Australian retail REITs are posting occupancy rates that approach perfection. Scentre Group occupancy sits at 99.8%. Vicinity Centres is at 99.6%. These figures arrive at a moment when much of the broader property sector is battling rising bond yields and a delayed recovery outlook, and that tension is where the investment case sharpens.

On 5 May 2026, with the ASX 200 sliding toward a one-month low and Dexus shares falling after management flagged macro headwinds, these two retail landlords stand apart as among the most operationally sound companies on the exchange. The divergence is not noise. It reflects structural differences in how sub-sectors within Australian real estate are absorbing the current environment, and it carries direct implications for how investors allocate within the A-REIT universe.

What follows is an examination of the specific operational metrics driving retail REIT outperformance, what those metrics mean for investors evaluating A-REIT exposure, and what the divergence signals about where value is concentrated in Australian listed property right now.

The performance gap that is reshaping A-REIT allocations

Dexus shares fell 2.72% to $6.09 as at 12:19 pm AEST on 5 May 2026. Management explicitly flagged that shifting macroeconomic conditions and the interest rate outlook were expected to delay recovery across its property portfolio.

That same day, the ASX 200 Real Estate sector was weighed on by elevated US energy costs feeding through to Australian markets and upward pressure on US bond yields. Retail REITs held firm against this backdrop. Vicinity Centres reaffirmed its FY26 funds from operations (FFO) guidance toward the top of the 15.0-15.2 cents per unit range.

This is not a single-day anomaly. It is a representative snapshot of a 12-month pattern in which retail sub-sector fundamentals have diverged materially from office, industrial, and data centre peers. The contrasts are stark:

- Dexus declined 2.72% in a single session, with management signalling delayed recovery

- The broader ASX Real Estate sector faced bond yield and energy cost headwinds

- VCX and SCG both reaffirmed forward earnings guidance at or above prior expectations

Dexus flagged that shifting macroeconomic conditions and the interest rate outlook were expected to delay recovery, a direct counterpoint to the confidence embedded in retail REIT guidance reaffirmations.

Investors scanning A-REIT exposure need to recognise that the sector label “Australian REITs” now masks material sub-sector divergence. Treating A-REITs as a monolithic allocation is likely to produce suboptimal outcomes in the current environment.

When big ASX news breaks, our subscribers know first

What near-perfect occupancy actually tells an investor

Occupancy rate measures the percentage of a landlord’s lettable space that is leased to paying tenants. FFO, or funds from operations, strips out non-cash items like depreciation to show the actual cash earnings a REIT generates from its properties. Both are the primary metrics for evaluating REIT health, more informative than net profit in a property context.

REIT valuation fundamentals like FFO yield, distribution yield, and net tangible asset discounts each capture a different dimension of income-stock pricing, and the relationship between them determines whether a given occupancy rate and leasing spread profile is already priced into the current unit price or still represents upside.

An occupancy rate of 99.6% or 99.8% is not merely an impressive number. It is analytically significant because it signals that tenants cannot find alternative space. When vacancy is effectively zero, the landlord controls rental negotiations. Tenants seeking to renew or enter a centre have limited leverage, and that dynamic converts directly into pricing power.

| Company | Occupancy Rate | Leasing Spread | Rent Escalation |

|---|---|---|---|

| Scentre Group (SCG) | 99.8% | +3.3% (specialty) | 5.3% (average specialty) |

| Vicinity Centres (VCX) | 99.6% | +4.6% (portfolio) | N/A |

From occupancy to income: how leasing spreads compound the advantage

A leasing spread is the percentage difference between the rent on a new lease and the rent on the lease it replaces at expiry. A positive spread means the landlord is re-leasing space at a higher rate each time a lease turns over.

Both VCX and SCG are cycling through lease renewals at above-inflation spreads. Scentre Group completed 636 deals in Q1 2026 at +3.3% specialty releasing spreads, with average specialty rent escalations of 5.3%. Vicinity Centres posted portfolio leasing spreads of +4.6% in H1 FY26. Each renewal cycle lifts the income base, creating a compounding effect over multi-year lease terms that is directly visible in both companies’ FFO guidance.

For investors weighing whether current valuations are justified, this occupancy-to-spread pipeline is where the answer sits. Near-full occupancy is the precondition for compounding rental income growth, which is the engine of long-term REIT total returns.

The consumer data backing the brick-and-mortar thesis

The landlord metrics tell one side of the story. The shopper metrics tell the other.

Scentre Group reported customer visitation of 160 million visits in the year to 19 April 2026, up 3.1%. Business partner sales reached $7.0 billion in Q1 2026, representing growth of 5.0%. Specialty sales grew 5.3% over the same period.

Scentre Group reported Q1 2026 business partner sales of $7.0 billion, a figure that reflects both foot traffic recovery and tenant revenue momentum across its Westfield portfolio.

Vicinity Centres posted retail sales growth of 4.5% in H1 FY26 and 3.4% in Q3 FY26 (to 5 May 2026). National retail sales rose 5% year-on-year in January 2026, providing a supportive macro backdrop.

- SCG customer visitation: up 3.1%, to 160 million visits

- SCG business partner sales: up 5.0%, to $7.0 billion (Q1 2026)

- SCG specialty sales: up 5.3% (Q1 2026)

- VCX retail sales: up 4.5% (H1 FY26); 3.4% (Q3 FY26)

The KPMG Australian Retail Outlook 2026 characterises the environment as one of gradual recovery supported by easing cost-of-living pressures. This consumer picture matters to REIT investors for a specific reason: tenant financial health underpins rent-paying capacity. A retailer with growing sales is a tenant with strong incentive to renew at positive spreads, which closes the loop back to the occupancy and leasing dynamics established above.

Why office and industrial peers are facing a different reality

Dexus’s explicit acknowledgement of delayed recovery reflects a fundamentally different demand dynamic. Office supply exceeds demand in multiple Australian CBD markets, and vacancy rates remain elevated. Retail, by contrast, operates from a position where vacancy is effectively zero. The two sub-sectors are absorbing the same macro environment from opposite structural positions.

Australian CBD office vacancy rates remained elevated in early 2026, with national vacancy reported above 15%, a structural overhang that places office landlords in a fundamentally weaker negotiating position than retail peers who are operating at effectively zero vacancy.

Three factors separate retail REIT positioning from that of its peers:

- Demand dynamics: Retail REITs benefit from consumer spending recovery and foot traffic growth; office REITs face structural work-from-home headwinds that have not fully resolved

- Supply conditions: Retail space at premium centres is undersupplied relative to tenant demand; office and some industrial markets carry excess supply or face new development competition

- Rate sensitivity management: Retail REITs like VCX have actively hedged interest rate exposure, with VCX maintaining an average hedge ratio of 89% on drawn debt for FY2026

Rate sensitivity and how retail REITs are managing it

Rising bond yields create valuation headwinds for all REITs by lifting the discount rate applied to future income streams. Industrial and data centre REITs, while positioned differently from office, face an environment where higher risk-free rates compress the yield spread advantage they previously enjoyed.

Vicinity Centres addresses this with an 89% interest rate hedge ratio on drawn debt, a mechanism that insulates near-term earnings from short-term rate movements. Its S&P ‘A’ credit rating, affirmed on 31 March 2026 with a stable outlook, provides access to capital markets at competitive rates. These balance sheet characteristics do not eliminate rate sensitivity, but they substantially reduce its impact on forward earnings.

Interest rate hedge structures vary significantly across the A-REIT universe: Waypoint REIT, for instance, maintains 90% hedge cover for FY26 alongside gearing below its target range, a comparable approach to VCX that illustrates how income-focused landlords across different sub-sectors are managing the same rate environment from different asset and lease bases.

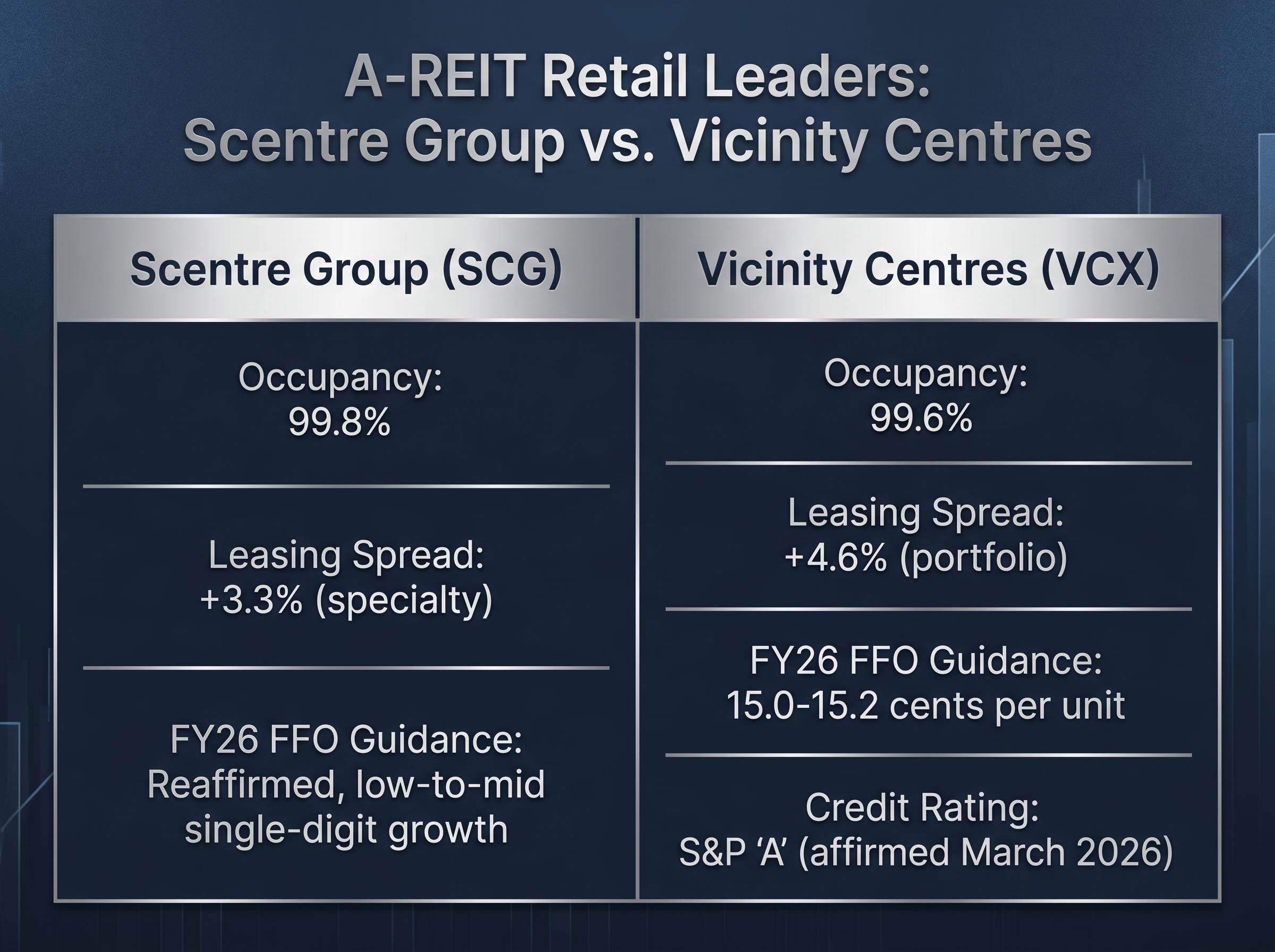

How Vicinity Centres and Scentre Group compare as investment propositions

Both companies are guiding to low-to-mid single-digit FFO per security growth for FY26, but they arrive at that guidance through different strengths.

Scentre Group reaffirmed its FY26 FFO guidance following its Q1 2026 operating update on 22 April 2026. The company settled the 19.9% divestment of Westfield Sydney for $864 million in Q1 2026, redeemed US$750 million in senior bonds, and issued a $750 million 6-year senior note at a 1.20% margin. SCG holds a structural advantage in tenant productivity and pipeline quality.

Vicinity Centres offers a conservative balance sheet anchored by its S&P ‘A’ credit rating, affirmed 31 March 2026. Portfolio leasing spreads of +4.6% in H1 FY26 demonstrate pricing power, and the 89% hedge ratio provides near-term earnings insulation.

| Metric | Scentre Group (SCG) | Vicinity Centres (VCX) |

|---|---|---|

| Occupancy | 99.8% | 99.6% |

| Leasing Spread | +3.3% (specialty) | +4.6% (portfolio) |

| FFO Guidance (FY26) | Reaffirmed, low-to-mid single-digit growth | Top of 15.0-15.2 cps range |

| Credit Rating | Conservative balance sheet | S&P ‘A’ (affirmed March 2026) |

| Analyst Consensus | N/A (current period) | 5 Buy, 7 Hold, 3 Sell |

VCX analyst consensus: Average price target of AU$2.51, with a split of 5 Buy, 7 Hold, 3 Sell. Next earnings update scheduled for 24 August 2026.

The two companies are complementary rather than competing propositions. SCG offers exposure to premium tenant productivity and active capital management. VCX offers a credit-rated balance sheet with strong leasing momentum. For investors deciding between the two or weighting their exposure, the different risk and quality profiles provide the framework for that decision.

The forward picture for retail REITs as rates and consumers evolve

The operational strength documented above is present-tense evidence. Whether it extends depends on two variables and one protective mechanism:

- RBA rate trajectory: The RBA monetary policy decision was scheduled for 2:30 pm AEST on 5 May 2026. Rate decisions remain a swing factor for REIT valuations even where earnings are hedged, because they influence investor discount rates and capital flows into the sector.

- Consumer spending durability: The KPMG outlook characterises 2026 as a gradual recovery supported by easing cost-of-living pressures. A sharper-than-expected consumer slowdown would eventually feed through to tenant sales and, with a lag, to leasing spreads at renewal.

- Hedge ratios as near-term protection: VCX’s 89% hedge ratio insulates earnings from short-term rate movements, buying time even if the rate environment turns less favourable.

Consumer spending durability is the variable that most directly connects macro conditions to retail REIT tenant health: per capita GDP growth of only 0.4% in Q4 2025 and corporate insolvencies at record highs suggest the gradual recovery characterised by KPMG may be less assured than headline figures imply, particularly for discretionary retailers that anchor major shopping centres.

The RBA May 2026 Statement on Monetary Policy sets out the central bank’s current assessment of inflation, economic conditions, and the rate trajectory, all of which feed directly into the discount rate assumptions investors apply when valuing income-producing property assets like A-REITs.

Both VCX (FFO guidance toward the top of the 15.0-15.2 cents per unit range) and SCG (FY26 FFO guidance reaffirmed following Q1 operational outperformance) have positioned their earnings outlook to absorb moderate headwinds. The risk is not that the thesis breaks tomorrow. The risk is that a sustained shift in either variable erodes the conditions that currently support near-full occupancy and positive spreads.

Retail REITs as the clearest value proposition in Australian listed property right now

Retail REITs are outperforming because their operational fundamentals, occupancy, spreads, and sales growth, are structurally stronger than peers. Scentre Group at 99.8% occupancy and Vicinity Centres at 99.6% are not riding sentiment or momentum. They are generating compounding rental income from centres where tenants are growing sales and renewing leases at above-inflation rates.

The investor action here is a sub-sector tilt decision, not a binary call on Australian real estate. In a market where Dexus is flagging delayed recovery and the broader ASX Real Estate sector faces bond yield headwinds, the combination of near-full occupancy, positive leasing spreads, and reaffirmed FFO guidance represents a rare alignment of quality signals within listed property.

Capital rotation within Australian portfolios is accelerating beyond individual stock selection: the Australian ETF market is tracking toward $380 billion as retail investors shift toward international diversification, a trend that creates a structural question about whether domestic A-REIT allocations benefit from or compete against the broader move away from purely domestic equity exposure.

VCX’s next earnings update on 24 August 2026 will be the next data point for tracking whether this operational strength is maintained. Until then, the evidence supports a clear reading: within Australian listed property, the retail sub-sector is where the fundamentals are strongest.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.