SK Hynix’s $26.5B Nasdaq Listing Shatters ADR Demand Records

1 hr ago

Crude oil prices surged more than 3% during the Asian session on Sunday, 11 May 2026, after President Trump rejected Iran’s latest diplomatic proposal, unwinding a week of cautious optimism that a Gulf shipping deal was within reach. Brent crude climbed to approximately $105.67-$105.72 per barrel during European hours, while West Texas Intermediate (WTI) opened near $99.41-$99.48 on NYMEX. The move erased the prior week’s decline in a single session.

The Strait of Hormuz has remained largely closed since the onset of the conflict, and the collapse of this negotiating channel removes the nearest off-ramp the market had been pricing in. What follows covers the specific terms that divided Washington and Tehran, how major producers are responding, where analysts see prices heading from here, and whether the Trump-Xi summit scheduled for 14-15 May offers any realistic path to de-escalation.

The U.S. framework, as reported by the Wall Street Journal, demanded a multi-decade freeze on uranium enrichment, the removal of Iran’s highly enriched uranium stockpiles, and the elimination of critical nuclear infrastructure. In exchange, Washington offered phased sanctions relief and a cessation of military operations in the region.

The gap between those terms and what Tehran offered back was not a difference of degree. It was structural.

| Party | Core nuclear demand | Military/security demand | Economic demand |

|---|---|---|---|

| United States | Multi-decade enrichment freeze; removal of HEU stockpiles; elimination of nuclear infrastructure | Cessation of military operations (conditional) | Phased sanctions relief |

| Iran | Recognition of limited nuclear activities; partial HEU dilution; remainder transferred to third country | Full U.S. naval withdrawal from Hormuz area; security guarantees | Full and immediate sanctions removal |

Iran’s counteroffer, relayed through Pakistani intermediaries and reported by Axios (cited in WSJ, 11 May, 09:00 UTC), included an offer to dilute a portion of its highly enriched uranium and transfer the remainder to a third country. The mechanism itself represented an Iranian concession in form; no previous proposal had acknowledged a transfer of enriched material outside Iranian territory.

Trump characterised Tehran’s response as “wholly unacceptable.” Saudi Crown Prince Mohammed bin Salman described the rejection as “regrettable,” according to Reuters (11 May, 03:20 UTC). For traders, the distance between these two positions suggests that any future proposals will need to bridge a structural divide, not merely refine language.

The scale of Sunday’s reversal is easier to calibrate against the 7 May commodity repricing, when Brent dropped approximately 7.6% from $116.55 to $101.88 in a single session as peace framework reports removed a substantial share of the geopolitical war premium; Trump’s rejection of the Iranian counteroffer has now unwound the optimism that produced that sell-off.

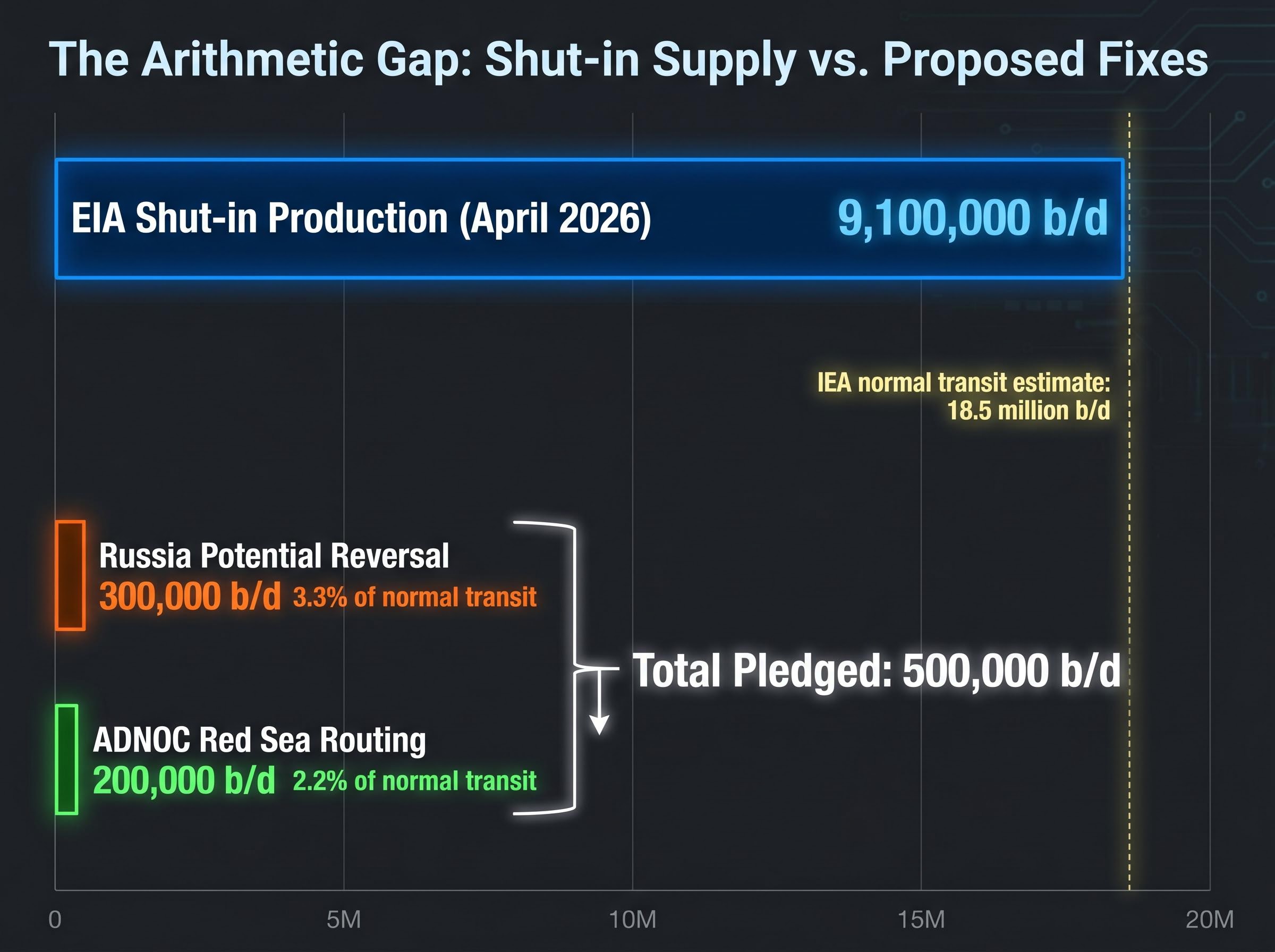

The physical scale of the disruption explains why the price surge is arithmetic, not sentiment. The International Energy Agency (IEA) estimates that 18.5 million barrels per day of seaborne trade normally transits the Strait of Hormuz. The U.S. Energy Information Administration (EIA) assessed production shut-ins at 9.1 million barrels per day as of April 2026.

Producers are attempting to route crude via Red Sea alternatives. ADNOC pledged an additional 200,000 barrels per day through those channels, according to the Financial Times (10 May, 23:50 UTC). That figure is less than 2.2% of the strait’s normal transit volume.

The downstream consequences are already visible at the pump:

JPMorgan warned that U.S. gasoline could reach approximately $5 per gallon as the Hormuz disruption continues to compress global supply, with no near-term resolution in sight.

The gap between what alternative routes can supply (hundreds of thousands of barrels per day) and what the strait normally moves (tens of millions) illustrates why price pressure is not easing regardless of producer goodwill signals.

The Strait of Hormuz is the narrow waterway between Iran and Oman through which a significant share of global seaborne oil and liquefied natural gas (LNG) flows. At its narrowest navigable point, the shipping channel is only a few kilometres wide, meaning it functions as a single chokepoint with no geographic alternative for tanker traffic exiting the Persian Gulf.

Alternative export routes exist. Overland pipelines and Red Sea rerouting can move some volume. But three factors prevent them from substituting at scale in the short term:

Even if political conditions shifted overnight, insurance market halts mean commercial shipping cannot immediately resume without a financial backstop. Goldman Sachs projected a minimum 4-6 week disruption if Iran maintains closure, citing ongoing naval patrols and the insurance freeze as twin constraints, according to Reuters (11 May, 06:30 UTC). Until insurers lift those halts, the physical reopening of the strait and its commercial reopening are two separate events.

The insurance withdrawal is not a secondary constraint on top of the naval standoff; it is the third pillar of what analysts have described as the Hormuz triple lock, combining US naval blockade operations, Iranian toll enforcement, and the near-total collapse of commercial war risk coverage into a single compounding mechanism that no single diplomatic gesture can undo.

Saudi Arabia’s energy minister warned against “panic” in energy markets on 11 May. Russia signalled a possible reversal of 300,000 b/d in voluntary production cuts, per Reuters (11 May, 08:15 UTC). An emergency OPEC+ call is scheduled for 12 May, according to the Wall Street Journal (11 May, 09:30 UTC).

The rhetoric suggests urgency. The arithmetic tells a different story.

| Producer/group | Action announced | Volume (b/d) | Shortfall context |

|---|---|---|---|

| ADNOC (UAE) | Red Sea alternative routing | 200,000 | 2.2% of normal strait transit |

| Russia | Potential voluntary cut reversal | 300,000 | 3.3% of normal strait transit |

| OPEC+ (collective) | Emergency call scheduled 12 May | TBD | No formal adjustments as of 11 May |

| Shut-in production | EIA assessment (April 2026) | 9,100,000 | Baseline disruption |

Combined, ADNOC and Russia’s pledges total 500,000 b/d against 9.1 million b/d in shut-in production. Meanwhile, Saudi Aramco raised Asian crude prices by $2 per barrel, per Bloomberg (11 May, 06:00 UTC), a move that signals pricing power rather than market stabilisation. The 12 May OPEC+ call will be closely watched, but the volume gap suggests it is unlikely to deliver material price relief.

Goldman Sachs has modelled the supply-demand imbalance as a shift from a 1.8 million barrels per day surplus in 2025 to a 9.6 million barrels per day deficit in Q2 2026, the sharpest institutional projection on record, and the 12 May EIA report represents the first scheduled opportunity for markets to reprice against updated official figures.

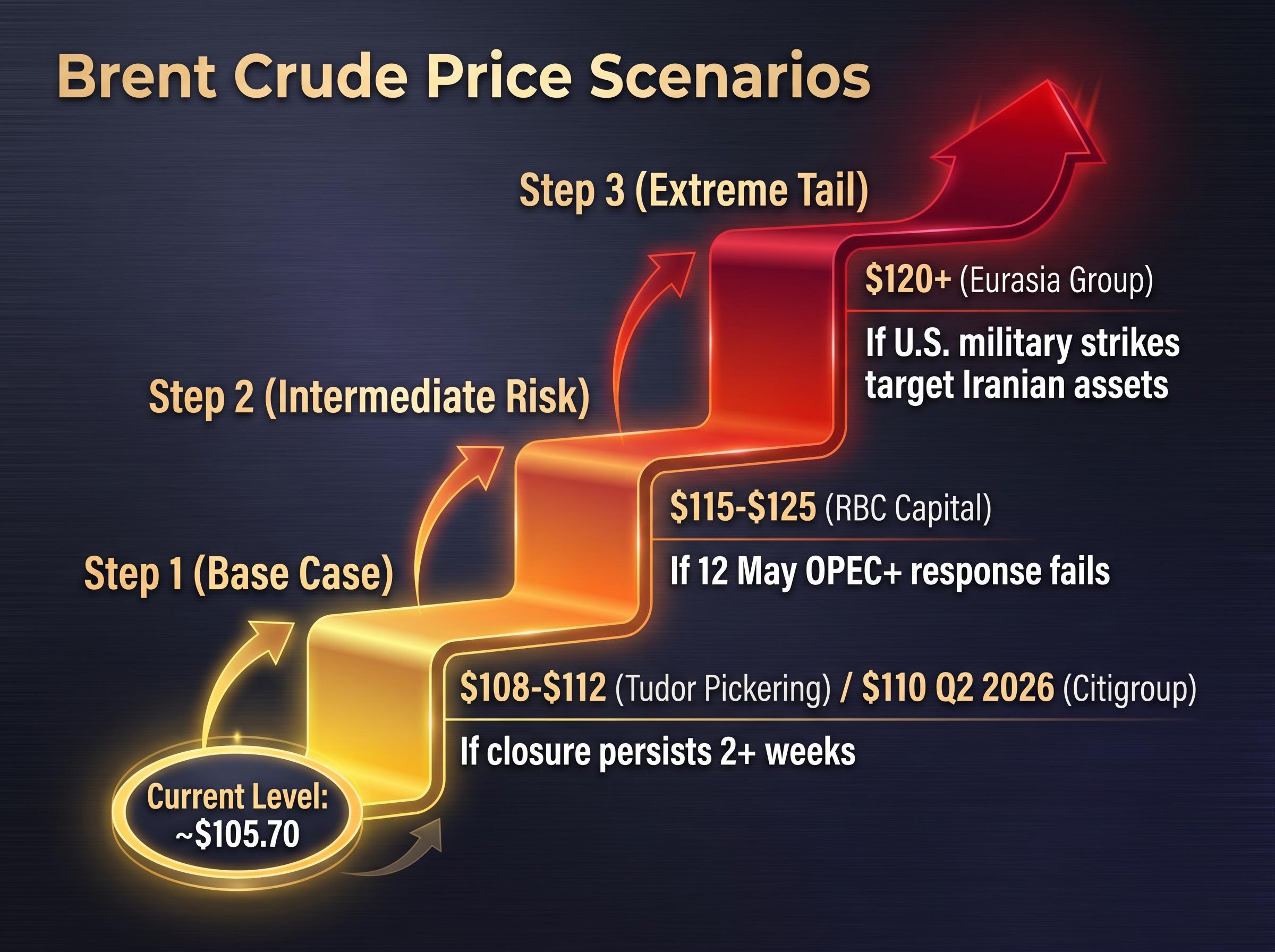

With Brent already trading near $105.70 per barrel, the market is partway up the first scenario tier. Analyst forecasts are not competing opinions; they are tiered outcomes tied to disruption duration and escalation risk.

Rystad Energy characterised the disruption risk as “indefinite” without Oman mediation, according to the Financial Times (11 May, 08:00 UTC), a stark counterpoint to the assumption that diplomatic momentum alone will cap prices.

The distance between current levels and the base-case ceiling is narrow. The distance between the base case and the extreme tail is wide, and dependent on decisions that could be made within days.

The Hormuz risk premium is not expected to decompress quickly even under a best-case diplomatic resolution: the IEA projects a two-year supply chain recovery timeline, and VLCC daily hire rates tracking approximately $110,000 per day signal that physical markets are pricing structural disruption rather than a temporary closure.

The Trump-Xi summit, rescheduled after a March postponement, is set for 14-15 May 2026 and remains on track. China’s substantial economic ties to Iran make Beijing a potential back-channel rather than a direct mediator, but the question is whether potential translates into action.

On 10 May, U.S. and Chinese officials held virtual talks in which Beijing urged de-escalation but offered no Iran-specific concessions, per the Financial Times (11 May, 04:15 UTC). Analysts have characterised the summit’s short-term oil market impact as neutral to bearish absent a breakthrough, though the fact the meeting is proceeding at all is modestly more constructive than a cancellation scenario.

Three factors will determine whether the summit moves the needle:

Brent at approximately $105 per barrel sits below even the base-case analyst consensus of $110 if the closure persists beyond two weeks. The market has repriced significantly, but if the diplomatic picture does not improve, further upside remains the path of least resistance.

Two variables will shape the next move. The 12 May OPEC+ emergency call is the nearest catalyst; a credible supply commitment above the current 500,000 b/d pledged would signal producer seriousness, while anything less confirms the arithmetic gap. The 14-15 May Beijing summit is the next diplomatic test, with any Iran-specific language in the communique carrying outsized significance.

Reuters noted “further gains on Hormuz risk premium” during the 11 May session. The signals to monitor in the coming days:

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. These forward-looking price projections are subject to market conditions and various risk factors, and past performance does not guarantee future results.

The Strait of Hormuz is a narrow waterway between Iran and Oman through which approximately 18.5 million barrels per day of seaborne oil and LNG normally flows. When it is closed, that volume cannot reach global markets, which directly drives crude oil prices higher.

Iran's counteroffer, relayed through Pakistani intermediaries, included only partial dilution of its highly enriched uranium and a transfer of the remainder to a third country, while demanding full and immediate sanctions removal and a U.S. naval withdrawal from the Hormuz area. Trump characterised the response as wholly unacceptable because it fell far short of the U.S. demand for a multi-decade enrichment freeze and elimination of nuclear infrastructure.

Analyst forecasts are tiered by escalation scenario: Tudor Pickering projects a base case of $108-$112 per barrel if the closure persists beyond two weeks, RBC Capital models $115-$125 if the OPEC+ response fails to close the supply gap, and Eurasia Group flags $120 or higher if U.S. military strikes target Iranian assets.

Combined pledges from ADNOC and Russia total only around 500,000 barrels per day, against an EIA-assessed shut-in of 9.1 million barrels per day, meaning producer commitments cover less than 6% of the disruption. Alternative pipeline and port infrastructure cannot scale to replace strait volumes in the short term.

Insurance syndicates have halted coverage for vessels transiting the Strait of Hormuz, meaning commercial shipping cannot resume even if political conditions shift overnight without a financial backstop. Goldman Sachs projects a minimum 4-6 week disruption, citing the insurance freeze alongside naval patrols as twin constraints that make the physical and commercial reopening of the strait two separate events.