklist that applies before, during, and after geopolitical shocks.

Modern mercantilism and AI are not transient themes. They are structural forces that have altered the distribution of global investment opportunities in ways that demand a response. Three implications stand above the rest: regional divergence requires country-level precision rather than regional bluntness; AI’s portfolio impact extends far beyond owning AI stocks into energy, infrastructure, and industrial metals; and the 60/40 framework needs structural supplementation with real assets, alternatives, and active currency management.

The investors best positioned for the next cycle will be those who have already updated their assumptions about where risk and return are being created. In a mercantilist, AI-driven world, the cost of holding yesterday’s allocation defaults is no longer theoretical. It is measurable in the divergence already visible across every market discussed above.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Global macro investing involves actively adjusting portfolio exposures across geographies, asset classes, and currencies based on macroeconomic regime shifts. Unlike passive index investing, which holds fixed market-cap-weighted allocations, global macro strategies respond to structural forces like trade fragmentation and capital concentration trends.

Modern mercantilism refers to the use of tariffs, industrial policy, procurement rules, and supply chain reshoring as instruments of national competitive strategy rather than pure economics. For investors, it fragments the global trading system into competing blocs, creating divergent return outcomes across geographies that passive allocation cannot capture.

AI is functioning as a macro-level capital reallocation force, drawing institutional spending toward semiconductors, power infrastructure, and data centre construction. TSMC returned approximately 35.85% year-to-date through mid-2026, illustrating how gains are concentrated in a narrow set of enablers rather than distributed broadly across AI-themed investments.

Sticky inflation from tariffs, positive equity-bond correlation during inflationary episodes, and geopolitical risk premia that conventional diversification cannot capture all challenge the 60/40 framework. Institutional research from Vanguard, JPMorgan Asset Management, and BlackRock points toward regime-aware construction with increased real assets, alternatives, and active currency hedging.

Japan benefits from corporate governance reform and semiconductor equipment exposure, though yen depreciation erodes returns for unhedged investors; India offers geopolitically neutral manufacturing growth via PLI schemes; Vietnam and Indonesia capture supply chain diversification flows; and China presents a contested case with both fiscal stimulus upside and significant tariff and regulatory headwinds.