VAS vs VHY: Why the Lower-Yield ETF Wins in Retirement

5 hrs ago

From 1 July 2027, the same ETF portfolio could face two meaningfully different tax outcomes depending on how often it trades. The gap between those outcomes compounds silently over decades, and the mechanics that determine which side of the gap an investor lands on have nothing to do with stock selection or market timing. They are structural choices about fund turnover, rebalancing method, and asset location.

The 2026 Federal Budget, announced on 12 May 2026, confirmed the replacement of the existing 50% capital gains tax (CGT) discount with inflation-indexed cost base adjustments and a 30% minimum effective tax floor. The policy shift has attracted attention as a headline rate change, but its practical consequences depend less on the new rate and more on portfolio construction decisions that most investors have never treated as tax decisions. What follows explains how the structural features of low-turnover ETF investing, specifically reduced realisation frequency, buy-only rebalancing, and automated cost base tracking, become materially more valuable under the new regime, and what the transitional framework means for investors managing their own records.

Most investors have absorbed the reform as a simple statement: the 50% CGT discount is being removed. That is directionally correct but mechanically incomplete, and the difference matters.

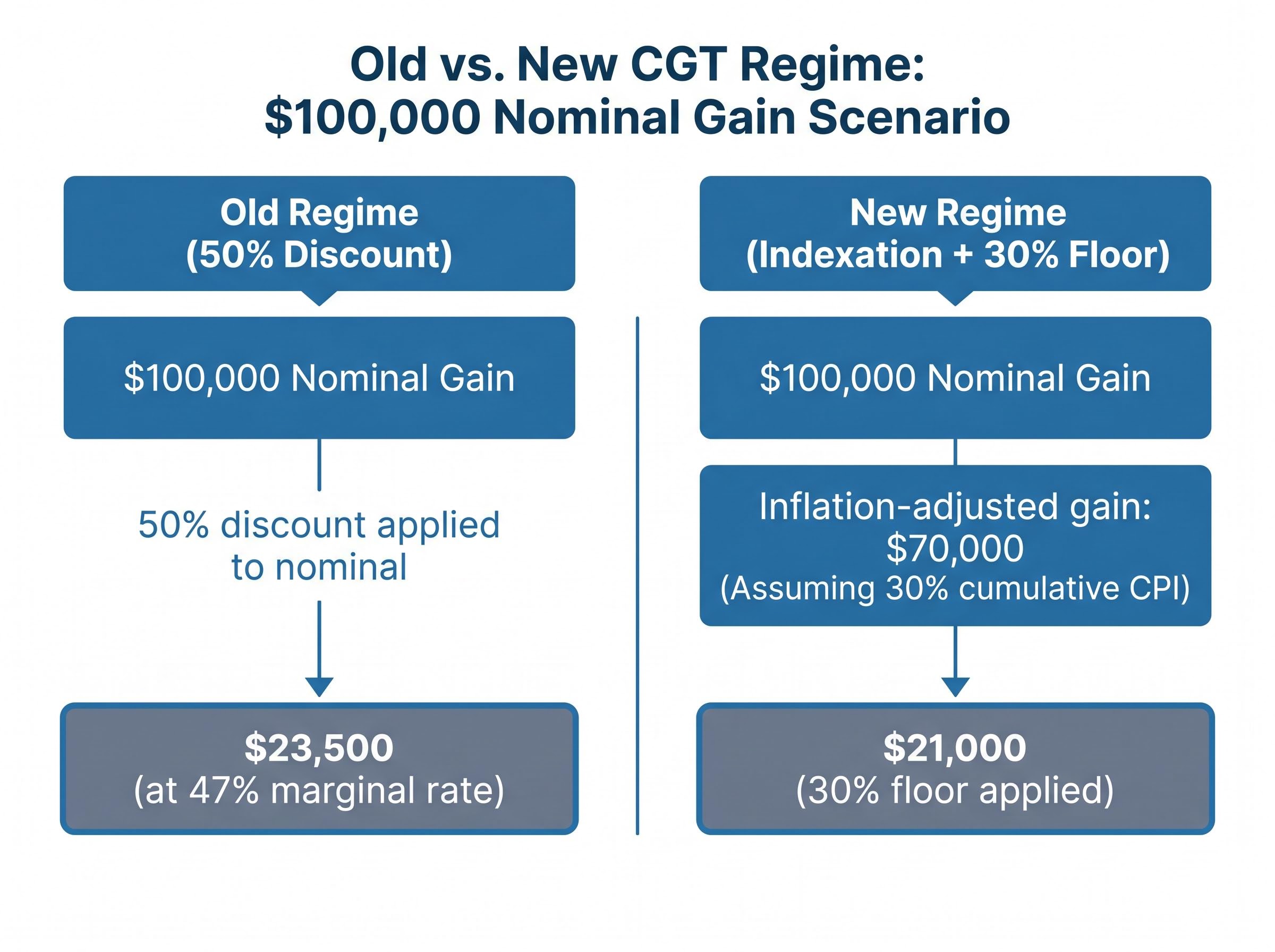

Under the current rules, an investor who holds an asset for longer than 12 months and sells at a gain applies a 50% discount to the nominal gain. For a high-income investor at the 47% marginal rate, this produces an effective CGT rate of 23.5% on the full nominal gain. The calculation is straightforward: half the gain is taxed at the marginal rate.

The new framework replaces that discount with two interacting features. First, the cost base of the asset is indexed for inflation, reducing the taxable portion of the gain to the real return above inflation rather than the full nominal return. Second, a 30% minimum effective tax floor applies to that inflation-adjusted gain. The floor is applied to the post-indexation gain, not to the original nominal amount.

The 30% minimum floor means that no amount of inflation indexation can reduce the effective tax rate on a capital gain below 30%, regardless of the investor’s marginal rate or holding period.

Whether any individual investor ends up paying more or less tax under the new rules depends on three variables: the inflation rate during the holding period, the length of the hold, and the size of the real return above inflation. In low-inflation environments, short holding periods, or scenarios with high real returns, the 30% floor on a modestly reduced gain may produce a higher effective tax burden than the old 23.5% on the full nominal gain.

The transitional rule splits the treatment: gains accrued before 1 July 2027 remain eligible for the 50% discount, while gains accruing after that date fall under the new framework. No draft legislation has been released as of the budget announcement date.

Investors wanting to quantify the dollar impact on specific asset sale scenarios, including a business founder selling a $1 million company, will find our dedicated guide to Australia’s 2026 CGT reform, which walks through the Stockspot modelling behind the $225,000 after-tax proceeds reduction and covers the lock-in effects the higher rate creates for investors weighing whether to sell or hold.

| Variable | Old regime (50% discount) | New regime (indexation + 30% floor) |

|---|---|---|

| Nominal gain | $100,000 | $100,000 |

| Inflation-adjusted gain | Not applicable (discount applied to nominal) | $70,000 (assuming 30% cumulative CPI indexation) |

| Effective tax at 47% marginal rate | $23,500 (23.5% of nominal gain) | $21,000 (30% of inflation-adjusted gain) |

The illustrative scenario above shows a case where significant cumulative inflation benefits the investor under the new rules. Where inflation is lower or the hold shorter, the outcome reverses.

Under the old regime, frequent trading was penalised, but the 50% discount softened the blow for any asset held beyond 12 months. The discount was generous enough that many investors treated the choice between low-turnover and high-turnover strategies as a matter of style rather than a material tax decision.

The 30% floor changes that calculation. Each unnecessary sale now triggers a minimum effective tax rate that does not diminish with holding period in the way the old discount suggested. The cost of every intermediate decision to sell rises, and portfolio construction choices that reduce the number of those decisions become genuinely strategic.

The distinction is visible across fund types. Low-turnover passive ETFs such as VAS (Vanguard Australian Shares, approximately 3% annual portfolio turnover) and VGS (Vanguard International Shares, approximately 5% annual turnover) generate relatively few CGT events. Active equity managed funds, by contrast, typically turn over 20-50% of their portfolio annually. That difference is no longer a marginal tax consideration; it is a structural one.

The ASX ETF structure that makes low-turnover passive funds so tax-efficient under any CGT regime, specifically the legally separate unit trust with independent custodian and the in-kind creation and redemption mechanism, means the fund itself rarely triggers internal realisation events, leaving the investor in control of when taxable disposals occur.

Three vehicle types illustrate the spectrum:

Unit trust distributions create a distinct problem. When a fund manager trades internally, realised gains flow through to unitholders as taxable distributions at the end of each financial year. The investor has no say in the timing, the size, or the frequency of those events.

Under the old regime, the 50% discount cushioned those involuntary distributions. Under the new framework, each distributed gain is subject to the 30% floor without the investor having chosen the moment of realisation. For investors who would otherwise have deferred that gain for years or decades, the annual distribution creates a compounding tax cost that accumulates silently.

The shift in rebalancing logic is practical, not theoretical. Consider the two common approaches.

Calendar-based rebalancing sells overweight positions at set intervals, typically annually or quarterly, to restore target allocations. Each sale is a realisation event. Under the new regime, each of those events carries a minimum 30% effective tax rate on any real gain, regardless of whether the drift was material enough to warrant action.

Threshold-based rebalancing takes a different approach. The investor defines a drift band, commonly 5-10%, and takes no action until an allocation breaches it. This defers realisation events to moments of genuine material drift rather than generating them on a calendar cycle.

Buy-only rebalancing goes further. The sequence is straightforward:

The third step is where the compounding advantage emerges. A gain that has not yet been taxed continues growing on the full amount. A gain that has been realised and taxed grows only on the after-tax remainder. Over 10, 20, or 30-year horizons, this difference accumulates disproportionately because early-period tax drag reduces the base on which all subsequent returns compound.

For a long-horizon investor, deferring a taxable event in year five of a 30-year accumulation phase does not merely save tax in year five. It preserves a larger compounding base for the remaining 25 years, and the cumulative difference grows with every year of deferral.

The rebalancing method is not an operational preference. It is a compounding decision.

For investors ready to implement threshold-based or buy-only rebalancing in practice, our comprehensive walkthrough of tax-efficient rebalancing for Australian investors covers the full execution sequence, including how to rebalance inside superannuation or SMSF structures at the 15% concessional rate, alternative capital destinations for trimmed equity positions, and the specific drift thresholds most commonly recommended by Australian advisers in 2026.

The comparison between superannuation and personal ownership is not a new consideration, but the reform recalibrates it in a way that requires investors to revisit decisions made under a different set of assumptions.

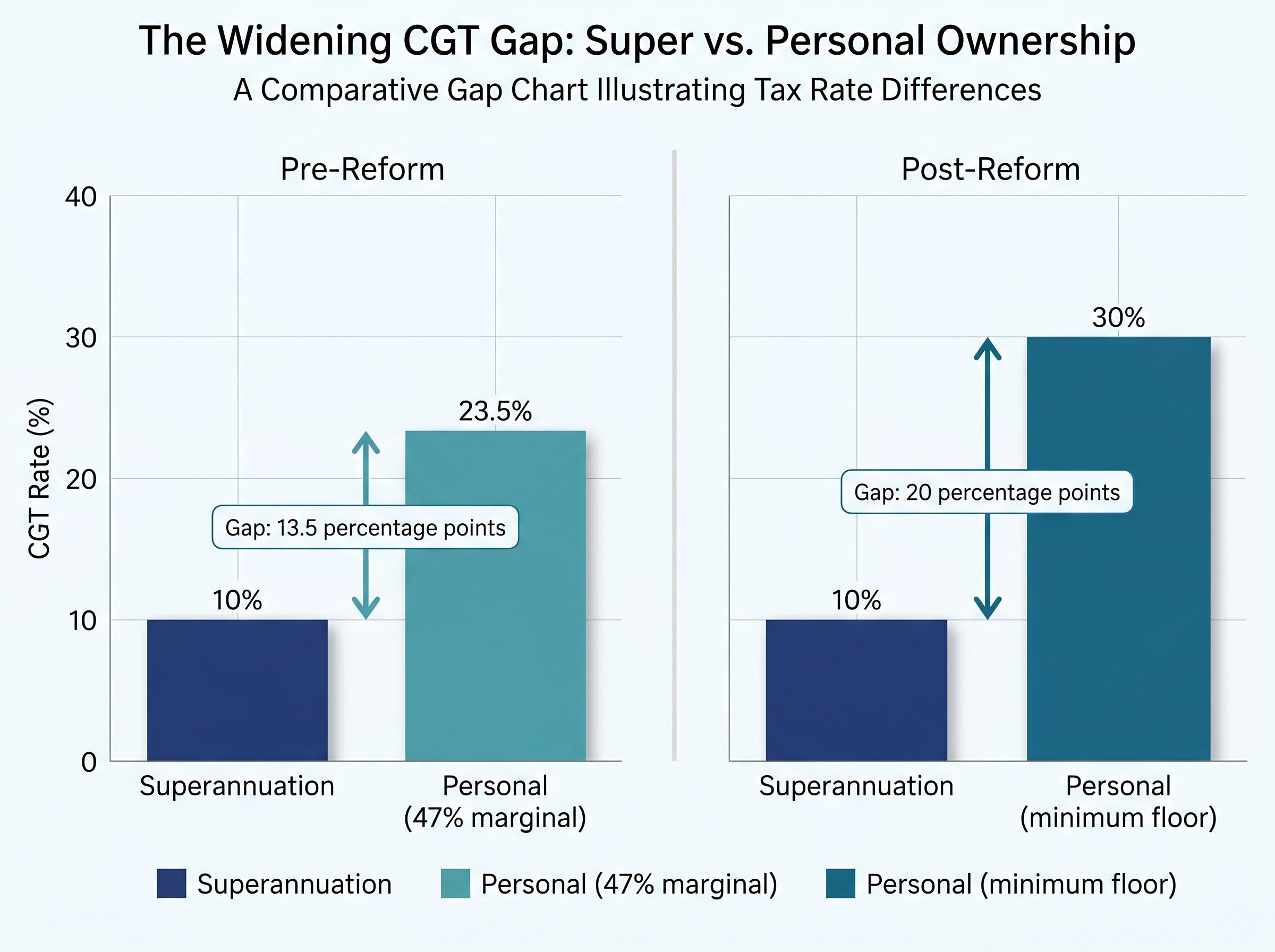

Superannuation funds are taxed at 15% on earnings, including capital gains. For assets held longer than 12 months, a one-third discount applies, producing an effective CGT rate of 10% within super. According to ATO guidance on super fund tax on income and investments, this concessional treatment remains unchanged by the 2026 budget reform. The 30% floor applies in the personal (non-super) context only.

The arithmetic has shifted. Before the reform, an investor at the 47% marginal rate holding growth assets personally paid an effective 23.5% CGT rate, compared with 10% inside super. The gap was 13.5 percentage points. After the reform, that personal rate rises to a minimum of 30%, widening the gap to 20 percentage points.

| Scenario | Effective CGT rate |

|---|---|

| Superannuation fund (long-held asset) | 10% |

| Personal investor, pre-reform (47% marginal rate) | 23.5% |

| Personal investor, post-reform (minimum floor) | 30% |

Investors who previously held growth ETFs in personal accounts because the 23.5% rate felt acceptable relative to super’s 10% may find the 30% floor prompts a genuine reconsideration of asset location, particularly for contributions still within concessional limits. The reform does not change the rules inside super, but by raising the rate outside it, the relative advantage of superannuation for long-term growth asset accumulation has widened materially.

The 2026 superannuation cap changes, including the concessional cap rising to $32,500 from 1 July 2026 and the permanent expiry of unused cap amounts from FY2020-21 on 30 June 2026, create a narrow, time-sensitive window for investors who are actively shifting asset location decisions in response to the CGT reform.

The strategic implications of the reform are one thing. The operational reality of the transitional framework is another, and for self-directed investors, it introduces a level of administrative complexity that has no precedent in Australian CGT compliance.

The core problem is split-gain tracking. An asset acquired before 1 July 2027 and sold after that date will require the total gain to be apportioned between the pre-transition period (eligible for the 50% discount) and the post-transition period (subject to the new indexation and floor framework). The method for that apportionment, whether time-based proration, actual market value at the transition date, or another approach, has not been confirmed in draft legislation as of 12 May 2026.

For investors holding positions across multiple platforms, the reconciliation challenge compounds. CommSec, SelfWealth, and Stake do not share data with each other or with the ATO. Acquisition dates and cost bases must be reconciled manually across systems that were never designed to produce split-period breakdowns. Current ETF issuer annual statements do not provide this information either, because it has not previously been required, and no confirmed timeline exists for when that capability will be available.

Four items remain unresolved and are being monitored by investors and advisers:

None of the three actions below require waiting for draft legislation, and all reduce complexity regardless of how the final rules are framed.

First, consolidate holdings onto a single brokerage platform. Multi-broker portfolios create the greatest reconciliation risk. A single platform simplifies acquisition-date tracking and reduces the number of systems that need to be reconciled at tax time.

Second, establish a complete acquisition-date and cost-base register for every existing position. This includes recording the purchase date, price paid (including brokerage), and any corporate actions (such as share splits or return of capital distributions) that have adjusted the cost base. The register should be created now, while records are accessible, rather than reconstructed retrospectively.

Third, engage a tax adviser early. Demand for transitional CGT advice is expected to surge as the 1 July 2027 date approaches, and early engagement allows time to structure responses thoughtfully rather than reactively.

The reform does not require a portfolio overhaul. It does, however, reward investors who have already built their portfolios around structural minimisation of taxable events, and it penalises those who have not.

Four structural features become more valuable under the new regime:

None of these are new ideas. The reform raises the return on each of them.

The limits of structural optimisation are real. The reform’s interaction with inflation, holding period, and real returns means no single portfolio configuration is universally optimal. Investors with complex existing positions, significant unrealised gains, or holdings across multiple trusts and entities should seek specific advice tailored to their circumstances.

Remaining invested in a diversified, low-friction structure through a policy transition typically produces better outcomes than reactive restructuring timed to anticipated legislative outcomes that have not yet been legislated.

Exposure draft legislation and Treasury consultation are expected in the second half of 2026. Final rules may differ materially from the budget announcement. All current planning is based on announced policy only, and no binding ATO guidance has been released as of 12 May 2026.

The reform raises the cost of every unnecessary realisation event. Portfolio construction choices that minimise those events, from low-turnover ETF selection to buy-only rebalancing, compound in value over long horizons. The structural advantage is not new, but the size of the advantage has increased.

The transitional framework creates a narrow window for preparation, particularly around record-keeping and platform consolidation, that does not depend on draft legislation. Investors who act on these administrative steps now avoid the retrospective reconciliation problem that will affect those who wait.

All analysis in this piece is based on the budget announcement of 12 May 2026. Draft legislation expected in the second half of 2026 may alter the mechanics materially. Investors with significant unrealised gains should consult a qualified tax adviser before making changes to their portfolio structure or asset location.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

The 2026 Federal Budget, announced on 12 May 2026, replaces the existing 50% capital gains tax discount with inflation-indexed cost base adjustments and a 30% minimum effective tax floor, applying to gains accrued from 1 July 2027 onward.

Under the new rules, every sale of an ETF holding triggers a minimum 30% effective tax rate on the real (inflation-adjusted) gain, meaning frequent trading or calendar-based rebalancing carries a higher and unavoidable tax cost compared to strategies that defer realisation events.

Buy-only rebalancing means directing new cash contributions toward underweight portfolio positions rather than selling overweight ones, which avoids triggering taxable disposal events and allows unrealised gains to keep compounding on the full pre-tax amount over time.

Superannuation funds pay an effective 10% CGT rate on long-held assets, a treatment unchanged by the 2026 reform, while personal investors now face a minimum 30% floor, widening the gap between the two from 13.5 percentage points to 20 percentage points.

Investors should consolidate holdings onto a single brokerage platform, create a complete acquisition-date and cost-base register for every existing position, and engage a tax adviser early, as the transitional framework will require splitting gains between pre- and post-transition periods for assets held across the cutover date.