Why a BoJ Rate Hike Hasn’t Stopped the Yen Carry Trade

1 hr ago

Australia’s exchange-traded fund market has crossed A$242 billion in funds under management, with over 375 products now listed on the ASX. Hundreds of thousands of retail investors have entered the market in recent years, drawn by the promise of low-cost, diversified investing in a single trade. Yet most beginner mistakes have nothing to do with picking the wrong fund. They stem from avoidable, repeatable errors in strategy, behaviour, and administration that compound quietly over time.

The gap between buying an ETF and investing in one well is wider than most new investors expect. New thematic launches arrive regularly, performance headlines create urgency, and the sheer product count can make simplicity feel inadequate. This guide identifies the most common mistakes Australian beginners make with ASX-listed ETFs, explains why each one damages long-term outcomes, and presents a practical framework for building a core portfolio from scratch, including specific ETF examples, fee benchmarks, and the tax realities that catch first-year investors off guard.

An ETF, or exchange-traded fund, is a basket of assets (shares, bonds, or commodities) that trades on the ASX like a single stock. Most ETFs track an index, such as the S&P/ASX 200, giving investors exposure to hundreds of companies in a single transaction. The buying process is straightforward.

A$242.52 billion in total funds under management as of March 2025, up 26.4% year-on-year, across 375 ASX-listed ETF products.

The BetaShares Australian ETF Review for March 2025 recorded A$3.43 billion in net inflows for the month and confirmed total market funds under management of A$242.52 billion across 375 listed products, figures that reflect how rapidly the local ETF market has scaled over the preceding 12 months.

The steps to purchase an ETF are simple:

The simplicity of execution is part of the problem. Buying an ETF takes five minutes. Building a portfolio that actually compounds over decades requires understanding the difference between a broad-market index ETF and a thematic ETF, and that distinction is the single most consequential product decision a beginner will make.

Every mistake below feels rational at the time. That is what makes each one persistent.

Concentration risk is the mechanism that makes ETF diversification valuable rather than just theoretically appealing: real 2025 examples show single-stock declines of up to 68.9% wiped out most of a concentrated investor’s capital, while the same decline in a 1% ETF holding produced only a 0.69% portfolio drag.

“A fund charging 0.7% versus one charging 0.2% may look identical in year one but can substantially erode returns when compounded across several decades.”

Fees are one of the few variables entirely within the investor’s control. Every basis point paid in management fees is a basis point that does not compound.

For readers wanting to move beyond comparing individual MERs and apply a structured framework across all 470 ASX-listed products, our dedicated guide to ETF fee screening walks through the Morningstar Price Score methodology and shows how a fee difference of less than 1% per annum can compound into a terminal wealth divergence of approximately $575,972 over a 30-year horizon.

Tax obligations on ETF holdings are not complicated, but they are commonly mishandled. There are three distinct obligations every ETF investor should understand before their first financial year ends:

ASIC flags cost base adjustments under the AMIT regime as commonly mishandled by retail investors.

Missing AMIT adjustments does not trigger an immediate penalty, but it creates compounding errors in cost base calculations that become increasingly difficult to unwind over multiple years. The ATO and ASIC Moneysmart both provide guidance on managing these obligations correctly.

ETFs can be held within self-managed superannuation funds (SMSFs) and increasingly within retail super platforms. The tax treatment changes significantly inside the superannuation environment, with concessional rates applying to both income and capital gains. Beginners with an SMSF, or those considering establishing one, should seek advice from a tax professional or financial adviser given the intersection of ATO superannuation rules and AMIT reporting obligations.

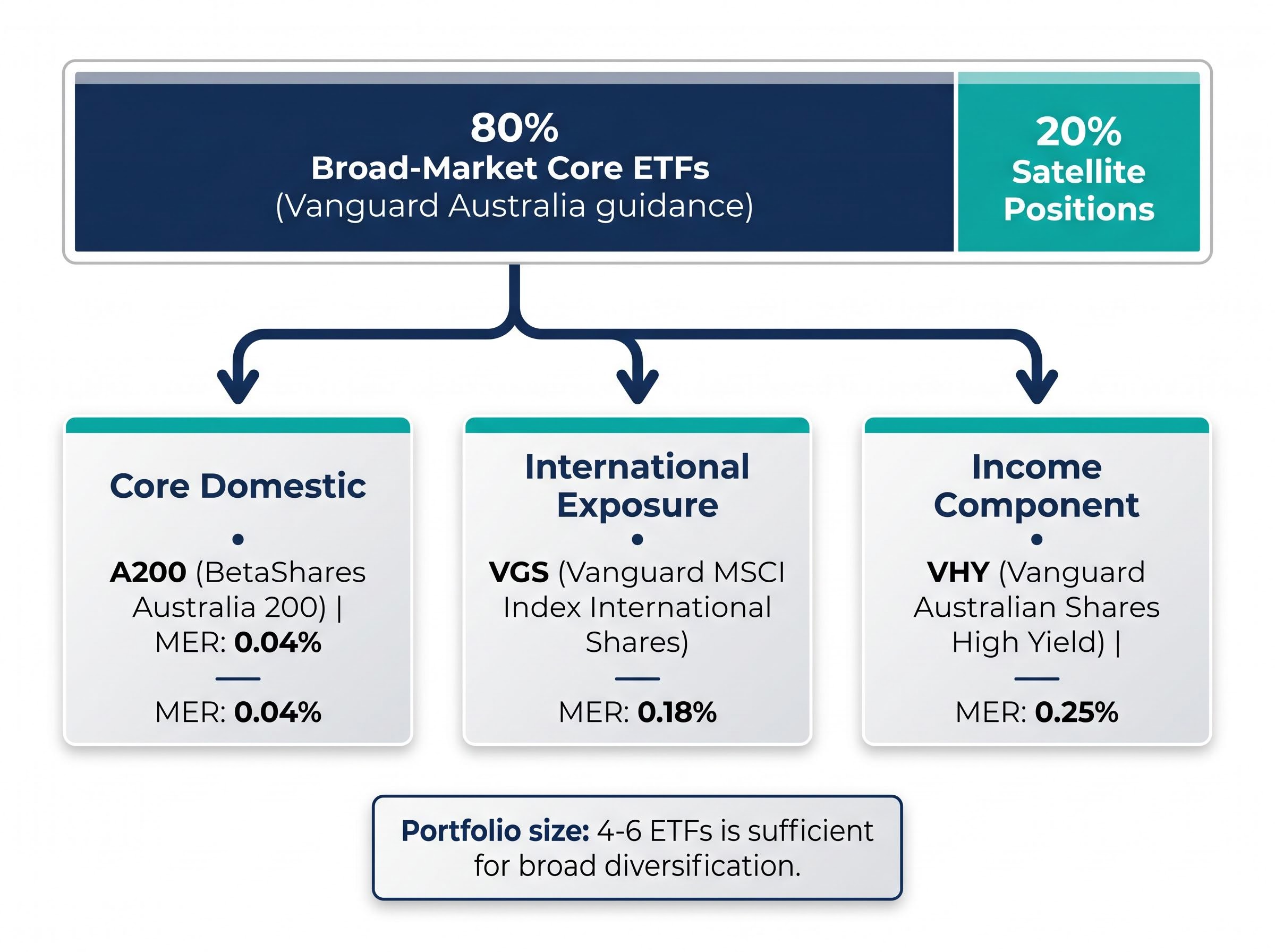

The core-satellite framework, consistent with Vanguard Australia’s guidance for most investors, allocates approximately 80% to broad-market core ETFs and up to 20% to satellite positions for specific exposures. For beginners, the core alone is a strong starting point.

Three ETF building blocks cover the primary bases:

International ETF demand among Australian retail investors crossed a structural threshold in Q1 2026 when international funds overtook domestic ETFs as the most purchased category on Selfwealth by Syfe, a shift driven partly by millennials allocating approximately 70% of their portfolios to ETFs with a tilt toward global developed-market exposure rather than ASX-heavy positions.

| ETF Ticker | Full Name | Market Exposure | MER (p.a.) | Primary Use Case |

|---|---|---|---|---|

| A200 | BetaShares Australia 200 | S&P/ASX 200 (domestic) | 0.04% | Core Australian equity exposure |

| VGS | Vanguard MSCI Index International Shares | Developed markets (global) | 0.18% | Core international equity exposure |

| VHY | Vanguard Australian Shares High Yield | High-dividend ASX shares | 0.25% | Income-focused distribution strategy |

A portfolio of 4-6 ETFs is sufficient for broad diversification. More than this typically adds complexity without adding meaningful risk reduction.

Dollar-cost averaging means investing a fixed dollar amount at regular intervals regardless of whether the market is up or down. The approach removes the timing question entirely. Beginners who wait for the “right moment” often miss prolonged periods of compounding that drive the majority of long-term returns.

Most major ASX brokerage platforms now support automatic recurring investment features, making a regular contribution schedule operationally simple to maintain. The discipline of contributing consistently matters more than the precision of any single entry point.

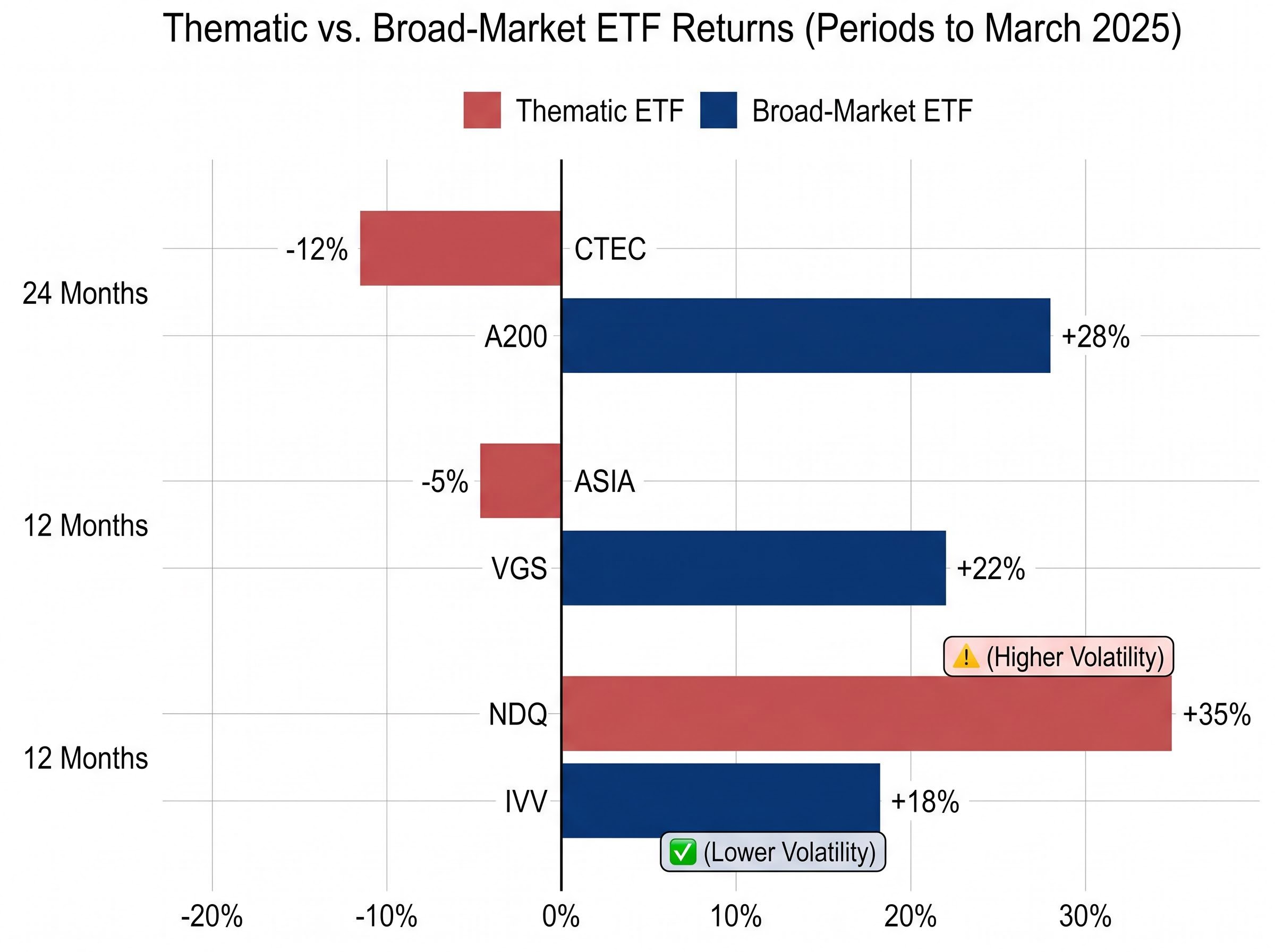

The following performance comparisons are directional, based on data for periods to March 2025. Figures should be verified against the latest Morningstar Australia ETF screener data or issuer fact sheets before making investment decisions.

| Comparison Pair | Thematic Return | Broad-Market Return | Period |

|---|---|---|---|

| CTEC vs. A200 | Approx. -12% | Approx. +28% | 24 months to March 2025 |

| URNM vs. VHY | Volatile (+15% / -22%) | Approx. +32% | 12-24 months to March 2025 |

| ASIA vs. VGS | Approx. -5% | Approx. +22% | 12 months to March 2025 |

| NDQ vs. IVV | Approx. +35% (higher volatility) | Approx. +18% (lower volatility) | 12 months to March 2025 |

NDQ outperformed IVV on a raw returns basis over that 12-month window. The outperformance came with significantly higher volatility and drawdown risk. A single strong year in US technology does not indicate suitability for a beginner core portfolio, particularly when the entry is FOMO-driven and the exit discipline is untested.

Thematic ETFs like NDQ or FANG hold heavy positions in a small number of large-cap US technology companies, creating single-theme exposure rather than genuine diversification. When the theme runs, returns look exceptional. When it reverses, drawdowns are sharp and concentrated.

The FOMO cycle reinforces the problem. Retail inflows into thematic ETFs tend to accelerate after peak performance runs, meaning many beginners buy high. Australian Financial Review commentary and adviser consensus suggest limiting thematic exposure to less than 10% of a total portfolio for most beginners.

For investors wanting to understand why fund-reported returns and actual investor-experienced returns diverge so sharply in thematic products, our deep-dive into the thematic ETF behaviour gap examines the ARK Innovation case study in detail, including Morningstar’s estimate that the fund destroyed approximately $13.4 billion in shareholder value over ten years despite reporting a +233% time-weighted return.

The product selection is the straightforward part. A two-to-four ETF portfolio of low-cost broad-market funds, built through regular contributions and reviewed annually, is not a beginner fallback. It is the structure recommended by ASIC, Vanguard Australia, Morningstar, and BetaShares for most investors.

The difficulty is sustaining it. Discipline breaks down at three specific moments:

Vanguard Australia’s guidance: “Annual rebalancing only; avoid reacting to short-term market narratives.”

Checking the INAV (Indicative Net Asset Value), which shows whether an ETF is trading at a premium or discount to its underlying holdings, before placing a trade is a simple habit that reduces spread costs. BetaShares guidance notes that bid-ask spreads at ASX open can reach 0.5% or more, reinforcing ASIC Moneysmart’s recommendation to use limit orders rather than market orders.

The ASIC Moneysmart ETF guidance for Australian retail investors covers limit order mechanics, bid-ask spread risks, and AMIT cost base obligations, making it a practical companion for anyone building their first ASX ETF portfolio.

The Australian ETF market offers genuine quality at remarkably low cost. The research-backed framework for beginners is simpler than the product count suggests: A200 for domestic exposure, VGS for international diversification, and optionally VHY for an income component. Three funds. Three tickers. Combined MERs below 0.25% on a weighted basis.

Before purchasing, verify each fund’s MER against the latest Product Disclosure Statement from the issuer. Open a brokerage account on a platform that supports limit orders. Commit to a regular contribution schedule before optimising anything else. The strategy only compounds if it is maintained through the periods when it does not feel like it is working.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

An ASX ETF (exchange-traded fund) is a basket of assets such as shares, bonds, or commodities that trades on the Australian Securities Exchange like a single stock. Most ETFs track an index, such as the S&P/ASX 200, giving investors exposure to hundreds of companies in a single transaction at low cost.

According to Morningstar Australia, a portfolio of 4-6 ETFs is typically sufficient for broad diversification. A simple starting point recommended by ASIC, Vanguard Australia, and BetaShares is a combination of A200 for domestic exposure, VGS for international diversification, and optionally VHY for income.

Australian ETF investors have three main tax obligations: income tax on distributions received, capital gains tax (CGT) on units sold at a profit (with a 50% CGT discount available for assets held longer than 12 months), and annual AMIT cost base adjustments required under the Attribution Managed Investment Trust regime even if no units were sold.

Dollar-cost averaging means investing a fixed dollar amount at regular intervals regardless of whether the market is up or down, removing the need to time the market. Most major ASX brokerage platforms now support automatic recurring investment features, making this approach straightforward for beginners to maintain consistently.

Thematic ETFs concentrate exposure in a small number of companies or sectors, meaning drawdowns are sharp and concentrated when the theme reverses. Retail inflows into thematic ETFs tend to accelerate after peak performance runs, so many beginners buy at or near peak valuations, with adviser consensus suggesting limiting thematic exposure to less than 10% of a total portfolio.