Delivery Hero Shareholders Reject Uber’s €33 Bid, Demand €40+

1 hr ago

Goldman Sachs has doubled its 2026 earnings growth forecast for the STOXX Europe 600 to 10%, but the revision tells a more complicated story than the headline suggests. The upgrade, published 5 May by strategist Sharon Bell’s team, arrives as Brent crude trades above $113 a barrel and TTF natural gas is up nearly 38% year-over-year. Those same energy prices are simultaneously boosting commodity-sector earnings and suppressing broader European economic growth, creating a split market that a single headline number obscures. What follows unpacks what is actually driving the upgrade, why the non-commodity earnings picture remains weak, what the macro backdrop means for European equity exposure, and how investors should read the difference between a headline-grabbing STOXX 600 forecast revision and a genuinely healthy earnings environment.

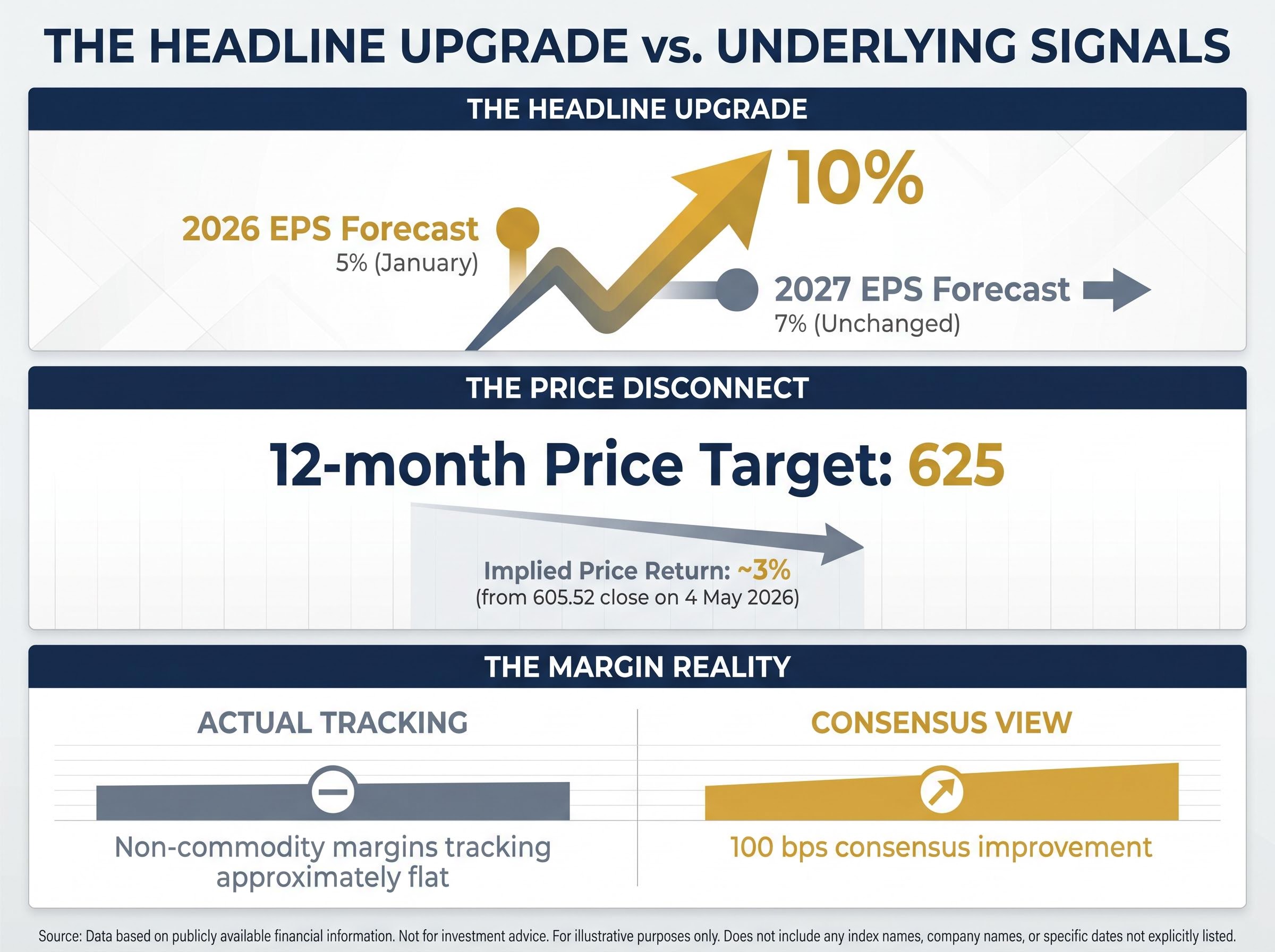

Goldman raised its STOXX Europe 600 earnings-per-share growth estimate to 10% for 2026, up from a prior forecast of 5% set in January 2026. The revision is substantial. It is also structurally narrow.

Goldman Sachs, 5 May 2026: STOXX Europe 600 EPS growth forecast revised to 10%, up from 5% in January, driven primarily by commodity-sector earnings improvements.

Commodity sector improvements, not broad economic strength, are the primary driver. Energy and mining companies are converting elevated oil and gas prices into earnings beats that lift the index-level number. The 2027 EPS growth forecast remains unchanged at 7%, with energy earnings expected to partially reverse next year, a signal that Goldman’s own team views the commodity tailwind as temporary rather than structural.

The STOXX Europe 600 index methodology uses free-float market capitalisation weighting across 600 large, mid, and small-cap constituents spanning 17 European countries, which means heavily weighted commodity names like Shell, BP, Glencore, and Rio Tinto can move index-level EPS figures substantially even when the majority of constituent sectors are experiencing flat or declining profitability.

The gap between a doubled earnings forecast and a modest 3% implied price upside is itself telling. The market is not pricing this upgrade as a signal of durable strength.

Earnings per share (EPS) growth forecasts are forward estimates of corporate profitability per share across an index. Investment banks publish them because they are one of the primary inputs investors use to price in future returns. When Goldman forecasts 10% EPS growth for the STOXX 600, it is estimating that the aggregate profits of the roughly 600 large and mid-cap companies in the index will grow by that amount over the year.

Not all EPS upgrades carry the same weight. A broad-based upgrade, where most sectors are lifting together, suggests underlying economic strength and tends to support sustained index gains. A sector-concentrated upgrade, where one area compensates for weakness elsewhere, creates a different risk profile. The rising EPS number may mask deterioration in the majority of the index’s constituents, which matters for investors whose holdings are diversified across sectors rather than concentrated in the outperforming group.

This distinction between earnings quality and earnings quantity is what connects Goldman’s 10% EPS forecast to its relatively modest 625 price target. The headline growth rate is high, but the composition of that growth limits the degree to which the broader index can reprice upward. Understanding this framework is what separates a surface reading of the revision from an informed one.

Goldman’s analysis finds that non-commodity profit margins are expected to remain approximately flat in 2026. That directly contrasts with the consensus expectation for 100 basis points of margin improvement across European equities.

Goldman Sachs notes that non-commodity margins are tracking approximately flat for 2026, versus the consensus forecast of 100 basis points of improvement, a gap that the headline EPS number does not reveal.

The divergence is sharpest in consumer-facing sectors. Since the Middle East conflict began in late February 2026, earnings estimates have been cut most aggressively in Travel and Leisure, Automobiles, and Luxury Goods. These sectors are absorbing the downstream effects of elevated energy costs through compressed margins and weakening demand.

| Sector | Earnings revision direction (post-conflict) | Notes |

|---|---|---|

| Shell / BP (Energy) | Upward | Shell Q1 2026 adjusted earnings ~$6.36 billion; BP Q1 profit $3.8 billion |

| Glencore / Rio Tinto (Mining) | Upward | Glencore copper production 199.6 kt Q1 2026 (up YoY); Rio Tinto 9% YoY increase in copper-equivalent output |

| Travel and Leisure | Downward | Among sharpest earnings estimate cuts since conflict onset |

| Automobiles | Downward | Margin pressure from input costs and weakening demand |

| Luxury Goods | Downward | Consumer discretionary weakness across European markets |

| Banks / Technology / Utilities | Relatively stable | Holding up better through the current cycle |

For investors holding diversified European equity exposure, the implication is direct: the index-level EPS upgrade may not translate proportionally into the sectors driving their portfolio returns.

Headline beats masking deterioration beneath the surface is not a uniquely European phenomenon in 2026: in the ASX earnings season, NAB beat consensus cash earnings by 7.1% while credit impairment charges surged 45.6%, a pattern that reinforces the broader argument that index-level or top-line earnings numbers can obscure where fundamental stress is actually accumulating.

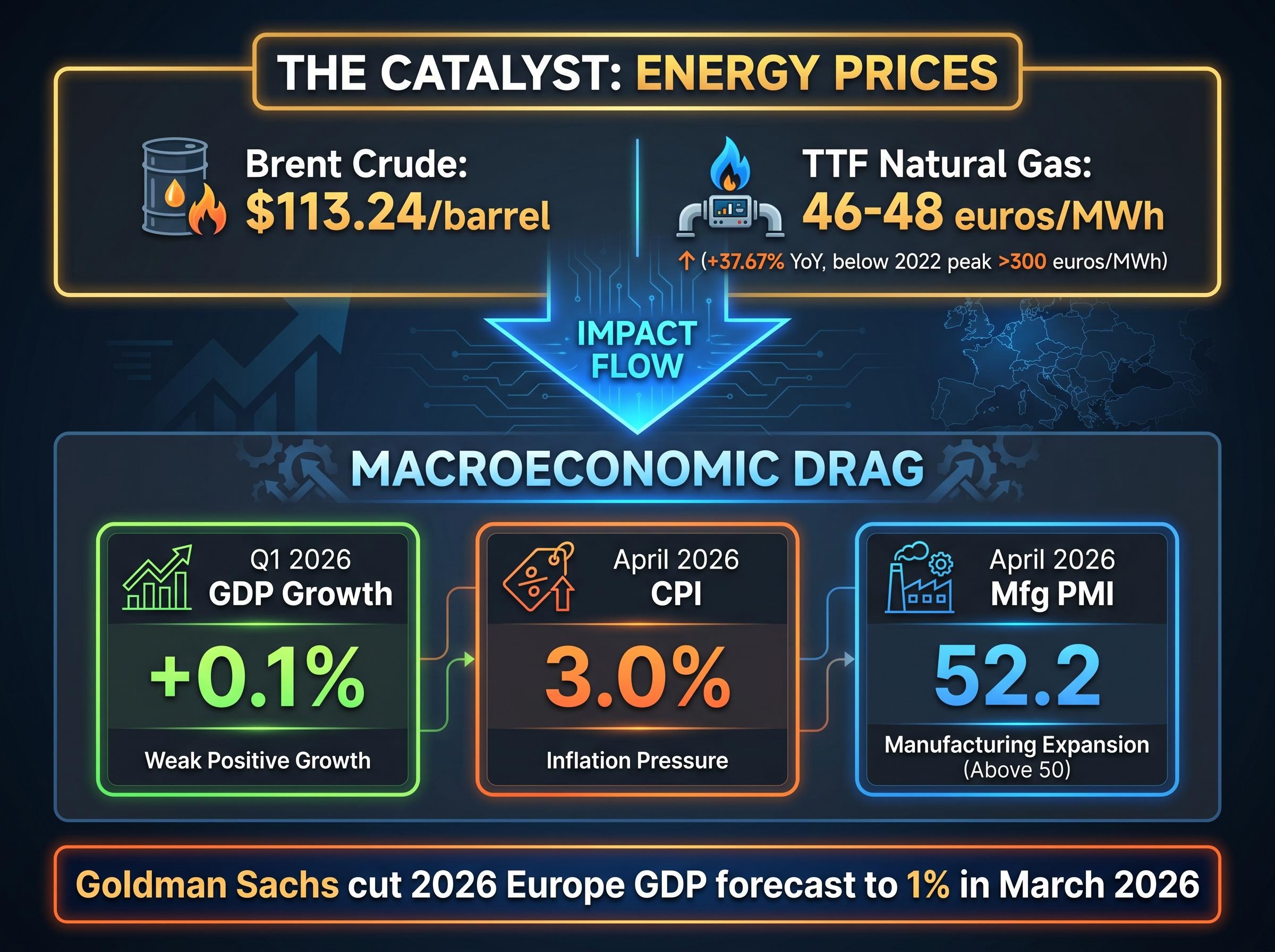

Brent crude at $113.24 per barrel and TTF natural gas at approximately 46-48 euros per MWh (up 37.67% year-over-year) are the engine of the EPS revision. They are also the brake on European GDP.

Goldman cut its Europe 2026 GDP growth forecast to 1% in March 2026, citing the energy price surge. The most recent macroeconomic data confirms an economy operating close to stall speed.

| Macro indicator | Current reading (April-May 2026) | Implication |

|---|---|---|

| GDP growth | +0.1% (Q1 2026) | Near-stagnation; consistent with Goldman’s 1% full-year downgrade |

| CPI (Eurozone) | 3.0% (April 2026) | Above ECB’s 2% target; persistent inflation alongside weak growth |

| Manufacturing PMI | 52.2 (April 2026) | Modest expansion, but fragile given energy cost headwinds |

The combination of near-stagnant growth and above-target inflation raises the question of stagflation. Goldman does not view stagflation as its central case, but the historical data is pointed.

In stagflationary environments, median real quarterly STOXX 600 returns fall to approximately -1%, compared with approximately +3% in normal periods, according to Goldman Sachs research.

Current TTF gas prices of approximately 46-48 euros per MWh remain well below the 2022 crisis peak of over 300 euros per MWh, providing some perspective on the severity of the current episode. The paradox, however, is real: Goldman’s EPS optimism and Goldman’s macro caution are not contradictory. They are two readings of the same energy price surge.

The STOXX 600 forward price-to-earnings ratio has fallen from approximately 18x in January 2026 to 14.4x-14.63x in May 2026. That compression has been substantial, but it has not approached the 10.4x trough reached during the 2022 energy crisis. Goldman has described this valuation resilience as “the most surprising aspect” of European market behaviour during the current geopolitical episode.

The relationship between valuation compression and stagflation has been particularly acute for growth-oriented names in 2026, with Morningstar data showing growth equities trading at a 21% discount to fair value as of late March, a level that has occurred less than 5% of the time since 2011 and that reflects the same energy-driven multiple compression now reshaping the STOXX 600’s sector rotation.

Capital-intensive sectors have been the clear beneficiaries. Goldman’s capital-intensive basket is up approximately 36% since January 2025 and has outperformed broader European equities by roughly 3% since the conflict’s onset in late February 2026. Quality strategies and Goldman’s GRANOLAS basket (the cohort of large-cap European growth names) are among the weakest performers year-to-date.

Each 1% rise in crude oil prices reduces European equity valuations by approximately 20 basis points through multiple compression, according to Goldman Sachs analysis.

Goldman’s current sector overweight recommendations reflect this rotation:

The valuation compression and the sector rotation together tell investors where risk and opportunity are distributed within European equities right now. The index is cheaper than it was five months ago, but the repricing has not been uniform.

The 10% EPS forecast is real and supported by commodity earnings data. It also rests on a narrow foundation that Goldman itself expects to partially reverse in 2027, when the EPS growth forecast drops to 7% with energy earnings projected to decline.

Goldman’s view sits in the middle of the Street. Peer forecasts offer useful context for positioning:

The contrast with the US picture is stark: earnings beat rates in the S&P 500 for Q1 2026 ran at 84%, with a blended growth rate of 27.1% against a 13.1% consensus forecast, a dynamic driven by mega-cap technology rather than commodity extraction, which illustrates how differently the same global energy shock is flowing through corporate income statements on either side of the Atlantic.

| Bank | 2026 STOXX 600 target | EPS growth forecast |

|---|---|---|

| Goldman Sachs | 625 | 10% |

| Morgan Stanley | ~630 | 14-16% |

| UBS | 650 | Not specified |

| Barclays | 620-623 | Not specified |

| JPMorgan | Positive (unspecified) | Positive EPS growth |

European equities remain roughly flat year-to-date and approximately 4% below pre-conflict peak levels reached in late February 2026. The market is not yet pricing in a full recovery, despite the EPS upgrade. Historical context underscores how different the current environment feels: the STOXX 600 gained 13% in 2023, 6% in 2024, and 17% in 2025.

Goldman’s January 2026 outlook had identified two swing factors as headwinds for the year:

The reversal on oil validates the EPS upgrade but does not resolve the underlying non-commodity weakness. That tension will define whether the second half of 2026 broadens the recovery or narrows it further.

Goldman’s 10% EPS forecast is a genuine upgrade. It is also commodity-led, consensus-beating on the headline but consensus-lagging on non-commodity margins, and expected to partially reverse in 2027 when the EPS growth forecast steps down to 7%.

European structural headwinds extend beyond the current energy shock: sluggish eurozone growth, elevated energy costs, and an ECB holding rates at 2.00% with no near-term stimulus catalyst have combined to make European equities a consistent underperformer in global capital flow rankings even as aggregate fund flows at the headline level remain superficially positive.

Elevated energy prices are the engine of both the upgrade and the headwinds. That duality will define European equity performance for the remainder of 2026. The index-level number looks strong; beneath it, non-commodity margins are flat against expectations for 100 basis points of improvement.

The single most telling number in the Goldman report: non-commodity margins are tracking approximately flat, versus the 100 basis point improvement the broader consensus had forecast for 2026.

Investors assessing European equity exposure should look through the headline EPS number to the sector composition of their holdings, and watch whether non-commodity margins begin to recover as the year progresses. A commodity tailwind can lift an index. Whether it can sustain one is a different question entirely.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Goldman Sachs revised its STOXX Europe 600 EPS growth forecast to 10% for 2026, up from a prior estimate of 5% set in January 2026, with a 12-month price target of 625 implying approximately 3% price return.

The upgrade was driven primarily by commodity-sector earnings improvements, as elevated Brent crude prices above $113 per barrel and TTF natural gas up nearly 38% year-over-year boosted profits at energy and mining companies like Shell, BP, Glencore, and Rio Tinto.

A commodity-driven upgrade means a narrow group of energy and mining companies is lifting the index-level number while the majority of sectors remain flat or weak; in the current case, Goldman notes non-commodity margins are tracking flat versus consensus expectations of 100 basis points of improvement.

Travel and Leisure, Automobiles, and Luxury Goods have experienced the sharpest earnings estimate cuts since the Middle East conflict began in late February 2026, as elevated energy costs compress margins and weaken consumer demand.

The STOXX 600 forward price-to-earnings ratio compressed from approximately 18x in January 2026 to around 14.4x-14.63x by May 2026, a significant de-rating that Goldman Sachs described as the most surprising aspect of European market behaviour during the current geopolitical episode.