The S&P/ASX 200 slipped 0.65% in the week ending 1 May 2026 and sits roughly flat for the year. Beneath that calm surface, the divergence is anything but flat. Twenty-two constituents touched fresh 52-week lows across the week, concentrated in Consumer Discretionary and Health Care. Eleven moved in the opposite direction, reaching new annual highs, with three lithium names posting one-year gains that would look extraordinary in any market environment: Liontown Resources up 412.6%, Pilbara Minerals up 314.86%, and Mineral Resources up 209.42%. This analysis maps which ASX 200 stocks hit new annual highs, what commodity and macro forces are driving them, how the sector distribution of highs and lows reveals a rotation already underway, and what the signal means for investors navigating a market still short of a breakout.

The 11 stocks that bucked the ASX 200’s weakening breadth

The index barely moved. The stocks underneath it moved violently in opposite directions.

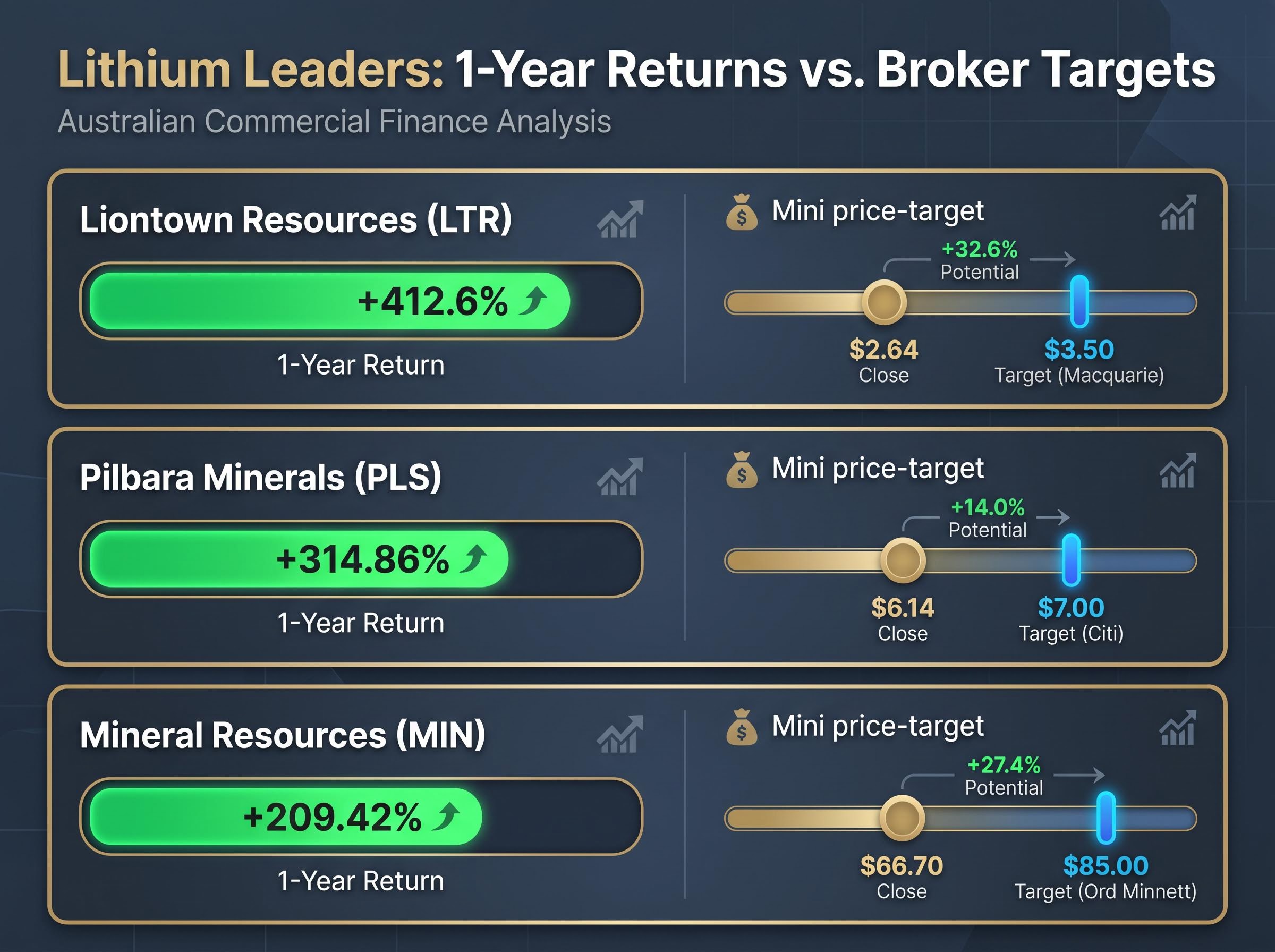

Liontown Resources (LTR) delivered a one-year return of +412.6%, the largest annual gain among all ASX 200 constituents reaching fresh 52-week highs in the week ending 1 May 2026.

Eleven names reached new annual highs across the week. Three Materials stocks with triple-digit annual returns dominated the list, but the full field spans Technology, Energy, Utilities, and one Consumer Discretionary name. The range matters: this is not a single-commodity phenomenon.

Two names on the list, Predictive Discovery and Karoon Energy, reached their annual highs during the week but finished lower on a closing basis, down 4.7% and 3.1% respectively. That distinction sharpens the picture. Intraweek highs followed by weekly losses suggest distribution at elevated prices rather than clean breakout momentum.

| Company (Ticker, Sector) | Close Price | Weekly Return | One-Year Return |

|---|---|---|---|

| Liontown Resources (LTR, Materials) | $2.64 | +17.9% | +412.6% |

| Pilbara Minerals (PLS, Materials) | $6.14 | +6.4% | +314.86% |

| Mineral Resources (MIN, Materials) | $66.70 | +12.4% | +209.42% |

| Codan (CDA, Technology) | $43.33 | +21.6% | +166.3% |

| Predictive Discovery (PDI, Materials) | $0.91 | -4.7% | +149.3% |

| Tabcorp Holdings (TAH, Consumer Discretionary) | $1.17 | +5.0% | +86.4% |

| Nickel Industries (NIC, Materials) | $1.07 | +7.0% | +79.0% |

| Karoon Energy (KAR, Energy) | $2.17 | -3.1% | +52.8% |

| Ampol (ALD, Energy) | $35.82 | +4.7% | +43.6% |

| Aurizon Holdings (AZJ, Industrials) | $4.27 | +2.2% | +42.3% |

| APA Group (APA, Utilities) | $10.50 | +3.8% | +25.6% |

For investors scanning for upward price discovery within a directionless index, these 11 names represent the specific points where momentum is trending higher rather than reverting.

When big ASX news breaks, our subscribers know first

What is powering the lithium names: commodity recovery meets Chinese EV demand

The lithium trade has a fundamental story underneath it, and that story starts at the commodity level.

Lithium carbonate spot prices averaged approximately $15,000 per tonne (lithium carbonate equivalent, or LCE) in April 2026, up 5% month-on-month. The price recovery is being supported by steady electric vehicle demand in China, where 2.1 million units were sold across Q1 2026. No major production cuts were announced during the period, meaning the price lift is demand-led rather than supply-constrained.

That commodity-level strength translated directly into institutional behaviour on 1 May 2026, when the Materials sector rallied +2.09%, leading 10 of 11 ASX sectors into positive territory. The session’s performance suggests institutional buyers returning to large miners at current valuations rather than retail-driven speculation.

Broker views and forward price targets

The three lead lithium and mining names carry broker targets meaningfully above their current share prices, which suggests the market has not yet fully priced the commodity recovery thesis:

- Liontown Resources (LTR): Macquarie rates the stock “Outperform” with a $3.50 price target, roughly 33% above the $2.64 close.

- Pilbara Minerals (PLS): Citi targets $7.00, citing the Pilgangoora expansion as the key production catalyst.

- Mineral Resources (MIN): Ord Minnett upgraded to a $85 price target, driven by iron ore strength rather than lithium, distinguishing MIN from the pure-play lithium thesis.

These targets sit at a premium to current prices across all three names. Whether the stocks close that gap depends on the same commodity fundamentals that built the rally.

What a 52-week high actually means for an ASX investor

A 52-week high is one of the most commonly screened data points in Australian retail and self-managed super fund investing. It is also one of the most frequently misread.

When a stock reaches its highest price in 12 months, every holder who purchased shares over that period is in profit. That dynamic has specific implications: selling pressure from profit-taking typically increases at annual highs, while buying pressure from breakout-chasing strategies also intensifies. The outcome depends on which force dominates.

The distinction between the two mechanisms producing a new high matters for sustainability:

- Fundamental re-rating: Earnings upgrades, commodity price recovery, or structural demand shifts push a stock to new highs because the underlying business is worth more. These highs tend to hold.

- Technical momentum breakout: Price clears a resistance level on volume and attracts short-term capital. These highs are more vulnerable to reversal if the fundamental case does not confirm.

ASX 200 RSI (14-day): approximately 46 as of 1 May 2026, indicating neutral to slightly bearish momentum on the broader index despite individual stock leadership. The index remains below the 9,230 resistance level that would confirm a bullish breakout, with support at 8,255.

The cases of Predictive Discovery (weekly return -4.7%) and Karoon Energy (weekly return -3.1%) illustrate the nuance. Both reached annual highs intraweek but closed lower, a pattern that can signal distribution, where larger holders sell into the strength of the new high. Investors using 52-week high screens as a starting point for momentum analysis should treat this pattern as a prompt for further investigation rather than automatic confirmation.

Passive flows and ASX price discovery have become increasingly entangled as ETF assets approach A$200 billion, with pod shops and quant funds amplifying intraweek moves at a level that can produce the kind of distribution pattern visible in Predictive Discovery and Karoon Energy, where stocks reach intraweek highs on institutional selling into ETF rebalancing flows before closing the week lower.

Sector rotation in plain sight: Materials and Energy lead while Financials and Health Care retreat

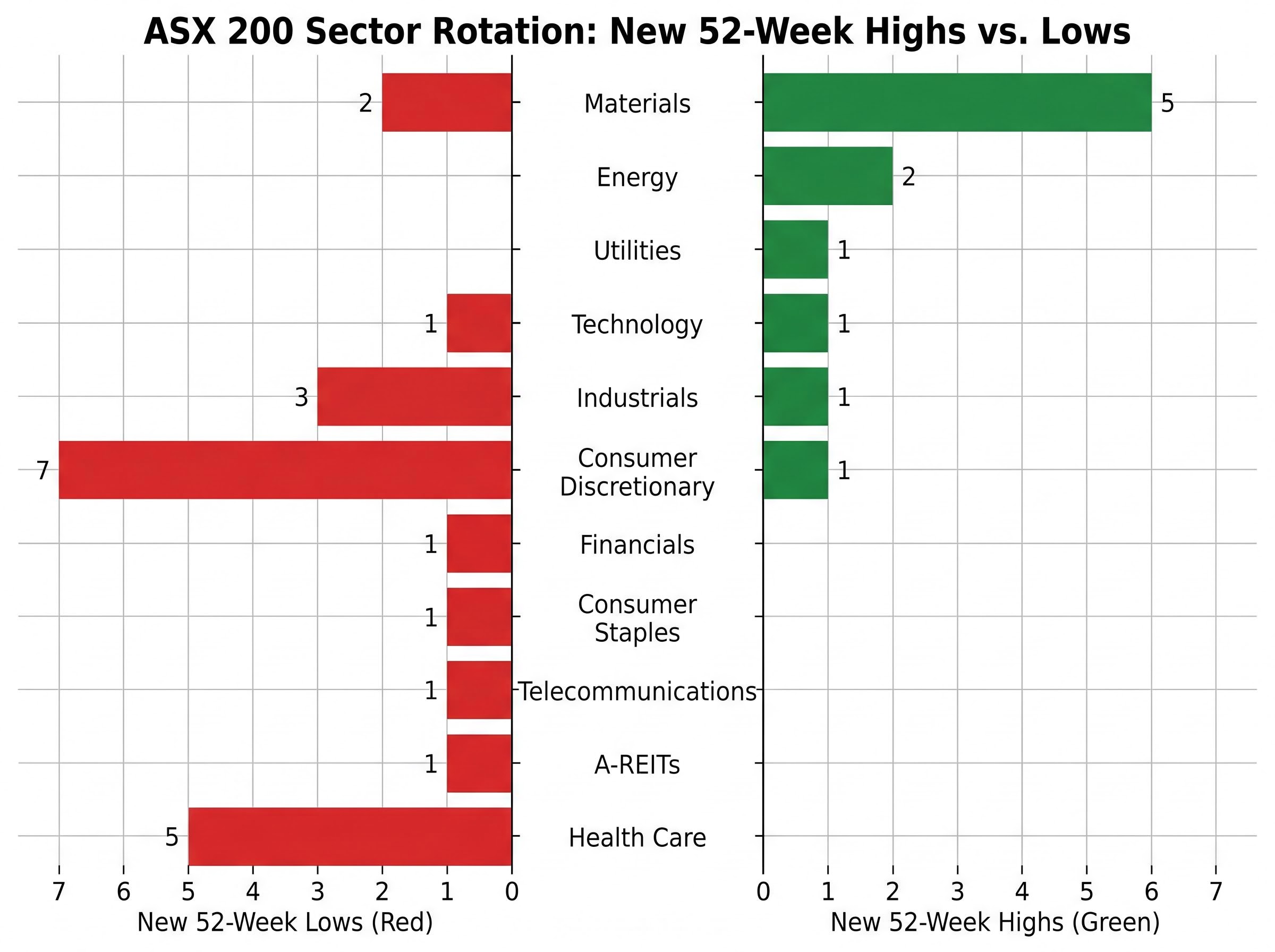

The distribution of new 52-week highs and lows across sectors maps the rotation with unusual clarity.

| Sector | New 52-Week Highs | New 52-Week Lows |

|---|---|---|

| Materials | 5 | 2 |

| Energy | 2 | 0 |

| Consumer Discretionary | 1 | 7 |

| Industrials | 1 | 3 |

| Utilities | 1 | 0 |

| Technology | 1 | 1 |

| Health Care | 0 | 5 |

| Financials | 0 | 1 |

| Consumer Staples | 0 | 1 |

| Telecommunications | 0 | 1 |

| A-REITs | 0 | 1 |

Energy produced two new highs and zero new lows. Health Care produced zero highs and five lows. Consumer Discretionary’s ratio of one high to seven lows is the week’s starkest sector-level signal.

The macro forces behind the rotation

Australia’s consumer price index rose to 4.6% in March 2026, up from 3.7% in the prior reading, pushing rate hike expectations higher ahead of the next central bank meeting. Rising inflation weighs directly on bank valuations through margin compression concerns and supports the commodities-as-inflation-hedge narrative that is channelling capital into Materials and Energy.

The ABS CPI data for March 2026 confirms the headline rate reached 4.6%, up from 3.7% in the prior reading, the official statistical basis for the rate hike expectations now pressuring domestic consumer and financial sector valuations.

On the energy side, Brent crude peaked at approximately $119-$126 per barrel in late April, driven by supply disruption fears. Thermal coal benefited as buyers sought alternatives to constrained LNG supply. Whitehaven Coal posted a +70.89% one-year return, while the S&P/ASX 200 Energy Index (XEJ) returned +48.96% over the same 12-month period.

The ASX energy sector repricing that followed Brent crude’s surge above $116 per barrel in late April created a direct transmission channel from oil markets into Australian inflation expectations, with RBC flagging headline CPI could peak at 5-6% if prices remain elevated, compressing equity multiples across rate-sensitive sectors at the same time it lifted Woodside, Santos, and Karoon.

A mild defensive tilt toward A-REITs (+1.05%) and Consumer Staples (+1.13%) on 1 May suggests cautious positioning without panic. The rotation is deliberate, not distressed.

The other side of the ledger: 22 stocks at annual lows and what they reveal

Twenty-two ASX 200 constituents hit fresh 52-week lows in the week ending 1 May 2026, roughly 11% of the index at the lower bound of its one-year range in a single week. Against 11 new highs, the two-to-one ratio of lows to highs confirms deteriorating breadth beneath a flat headline number.

April 2026 consumer confidence posted its largest monthly decline since the COVID-19 pandemic period, providing the macro backdrop for the worst-affected sector.

Consumer Discretionary accounted for seven of the 22 new lows, the heaviest concentration of any sector. The declines are severe: Temple & Webster (TPW) is down 67.9% over one year, IDP Education (IEL) down 65.2%, Flight Centre (FLT) down 19.5%, and Harvey Norman (HVN) down 15.1%. These are not shallow pullbacks from recent highs; they are sustained declines reflecting weakened consumer spending conditions.

Health Care’s five new lows tell a different story. The scale of the annual declines raises structural rather than cyclical concerns:

- Cochlear (COH): Health Care, -63.1% one-year return

- CSL (CSL): Health Care, -50.2% one-year return

- ResMed (RMD): Health Care, -23.0% one-year return

- Temple & Webster (TPW): Consumer Discretionary, -67.9% one-year return

For investors considering value plays in beaten-down sectors, the distinction between cyclical lows and structural lows is the relevant question. Consumer Discretionary names may recover with consumer confidence; Health Care names carrying multi-year growth downgrades face a longer path.

Capital rotation toward global index products is running in parallel with the domestic sector rotation this week’s data captures, with younger investors systematically moving from ASX stock selection into international ETFs targeting technology and healthcare, the same sectors that are producing the week’s worst domestic performers as offshore capital exits them.

Company-specific catalysts driving Industrials and Technology lows

Cleanaway Waste Management reduced guidance during the period, attributing the cut to Middle East-related factors affecting operations. The revision removed near-term earnings visibility at a point where the stock was already under pressure.

Orora (ORA) received a material Saverglass earnings downgrade for FY26, driven by lower volumes and an adverse product mix shift. The downgrade shifted consensus expectations meaningfully lower.

Iress (IRE) guided in late April that FY26 revenue is expected to land at the bottom of its $520-$528 million guidance range, announced on 23 April 2026.

Reading the rotation signal: what the high-and-low divergence is telling the market

The week’s data synthesises into a single rotation thesis. Institutional capital is moving out of domestic consumer exposure and growth-sensitive Health Care into commodity-linked and inflation-resistant names. The 52-week high and low distribution is the clearest weekly confirmation of that shift.

The durability of the rotation depends on three variables investors should monitor:

- Lithium carbonate prices holding above $15,000 per tonne LCE. The lithium recovery is demand-led; a slowdown in Chinese EV orders through Q2 2026 would remove the fundamental support beneath LTR, PLS, and the broader Materials leadership.

- Chinese EV demand sustaining through Q2 2026. The 2.1 million units sold in Q1 set the baseline. Seasonal Q2 strength is expected but not guaranteed amid evolving trade policy dynamics.

- Brent crude remaining elevated. Energy sector outperformance is directly tied to oil prices in the $119-$126 range; a demand-driven correction in crude would narrow the sector’s return advantage.

ASX 200 technical summary: RSI (14-day) at approximately 46 (neutral), with the 9,230 resistance level unbroken. The broader index has not confirmed the rotation with a bullish breakout.

The ASX 200’s year-to-date return remains approximately flat, with a one-year return of roughly +5.5%. The index-level RSI at 46 and the unbroken 9,230 resistance level mean the broader market has not confirmed the rotation with a directional move. For now, the divergence is a sector-level trade rather than a broad market signal. Investors who understand the rotation thesis and its conditions can position deliberately rather than chasing individual stock momentum without the macro scaffolding that supports it.

For investors wanting to build an actionable response to the macro backdrop shaping the rotation, our dedicated guide to ASX sector positioning around RBA decisions maps which sectors have historically moved first and fastest in easing cycles, why bank stocks are typically weaker short-term beneficiaries than REITs and infrastructure, and how the deposit-to-equity rotation creates a structural bid for dividend-paying names among SMSF investors.

The divergence may deepen before it resolves

Within a flat and range-bound index, 11 stocks reached annual highs and 22 reached annual lows in a single week. The divergence maps almost perfectly onto commodity exposure versus domestic consumer and growth sensitivity.

The three lithium names at the centre of the week’s signal are not noise. Liontown at +412.6%, Pilbara Minerals at +314.86%, and Mineral Resources at +209.42% over one year represent the market’s verdict on where commodity fundamentals currently sit. The question for the weeks ahead is whether the ASX 200 can clear 9,230 resistance with the same sector mix leading, or whether the rotation stalls at the index level even as individual stocks continue making highs.

+412.6%: Liontown Resources’ one-year return as of 1 May 2026, the largest annual gain among all ASX 200 constituents reaching fresh 52-week highs during the week.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.