Morgan Stanley Rules Out Fed Hikes, Names Two Numbers to Watch

11 mins ago

The ASX 200 is sitting at a one-month low with fewer than 30 minutes until the most consequential domestic rate decision of the year, and the market is not hiding its nerves. At midday AEST on Tuesday 5 May 2026, the benchmark index is down 52 points (0.60%) to approximately 8,697, weighed by weakness across Financials, Materials, Industrials, and Real Estate. The RBA Board is set to deliver its cash rate decision at 2:30 pm AEST, with futures markets pricing a 25-basis-point hike to 4.35% at roughly 62-76% probability. Brent crude trading around US$113-116 per barrel is adding a separate layer of pressure. This midday wrap covers the state of play across the index, the sectors driving gains and losses, the day’s biggest individual movers, corporate announcements including Westpac’s half-year result, Macquarie Conference highlights, and a full summary of broker rating changes issued this morning.

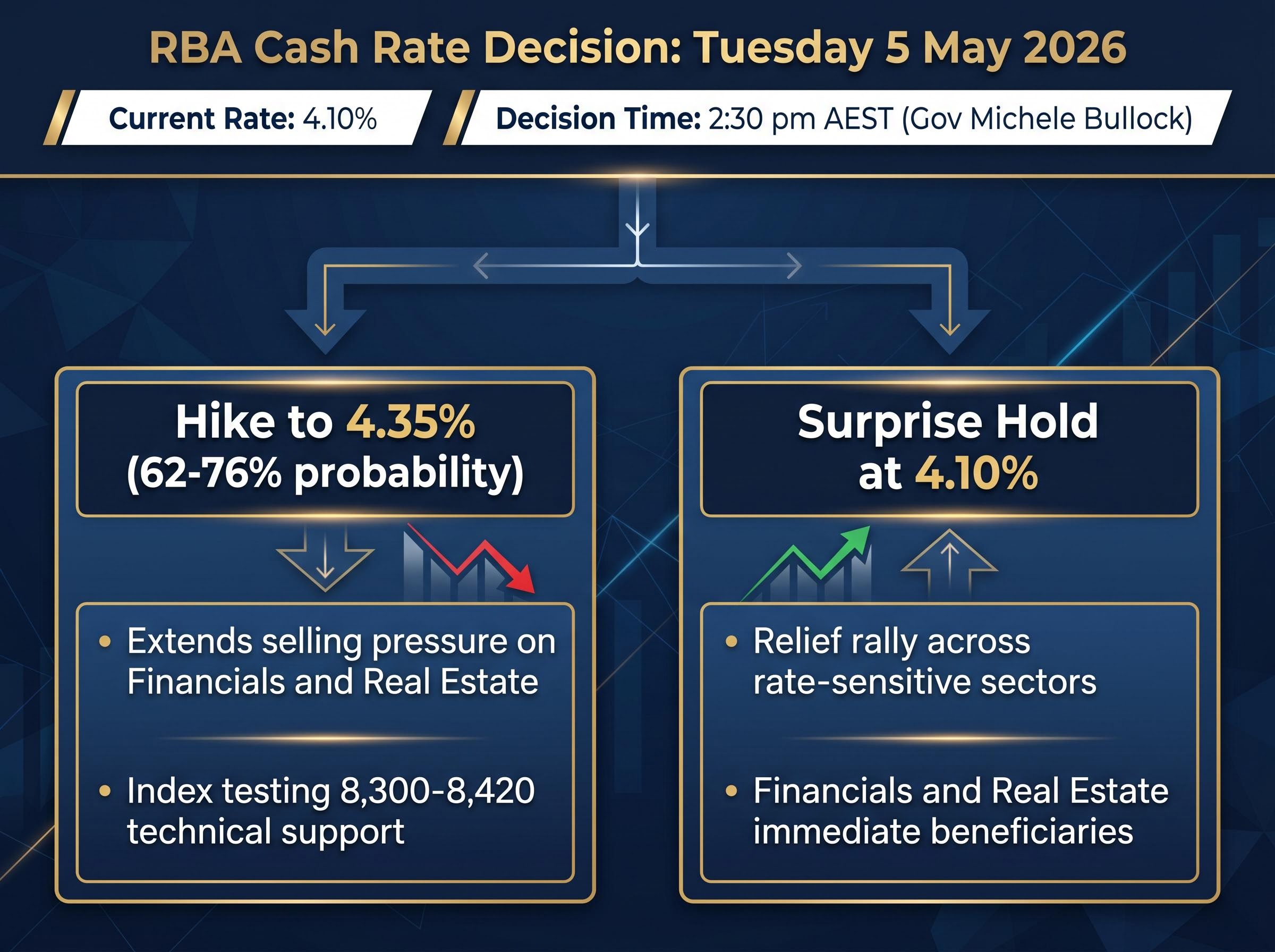

The RBA’s cash rate sits at 4.10%. By 2:30 pm AEST, Governor Michele Bullock will announce whether it stays there or rises to 4.35%. ASX 30-Day Interbank Cash Rate Futures are trading at 95.74, implying a yield of approximately 4.26%, which places the probability of a hike in the 62-76% range.

Futures-implied probability of a hike to 4.35%: approximately 62-76%, meaningful but not a foregone conclusion.

That probability is high enough that markets have already repositioned for pain, but low enough that a surprise hold would catch sellers offside. The RBA’s posture itself is a source of unease; while central banks in several other jurisdictions have begun moving toward easing, Australia’s inflation dynamics are keeping hike risk alive.

The two scenarios for the afternoon session:

The ASX 200 is trading at approximately 8,697-8,710, down 0.60% at midday AEST. The index has now declined in 13 of the prior 14 trading sessions, breaching the 30 April low and sitting beneath the 200-day moving average for a second consecutive session.

This is not scattered selling. The sector breakdown shows a coherent response to the macro environment.

| Sector | Direction | Primary Driver |

|---|---|---|

| Financials | Down | RBA hike risk repricing bank margins |

| Materials | Down | Elevated US bond yields from energy price pressure |

| Real Estate | Down | Higher bond yields compressing valuations |

| Technology | Up | Overnight Nasdaq software stock rebound |

| Energy | Up | Crude oil up approximately 4% overnight |

Financials are absorbing the most direct pressure from hike expectations, while Materials softness reflects the flow-through from elevated US bond yields tied to energy-driven inflation concerns. Real Estate and Industrials face the same yield headwind.

Technology is the session’s relative bright spot, benefiting from an overnight Nasdaq rebound in software stocks. Wisetech Global (WTC) is up 2.53% to $45.73 at midday, catching that flow-through. Energy stocks are finding support from crude oil’s approximately 4% overnight surge, with Brent at US$113-116 per barrel. The irony is that the same elevated oil prices supporting the Energy sector are feeding the bond yield pressure weighing on everything else.

The ASX energy sector rotation playing out in today’s session, where Brent crude near US$113-116 is lifting energy producers while simultaneously feeding the bond yield pressure that weighs on Financials, Real Estate, and Materials, reflects a dynamic that has been building since crude broke through US$110 and forced investors to reposition across the index.

The RBA cash rate is the interest rate the Reserve Bank of Australia charges on overnight loans between commercial banks. It functions as the baseline cost of money in the Australian economy.

The RBA cash rate target mechanism sets the interest rate on overnight loans in the money market, with the Reserve Bank using open market operations to keep the actual overnight rate trading close to the announced target.

The transmission chain works in three steps:

Each 25-basis-point move in the cash rate can shift equity valuations across entire sectors simultaneously, because higher rates raise the discount rate applied to future corporate earnings, reducing their present value today.

Rate-sensitive sectors such as Financials and Real Estate feel this most acutely. Banks face higher funding costs that compress margins, while property valuations are directly tied to discount rates.

The current 4.10% rate is elevated relative to the post-GFC decade of near-zero settings. Each incremental move carries outsized significance precisely because borrowers and businesses are already stretched. Brent crude at US$113-116 per barrel is feeding into inflation readings that complicate any pivot toward easing, which is why the market is braced for a hike rather than relief.

The headline versus underlying inflation divergence, with Australia’s CPI printing at 4.6% while the RBA’s preferred trimmed mean held at 3.3%, is the analytical lens that explains why the rate decision today is genuinely contested: a central bank that responded only to the headline figure would hike aggressively, while one focused solely on trimmed mean might hold, and the RBA is navigating both simultaneously.

Five corporate announcements are shaping individual stock moves today:

Westpac released its H1 FY26 result this morning and the numbers disappointed. Cash earnings and net interest margin came in below expectations, with elevated impairments and an energy sector provision overlay cited as the primary drags. Shares are trading around $38.50. The result reinforces the margin pressure narrative confronting Australian banks ahead of a potential rate hike this afternoon.

Regis Resources and Vault Minerals announced a merger of equals that would create a combined entity producing in excess of 700,000 ounces of gold annually, a significant consolidation move in domestic gold production.

The Lottery Corporation secured a 40-year Victorian licence extension for a premium of $1.15 billion. The market is rewarding the certainty: TLC shares are up 2.62% to $5.68 at midday.

| Stock (Code) | Change (%) | Price | Direction | Catalyst |

|---|---|---|---|---|

| Pinnacle Investment (PNI) | +6.15% | $16.14 | Gainer | Acquired additional 6.8% Metrics stake for $100.5M |

| Wisetech Global (WTC) | +5.70% | $45.73 | Gainer | Guidance reaffirmed; AI adoption highlighted at conference |

| Droneshield (DRO) | +3.49% | $3.86 | Gainer | Defence sector momentum |

| Capricorn Metals (CMM) | +3.22% | $12.04 | Gainer | Gold sector strength |

| Nine Entertainment (NEC) | +3.20% | — | Gainer | Strong Q3 revenue; Q4 ad market uncertainty flagged |

| Magellan Financial (MFG) | -6.11% | $9.52 | Loser | Global equities fund wind-up announced |

| Codan (CDA) | -5.20% | $39.77 | Loser | Profit-taking |

| Regis Healthcare (REG) | -4.99% | $6.48 | Loser | Rate sensitivity and sector rotation |

| Dexus (DXS) | -2.80% | $6.09 | Loser | Macro headwinds delaying portfolio recovery |

Pinnacle Investment Management (PNI) is the day’s standout, surging 6.15% to $16.14 after announcing its acquisition of an additional 6.8% equity stake in Metrics for $100.5 million. The market read the deal as strategically positive, deepening Pinnacle’s exposure to private credit.

Magellan Financial Group (MFG) sits at the other end, falling 6.11% to $9.52 after announcing the wind-up of its global equities fund. For a funds management business, voluntarily closing a flagship product signals a fundamental reassessment of its investment strategy.

The Macquarie Australia Conference opened today with a common theme: most presenting companies reaffirmed guidance, but several flagged sensitivity to macroeconomic conditions, particularly interest rates and fuel costs.

Judo Capital provided a credit quality update noting that a borrower-by-borrower review showed no measurable shift in risk profile, though an economic overlay provision was added for agriculture, construction, retail, manufacturing, and transport sectors. Medibank maintained its FY26 outlook unchanged. Sigma Healthcare highlighted positive Chemist Warehouse integration momentum and confirmed a UK market entry via joint venture.

Accent Group (AX1) is the most heavily revised name on broker desks this morning. Citi downgraded to neutral and cut its target from $1.25 to $0.57, a 54% reduction that signals a fundamental reassessment rather than a modest trim. Four other brokers followed with sharp target reductions.

| Stock (Code) | Broker | Action | New Target | Old Target |

|---|---|---|---|---|

| Accent Group (AX1) | Citi | Downgrade to neutral | $0.57 | $1.25 |

| Accent Group (AX1) | CLSA | Hold | $0.50 | $0.80 |

| Accent Group (AX1) | Jarden | Neutral | $0.70 | $1.20 |

| Accent Group (AX1) | Morgan Stanley | Underweight | $0.55 | $1.04 |

| Accent Group (AX1) | RBC | Sector perform | $0.80 | $1.30 |

| Sonic Healthcare (SHL) | Morgan Stanley | Downgrade to underweight | $20.30 | $24.20 |

| Endeavour Group (EDV) | JPMorgan | Downgrade to underweight | $3.10 | $3.50 |

| Coles Group (COL) | Bell Potter | Downgrade to hold | $22.80 | $22.35 |

| PEXA Group (PXA) | Jarden | Downgrade to underweight | $11.35 | $12.40 |

| NAB (NAB) | E&P | Upgrade to neutral | $38.00 | — |

| NAB (NAB) | Morgans | Upgrade to trim | $36.10 | $34.56 |

| NAB (NAB) | UBS | Retained buy | $48.50 | $50.50 |

| Ventia Services (VNT) | CLSA | Upgrade to outperform | $6.20 | $6.00 |

| Sigma Healthcare (SIG) | JPMorgan | Retained overweight | $3.50 | $3.40 |

| PEXA Group (PXA) | Macquarie | Retained outperform | $19.05 | $18.35 |

National Australia Bank (NAB) received two upgrades: E&P lifted its rating to neutral with a $38.00 target, and Morgans upgraded to trim with a target of $36.10, up from $34.56. UBS maintained its buy rating on NAB, albeit trimming the target from $50.50 to $48.50.

Ventia Services Group (VNT) was upgraded to outperform by CLSA with a target of $6.20. Sigma Healthcare maintained positive ratings across multiple brokers, with JPMorgan lifting its target to $3.50 from $3.40 while retaining an overweight stance.

Morgans’ simultaneous sell ratings across the major banks, issued before Westpac’s H1 FY26 result today confirmed elevated credit impairment charges and margin compression, sit alongside E&P and Morgans’ own upgrade of NAB this morning — a divergence that illustrates how broker views on the sector are splitting sharply along individual bank fundamentals rather than treating the four names as a monolith.

The afternoon session reduces to a single variable. At 2:30 pm AEST, Governor Michele Bullock will deliver the RBA’s decision and statement.

The two scenarios remain clearly defined:

The 2:30 pm AEST RBA announcement is the definitive afternoon pivot point. Every sector and individual stock move from that moment will be read through the lens of the rate outcome.

Global conditions are not offering support. US equity futures are modestly negative at approximately minus 0.3% at midday AEST, and European markets are broadly flat. The RBA outcome is the dominant variable.

A market already at a one-month low is waiting on a binary decision that will define the afternoon session and potentially the week’s direction. Beneath the macro tension, the fundamental news flow remains active: Westpac’s earnings miss, Pinnacle’s surge on its Metrics stake acquisition, Magellan’s fund wind-up, Macquarie Conference updates, and the coordinated broker cuts to Accent Group are all repricing individual names on their own merits.

ASX earnings season stress signals are accumulating across unrelated sectors simultaneously: Westpac’s elevated impairment charges today, the coordinated Accent Group broker downgrades, and NAB’s earlier surge in credit impairment charges beneath a headline earnings beat all point to a corporate earnings environment where the surface numbers are concealing the direction of underlying credit quality and margin pressure.

The next scheduled catalyst is the 2:30 pm AEST RBA announcement and Governor Bullock’s accompanying statement. Financials and Real Estate are the sectors to watch for the immediate post-decision reaction.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The RBA cash rate is the interest rate the Reserve Bank of Australia charges on overnight loans between commercial banks, setting the baseline cost of money in the economy. When the RBA raises this rate, borrowing costs rise across the economy, which compresses bank margins, reduces property valuations, and lowers the present value of future corporate earnings, putting broad pressure on ASX-listed stocks.

The ASX 200 fell approximately 52 points (0.60%) to around 8,697 at midday AEST on 5 May 2026, hitting a one-month low as markets braced for the RBA's cash rate decision at 2:30 pm AEST. The index had declined in 13 of the prior 14 trading sessions, with Financials, Materials, Real Estate, and Industrials leading losses.

Westpac's H1 FY26 result disappointed the market, with cash earnings and net interest margin both coming in below expectations. Elevated impairments and an energy sector provision overlay were cited as the primary drags, reinforcing the margin pressure narrative confronting Australian banks.

Pinnacle Investment Management surged 6.15% after acquiring an additional 6.8% stake in Metrics for $100.5 million, while Wisetech Global rose 5.70% on reaffirmed guidance. On the downside, Magellan Financial fell 6.11% after announcing the wind-up of its global equities fund, and Accent Group was heavily downgraded by multiple brokers including Citi, which cut its target by 54%.

According to the article, a confirmed hike to 4.35% would likely extend selling pressure on rate-sensitive Financials and Real Estate, potentially pushing the index toward technical support in the 8,300-8,420 range. A surprise hold at 4.10% could trigger a relief rally in those same sectors as traders unwind short positioning.