At a trailing price-to-earnings (PE) ratio of 27.20x and a share price sitting around $72.66, Wesfarmers is priced for a future that has not yet fully arrived. Analysts are split on whether it ever will. With an FY26 consensus net profit forecast of approximately $2.8 billion, 17 analysts having trimmed their price targets to an average of $78.01 in April 2026, and the Covalent lithium project still mid-ramp, the question of whether Wesfarmers deserves its premium multiple is genuinely unresolved. Healthcare is growing fast. Retail is grinding. Lithium pricing has recovered sharply. The valuation case is live. This analysis breaks down how each of Wesfarmers’ four major growth pillars contributes to the earnings story, what the analyst target range of $66.63 to approximately $105 implies about market disagreement, and how investors should think about the risk-reward at current prices.

A $82 billion business on a 27x multiple: what the market is pricing in

The valuation arithmetic is specific, and it matters. At a closing price of $72.66 on 4 May 2026, Wesfarmers commands a market capitalisation of approximately $82.02 billion, a trailing PE of 27.20x, and a dividend yield of 2.93%. Those numbers price in an earnings trajectory that has not yet materialised in full.

| Metric | Value |

|---|---|

| Share price (4 May 2026) | $72.66 |

| Trailing PE | 27.20x |

| Market capitalisation | ~$82.02 billion |

| EPS (trailing) | ~$2.70 |

| Dividend yield | 2.93% |

| FY26 consensus net profit | ~$2.8 billion |

27.20x trailing earnings. At this multiple, the market is not paying for the current earnings run-rate. It is underwriting sustained acceleration across multiple divisions, and anything short of that creates de-rating risk.

The implied forward PE on a $2.8 billion profit forecast sits at roughly 29x against the current market cap. That is a multiple reserved for businesses delivering double-digit earnings growth with high confidence. For a conglomerate spanning hardware retail, discount fashion, healthcare distribution, and lithium mining, the confidence required is considerable.

The premium multiple problem becomes more intuitive when considered alongside a dividend discount model framework: at a 2.93% yield with mid-single-digit dividend growth assumptions from the retail core, the implied required return is well below the level that typically justifies a 27x earnings multiple, meaning the market is effectively valuing Wesfarmers on a growth stock basis despite the conglomerate structure.

When big ASX news breaks, our subscribers know first

Bunnings and Kmart: how much earnings weight two retail giants are carrying

The premium multiple discussion becomes more grounded when measured against the two businesses that generate the majority of group cash flow. Wesfarmers reported overall divisional earnings growth of 6.8% for the half-year to December 2025 (released 19 February 2026). That figure looks solid. It is also not the kind of number that justifies a 27x multiple on its own.

Bunnings: productivity gains in a soft home improvement market

Bunnings delivered solid earnings in a period where the broader home improvement market offered little volume tailwind. Weak housing turnover and cautious consumer spending defined the trading environment.

- Productivity initiatives drove earnings improvement rather than top-line growth

- Cost management offset the absence of volume-led revenue expansion

- The home improvement segment remains exposed to housing cycle timing

The result is a business holding earnings without accelerating them, a floor rather than a catalyst.

Kmart Group: margin discipline as the growth lever

Kmart Group’s contribution came through a different mechanism: margin expansion via pricing discipline and operational efficiency.

- Pricing strategy delivered margin improvement independent of volume growth

- Operational efficiency gains suggest structural rather than cyclical improvement

- Consumer discretionary macro pressures remain a near-term headwind

Together, these two divisions provide stability. Mid-single-digit earnings growth from the retail core sustains the business, but it does not pay for a 27x multiple. The premium must come from elsewhere.

What Wesfarmers’ healthcare numbers actually say about its transformation

The healthcare division has moved well past the diversification experiment stage. Half-year revenue to December 2025 reached $3.3 billion, up 8.4% year-on-year, according to PharmaDispatch reporting on 19 February 2026. The annualised run-rate now exceeds $6 billion.

The earnings figure is the one that demands attention.

35.7% half-year earnings growth on $3.3 billion in revenue. At this scale and growth rate, healthcare is no longer a peripheral division. It is the single largest contributor to the premium multiple argument.

Post-acquisition integration has stabilised, and the division is now contributing meaningfully to group earnings rather than diluting them. For investors building a sum-of-parts valuation, three implications stand out:

- Revenue scale: A $6 billion-plus annualised run-rate makes healthcare a material segment by any measure

- Growth momentum: 35.7% earnings growth is the only double-digit figure across any Wesfarmers division

- Integration completion: The drag from acquisition-related costs appears to have passed, allowing the underlying growth to show through

This is the division doing the most work to justify the premium. If healthcare earnings growth sustains at or near this level, the valuation argument strengthens considerably. If it decelerates toward single digits, the gap between the current multiple and the earnings it requires widens.

The 35.7% earnings growth figure sits in sharp contrast to what is happening across the broader ASX healthcare sector, which has fallen approximately 39% over 12 months to a six-year low as currency headwinds, rising rates, and FDA regulatory uncertainty have compressed multiples across the index. Wesfarmers’ healthcare division is growing through conditions that are destroying value elsewhere, which is precisely why the market is awarding it such a disproportionate share of the group’s premium multiple.

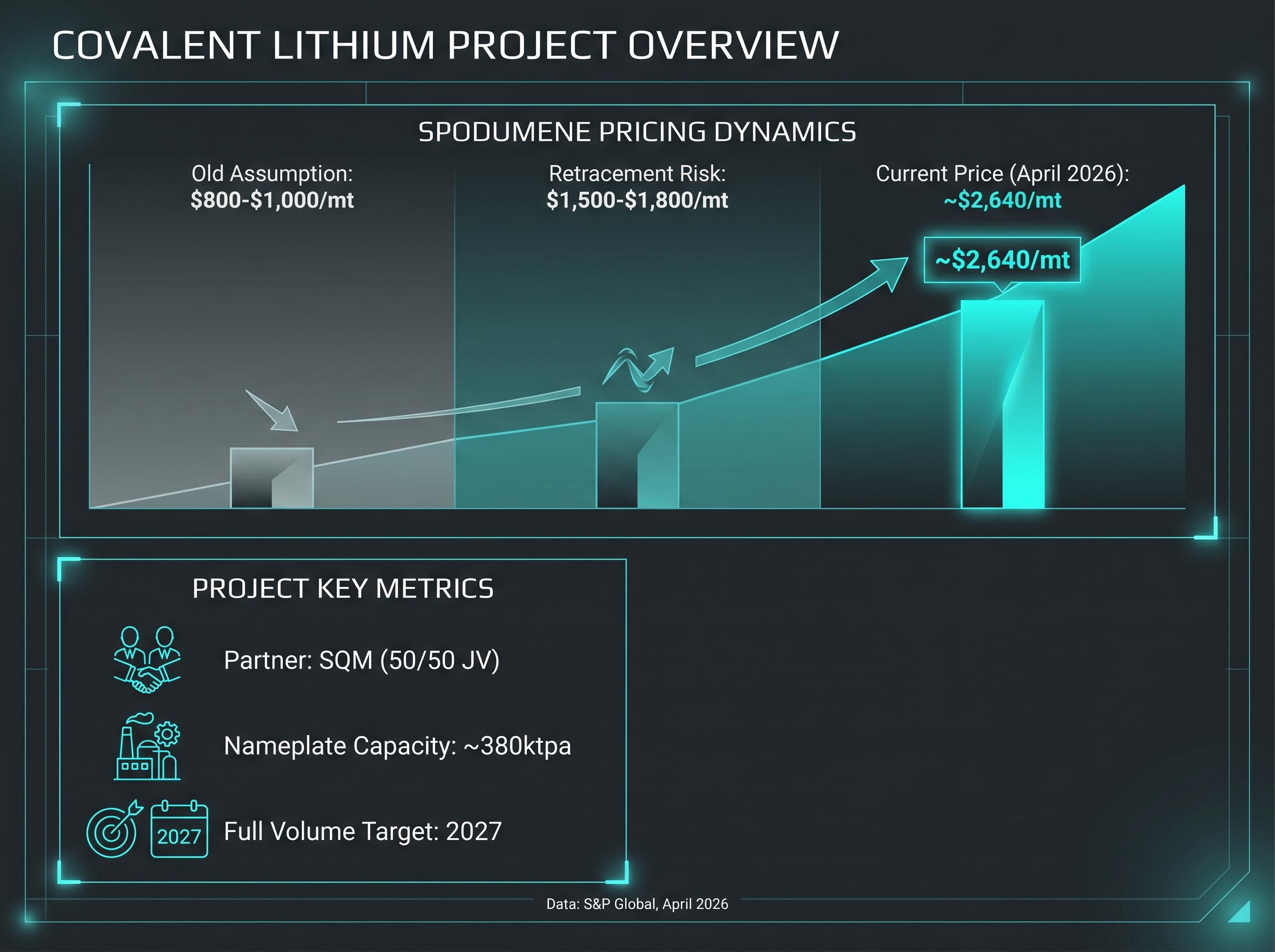

Covalent lithium: the speculative kicker, and why $2,640 per tonne changes the maths

Twelve months ago, the Covalent lithium project at Mt. Holland looked like an earnings drag. Spodumene prices had been depressed, and the ramp-up timeline carried uncertainty that weighed on sentiment.

The pricing environment has shifted materially. Spodumene concentrate (6%) prices reached approximately $2,640 per metric tonne as of April 2026, the highest level in two years according to S&P Global data published on 27 April 2026. At this price point, the project economics improve significantly compared to earlier assumptions that were built around $800-$1,000 per tonne pricing.

The spodumene price move does not exist in isolation; a broader lithium complex recovery has seen lithium carbonate rise approximately 197% from cycle lows to around US$26,800 per tonne as of early May 2026, with NdPr oxide up approximately 88% year-to-date, confirming that the pricing environment Covalent is now ramping into reflects a structural supply and demand rebalancing rather than a short-term speculative spike.

| Parameter | Detail |

|---|---|

| Nameplate capacity (100% basis) | ~380ktpa |

| Current spodumene price (April 2026) | ~$2,640/mt |

| Full volume timeline | 2027 |

| JV partner | SQM (50/50) |

| Wesfarmers’ economic share | 50% |

The transformation from earnings drag to potential contributor is real, but three execution risks remain:

- Ramp-up timing: Most spodumene volumes are expected to reach the market by 2027, and delays would push the earnings contribution further out

- Spodumene price sustainability: The $2,640/mt level reflects tight supply and demand growth; a retracement toward $1,500-$1,800/mt would materially reduce the earnings uplift

- JV complexity: The 50/50 structure with SQM means Wesfarmers captures only half the project economics, and joint venture coordination can introduce operational friction

Lithium is the highest-variance component of the investment case. At current pricing, it upgrades the outlook. At lower pricing, it reverts to a drag. Investors need to decide how much of this optionality the current share price already reflects.

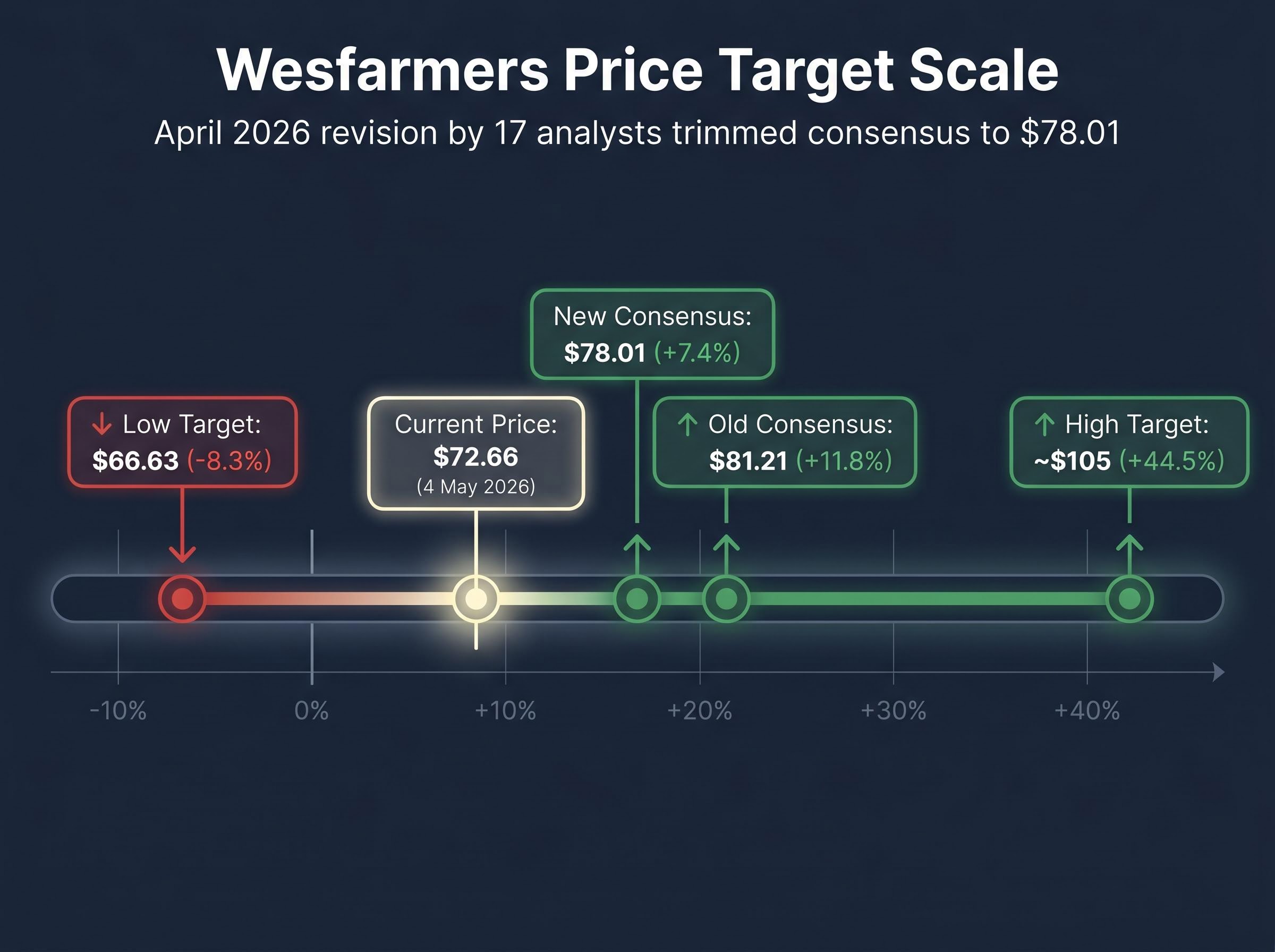

Reading the analyst target range: what $66 to $105 tells investors about uncertainty

The spread between the lowest and highest analyst price targets on Wesfarmers is nearly $40. That is not consensus. That is a map of disagreement.

| Target | Price | Implied move from $72.66 |

|---|---|---|

| Low | $66.63 | -8.3% |

| Consensus (pre-revision) | $81.21 | +11.8% |

| Consensus (post-revision, April 2026) | $78.01 | +7.4% |

| High | ~$105 | +44.5% |

April 2026 revision context: 17 analysts trimmed the consensus target from $81.21 to $78.01 as of 19 April 2026, reflecting softer revenue growth expectations and margin assumption downgrades.

The post-revision consensus of $78.01 implies approximately 7% upside from current levels. Alternative consensus sources sit lower still: TipRanks at approximately $77.33 and Investing.com at approximately $76.31. The consensus recommendation is Hold.

What separates the $66.63 bear case from the approximately $105 bull case is not a disagreement about Bunnings. It is a disagreement about healthcare growth durability, lithium ramp execution, and whether the multiple should expand or compress. The analyst at the low end is pricing in a retail earnings miss, lithium execution delay, or both. The analyst at the top is pricing in healthcare sustaining 30%-plus growth while lithium volumes arrive on schedule at elevated pricing.

One small data point for context: director B. English acquired 75 shares at $75.69 on 31 March 2026, a modest purchase via dividend reinvestment rather than a conviction-driven open-market buy.

The premium multiple problem: what has to go right for Wesfarmers to outperform from here

At 27.20x trailing earnings and roughly 29x forward on the $2.8 billion FY26 forecast, Wesfarmers is not priced for steady-state performance. It is priced for sustained double-digit group profit growth. The consensus Hold recommendation, with a target of $78.01 implying approximately 7% upside, reflects a market view that upside and downside are roughly balanced at current levels.

Bull case conditions for Wesfarmers to re-rate above consensus

Three segment-level outcomes would need to arrive in combination:

- Healthcare earnings growth sustains at or above 30%, extending the trajectory established in the first half of FY26

- Covalent lithium volumes reach the market by late 2027 at spodumene prices at or above $2,000/mt, delivering a meaningful earnings contribution to Wesfarmers’ 50% share

- Retail divisions hold mid-single-digit earnings growth, keeping the earnings floor intact while the growth segments do the re-rating work

Bear case triggers and multiple compression risk

Three risks would pressure both earnings and the multiple simultaneously:

- Retail earnings miss from consumer discretionary deterioration, which would remove the stability anchor that allows the market to pay a premium for the growth segments

- Spodumene price retracement below $1,500/mt, which would undermine the Covalent lithium earnings contribution story and revert the project to a drag

- Any group-level earnings disappointment, which at 27x trailing carries amplified downside because premium multiples compress faster than value multiples when expectations are missed

The amplified downside risk at a 27x multiple is partly a function of passive flow dynamics: with approximately A$200 billion in Australian ETF assets under management and pod shop gross leverage sitting at approximately 12x, blue-chip ASX stocks that miss earnings expectations now face de-rating velocity that is structurally faster than in the pre-2020 regime, as forced passive rebalancing and quant deleveraging can compound an initial fundamental miss into a significantly larger price adjustment.

The path to outperformance requires execution across all four divisions simultaneously. That is what the market is paying for at current prices.

Premium, fairly priced, or a value trap? The verdict on Wesfarmers at $72.66

At $72.66 against a consensus target of $78.01, the implied upside is approximately 7%. For a stock trading at 27x trailing earnings, that margin provides limited cushion against any divisional underperformance. The dividend yield of 2.93% offers a holding return floor, but it does not compensate for multiple compression risk on its own.

This is a story about timing and catalyst sequencing rather than a straightforward directional call. Three catalysts will determine which end of the $66-$105 range proves correct:

- FY26 full-year results as the base-case re-rating event, where divisional performance either confirms or undermines the forward earnings assumptions

- Covalent lithium volume delivery through 2027 as the bull-case accelerant

- Consumer discretionary conditions over the next two reporting periods as the bear-case trigger

The gap between $72.66 and the $78.01 consensus is approximately 7%. That is the market’s current assessment of the risk-reward: modest upside in the base case, meaningful upside if healthcare and lithium deliver simultaneously, and material downside if earnings disappoint at this multiple.

For Australian investors already holding Wesfarmers or weighing an entry, the investment case is intact but not urgent. The premium requires patience and execution across all four divisions to pay off. The next two reporting periods will determine whether that patience is rewarded.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.