Barclays Warns of Prolonged Market Volatility Under New Fed Reality

15 hrs ago

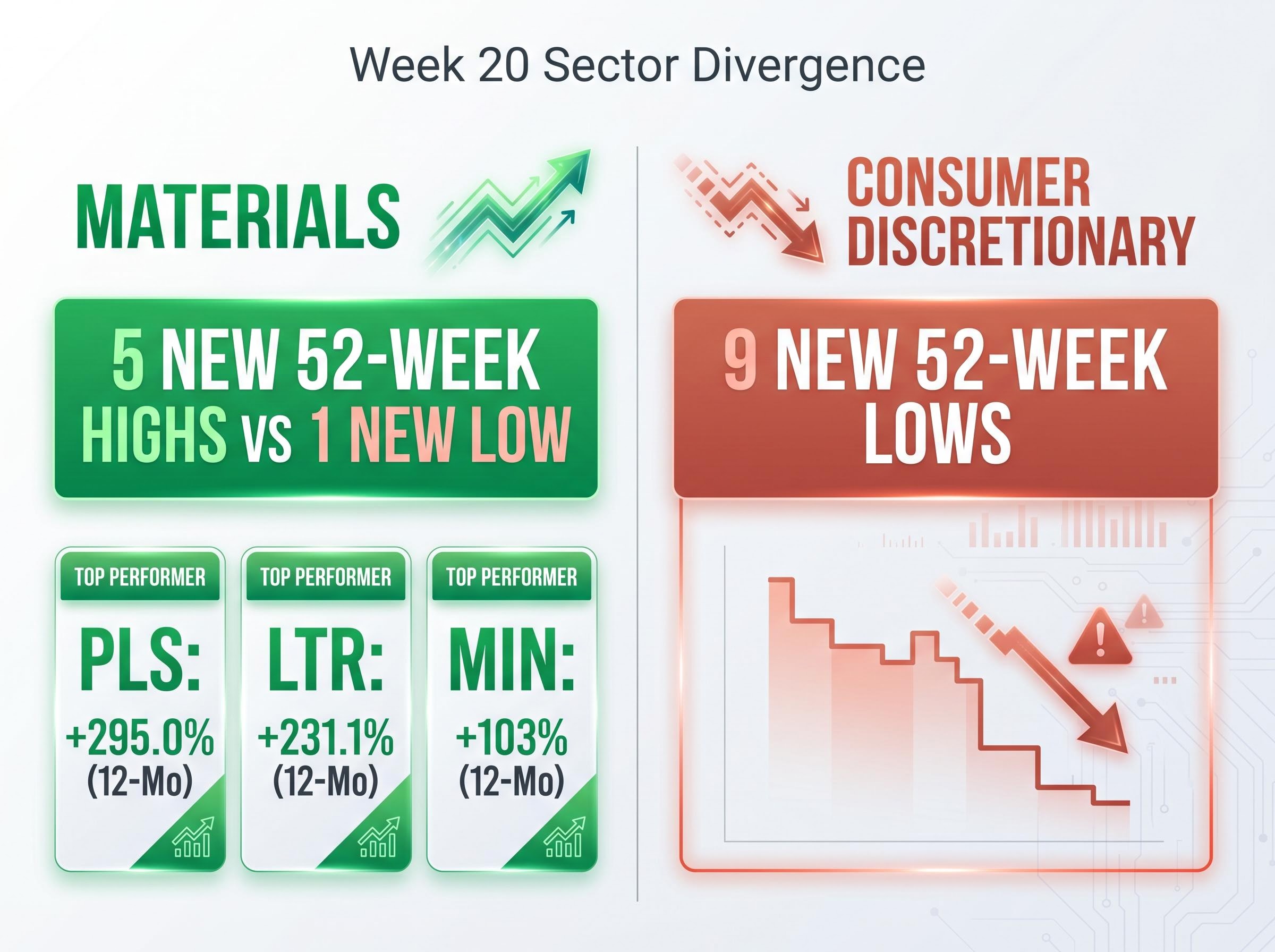

Lithium carbonate spot prices have surged approximately 65% year-to-date to reach their highest level since August 2023, and ASX lithium stocks are responding in kind. Pilbara Minerals (ASX: PLS) has gained 47% year-to-date, Liontown Resources (ASX: LTR) has climbed 286% over the past 12 months, and Mineral Resources (ASX: MIN) has gained approximately 103% over the same period. The week ending 8 May 2026 produced the most concentrated cluster of new 52-week highs in the materials sector since the commodity supercycle peak, with five materials stocks hitting annual highs against just one new low. The rest of the ASX 200 tells a different story: healthcare and consumer discretionary are deep in correction territory, with discretionary posting nine new 52-week lows in the same week.

This article covers what is driving the lithium and resources breakout, which stocks are leading it, what structural forces are sustaining the rally beyond electric vehicle demand, and what the current M&A wave signals about where strategic capital is flowing.

Five ASX materials stocks printed new 52-week highs in Week 20, against just one new low. Consumer discretionary, by contrast, recorded nine new lows. The divergence is the sharpest single-week gap between the two sectors this year.

The prior week’s 52-week high cluster, covering the seven days ending 1 May 2026, showed eleven ASX 200 names hitting new annual highs with Liontown Resources leading at a 12-month gain of 412.6%, providing a baseline against which Week 20’s more concentrated five-stock reading can be assessed.

PLS closed at $6.26, up 2.0% for the week and 295.0% over the prior 12 months. LTR closed at $2.45, up 231.1% over 12 months. MIN hit $69.55, gaining 4.3% on the week and 103% over the year.

The breakout extends beyond lithium. Nickel Industries (ASX: NIC) closed at $1.09, up 2.4% for the week and 73.0% over 12 months, while Rio Tinto (ASX: RIO) reached an all-time high of $178.72, up 3.9% on the week and 49.1% over the year. This is not a single-stock anomaly; it is a sector-wide repricing.

| Ticker | Close Price | Weekly Change | 12-Month Change | 52-Week Status |

|---|---|---|---|---|

| PLS | $6.26 | +2.0% | +295.0% | New 52-week high |

| LTR | $2.45 | — | +231.1% | New 52-week high |

| MIN | $69.55 | +4.3% | +103% | New 52-week high |

| NIC | $1.09 | +2.4% | +73.0% | New 52-week high |

| RIO | $178.72 | +3.9% | +49.1% | All-time high |

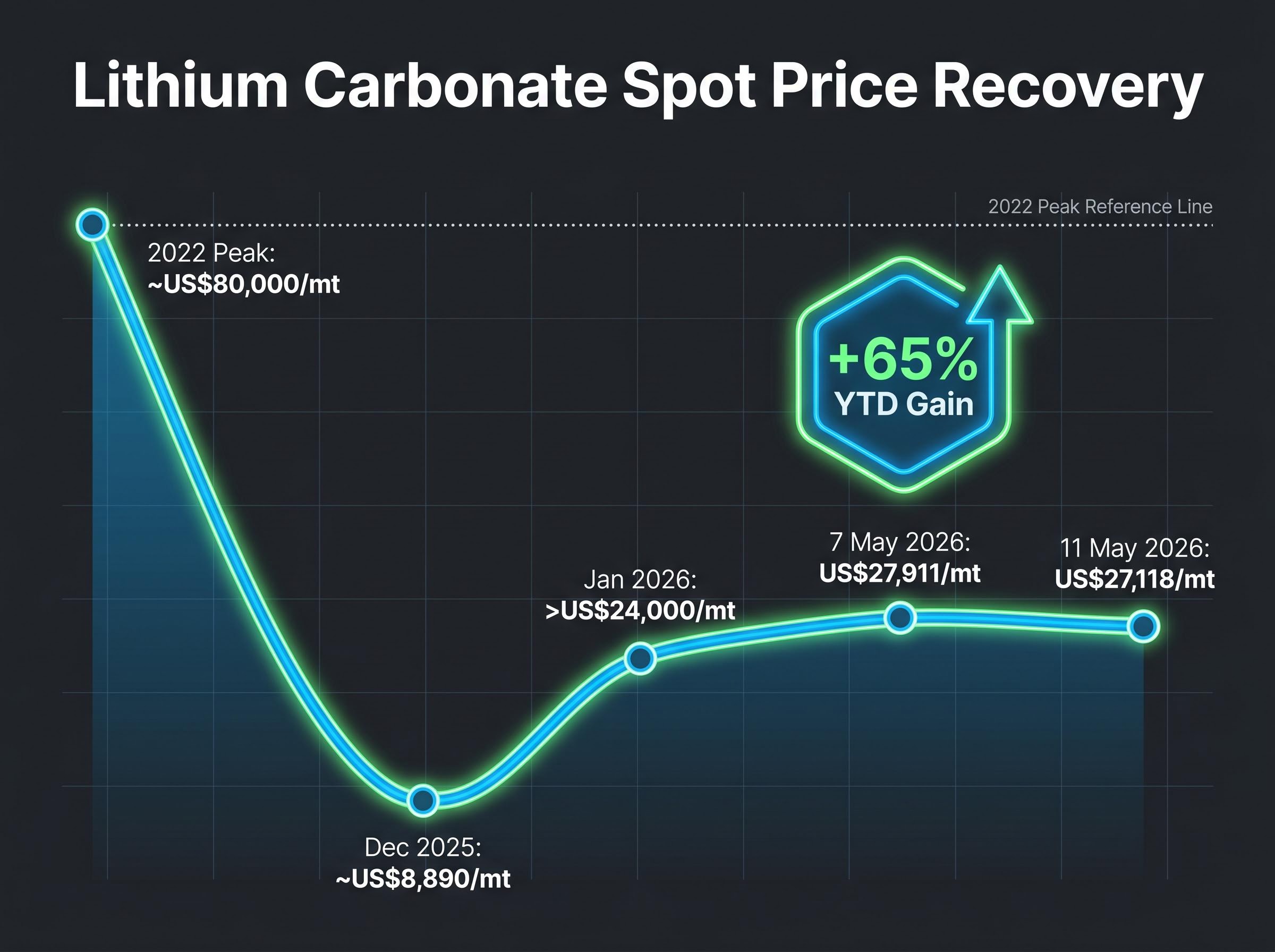

The speed of the lithium carbonate recovery has been the single largest driver of ASX lithium equity re-ratings in 2026. Spot prices have moved from approximately US$8,890/mt in December 2025 to above US$27,000/mt by early May 2026, a trajectory that has compressed roughly two years of expected recovery into five months.

Lithium carbonate spot prices gained approximately 65% year-to-date by 7 May 2026, recovering from US$8,890/mt in December to US$27,911/mt, the strongest reading since August 2023.

Key price milestones in the recovery:

The pullback from 7 May to 11 May is a reminder that near-term volatility persists within the broader uptrend. Current prices remain well below the 2022 peak of approximately US$80,000/mt, but the recovery has already been sufficient to re-rate equities. PLS gained approximately 47.1% year-to-date to $6.34 as of 7 May, directly tracking the commodity price recovery.

Investors wanting to go beyond the sector-level picture and assess individual stock positioning will find our dedicated guide to ASX lithium stock signals, which covers the technical momentum readings for PLS and LTR, the fragility profile of junior names like Core Lithium, and how the Global X Battery Tech and Lithium ETF provides an alternative exposure pathway for investors who want to avoid single-stock selection risk.

The investment case for lithium has traditionally rested on one pillar: electric vehicle battery demand. That thesis still holds, but two additional structural demand vectors are now contributing to the rally, broadening the base of the current cycle:

JPMorgan has projected that energy storage will represent approximately 30% of global lithium demand in 2026, driven by grid-scale battery installations and data centre backup power systems. The AI infrastructure buildout is accelerating this demand; as hyperscale data centres proliferate, their energy storage requirements are creating a second structural consumption channel for lithium carbonate that operates independently of automotive sales cycles.

Grid-scale battery deployment accelerated sharply in 2025 as renewables crossed 51% of electricity supply in Australia’s National Electricity Market for the first time, creating structural demand for lithium carbonate that operates on energy infrastructure procurement cycles rather than consumer product cycles.

The sentiment spillover is visible across the ASX. BrainChip, an ASX-listed neuromorphic chip company, has gained approximately 68% on AI-related demand, illustrating how AI capital expenditure flows are lifting adjacent sectors including critical materials.

Geopolitical tensions have elevated the strategic value of Australian critical minerals producers positioned outside Chinese processing capacity. Lynas Rare Earths has gained approximately 29%, reflecting how the market is pricing supply chain repositioning in real time. For lithium producers, the same dynamic applies: strategic buyers and government procurement programmes are increasingly favouring non-Chinese sources, creating a structural tailwind that is additive to commercial demand.

Two significant acquisitions in the lithium space, announced within days of each other, point to a pattern rather than coincidence. Strategic acquirers are paying acquisition premiums now, a signal that sophisticated capital believes the price recovery is durable enough to justify locking in assets at current valuations.

Critical minerals processing concentration, specifically China’s approximately 70% share of global lithium and rare earth processing capacity, creates a 2-4% annual return drag on Australian clean energy positions and explains why supply chain repositioning has become a strategic priority for both government procurement programmes and corporate acquirers.

Zhejiang Huayou Cobalt, a major Chinese cobalt and lithium chemicals group, agreed to acquire Atlantic Lithium for approximately $285 million (£155 million) around 8 May 2026. The deal followed Ghanaian parliamentary approval of the Ewoyaa mining lease in March 2026, which cleared the regulatory path. The project’s fundamentals had strengthened materially: lithium metal estimates were upgraded from 32,000 tonnes to 103,000 tonnes, and specific yield improved from 4.8% to 11.85%.

Separately, Critical Metals agreed to acquire European Lithium for approximately $835 million in late April 2026, with shareholders to receive 0.035 Critical Metals shares per European Lithium share. The transaction is expected to close in the second half of 2026.

| Target | Acquirer | Deal Value | Key Asset/Project | Announced |

|---|---|---|---|---|

| Atlantic Lithium | Zhejiang Huayou Cobalt | ~$285M (£155M) | Ewoyaa (Ghana) | ~8 May 2026 |

| European Lithium | Critical Metals | ~$835M | European lithium assets | Late April 2026 |

The Australian government’s $1.2 billion Critical Minerals Strategic Reserve, allocated in the 2025-26 federal budget, provides a macro backdrop that further supports deal activity by reducing sovereign risk for producers operating in Australia.

The recovery is real, but calibration matters. Current lithium carbonate prices of approximately US$27,000/mt sit roughly 66% below the 2022 cycle peak of approximately US$80,000/mt. The rally has been sharp from the trough, but the sector is recovering lost ground rather than charting new territory in commodity terms.

Lithium carbonate at approximately US$27,000/mt remains roughly 66% below the 2022 peak of US$80,000/mt, placing the recovery in the middle innings of the cycle rather than at the top.

In equity terms, however, several names have moved into price discovery. PLS closed approximately 16% above its own 2023 high as of 8 May 2026, a level where near-term volatility risk is elevated simply because there is no recent resistance to anchor expectations.

Three policy and macro tailwinds are supporting the rally beyond commodity fundamentals:

The Critical Minerals Strategic Reserve, established by the Australian government with a $1.2 billion allocation in the 2025-26 federal budget, is designed to secure domestic supply of lithium and other battery materials while strengthening Australia’s position in global supply chains against geopolitical disruption.

These frameworks reduce sovereign risk and improve the structural outlook for Australian producers, but they do not eliminate the near-term price volatility that comes with a commodity still repricing from multi-year lows.

Five new 52-week highs in materials against nine new lows in consumer discretionary, in the same week, is the kind of divergence that typically accompanies a sector rotation rather than a single-week anomaly.

The rally is supported by three reinforcing signals that rarely converge simultaneously: commodity price recovery (lithium carbonate up 65% year-to-date), strategic M&A activity (over $1.1 billion in lithium deals announced in the past fortnight), and government policy backing ($1.2 billion in federal budget allocation plus bilateral cooperation frameworks). Each signal alone would be noteworthy. Together, they form the strongest case for a sustained materials rotation in over two years.

Two near-term indicators are worth monitoring to assess whether the rotation has durability beyond this week:

The materials sector’s Week 20 performance is not proof that the rally continues indefinitely. Prices remain well below the 2022 peak, and near-term pullbacks are likely. What the data does confirm is that the three conditions most commonly associated with durable sector rotations, commodity strength, strategic capital deployment, and policy alignment, are all present at the same time.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

The rally is driven by a 65% year-to-date surge in lithium carbonate spot prices, growing demand from AI data centre energy storage, defence-related supply chain diversification away from Chinese processing, and over $1.1 billion in strategic M&A deals announced in May 2026.

Lithium carbonate spot prices recovered from approximately US$8,890 per tonne in December 2025 to US$27,911 per tonne by 7 May 2026, a gain of approximately 65% year-to-date and the strongest reading since August 2023.

The Critical Minerals Strategic Reserve is a $1.2 billion allocation in the 2025-26 federal budget designed to secure domestic supply of lithium and other battery materials while strengthening Australia's position in global supply chains against geopolitical disruption.

Pilbara Minerals (PLS), Liontown Resources (LTR), and Mineral Resources (MIN) all hit new 52-week highs, alongside Nickel Industries (NIC) and Rio Tinto (RIO), which reached an all-time high of $178.72.

JPMorgan has projected that energy storage will represent approximately 30% of global lithium demand in 2026, as grid-scale battery installations and data centre backup power systems for AI infrastructure create a second structural consumption channel independent of automotive sales cycles.