How ASX’s CHESS Overhaul Became a $250M Governance Failure

2 hrs ago

Most Australians who own shares listed on the Australian Securities Exchange (ASX) have never seen the infrastructure executing their trades. They tap “buy,” the order disappears, and shares appear in their portfolio. What happens in between is an engineered system running at approximately 250 microseconds per trade, and most retail investors have never needed to think about it until something goes wrong. With average daily equity trading on the ASX reaching $7.524 billion as of April 2026, the exchange ranks among the most active in the Asia-Pacific. Yet for the retail investor placing a market order through a mobile broker app, the mechanics of auctions, order books, and settlement cycles remain largely invisible. This guide explains how the ASX works as a trading venue: when the market opens and what happens in those first seconds, how buy and sell orders find each other, what the bid-ask spread actually costs, and what occurs after a trade is struck.

The ASX’s official trading window runs from 10:00 AM to 4:00 PM AEST. That much is widely known. What most retail investors do not realise is that the 10:00 AM open is not a switch being flipped; it is the output of a pre-open auction that has been collecting orders for several minutes beforehand.

The trading day breaks into three distinct phases:

“The 10:00 AM open is not a switch. It is the output of an auction that has been collecting orders for several minutes and resolves at a randomised moment to prevent last-second manipulation.”

Retail investors who place market orders near the open or close face different execution dynamics than at mid-session. A market order submitted during the pre-open period may execute at a price that was not visible when the order was placed. Understanding this structure turns timing from an accident into a deliberate decision.

Consider a retail investor who opens a broker app at 10:15 AM and submits a buy order for 500 shares of an ASX-listed company. The order does not search the market for a willing seller. Instead, it enters a central limit order book (CLOB), a live ledger of every outstanding buy and sell order for that security, visible to market participants in real time.

The ASX Trade platform, built on NASDAQ OMX Genium INET technology, processes these orders at approximately 250 microseconds per trade. A separate platform, ASX Trade24, handles derivatives. When that buy order arrives, the system checks the order book for a matching sell order using a principle called price-time priority: the sell order offering the lowest price is matched first. If multiple sell orders sit at the same price, the one submitted earliest gets priority.

Price discovery mechanics operate continuously across every security on the exchange, with passive limit orders sitting in the book contributing to price formation even when they never execute — meaning the orders that never fill are doing as much work to set prices as the ones that do.

ASIC’s review of high-frequency trading and dark liquidity examined how speed-driven participants interact with the central limit order book, finding that price-time priority matching remains the foundational mechanism protecting retail order fairness even in markets where professional participants operate at microsecond speeds.

The investor’s buy order hits the book. If a matching sell order exists at an acceptable price, execution is immediate. If no match exists, the order sits on the book, waiting.

How the order behaves depends entirely on its type.

| Order Type | Execution Trigger | Risk to Buyer | Best Use Case |

|---|---|---|---|

| Market order | Executes immediately at best available price | Price is not guaranteed; may execute at a worse price in low-liquidity conditions | When speed of execution matters more than price precision |

| Limit order | Executes only at a specified price or better | May not execute at all if the market does not reach the limit price | When price control matters more than guaranteed execution |

| Stop-loss order | Triggers a market order once the price falls to a specified level | Once triggered, becomes a market order with the same price uncertainty | Protecting against downside beyond a pre-determined threshold |

A market order guarantees execution but not price. A limit order guarantees price but not execution. During the opening auction, market orders submitted in the pre-open session may execute at a price the investor cannot predict in advance, because the auction’s clearing price is determined by the full set of accumulated orders at the randomised resolution moment. Knowing this trade-off is the difference between deliberate order placement and accidental overpayment.

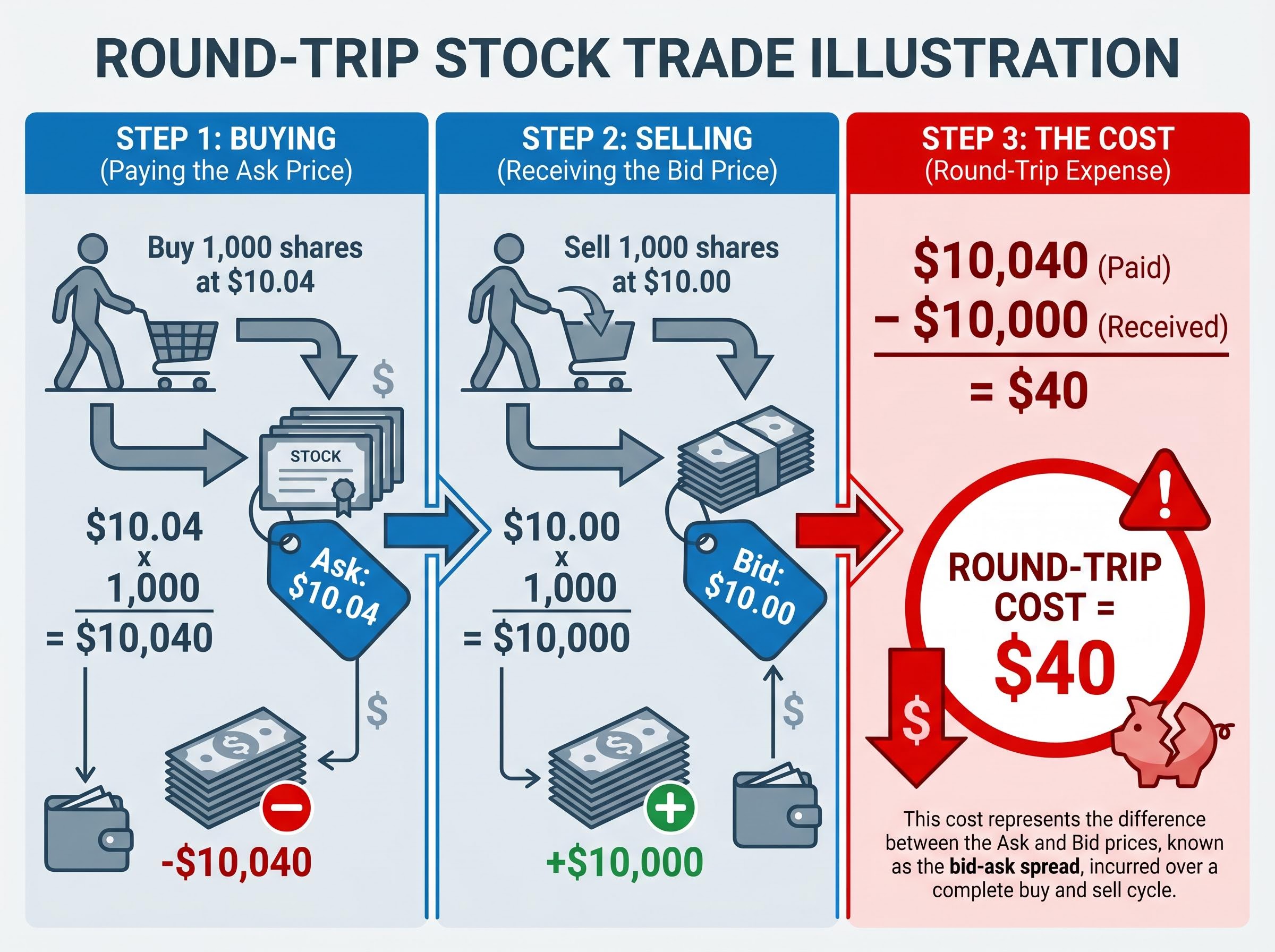

Every ASX-listed security has two prices at any given moment: the bid (the highest price a buyer is currently willing to pay) and the ask (the lowest price a seller is currently willing to accept). The gap between them is the bid-ask spread, and it functions as a cost that retail investors pay on every trade.

When an investor places a market buy order, they pay the ask price. When they sell, they receive the bid price. The spread is paid in both directions.

Worked example: A stock has a bid of $10.00 and an ask of $10.04. An investor buying 1,000 shares pays $10,040. If the bid-ask spread remains unchanged and the investor immediately sells, they receive $10,000. The round-trip cost is $40, separate from any brokerage commission charged by the broker.

On large-cap ASX 200 constituents, where daily volume is high and multiple participants are quoting prices, the spread tends to be tight, sometimes just a cent or two. On smaller-cap or lower-volume securities, the spread can widen substantially.

Three factors tend to widen a spread:

RBA research on order book liquidity and spread determinants published in 2025 confirms that the depth of bids and asks at each price level is the primary driver of how tightly a security’s spread is maintained, with thinner books producing wider spreads and greater price impact per trade.

Verified 2025-2026 benchmark spread data for ASX securities is not publicly available in current research. Readers seeking current figures can reference ASIC’s annual Market Conduct Report or broker liquidity reports for the most up-to-date benchmarks by security type.

For a retail investor trading frequently or dealing in smaller-cap stocks, the bid-ask spread can dwarf the explicit brokerage fee paid per trade. Recognising this cost is foundational to evaluating total transaction costs honestly.

ETF execution on the ASX introduces an additional spread dimension worth noting: units trade at prices that can sit at a premium or discount to the fund’s net asset value, meaning investors who ignore the iNAV during the opening or closing auction may pay more than the underlying basket of securities is worth.

The order book described above does not fill itself. Behind the visible flow of bids and asks are market makers: entities that continuously quote both a buy price and a sell price for a security, ensuring investors can transact without waiting for a natural counterparty to appear on the other side.

Market makers earn the spread as compensation for taking on inventory risk. They buy at the bid and sell at the ask, pocketing the difference, but they also bear the risk that the security’s value moves against them while they hold it. This incentive structure sustains liquidity across the exchange.

Not all ASX-listed securities have designated market makers. Investor appetite and institutional interest largely determine which stocks remain liquid. The ASX 200, a capitalisation-weighted index of the 200 largest eligible securities reviewed periodically, serves as a reasonable proxy: index membership strongly correlates with sustained liquidity, active market making, and tighter spreads.

The contrast matters for retail investors considering positions outside the large-cap universe:

Retail investors who venture beyond large-cap names into smaller or speculative ASX-listed stocks are implicitly accepting wider spreads and less reliable execution. That is a trade-off worth entering consciously rather than discovering after the fact.

When a buy order matches a sell order, a trade has been executed. But execution is an agreement, not a transfer. The shares and cash do not actually change hands at that moment. What follows is a two-stage process that turns the agreement into ownership.

| Stage | What Happens | Who Is Involved | When It Occurs |

|---|---|---|---|

| Trade Execution | Buyer and seller agree on price and quantity through the order book | Buyer, seller, ASX Trade platform | Immediately at the moment of the match |

| Clearing | Trade details are confirmed and reconciled between counterparties; obligations are calculated | ASX Clear (central counterparty) | After execution, before settlement |

| Settlement | Shares are transferred to the buyer; cash is transferred to the seller | ASX Settlement (via CHESS), buyer’s and seller’s brokers | T+2: two business days after the trade date |

The current settlement cycle is T+2, meaning a trade executed on Monday settles on Wednesday. Until settlement completes, the buyer does not legally own the shares and the seller does not have the cash.

The infrastructure underpinning this process is actively being modernised. The Clearing House Electronic Subregister System (CHESS) replacement project, which was re-designed after the original blockchain-based approach was abandoned in 2023, reached a significant milestone when Release 1 went live on 20 April 2026. The full CHESS replacement is targeted for approximately Q1 2029. A further shift to T+1 settlement (one business day) is not expected before approximately 2030, as it depends on the full CHESS replacement completing first. ASIC and the Reserve Bank of Australia share oversight responsibility for the settlement framework.

ASX’s confirmed staged CHESS replacement plan details a phased delivery structure in which settlement and sub-register functionality are addressed in successive releases, meaning the clearing and ownership record systems that directly affect retail investors will be modernised in steps rather than all at once.

For retail investors, the T+2 cycle has several practical implications:

The speed, transparency, and reliability described throughout this guide are not accidental. They are maintained by a layered regulatory structure designed to keep the market functioning fairly for all participants, including retail investors.

| Regulator | Primary Role | Key Tool or Mechanism |

|---|---|---|

| ASIC (Australian Securities and Investments Commission) | Market surveillance and compliance oversight | Continuous monitoring for anomalous trading activity; enforcement action against misconduct |

| Reserve Bank of Australia | Payment systems and settlement framework oversight | Oversight of systemically important clearing and settlement facilities |

| ASX Group (self-regulatory) | Exchange-level market stability | Circuit breakers designed to halt or slow trading in extreme volatility conditions, modelled on mechanisms similar to those used at NYSE Arca |

Circuit breakers act as structural safeguards. In periods of extreme volatility, trading in an individual security or across the broader market can be paused automatically, giving participants time to reassess rather than reacting in a disorderly cascade.

Alongside these trading-side mechanisms, ASX-listed companies are subject to continuous disclosure obligations that are considered more stringent than those in some comparable international markets. A listed company is required to release material information to the market immediately, ensuring that all investors, institutional and retail, trade on the same publicly available information. This obligation means that a company cannot tip off institutional investors before informing the broader market. Retail participants benefit directly from this requirement, receiving the same informational access to price-sensitive announcements as any other market participant.

Short sale reporting obligations sit alongside continuous disclosure as part of the same market integrity framework, with enforcement outcomes illustrating how data quality failures in ASIC’s surveillance systems can persist across large volumes of transactions before action is taken.

The system’s reliability is not a background assumption. It is actively maintained, monitored, and enforced by multiple regulators operating in parallel.

Retail investors do not need to operate the ASX’s infrastructure. But understanding how it functions changes how they use it. Timing orders relative to the auction structure, choosing between market and limit orders deliberately, accounting for the bid-ask spread as a real recurring cost, and respecting the T+2 settlement window are all practical decisions that become sharper once the system behind them is visible.

The infrastructure itself is improving. With CHESS Release 1 live as of 20 April 2026 and the full replacement targeted by approximately Q1 2029, the settlement backbone is being modernised for greater efficiency. A T+1 settlement pathway sits on the horizon for around 2030, shortening the gap between trade and ownership further.

Readers can review the official ASX trading hours and auction documentation at asx.com.au to confirm current session parameters. For the most current bid-ask spread benchmarks by security type, ASIC’s annual Market Conduct Report provides a useful reference.

For investors curious about what operates on the other side of the 250-microsecond matching window, our deep-dive into high frequency trading infrastructure examines how firms deploy co-located servers and custom execution platforms to extract returns from the same price-time priority rules that govern every retail order on the exchange.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The bid-ask spread is the gap between the highest price a buyer will pay (bid) and the lowest price a seller will accept (ask) for an ASX-listed security. Investors pay the ask when buying and receive the bid when selling, meaning the spread is a real recurring cost on every trade, separate from any brokerage commission.

The ASX continuous trading session runs from 10:10 AM to 4:00 PM AEST, but a pre-open auction collects orders from approximately 10:00 AM and resolves at a randomised moment within that window to produce the official opening price. This randomisation prevents participants from gaming the exact moment of the open.

ASX trades currently settle on a T+2 cycle, meaning a trade executed on Monday will settle on Wednesday. Until settlement completes, the buyer does not legally own the shares and the seller does not have access to the cash proceeds.

Price-time priority is the matching rule used by the ASX central limit order book, where sell orders offering the lowest price are matched first, and if multiple orders sit at the same price, the one submitted earliest gets priority. This rule protects retail order fairness even when professional participants operate at microsecond speeds.

CHESS is the Clearing House Electronic Subregister System that records share ownership and manages settlement on the ASX. The original blockchain-based replacement was abandoned in 2023, and a redesigned staged replacement had its Release 1 go live on 20 April 2026, with the full system targeted for approximately Q1 2029 and a T+1 settlement cycle expected around 2030.