When in1Bank’s banking licence was formally cancelled on 4 May 2026, no Australian depositor lost a cent. That outcome was not luck. It was the Australian prudential framework working precisely as designed.

The revocation of in1Bank’s authorised deposit-taking institution (ADI) licence by the Australian Prudential Regulation Authority (APRA) marks the end of a structured four-month wind-down that began with a voluntary exit announcement in January 2026. For most Australians, the event passed without incident. But the mechanics behind that quiet exit reveal how Australia regulates the institutions licensed to hold public deposits.

This article explains what an ADI licence is, how APRA grants and revokes one, and what the in1Bank process tells depositors about the protections that exist when a bank leaves the industry. Readers will finish with a clear understanding of how the Banking Act 1959 framework operates in practice, and what the Financial Claims Scheme (FCS) actually does.

What happened to in1Bank and why its licence was cancelled

The revocation on 4 May 2026 was not a sudden regulatory intervention. It was the final, predictable step in a sequence that in1Bank itself initiated four months earlier. The timeline unfolded in five stages:

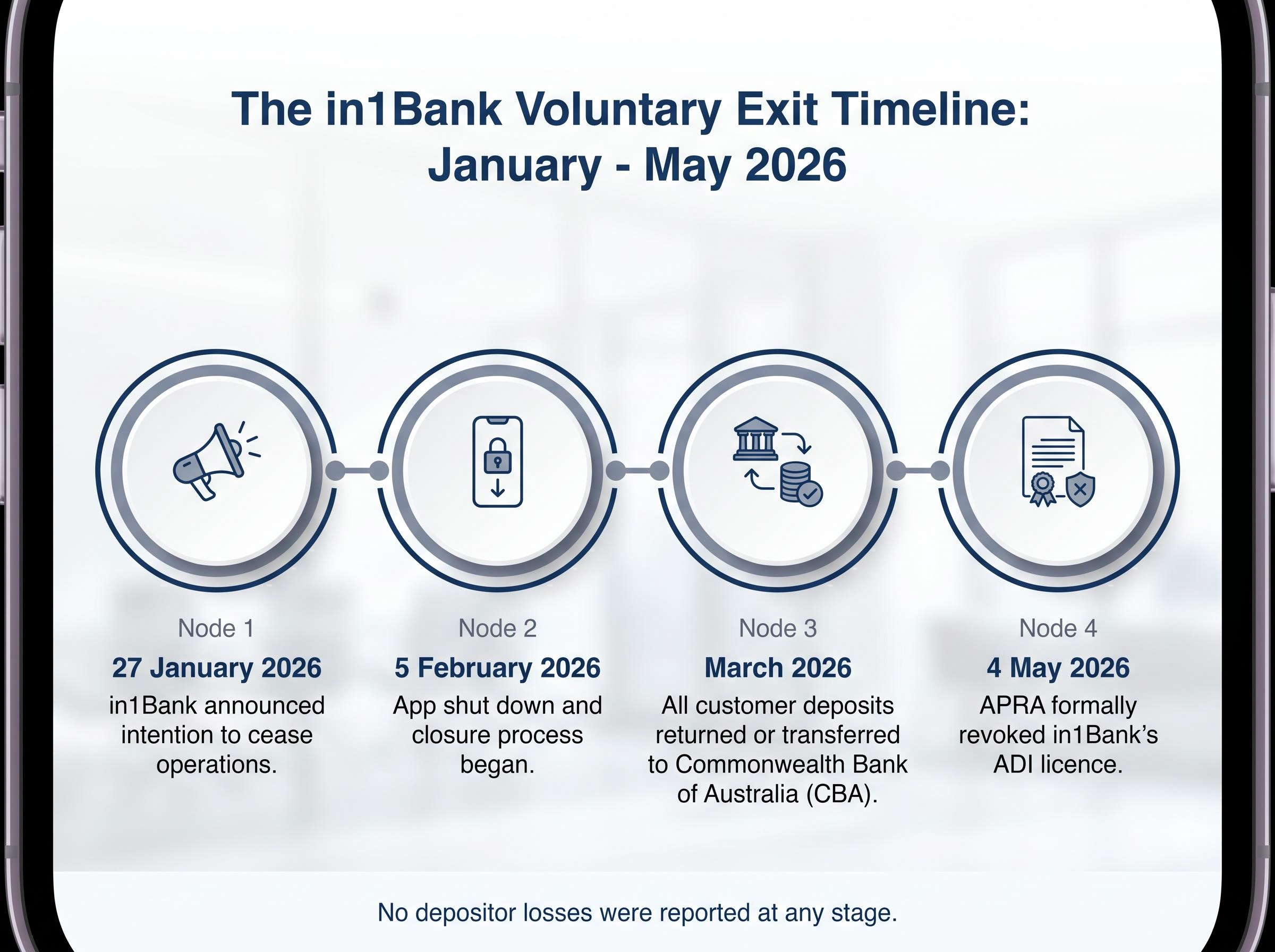

- 27 January 2026: in1Bank announced its intention to cease operations. Fintechnews.au reported that customer funds remained safe under FCS protections.

- 5 February 2026: The in1Bank app was shut down and the account closure process began, with customers given a structured window to transfer funds.

- March 2026: All customer deposits were returned or transferred. Most customers self-transferred funds; remaining balances were moved to the Commonwealth Bank of Australia (CBA) under APRA-supervised transfer powers.

- 4 May 2026: APRA formally revoked in1Bank’s ADI licence under the Banking Act 1959.

- Post-revocation: APRA updated its register of authorised deposit-taking institutions to reflect the cancellation.

No depositor losses were reported at any stage of the wind-down process. Funds were returned or transferred before formal revocation, meaning the FCS backstop was never triggered.

The distinction matters. This was a voluntary exit, not a failure. APRA supervised the handoff at every stage, and CBA served as the receiving institution for any balances customers had not already moved. By the time the licence was cancelled, there was nothing left to protect.

When big ASX news breaks, our subscribers know first

What an ADI licence is and who needs one

An ADI licence is the legal authority an institution must hold to accept deposits from the Australian public. Without it, taking deposits is prohibited under the Banking Act 1959. The licence applies equally to the major four banks, credit unions, building societies, and mutual banks; any entity that wants to hold customer deposits must sit within this regulatory perimeter.

APRA, the regulator that grants and supervises these licences, oversees institutions holding approximately $9.8 trillion in assets on behalf of Australian depositors, policyholders, and superannuation fund members (as of 4 May 2026). That figure reflects the scale of the framework’s reach. A neobank like in1Bank sat within the same regulatory structure as CBA or Westpac, subject to the same deposit protection obligations.

Full ADI licence versus the Restricted ADI pathway

APRA offers two licensing pathways, and the distinction is particularly relevant for newer entrants to the banking sector.

| Attribute | Full ADI licence | Restricted ADI (RADI) licence |

|---|---|---|

| Eligibility | Established institutions meeting all prudential requirements at application | New entrants, typically fintechs and digital banks |

| Deposit restrictions | None beyond standard prudential requirements | Capped deposits during the transition period |

| Transition period | Not applicable | Two-year window to meet full ADI requirements |

| Typical applicant | Banks, credit unions, building societies with existing operations | Fintech start-ups and challenger banks entering the market |

The RADI pathway was designed to lower the barrier for new entrants without lowering the standard. Applicants operate under deposit caps and phased compliance obligations during a two-year transition window, after which they must meet the full ADI requirements or surrender the licence. in1Bank entered the market through the RADI pathway before graduating to full ADI status, a trajectory APRA intended when it created the restricted licence category.

How APRA grants an ADI licence: the application process

Obtaining an ADI licence is a credentialing process, not a form submission. APRA assesses whether an applicant can safely hold public deposits before, during, and after authorisation. The process follows a defined sequence:

- Pre-application contact: Early consultation with APRA before formal lodgement, designed to filter out underprepared applicants and clarify expectations.

- Formal submission: Detailed application including business plans, capital adequacy evidence, governance structures, and risk management frameworks.

- APRA assessment: Evaluation across four criteria: capital adequacy, governance structures, operational readiness, and risk management frameworks.

- Approval: Licence granted with conditions appropriate to the applicant’s risk profile and structure.

- Ongoing supervision: Continuous prudential oversight under APRA’s regulatory framework.

Post-licensing supervision is continuous, not a one-time assessment. APRA does not step back once a licence is issued. Ongoing compliance with capital, governance, and operational requirements is monitored throughout the life of the licence.

APRA’s enforcement toolkit includes intensified oversight, additional licence conditions, and direct enforcement action, a point the regulator made explicit in its April 2026 supervisory letter to Australian banks, insurers, and superannuation trustees, signalling that its supervisory reach is active and escalating across multiple dimensions of regulated conduct.

That continuous oversight is what made in1Bank’s exit orderly. APRA was not reacting to a surprise. The regulator was supervising a process it had visibility over from the moment in1Bank signalled its intention to leave.

Full details of APRA’s licensing requirements are available through its published licensing guidelines and application steps.

APRA’s ADI licensing guidelines detail the specific capital adequacy, governance, and risk management standards that applicants must satisfy across both the full ADI and Restricted ADI pathways, setting out exactly what APRA evaluates before granting any institution the authority to hold public deposits.

How APRA revokes an ADI licence: the five-stage voluntary exit process

The voluntary exit framework APRA applies is designed to protect depositors at every stage, not just at the point of formal revocation. in1Bank’s case maps directly onto the five stages:

- Intent notification: in1Bank notified APRA on 27 January 2026 of its plan to cease operations, triggering the formal wind-down process.

- Deposit return: Between February and March 2026, all customer deposits were returned directly to customers or transferred to CBA under APRA-supervised transfer powers, drawing on the Financial Sector (Transfer and Restructure) Act 1999.

- Operational cessation: The in1Bank app was shut down on 5 February 2026 and account closure processes completed by March.

- Formal revocation: On 4 May 2026, with all deposits cleared and no ADI activities remaining, APRA cancelled the licence under the Banking Act 1959.

- Register update: APRA published a revised list of registered ADIs reflecting in1Bank’s removal.

APRA’s consistent preference across voluntary exits is deposit transfer over liquidation. The process is designed so that by the time formal revocation occurs, it is administrative confirmation of an exit that has already been completed in practice.

Other recent ADI revocations: in1Bank is not an isolated case

The in1Bank revocation follows a pattern. In October 2024, APRA revoked two banking licences. In March 2026, the Bank of Nova Scotia’s ADI licence was revoked. Across all recent cases, no consumer losses were reported.

These exits demonstrate that voluntary ADI revocations are a recurring, managed feature of the Australian banking sector. Challenger banks and foreign-licensed institutions can exit without broader disruption when the supervised process is followed.

What the Financial Claims Scheme actually protects and when it applies

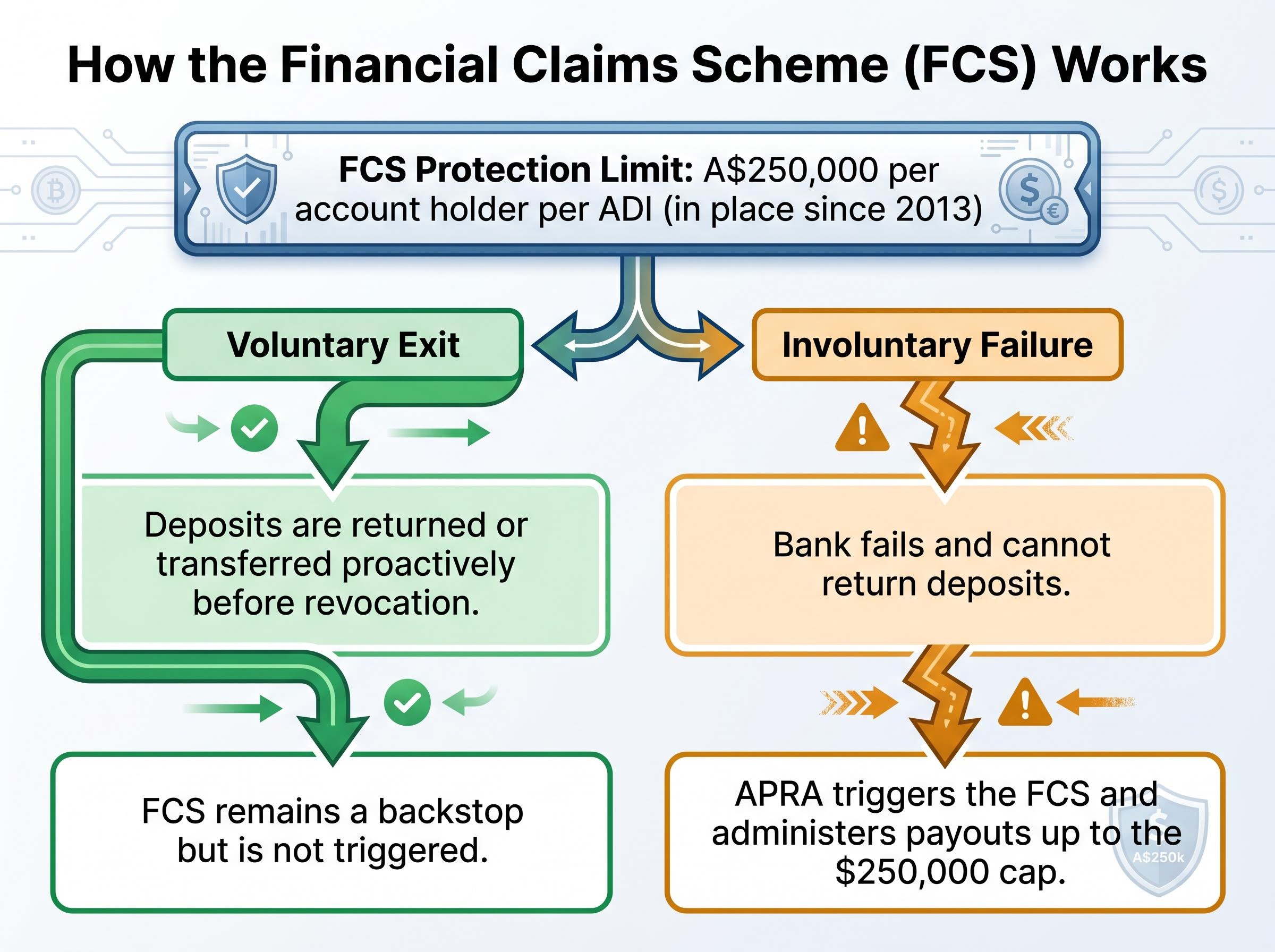

The FCS is Australia’s depositor safety net, administered by APRA under the Banking Act 1959. Its core protection is a defined limit.

The FCS protects eligible deposits up to A$250,000 per account holder per ADI. This figure is aggregated across all accounts held with that institution. The limit has been in place since 2013.

Understanding when the FCS applies, and when it does not, requires distinguishing between two scenarios:

APRA’s Financial Claims Scheme framework draws its legislative authority from the Banking Act 1959 and the Financial Claims Scheme (ADIs) Levy Act 2008, establishing the legal basis under which APRA can administer payouts to eligible depositors when an ADI fails and the orderly transfer process cannot be completed.

- Voluntary exit (the in1Bank case): Deposits are returned or transferred proactively before revocation. The FCS is in place as a backstop but is not triggered because customers receive their funds through the orderly wind-down process.

- Involuntary failure: If an ADI fails and cannot return deposits, APRA triggers the FCS and administers payouts to eligible depositors up to the $250,000 cap.

Fintechnews.au reported in January 2026 that customer funds remained safe under FCS protections during the in1Bank wind-down. That reporting was accurate in the sense that the FCS backstop was available. In practice, though, the scheme was never needed. Deposits were returned before revocation made the question relevant.

The $250,000 per ADI limit is the single most practically useful number for Australian depositors managing where they hold savings, particularly those considering whether to spread deposits across multiple institutions. Current FCS parameters are available directly from APRA’s dedicated FCS information page.

Australian bank valuations and their concentration within the ASX 200 represent a separate dimension of risk for depositors who hold savings and investments with the same institutions, with Morningstar flagging all four major banks as overvalued at current multiples as at late April 2026.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The next major ASX story will hit our subscribers first

Australia’s ADI framework has a quiet record on depositor safety

The in1Bank revocation is worth understanding not as a warning sign but as a demonstration. The ADI framework worked. A small digital bank announced it was leaving, APRA supervised the process, deposits were returned, and the licence was cancelled. No depositor harm. No systemic disruption.

APRA’s supervision covers institutions holding $9.8 trillion in assets as of 4 May 2026. Recent exits, including in1Bank, the Bank of Nova Scotia in March 2026, and two revocations in October 2024, were all completed without consumer loss. A slight downward trend in ADI numbers from these voluntary exits reflects normal consolidation in maturing digital banking markets, not structural weakness.

APRA’s systemic oversight extends well beyond licensing decisions: the regulator supervises institutions holding $9.8 trillion in assets across banking, insurance, and superannuation, meaning its supervisory posture on any emerging risk carries consequences for the entire financial system, not just individual institutions.

Three practical steps follow from this:

- Check that any bank holds an ADI licence by verifying its listing on APRA’s official register.

- Confirm deposits remain under $250,000 per ADI to maximise FCS coverage, particularly when holding savings across multiple accounts at one institution.

- Understand the difference between voluntary exit and involuntary failure. The protections apply in both cases, but the mechanisms differ.

APRA’s quarterly ADI statistics publications provide ongoing data on the sector for those who want to monitor trends directly.

The in1Bank case is an example of how the system is supposed to work

The in1Bank revocation illustrates a straightforward principle: Australia’s ADI licensing framework, when followed, produces orderly exits with no depositor harm. The process rests on three structural pillars. The ADI licence itself functions as a regulatory threshold that places every licensed institution within APRA’s supervisory reach. The supervised exit process ensures deposits are returned before a licence is cancelled. The FCS provides a backstop guarantee that protects depositors up to $250,000 per ADI if the orderly process cannot be completed.

For Australian depositors, the practical value sits in two actions. Verify that any institution holding deposits appears on APRA’s official ADI register. And review deposit distribution if total savings at a single ADI exceed the $250,000 FCS protection limit.

The framework is designed to make banking exits unremarkable. In the in1Bank case, that is precisely what it achieved.