Barclays Warns of Prolonged Market Volatility Under New Fed Reality

18 hrs ago

Nine consumer discretionary stocks and five healthcare stocks hit fresh ASX 52-week lows in the week ending 8 May 2026, the worst combined sector reading in 12 months. The collapse was led by CSL, which shed 17% in a single session after a guidance downgrade wiped billions from its market capitalisation. The RBA’s cash rate hike to 4.35% in early May, arriving alongside collapsing consumer confidence and surging fuel costs, has compressed household spending capacity at the very moment several ASX 200 companies issued profit warnings. The result is a concentrated cluster of new annual lows that signals earnings risk is no longer theoretical for investors in these two sectors. What follows maps which stocks are now at 52-week lows, what corporate commentary reveals about the earnings outlook, what the macro drivers mean for rate-sensitive sectors, and what to watch ahead of the next RBA meeting on 4 June 2026.

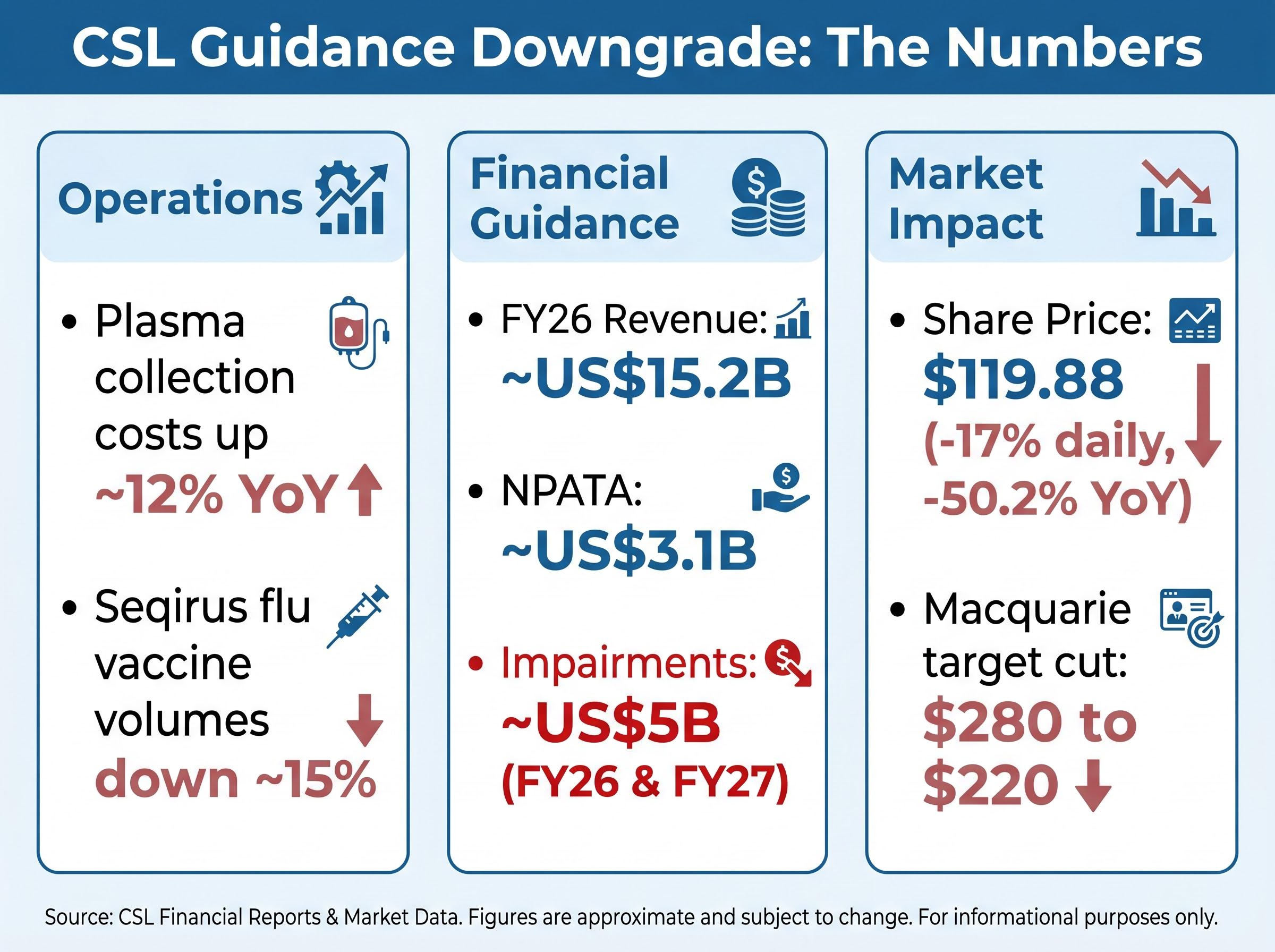

CSL fell 17% in a single session on the Monday of the reporting week, closing at $119.88 and confirming a 50.2% year-on-year decline. For Australia’s largest healthcare stock, the selloff was not a surprise event so much as a violent confirmation of what the sector’s 12-month decline had been pricing all along.

The guidance downgrade centred on three verified drivers:

FY26 revenue guidance was cut to approximately US$15.2 billion, with NPATA guidance reduced to approximately US$3.1 billion. CSL also flagged approximately US$5 billion in non-cash impairments across FY26 and FY27, a material disclosure that amplified the market reaction well beyond the revenue line.

Management framed the discrete revenue headwinds as timing and structural rather than demand destruction, and a transformation programme targeting savings by FY28 of $500-550 million in annualised benefits forms the cornerstone of the recovery thesis that some brokers are weighting against the current price.

Macquarie downgraded CSL to Neutral from Outperform, cutting its price target from $280 to $220, citing plasma cost inflation as structural rather than cyclical.

Citi maintained a hold position, noting that “demand softness signals peak cycle for CSL.” The average consensus price target fell to approximately $240, down roughly 15% post-downgrade. With the stock trading at $119.88, the gap between consensus and market price suggests either the street is slow to adjust or the market is pricing in a deeper earnings deterioration than brokers have modelled.

UBS had already downgraded the ASX healthcare sector to Sell on 4 May 2026, a call that CSL’s guidance cut validated within days.

CSL dominated the headlines, but four additional healthcare names hit independent 52-week lows in the same week, reinforcing that the sector’s approximately 40% index decline over 12 months reflects structural pressure spreading across every major ASX healthcare constituent.

| Stock | Ticker | Close Price (AUD) | Week Change (%) | Year-on-Year Change (%) |

|---|---|---|---|---|

| Ansell | ANN | $26.42 | +0.4% | -18.2% |

| Fisher and Paykel Healthcare | FPH | $29.00 | -2.1% | -12.4% |

| ResMed | RMD | $28.56 | -0.6% | -25.4% |

| Sonic Healthcare | SHL | $18.94 | -5.1% | -29.0% |

UBS downgraded Sonic Healthcare to Sell with a price target cut from $25 to $18, a level already breached by the week’s close. The downgrade cited end of post-COVID rerating and margin compression across pathology operations.

AustralianSuper reduced its healthcare sector weighting by approximately 20% (announced 8 May 2026), rotating toward consumer staples, a signal that institutional conviction in the sector’s near-term recovery is fading.

The simultaneous breach of 52-week lows across five healthcare names in a single week points to sector-wide repricing rather than isolated stock-specific problems.

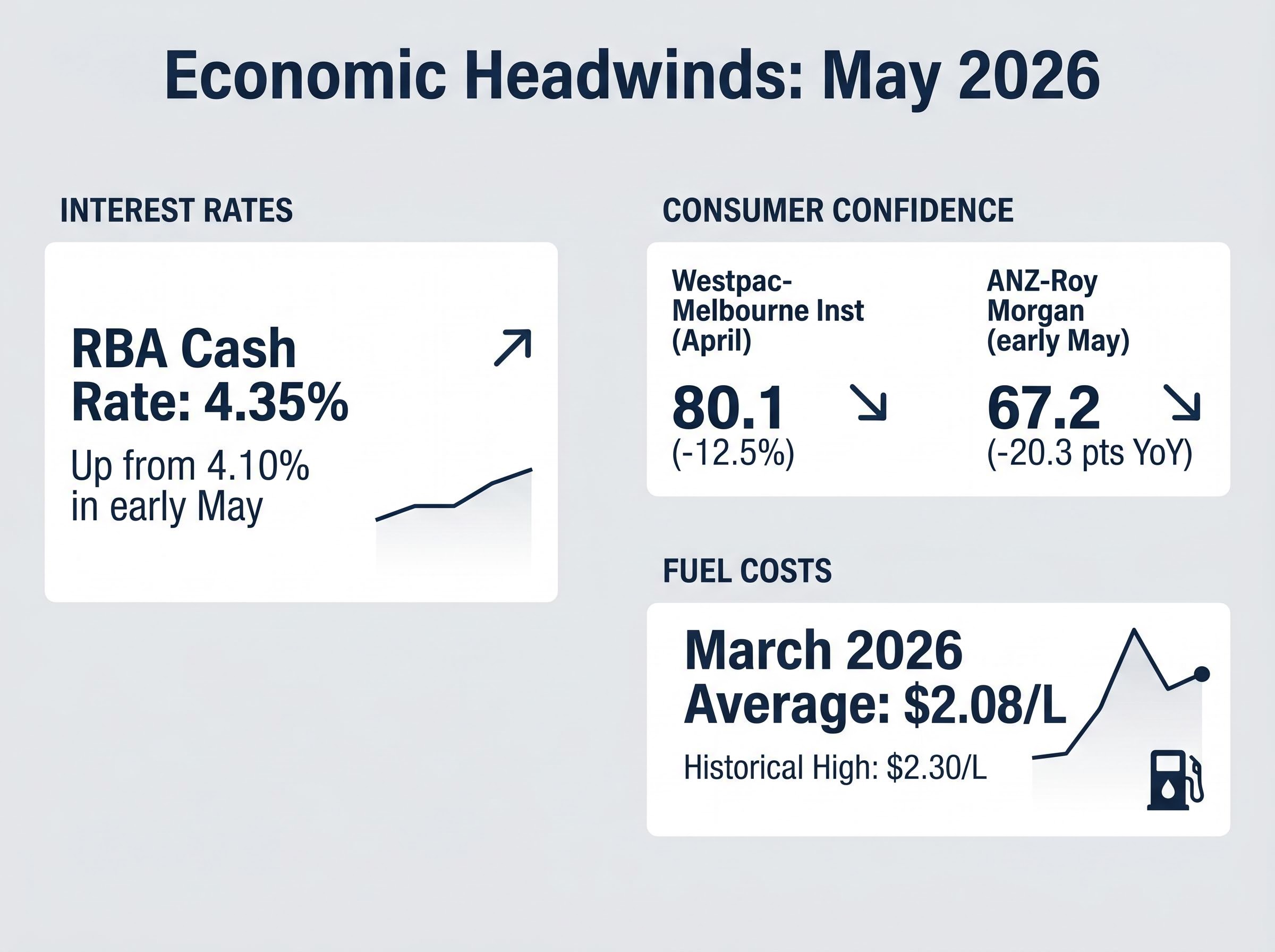

The RBA raised the cash rate to 4.35% in early May 2026, up from 4.10%. Governor Michele Bullock’s post-meeting communication was firmly data-dependent, citing persistent underlying inflation while acknowledging softening labour market signals. No unconditional pause was indicated. The next scheduled meeting is 4 June 2026.

The May decision was the third consecutive tightening move from a cash rate of 3.85% in January 2026, with eight of nine Board members voting for the increase and the single dissent indicating the threshold between hiking and holding is narrower than the headline margin implies.

The RBA’s May 2026 rate decision statement confirmed the 25 basis point increase to 4.35% while explicitly framing future moves as contingent on incoming data, a position that keeps the June meeting live and leaves rate-sensitive sectors exposed to further tightening if inflation persistence continues.

The transmission from a rate hike to corporate earnings runs through three channels:

Governor Bullock’s data-dependent forward guidance, with the next RBA meeting on 4 June 2026, means the rate path remains a live risk for the sectors covered in this article.

ASX 30-Day Interbank Cash Rate Futures (June contract at 95.63) implied approximately 17% probability of a further hike, roughly 8 basis points priced in for June. The market does not expect imminent relief, but it is not pricing in aggressive tightening either.

Consumer sentiment data confirms the damage is already registering. The Westpac-Melbourne Institute Consumer Sentiment Index recorded an April 2026 reading of 80.1, down 12.5% from March. The ANZ-Roy Morgan Consumer Confidence weekly reading came in at 67.2 for the week ending approximately 5 May 2026, down 20.3 points year-on-year. Both readings sit in territory historically associated with spending contraction.

Consumer confidence indices function as forward indicators for retail sales. The ANZ-Roy Morgan weekly measure tracks how households feel about their finances and the economy; when it drops below 80, spending intentions tend to contract. At 67.2, the reading is 20.3 points below the year-ago level, a decline associated historically with meaningful pullbacks in discretionary retail turnover.

Rising fuel costs compound the effect. The national average petrol price sat at approximately $2.08/L as at March 2026, with a historical high of approximately $2.30/L recorded that same month. For households already absorbing higher mortgage repayments, elevated fuel costs act as a secondary reduction to the budget available for discretionary purchases.

JPMorgan flagged 10-15% earnings risk for the consumer discretionary sector in a note dated 6 May 2026, citing the combined impact of rates and energy costs.

Corporate commentary arriving in the same week as 52-week lows confirms that earnings downgrades are driving the price action:

The pattern across all three is consistent: trading conditions deteriorated from late March into April, aligning precisely with the confidence data. This shifts the investment case from a valuation-driven dip to a fundamental earnings revision cycle.

Nine consumer discretionary stocks confirmed fresh 52-week lows as at 8 May 2026. Year-on-year declines ranged from 9.9% to 71.5%, with the deepest losses concentrated in names facing company-specific headwinds on top of the sector downturn.

| Stock | Ticker | Close Price (AUD) | Week Change (%) | Year-on-Year Change (%) |

|---|---|---|---|---|

| ARB Corporation | ARB | $18.66 | -0.2% | -43.6% |

| Flight Centre | FLT | $10.74 | +5.8% | -21.8% |

| Harvey Norman | HVN | $4.48 | -0.2% | -17.7% |

| IDP Education | IEL | $2.83 | -13.7% | -71.5% |

| Light and Wonder | LNW | $114.64 | 0.0% | -15.8% |

| Nick Scali | NCK | $14.64 | -1.7% | -22.5% |

| Super Retail Group | SUL | $11.60 | -3.8% | -18.9% |

| Temple and Webster | TPW | $5.93 | +7.0% | -69.2% |

| Wesfarmers | WES | $72.25 | -1.6% | -9.9% |

IDP Education’s 71.5% year-on-year decline and Temple and Webster’s 69.2% fall stand out as outliers, suggesting company-specific issues compounding the sector headwind.

JPMorgan initiated an Underweight on the consumer discretionary sector on 6 May 2026, flagging 10-15% earnings risk for retailers from the combined rate hike cycle and fuel price shock.

JPMorgan downgraded JB Hi-Fi to Neutral with a price target of $65 and Harvey Norman to Underweight with a price target of $3.80. Morningstar separately cut its Super Retail Group price target to $14 on 2 May 2026. The S&P/ASX 200 Consumer Discretionary Index is down approximately 16% year-to-date, its weakest level since May 2024.

The 52-week low list extended beyond healthcare and discretionary in the same week, signalling that macro pressure is not contained to the two headline sectors:

ASX market breadth had already deteriorated sharply in the prior week, with 22 index constituents hitting 52-week lows in the seven days ending 1 May 2026 even as the headline ASX 200 fell just 0.65%, revealing that the stress now visible across healthcare and consumer discretionary had been building beneath the surface for weeks.

ANZ-Roy Morgan Consumer Confidence has recorded 12 consecutive weeks of declines, with the latest reading at 67.2. Three forward-looking catalysts will determine whether current prices reflect fair value or incomplete repricing:

Investors in balanced or growth superannuation funds, or in ASX 200 ETFs, carry indirect exposure to every company named in this article.

Healthcare’s approximately 40% 12-month index decline culminated in CSL’s guidance downgrade, dragging five sector names to annual lows. Consumer discretionary’s 16% year-to-date fall, driven by the RBA hike to 4.35%, a confidence collapse, and confirmed trading deterioration at three companies, pushed nine more names to the same threshold.

The macro drivers covered in this article, rates, currency, and confidence, explain much of the sector’s underperformance, but US structural policy risk from FDA approval instability and declining vaccination rates under the current HHS policy direction represents a separate layer of pressure with no natural cyclical reversal point and may be incompletely priced across several of the names on this list.

The forward tension is whether current prices reflect fair value or whether incomplete earnings downgrades mean further downside remains. The 4 June RBA meeting is the near-term fulcrum. Investors should assess their sector exposure ahead of that decision and monitor May and June earnings updates from the companies named in this article for evidence of whether the repricing is done or still unfolding.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

—

A 52-week low is the lowest price at which a stock has traded over the past 12 months, and a cluster of new annual lows across multiple stocks in the same sector often signals broad earnings risk or a structural repricing event rather than isolated company problems.

Five ASX healthcare stocks confirmed 52-week lows in the week ending 8 May 2026: CSL (down 50.2% year-on-year), Ansell (down 18.2%), Fisher and Paykel Healthcare (down 12.4%), ResMed (down 25.4%), and Sonic Healthcare (down 29.0%).

Higher RBA cash rates increase mortgage repayments for variable-rate borrowers, reducing household disposable income and cutting spending on discretionary items like furniture, electronics, and travel, which directly compresses the revenue and margins of ASX-listed retailers and hospitality companies.

CSL fell 17% after issuing a guidance downgrade driven by currency headwinds, plasma collection costs rising approximately 12% year-on-year, and softer Seqirus influenza vaccine volumes, while also flagging approximately US$5 billion in non-cash impairments across FY26 and FY27.

Investors should monitor the RBA's 4 June 2026 decision for any further rate increase, trading updates from consumer discretionary and healthcare companies during May and June earnings season, and the ANZ-Roy Morgan Consumer Confidence reading, which has fallen for 12 consecutive weeks to a historically low 67.2.