Why a Rising AUD Is Quietly Eroding Your International ETF Returns

5 hrs ago

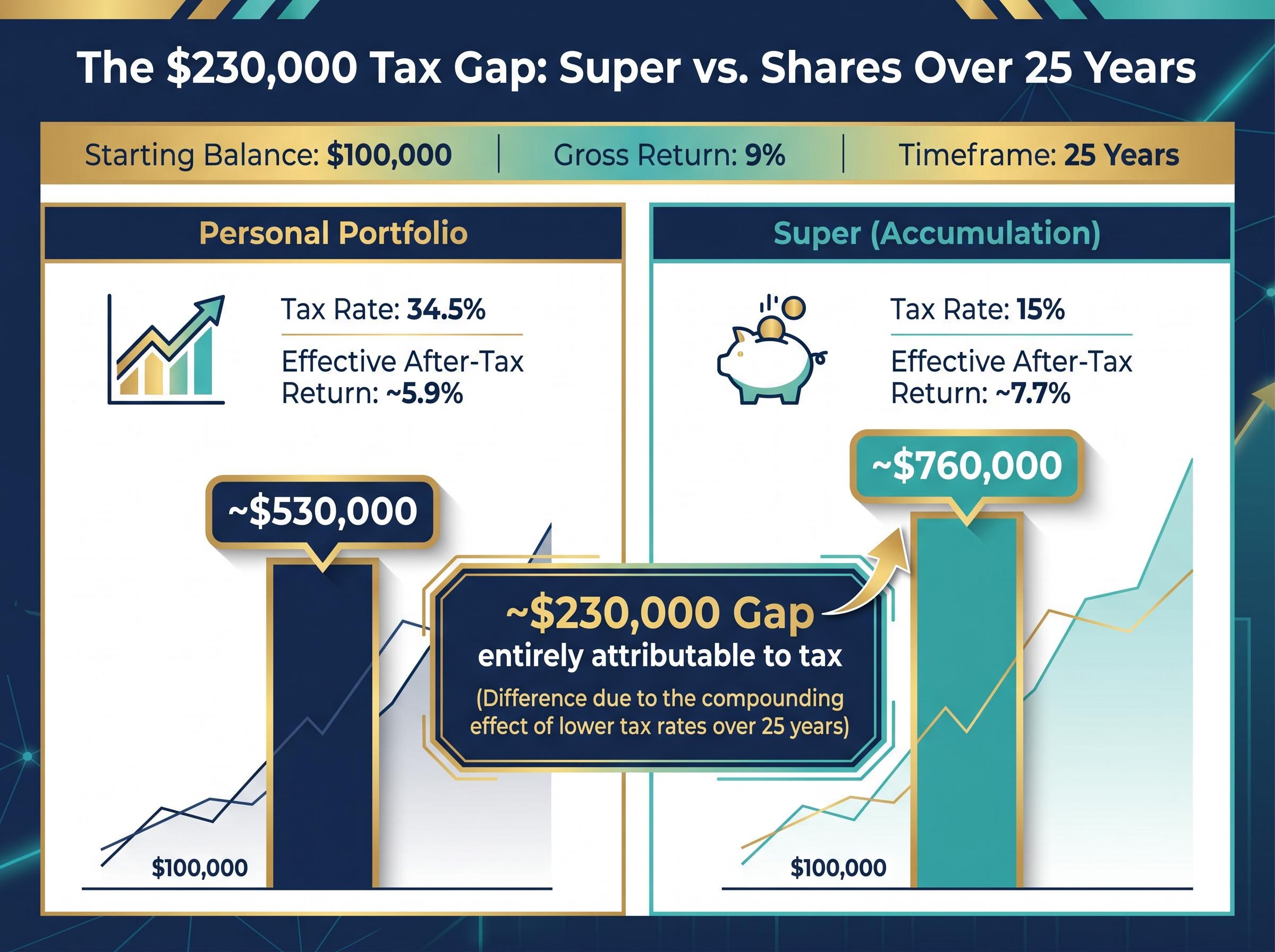

A 35-year-old Australian who puts $100,000 into a low-cost ASX 200 index fund and earns 9% gross returns could end up with roughly $230,000 less at age 60 than if that same capital went into superannuation. Same starting amount. Same underlying return. Different tax environment.

The raw return comparison between super and shares is a familiar debate, but it consistently misframes the real question. The ASX 200 Accumulation Index has delivered approximately 9.2% per annum over the 10 years to December 2025, outpacing the median balanced super fund (7.7%-7.8% over the same period, per SuperRatings and APRA data). Most investors see this gap and assume the share portfolio wins. They are measuring the wrong thing.

This guide explains why the tax structure, not the return figure, determines which vehicle builds more wealth for working Australians. It covers how marginal tax rates erode share portfolio returns, how the 15% super earnings tax compounds into a material wealth gap, where accessibility constraints change the calculus by age, and how to structure a practical allocation decision using 2025-26 figures.

Contributions to super cannot be accessed until preservation age, which is 60 for all Australians born after 1 July 1964. For a 35-year-old, that means locking funds away for approximately 25 years with no emergency access outside limited hardship provisions.

The ATO preservation age rules confirm that Australians born on or after 1 July 1964 cannot access their super until age 60, a hard constraint that defines the entire liquidity calculus for investors currently in their 30s and 40s.

A personal share portfolio carries no such restriction. ETF holdings can be sold at any age to fund a property purchase, a business investment, a career transition, or an unexpected family need. Brokerage costs for typical online trades sit at $10-$20 per trade, and broad-market ETF management expense ratios range from 0.03%-0.20% per annum, substantially lower than industry super fund fees of 0.5%-1.0% per annum.

The fee comparison between ETFs and super funds is further complicated by structural costs inside super funds that sit entirely outside the headline fee figure, including pooled CGT drag from member redemptions and swap-based financing spreads embedded in some index options, none of which appear in the standard fee disclosures required under Regulatory Guide 97.

Super’s rules have been amended multiple times over the past two decades. Contribution caps, tax rates, and preservation thresholds are subject to legislative change. A personal investment portfolio is immune to retrospective rule changes on access.

Some financial advisers frame super’s illiquidity as a discipline advantage: money that cannot be accessed cannot be spent on lifestyle costs. There is behavioural evidence supporting this view, but it does not change the practical reality for anyone who may need capital before 60.

“The $230,000 super advantage is only realisable if you never need the money before you turn 60.”

Key attributes of each vehicle at a glance:

The gross return gap is real. Over the decade to December 2025, the ASX 200 Accumulation Index returned approximately 9.2% per annum while the median balanced super fund returned 7.7%-7.8%. On the surface, a personal share portfolio looks like the better vehicle.

Then tax arrives.

Dividend income earned outside super is assessed at the investor’s marginal rate. For someone earning $90,000-$120,000, that effective marginal rate is 34.5% (the 32.5% bracket plus the 2% Medicare levy). A nominal 9% gross return on a personal share portfolio is effectively reduced to approximately 5.8%-6% once that rate is applied to income distributions and capital gains events triggered by rebalancing.

Franking credits offer partial relief on fully franked Australian dividends, but they do not apply to international ETFs, unfranked income, or capital gains realised through portfolio rebalancing. For investors holding diversified portfolios with global exposure, the franking credit offset covers only a fraction of the tax drag.

Franking credit calculations apply a standard 30/70 formula to the cash dividend, but the tax outcome differs substantially depending on whether the recipient is a high-income individual, a pension-phase SMSF, or a zero-tax investor, with the latter two receiving the full credit as a cash refund from the ATO rather than merely an offset against a personal tax liability.

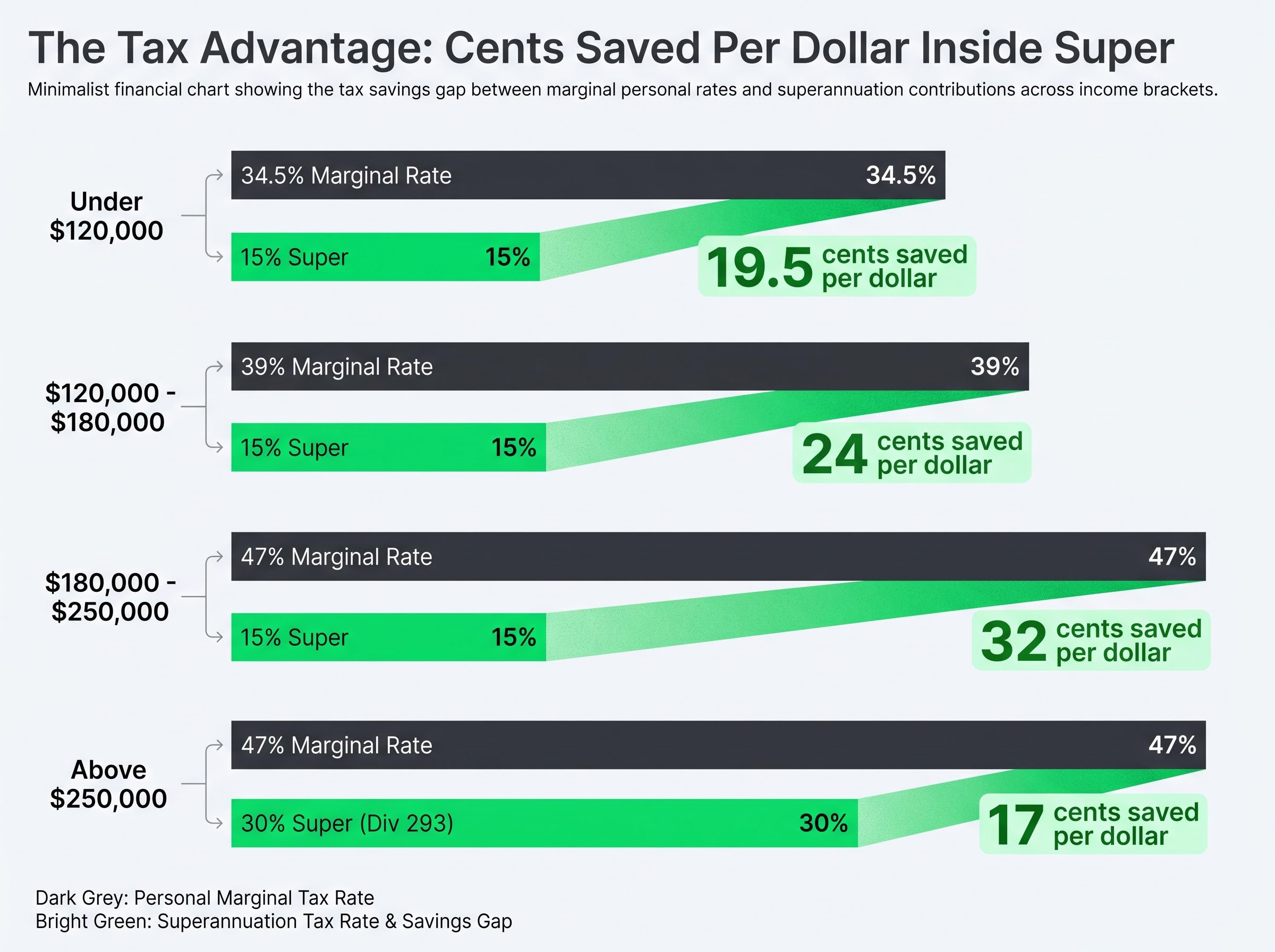

Inside super, those same earnings are taxed at a flat 15%. For assets held longer than 12 months, the effective capital gains tax rate inside super drops to 10% after the one-third discount. The gap between 34.5% and 15% is not a marginal difference. It is 19.5 cents on every dollar of return, compounding annually for decades.

“For a $90,000 earner, every dollar of investment return outside super is taxed at 34.5 cents. Inside super, it is taxed at 15 cents.”

| Vehicle | Gross Return | Tax Rate on Earnings | Effective After-Tax Return |

|---|---|---|---|

| Personal shares ($90,000 earner) | 9% | 34.5% | ~5.9% |

| Personal shares ($150,000 earner) | 9% | 39% | ~5.5% |

| Super (accumulation phase) | 9% | 15% | ~7.7% |

The apparent return advantage of a personal share portfolio disappears once the after-tax comparison is made. For most working Australians, super’s lower return figure produces a higher after-tax outcome.

Super fund earnings, including interest, dividends, rent, and capital gains, are taxed at a flat 15% inside an accumulation account. This rate applies regardless of the member’s personal income level. A worker earning $60,000 and a worker earning $200,000 both pay 15% on the returns their super balance generates.

The three contribution pathways each carry different tax treatment:

The concessional contributions cap sits at $30,000 for 2025-26, rising to $32,500 from 1 July 2026. The non-concessional cap is $120,000 in 2025-26, increasing to $130,000 from 1 July 2026.

The carry-forward concessional rule adds another lever. Unused concessional cap amounts from the previous five years can be applied in a single year, provided total super balance was below $500,000 at the prior 30 June.

“The carry-forward rule means an eligible individual with five years of unused caps could potentially contribute $100,000 or more into super in a single high-income year.”

From 1 July 2026, individuals with total super balances exceeding $3 million will face an additional 30% tax on earnings attributable to the portion above that threshold. This lifts the effective earnings tax rate to 30% on that component.

At 30%, the super tax advantage over a 34.5% marginal rate earner narrows to just 4.5 percentage points, substantially reducing the compounding benefit modelled in the projections that follow. This measure applies from 1 July 2026 and is relevant only to those approaching the $3 million threshold. For the vast majority of accumulators aged 35-50, the standard 15% rate continues to apply.

The ATO confirmation that Division 296 is now law establishes that the additional 30% tax on super earnings above $3 million applies from the 2026-27 financial year, a detail material to any accumulator whose balance is approaching that threshold and who is weighing where to direct the marginal contribution dollar.

Consider a 35-year-old who invests $100,000 today, earning 9% gross per annum, and leaves it untouched until age 60.

The $100,000 scenario modelled above assumes a single lump sum entry, but a lump sum deployment strategy is not automatically the right choice for every investor: research covering 10-year periods on the ASX suggests lump sum investing outperforms dollar-cost averaging in roughly two-thirds of scenarios, yet the one-third of periods where DCA wins tend to cluster around exactly the kind of elevated volatility conditions that characterised early 2026.

In a personal share portfolio, tax applies every year. Dividend distributions and capital gains events from rebalancing are assessed at the investor’s marginal rate. Assuming a 34.5% effective tax rate on those distributions (consistent with a $90,000-$120,000 earner), the annual after-tax return sits around 5.9%. Over 25 years, $100,000 compounding at that rate grows to approximately $530,000.

Inside super’s accumulation phase, the same 9% gross return is taxed at 15%, producing an after-tax return of approximately 7.7%. Over the same 25 years, the super balance grows to approximately $760,000.

The projected gap: roughly $230,000. Same capital. Same underlying market return. The difference is entirely attributable to the tax environment.

| Metric | Personal Portfolio | Super (Accumulation) |

|---|---|---|

| Starting balance | $100,000 | $100,000 |

| Tax rate on earnings | 34.5% | 15% |

| Effective after-tax return | ~5.9% | ~7.7% |

| Projected balance at age 60 | ~$530,000 | ~$760,000 |

Both scenarios assume comparable underlying investments. The $100,000 lump sum fits within the non-concessional contribution cap of $120,000 in 2025-26 (rising to $130,000 from 1 July 2026), making this a practical scenario, not a theoretical one.

The projection above stops at age 60, but the tax advantage does not. Once a member commences a pension account from their super balance at or after age 60, earnings on that balance become tax-free (0% tax). Withdrawals from a taxed super fund are also tax-free for members aged 60 and over.

No other Australian investment vehicle, including trusts, companies, or investment bonds, replicates this structural benefit. The 25-year projection is conservative; the actual advantage widens further if returns continue to compound at 0% tax in pension phase.

The optimal allocation is not super or shares. It is a sequenced combination that shifts with age.

50 and over: shift weight toward super. With 10 or fewer years to preservation age, the lock-up period shortens and the compounding window narrows, but the marginal tax saving on concessional contributions remains the same. Liquidity risk is lower because the funds are accessible sooner. This cohort benefits most from maximising both concessional and non-concessional contributions where total super balance permits.

Under 40: lean toward accessible investments. Investors under 40 face the highest opportunity cost from locking capital inside super. The liquidity constraint covers 20-plus years and intersects with the life stage most likely to demand capital for a first home, career changes, or family costs. The practical action: contribute concessionally to the $30,000 cap to capture the marginal tax saving, then direct surplus savings into a diversified ETF portfolio held outside super.

40-50: the hybrid bracket. With 10-20 years to preservation age, the compounding benefit of super’s tax rate becomes more valuable while liquidity needs remain real. The three-step sequence:

For a $120,000 earner, the annual tax saving from maximising concessional contributions is approximately $2,925, captured every year the strategy is maintained.

| Age Tier | Primary Vehicle | Super Strategy | Liquidity Position | Key Action |

|---|---|---|---|---|

| Under 40 | Personal ETF portfolio | Concessional cap only | High liquidity priority | Max concessional; surplus to ETFs |

| 40-50 | Hybrid | Max concessional; consider non-concessional | Moderate liquidity priority | Three-step sequence above |

| 50+ | Super | Maximise both contribution types | Lower liquidity priority | Accelerate super contributions |

Australia’s wealthiest retirees typically maintain both a super balance and a personal investment portfolio running in parallel. The either/or framing is the wrong question. The right question is how much in each, adjusted for age.

For incomes above $180,000, the effective marginal rate rises to 47% (45% plus the 2% Medicare levy). The gap between the personal tax rate and super’s 15% rate widens to 32 percentage points, making the super tax saving even more powerful than the base case projection suggests.

Division 293 introduces a caveat. For incomes above $250,000, concessional contributions are taxed at 30% rather than 15%, halving the entry concession. Super remains advantageous relative to the 47% marginal rate, but the benefit is reduced.

The income-based tax scenarios break down as follows:

From 1 July 2026, the Division 296 tax changes the calculus for individuals whose total super balance is growing toward $3 million. The additional 30% tax on earnings attributable to the portion above that threshold may make redirecting incremental contributions to a personal portfolio more advantageous for that marginal dollar.

“From 1 July 2026, a super balance above $3 million means the extra dollar inside super is taxed at 30%, the same rate a $90,000 earner’s marginal bracket starts at outside super.”

The 50% CGT discount for personal portfolios becomes more relevant at this level. Individual investors who hold shares or ETFs for more than 12 months pay CGT on only 50% of the nominal gain. At a 47% marginal rate, this produces an effective CGT rate of 23.5%, a meaningful concession that partially offsets super’s earnings tax advantage for high-balance investors.

For this cohort, the question is not whether super is useful. It is where the marginal dollar should go once the balance approaches the $3 million threshold.

For most working Australians earning above $45,000, the super tax environment produces meaningfully better after-tax compounding than a personal share portfolio. The $230,000 projected gap over 25 years on a $100,000 investment is not a rounding error. It is the cost of ignoring how tax interacts with compounding.

But super alone is not the answer for anyone who may need liquidity before 60. The practical default sequence:

Choosing a high-growth investment option inside super, rather than the default balanced option, has historically added approximately 1.5% per annum in returns. Over 25 years on a $100,000 balance, that difference represents more than $200,000 in additional wealth, a decision that takes minutes to implement and costs nothing.

Active fund investment decisions inside super carry a cost that compounds alongside the fee drag: elevated portfolio turnover generates transaction costs, cash drag, and mistimed re-entries that reduce after-tax returns without appearing as a line item in member statements, which is why the choice of investment option within super matters almost as much as the decision to use super in the first place.

Personal tax circumstances, total super balance, age, and specific financial goals mean professional financial advice is recommended before making large contribution decisions, particularly regarding non-concessional and carry-forward strategies.

Members sitting in a default balanced super option may be forfeiting approximately 1.5% per annum compared to a high-growth option within the same fund. Switching options is typically free and can be completed in minutes through the fund’s online portal.

This is separate from the super vs. shares allocation decision. It applies regardless of how much a member contributes and affects every dollar already inside super.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—

Superannuation and personal share portfolios both invest in similar underlying assets, but they are taxed very differently. Super earnings are taxed at a flat 15%, while personal share portfolio returns are taxed at your marginal income tax rate, which can be as high as 47% for high earners.

Based on a $100,000 investment earning 9% gross per annum over 25 years, a super accumulation account produces approximately $760,000 at age 60, compared to around $530,000 in a personal share portfolio for a $90,000-$120,000 earner, a projected gap of roughly $230,000 due entirely to the different tax environments.

No, Australians born on or after 1 July 1964 cannot access their superannuation until they reach preservation age, which is 60. Outside of limited hardship provisions, funds locked inside super are inaccessible for decades, which is a key reason younger investors should also hold liquid assets outside super.

The concessional contributions cap for the 2025-26 financial year is $30,000, rising to $32,500 from 1 July 2026. These pre-tax contributions, made via salary sacrifice or personal deductible contributions, are taxed at 15% upon entry into super rather than at your marginal income tax rate.

Division 296 is a tax measure that applies from 1 July 2026 to individuals with total super balances above $3 million, adding an extra 30% tax on earnings attributable to the portion of the balance above that threshold. This effectively reduces super's tax advantage for high-balance investors, narrowing the gap between super and personal portfolio tax rates.