June US Inflation Report Hits as Fed Sits 9-9 on Rate Hikes

3 hrs ago

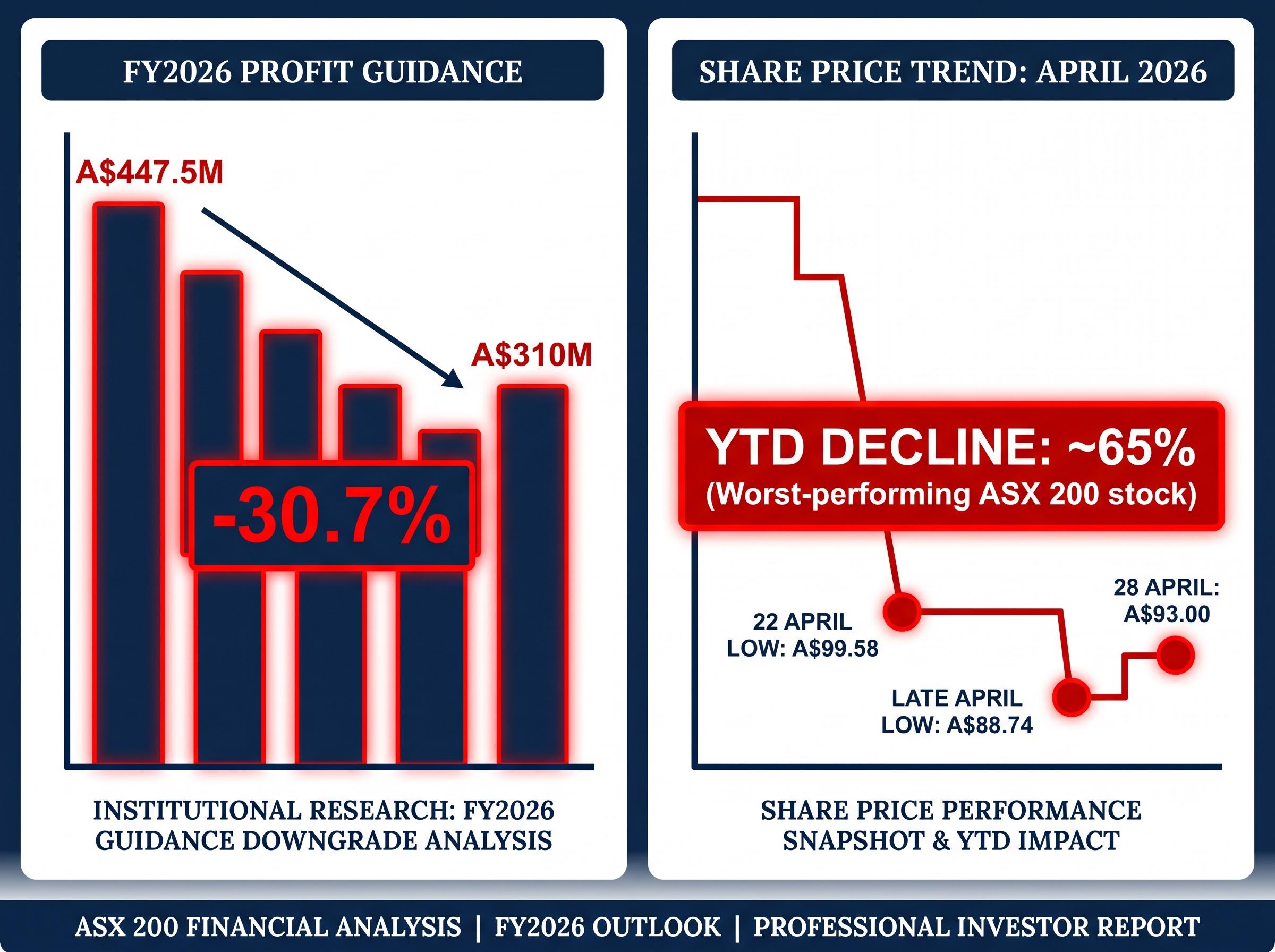

On 22 April 2026, Cochlear Ltd (ASX: COH) lost roughly 40% of its market value in a single session, printing a share price not seen since 2016 and wiping billions from investor portfolios in hours. The trigger was a guidance revision that almost no analyst had anticipated at that magnitude: FY2026 underlying net profit slashed from a midpoint of A$447.5 million to A$310 million, a cut of approximately 30.7%. The shock was not simply the number but the speed. Only weeks earlier, the first-half result had already flagged modest softness, yet the scale of deterioration between February and April blindsided the sell side.

This analysis unpacks what drove the downgrade across four geographies, why the selloff spread to CSL and the broader ASX healthcare sector, where the analyst community now stands on fair value, and what COH investors need to weigh before making any portfolio decision.

The sequence matters. On 22 April, Cochlear shares closed in a range of A$99.58 to A$106.01, with the intraday low of approximately A$99.58 marking a 10-year trough. The selling did not stop there.

By late April 2026, Cochlear’s year-to-date decline had reached approximately 65%, placing it as the worst-performing stock in the ASX 200 during the period.

A 30.7% earnings cut and a 44% share price collapse are not the same number. The gap between them is where the real damage occurred.

When a company cuts guidance by a third, the market does not simply reprice the lower earnings. It reprices the multiple it is willing to pay for those earnings simultaneously. This is earnings multiple compression: the share price falls because the earnings base drops, and the price-to-earnings ratio the market applies to that base contracts at the same time.

Earnings multiple compression operates across the broader market as well as individual stocks: with the Buffett Indicator sitting at approximately 223.6% as of May 2026 and the equity earnings yield offering thin compensation over Treasury yields, the macro environment offers institutional investors few reasons to aggressively re-rate any large-cap growth holding that has just demonstrated forecast fragility.

The distinction between an anticipated miss and a surprise miss amplifies the effect. Sell-side consensus had not positioned for a cut of this magnitude, meaning institutional portfolios were caught overweight. Forced selling from funds breaching risk thresholds, combined with a collapse in guidance credibility, pushed the share price well beyond the arithmetic of the earnings reduction alone.

Each of Cochlear’s geographic headwinds tells a structurally distinct story. Collapsing them into a single “weaker demand” narrative obscures why the downgrade was so severe: management could not offset weakness in one market with strength in another because the pressures were unrelated and simultaneous.

| Geography | Primary Driver | Nature | Status (Late April 2026) |

|---|---|---|---|

| United States | Material decline in surgical volumes from March 2026; cost-of-living pressures reducing adult and senior elective procedures | Cyclical | No stabilisation confirmed |

| Europe | Hospital capacity constraints and growing waiting lists (UK, Germany); industrial action limiting throughput (Italy, Spain) | Structural / Cyclical | Waiting lists extending |

| Middle East | Order cancellations linked to regional conflict | Geopolitical | Conflict ongoing |

| China | Reimbursement policy changes compressing pricing and volumes | Structural | Policy changes in effect |

Layered on top of these operational drivers, foreign exchange headwinds contributed an estimated A$25-30 million after-tax hit, a meaningful but secondary factor relative to the volume declines.

US consumer pressure on elective medical procedures sits within a broader pattern of savings depletion and deteriorating household financial buffers: with the US personal savings rate at 4.0% in February 2026 and mass-market spending softening beneath supportive headline retail figures, the demand headwind facing adult and senior cochlear implant candidates is not an isolated product-category phenomenon but a symptom of a wider consumption squeeze.

The services segment offered the sole confirmed bright spot. Q3 services revenue grew +13% in constant currency, driven by sound processor upgrades, accessories, and connectivity products sold to existing implant recipients. This revenue stream is recurring and less discretionary than implant surgery volumes; once a patient has a cochlear implant, the upgrade cycle is largely independent of hospital capacity or elective procedure dynamics.

The services result does not offset the scale of the implant volume decline, but it does demonstrate that Cochlear’s installed base continues to generate durable revenue even in a period of acute surgical disruption.

Cochlear manufactures cochlear implants, surgically implanted electronic devices that provide hearing to individuals with severe-to-profound hearing loss. The company holds a leading global market position, built on a proprietary sound processor ecosystem that creates a long-term recurring revenue relationship with each recipient.

Revenue falls into three categories:

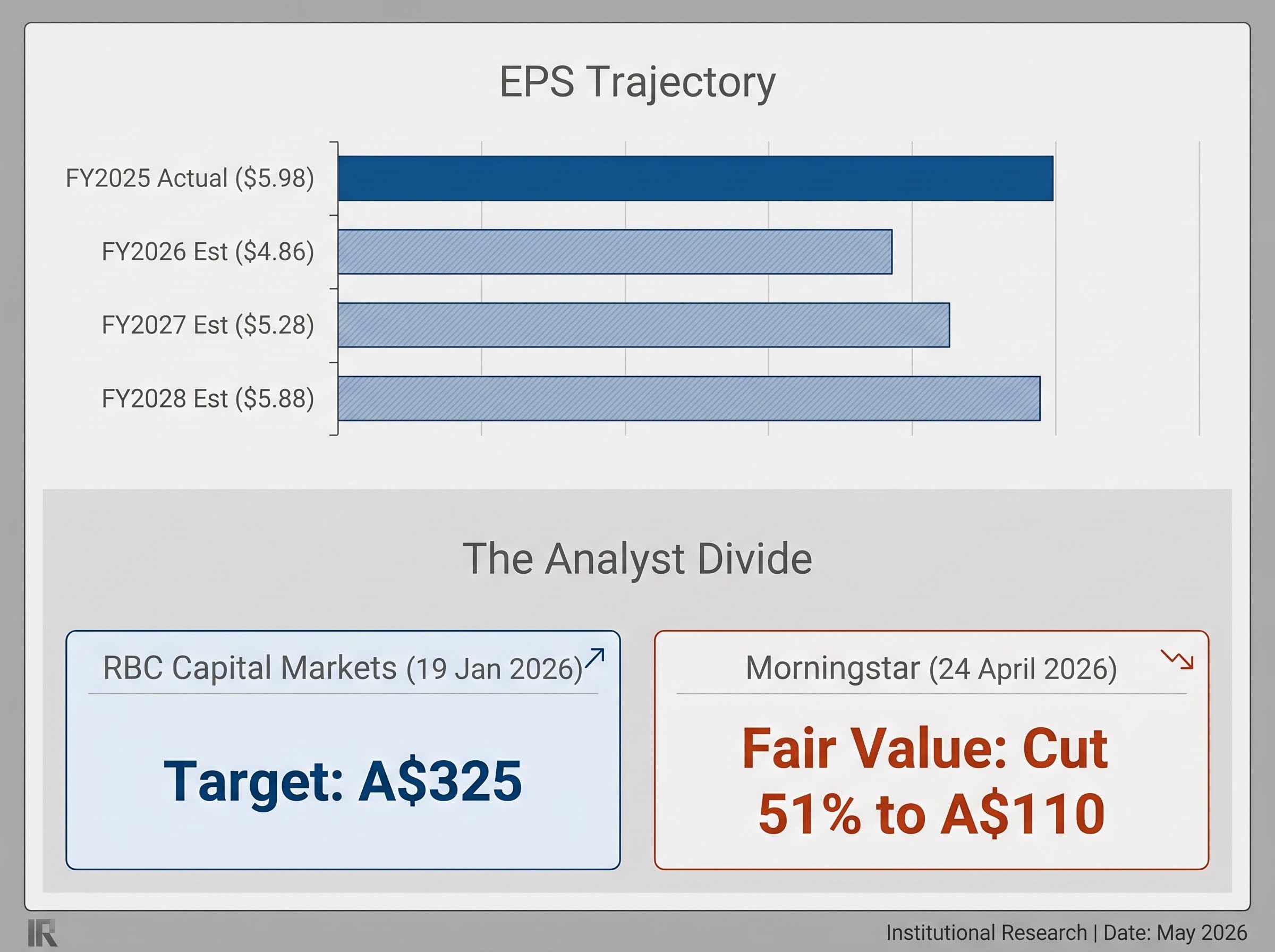

The demographic tailwind underpinning Cochlear’s long-term thesis is straightforward: ageing populations in developed markets structurally expand the addressable patient pool over decades. H1 FY2026 underlying NPAT of A$195 million, down approximately 10%, had already signalled emerging softness before the April revision. Against FY2025 actual EPS of $5.98, the trajectory was weakening before it broke.

The business quality is not in dispute. What the April event forced investors to confront is how sensitive the near-term earnings path is to hospital throughput, patient discretion, and government reimbursement policy, factors that the market had previously underweighted.

The analyst community is split, and the divide is not a matter of minor calibration. It is a genuine disagreement about whether Cochlear’s earnings capacity has been permanently reduced.

The bear case rests on three pillars:

The bull case carries its own evidence:

On 24 April 2026, Morningstar cut its fair value estimate for Cochlear by 51% to A$110, reducing its 10-year cochlear implant sales growth forecast to 5% from 6%. The severity of the revision reflected not just the earnings cut but a fundamental reassessment of the company’s medium-term growth profile.

RBC Capital Markets had upgraded Cochlear to Outperform with a price target of A$325 as recently as 19 January 2026, approximately three months before the downgrade. That target is now invalidated.

Post-downgrade consensus places FY2026 EPS at $4.86, against FY2025 actual EPS of $5.98. Directional consensus estimates point to $5.28 for FY2027 and $5.88 for FY2028, though these forward figures have not been independently confirmed and should be treated as indicative rather than settled. At sub-19x FY2026 earnings, some analysts view the stock as offering long-term value, though this valuation itself reflects the meaningful risk premium the market is demanding for forecast uncertainty.

Management’s failure to anticipate the March 2026 deterioration until April carries a specific cost: it raises the price of trusting forward guidance in the near term. Institutional buyers frequently remain on the sidelines after a guidance miss of this magnitude, regardless of whether valuation metrics appear attractive, until management demonstrates it can deliver against a revised forecast through at least one full reporting cycle.

The damage did not stay contained to one stock. CSL Ltd declined approximately 12% during April 2026, despite operating in a fundamentally different healthcare segment: plasma-derived therapies and vaccines. The business models share little operational overlap:

That CSL sold off at all, given the absence of any company-specific catalyst, illustrates the contagion mechanism at work. If a market-leading, well-managed healthcare company can miss guidance by 30% with only weeks of warning, institutional investors reprice the forecast risk across all large-cap ASX healthcare holdings. The logic is not that CSL faces the same operational headwinds as Cochlear. The logic is that the certainty premium the market had assigned to ASX healthcare earnings broadly was too high.

The broader ASX equity repricing underway in April 2026 compounded the Cochlear-specific selloff: Brent crude at $116.62 per barrel was pushing Australian CPI toward 4.6% and raising the probability of further RBA tightening, a macro configuration that increases the discount rate applied to all long-duration earnings streams and reduces the market’s appetite for any stock carrying elevated forecast uncertainty.

Cochlear was confirmed as the ASX 200’s worst-performing stock during this period. No sector-wide recovery or stabilisation data has been confirmed as of late April 2026, leaving the question of whether the healthcare repricing has further to run unanswered.

The decision confronting Cochlear investors is not a single binary choice. It breaks into three sequential questions:

The revised FY2026 guidance range of A$290-A$330 million (midpoint A$310 million) is the new earnings anchor investors must work from. Any re-entry thesis needs to start here, not from the pre-April trajectory.

The services segment and demographic tailwinds remain the two factors most likely to determine the bull case over a three-to-five year horizon. Directional consensus EPS estimates of $5.28 for FY2027 and $5.88 for FY2028 sketch a recovery path, but these figures carry considerable uncertainty given the credibility gap opened by the April revision.

Investors who entered Cochlear above A$200 face a fundamentally different calculation to those evaluating the stock for the first time at A$93. Both groups, however, need the same data to arrive at an informed decision, and that data will not arrive until August.

For investors weighing how to reposition after a repricing event of this scale, our dedicated guide to ASX portfolio rotation in 2026 covers the broader capital flows reshaping Australian retail portfolios, including the shift away from domestic defensive holdings toward global diversification strategies that has accelerated as macro volatility has increased.

Cochlear’s long-term investment thesis, built on demographic tailwinds, a durable technology moat, and recurring services revenue, remains structurally intact. What the April 2026 event permanently altered is the risk profile. Near-term implant volumes have been revealed as more discretionary and geography-dependent than the market had previously assumed, and that repricing cannot be reversed by a single quarter of stabilisation.

Global cochlear implant market forecasts published in March 2026 project sustained long-term growth through 2035, driven by rising hearing loss prevalence and ageing populations in developed markets, providing quantitative grounding for the demographic tailwind that underpins the bull case on Cochlear’s installed base expansion.

The sub-19x FY2026 earnings entry point reflects a meaningful valuation reset, but it also reflects the meaningful risk premium the market is demanding for forecast uncertainty. Morningstar’s reduced long-term growth forecast of 5% (from 6%) for cochlear implant sales over 10 years signals that even the bull case has been trimmed, not abandoned.

Recovery signposts worth monitoring in coming reporting periods include:

The directional FY2028 EPS estimate of $5.88 represents the outer bound of the consensus recovery scenario, a return to approximately FY2025 earnings levels. Whether the path to that figure is credible depends on the specific conditions above, not on sentiment or short-term price action.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections referenced in this analysis are subject to market conditions and various risk factors.

Cochlear slashed its FY2026 underlying net profit guidance by approximately 30.7%, from a midpoint of A$447.5 million to A$310 million, triggering a roughly 40% single-session collapse as markets repriced both the lower earnings base and the valuation multiple simultaneously.

Earnings multiple compression occurs when a share price falls because both the earnings base and the price-to-earnings ratio the market applies to that base contract at the same time, which is why Cochlear's share price dropped approximately 44% even though the earnings cut was around 30.7%.

The downgrade was driven by a material decline in US surgical volumes from cost-of-living pressures, European hospital capacity constraints and industrial action, Middle East order cancellations linked to regional conflict, and Chinese reimbursement policy changes compressing pricing and volumes.

Morningstar cut its fair value estimate for Cochlear by 51% to A$110 on 24 April 2026, while post-downgrade consensus places FY2026 EPS at $4.86 and the stock was trading at approximately A$93 in late April, below Morningstar's revised fair value.

Analysts are genuinely divided: the bull case rests on intact demographic tailwinds, a durable technology moat, and resilient services revenue, while the bear case centres on structural headwinds in China and Europe, a forecasting credibility gap, and simultaneous weakness across all four key geographies.