How to Value Transition-Stage Stocks Using Scenario Analysis

8 mins ago

At $428 per share, Tesla trades at roughly 200x forward earnings. A buyer at that price is not paying for the car company that exists today. They are paying for a version of Tesla that has not been built yet.

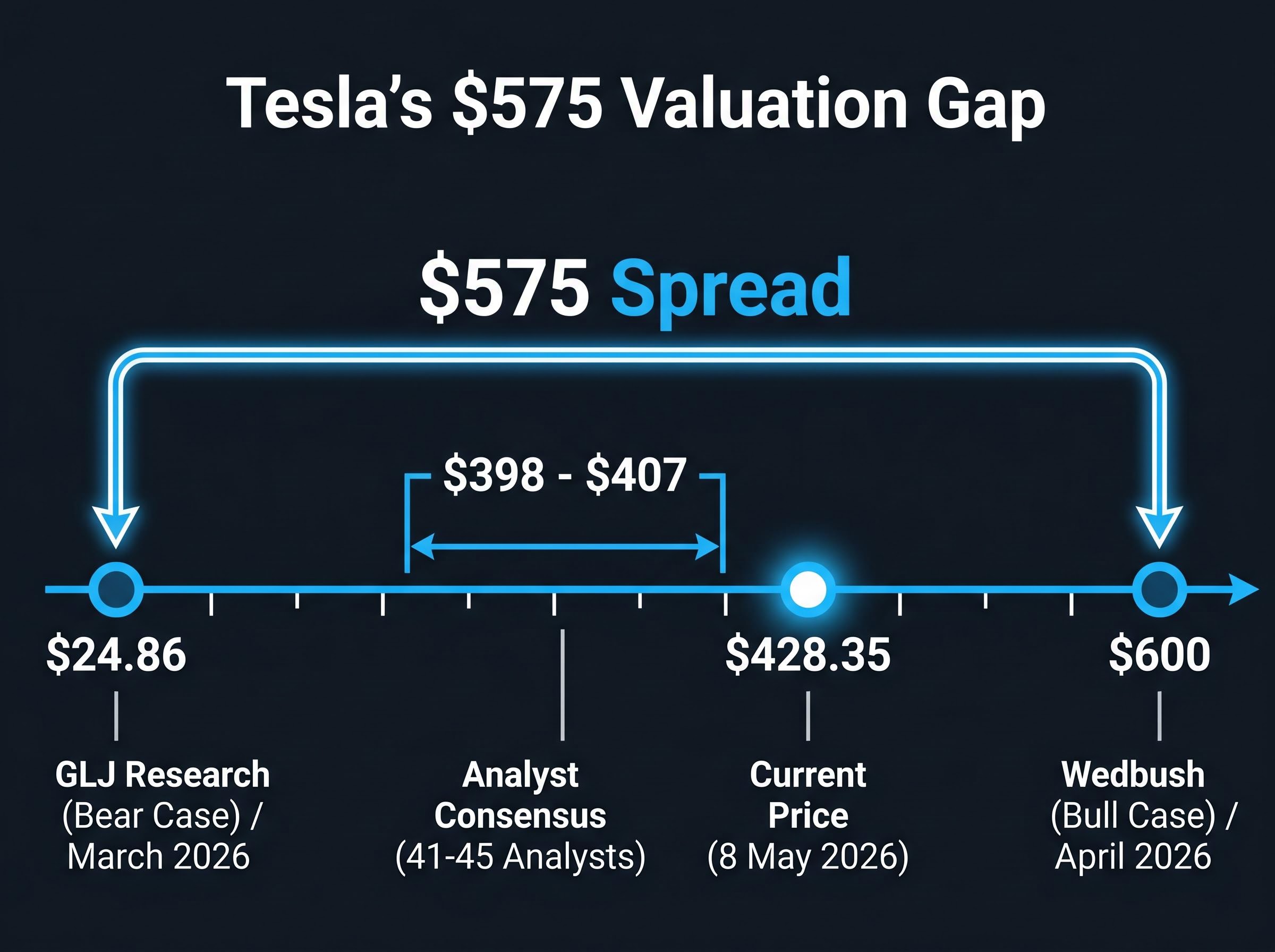

Tesla’s Q1 2026 earnings reignited the bull-and-bear debate that has defined the stock for years. With analyst price targets ranging from $24.86 (GLJ Research) to $600 (Wedbush), the spread tells investors something important: this is not primarily a disagreement about near-term financials. It is a disagreement about which company Tesla will become, and what that company is worth. That disagreement is itself a lesson in how to think about valuation when transformation is the thesis.

This article uses Tesla’s current valuation as a real-world case study for a methodology every investor needs: how to build bull and bear case scenarios, stress-test a stock price against them, and understand why the price paid at entry is often the most consequential variable in an investment outcome.

The gap between Tesla’s highest and lowest analyst price targets spans $575. That is not a rounding error or a difference of opinion on next quarter’s margins. It is one of the widest target spreads on record for a large-cap stock, and it reflects something more structural than disagreement about numbers.

The spread: GLJ Research’s Gordon Johnson holds a $24.86 target (Sell rating, March 2026). Wedbush’s Dan Ives holds a $600 target (Outperform, April 2026). Tesla closed at $428.35 on 8 May 2026.

The two camps are not arguing about the same company. They are applying entirely different valuation frameworks:

Tesla’s forward price-to-earnings ratio sits at approximately 191-217x, compared with 8-12x for peers like Ford and GM. That premium exists because the market is pricing a transformation thesis, not a quarterly earnings run rate.

The first lesson is direct: whenever a stock price embeds a transformation thesis, the investor must decide which scenario they are buying into before they buy. The price itself does not make that decision. The investor does.

A stock price is always a claim about the future. When two investors look at the same company and see radically different values, they are not disagreeing about today. They are disagreeing about which version of the future will materialise, and how much that version is worth in present terms.

For transition-stage companies, a single discounted cash flow model often produces misleading precision. The discount rate and the terminal multiple both shift depending on which business the company becomes. Scenario-based analysis addresses this by defining multiple possible futures and evaluating the stock against each.

Three inputs drive any scenario-based valuation:

These three variables compound across a multi-year horizon. Small changes in each input produce dramatically different terminal values, which is precisely why the bull-bear spread on Tesla is so wide.

The table below contrasts the assumptions underlying Tesla’s bull and bear scenarios:

| Scenario | Revenue Growth Range | Net Margin Range | Valuation Multiple Range |

|---|---|---|---|

| Bull Case | 20-35% (midpoint 27%) | 20-30% | 25-35x |

| Bear Case | 6-12% (midpoint 9%) | 8-14% | 18-22x |

Under the bear case, even at an entry price of approximately $375 per share, all projected return outcomes are negative. Under the bull case, projected annualised returns range from approximately 11-35% over a ten-year horizon, but analysts assign only a 5-10% probability to the bull case fully materialising. Tesla’s five-year average trailing P/E of approximately 150x and current EV/EBITDA of approximately 120x sit far above both auto and tech peer averages, illustrating how much transformation premium is already embedded.

The bear case does not assume Tesla fails entirely. It assumes Tesla succeeds as a car company but never becomes an AI platform. That distinction matters enormously.

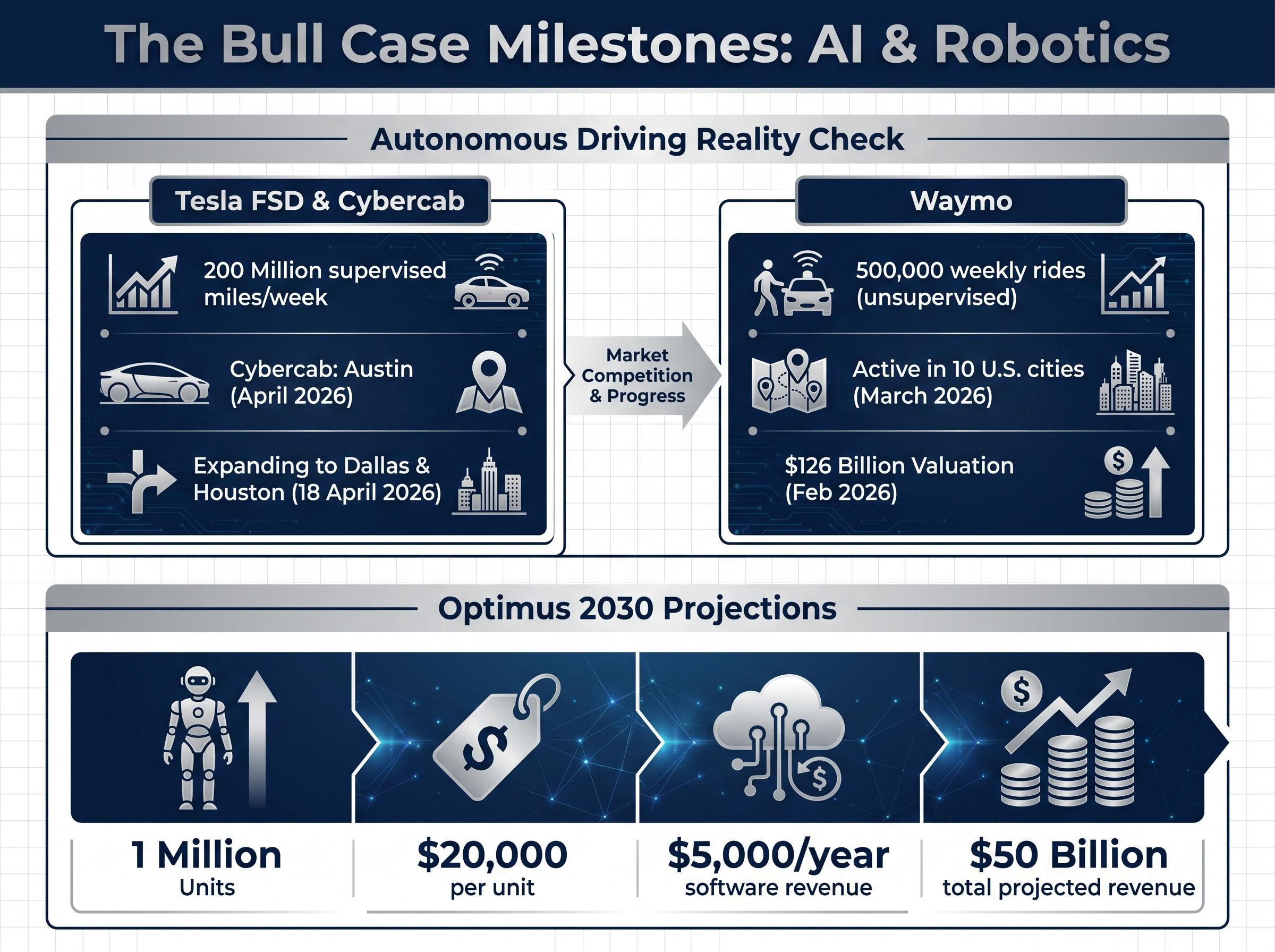

Wedbush’s $600 target rests on three specific pillars, each of which must materialise for the number to hold. Treating the bull case as a checklist of required conditions, rather than a sentiment position, is how investors evaluate its plausibility.

Wedbush’s Dan Ives has described Tesla as an “AI pure-play disguised as automaker,” targeting 40x on non-auto revenue. That framing encodes a specific valuation assumption: the automotive business is a shell, and the real value sits in software and services that do not yet generate meaningful revenue.

The National Highway Traffic Safety Administration (NHTSA) has an open probe into FSD v12 phantom braking behaviour, which could delay broader unsupervised deployment approvals. In California, Tesla had not filed the necessary permits for commercial autonomous vehicle operations as of the reporting period. Analysts broadly estimate Waymo holds a 12-18 month commercial lead over Tesla, and Waymo’s $126 billion valuation in its February 2026 financing round suggests the market already prices a credible rival.

There is also a pattern to consider. Elon Musk announced Optimus would be deployment-ready by 2022 (the announcement came in 2021) and projected one million robo-taxis by 2020 (announced in 2019). Neither timeline held. Past performance on announced timelines does not guarantee future delays, but it does inform how investors might probability-weight management projections.

The bear case is not a prediction of Tesla’s collapse. It is the scenario where Tesla succeeds as an electric vehicle manufacturer but fails to generate meaningful AI or robotics revenue. Under that scenario, applying auto-sector multiples to current earnings produces a price target far below the market price.

GLJ Research’s Gordon Johnson holds a $24.86 target. JPMorgan applies an auto-style multiple and has cautioned that “AI hype masks modest underlying growth.” The bear case multiple of 18-22x earnings contrasts sharply with Tesla’s current forward P/E of 191-217x.

Tesla’s Q1 2026 financials illustrate why the bear case is not unreasonable:

Three structural pressures weigh on the automotive segment:

Under bear case assumptions, at an entry price of approximately $375 per share, every projected return outcome was negative. A strong operating business and a good investment are not the same thing when the entry price already reflects a much larger business than the one that currently exists.

Consider two investors who hold identical views on Tesla’s long-term business potential. One bought shares at approximately $100 a few years prior to this analysis. The other buys at $428 today. Even if the underlying business performs identically for both, their return outcomes diverge dramatically.

The investor who entered at $100 has already absorbed more than 300% in gains. A reversion to bear-case fair value would still leave that investor with a positive return. The investor who enters at $428, near the stock’s all-time high of approximately $450, faces a different proposition entirely: the transformation premium is already in the price, and any scenario short of the full bull case may produce negative returns.

| Entry Price | Implied Outcome Under Bear Case |

|---|---|

| ~$100 | Positive annualised return even under bear assumptions |

| ~$428 | Negative projected returns under bear assumptions |

Forward analyst EPS estimates project earnings growing more than 5x from current levels, but that growth trajectory is already embedded in the current multiple. Analyst EPS estimates for Tesla declined more than 90% from their peak before recovering, a reminder that forward projections carry their own uncertainty.

Scenario-based valuation is most useful not for picking a target price but for establishing the entry price at which each scenario offers an acceptable return. A practical three-step process:

Tesla’s valuation debate is specific to one company, but the methodology it illustrates applies wherever a stock price embeds a future that has not arrived yet. The transferable framework has four steps:

The bull case for Tesla is assigned a 5-10% probability of full materialisation. That means a rational buyer needs very high bull-case returns to produce an acceptable probability-weighted expected return. When the best outcome is both spectacular and unlikely, the maths demands that the entry price compensate for the low odds.

The consensus analyst average target sits at approximately $398-$407 across 41-45 analysts, suggesting the current price of $428.35 is marginally above consensus. Approximately 46% of analysts (roughly 19 of 41) hold Buy ratings, indicating more mixed conviction than a casual reading of the stock price might suggest.

The $575 spread between Wedbush’s $600 and GLJ’s $24.86 is not a failure of analysis. It is the concrete embodiment of scenario divergence, and it exists in some form for every company whose stock price prices in a transformation.

Tesla is simultaneously a growing business and a high-risk investment at current prices. The gap between those two judgments comes entirely from entry price and scenario probability.

The three-variable framework (growth rate, net margin, exit multiple) demonstrated through this case study applies to any transition-stage company. Before consulting analyst targets or headlines, investors can define their own scenarios, attach numerical assumptions, and calculate what each scenario implies at the current price. That exercise, more than any single price target, clarifies what an investor is actually betting on.

Tesla may prove the bulls right. The robo-taxi network could scale, Optimus could generate tens of billions in revenue, and FSD margins could reach software-level profitability. But an investor buying at $428 in May 2026 is not merely betting on Tesla’s potential. They are betting on a specific combination of outcomes, at specific probabilities, at a price that leaves little room for the thesis to arrive late.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Scenario-based stock valuation analysis defines multiple possible futures for a company, typically a bull case and a bear case, and calculates projected investment returns under each using three key inputs: revenue growth rate, net profit margin, and exit valuation multiple.

Tesla's forward P/E of approximately 191-217x compared to 8-12x for Ford and GM reflects a transformation premium: the market is pricing in the possibility that Tesla becomes an AI and robotics platform rather than a traditional automaker.

A practical approach is to define specific bull and bear scenarios with numerical assumptions for growth, margin, and valuation multiple, then calculate projected returns at the current share price to identify the entry point where the most probable scenario delivers an acceptable annualised return.

The three core variables are revenue growth rate, net profit margin, and exit multiple; small changes in each compound across a multi-year projection horizon, which is why bull and bear price targets for transformation-stage companies can diverge by hundreds of dollars.

Two investors with identical views on a company's long-term potential can experience dramatically different outcomes if they paid different prices; an investor who enters near an all-time high already has the transformation premium embedded in their cost basis, meaning any scenario short of the full bull case may produce negative returns.