Apple just delivered the strongest quarter in its history by nearly every measure, and the stock fell anyway. That tension sits at the centre of the company’s fiscal Q2 2026 results, released on 30 April 2026: all-time records for total revenue, iPhone revenue, and diluted earnings per share, arriving ten days after a surprise CEO succession announcement rattled investors. The numbers answered questions about near-term execution. They did not answer the ones the market cares about most: whether Apple Intelligence can generate revenue at scale, what a leadership change means for competitive positioning, and whether a record quarter was already priced in. What follows is the complete picture of Apple’s earnings, from the scorecard to the stock reaction and the unresolved questions between them.

Apple’s Q2 2026 by the numbers: records across every major line

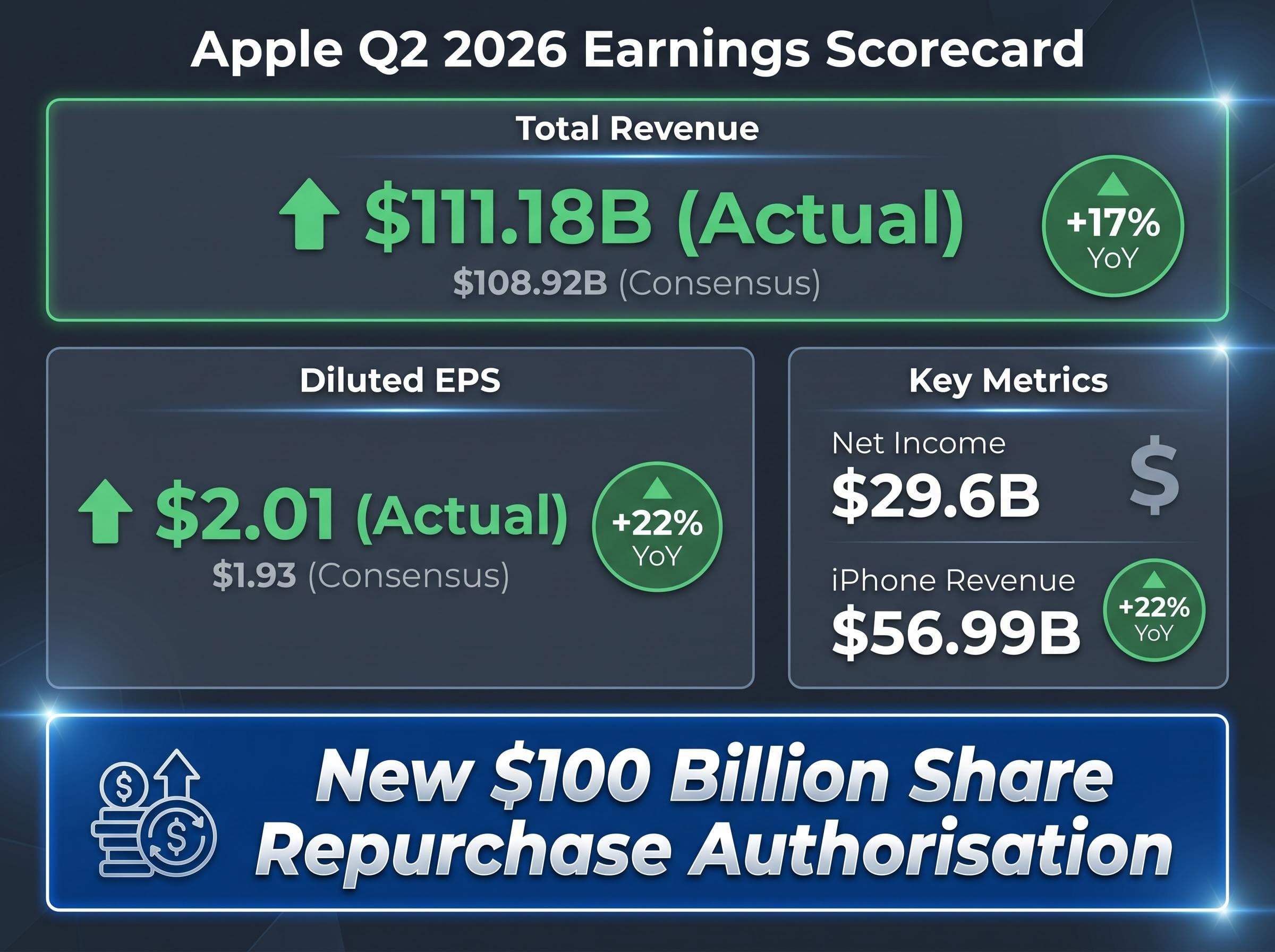

Apple reported fiscal Q2 2026 revenue of $111.18 billion, a 17% increase year over year and comfortably ahead of the $108.92 billion analyst consensus. Diluted earnings per share reached $2.01, a 22% year-over-year gain that also exceeded Wall Street expectations. Net income landed at $29.6 billion.

$2.01 per share versus the $1.93 analyst consensus, a 22% year-over-year gain.

These were not routine beats. All three headline metrics, total revenue, iPhone revenue, and diluted EPS, set simultaneous all-time company records. The board paired the results with a new $100 billion share repurchase authorisation, the largest single buyback programme in Apple’s history.

Apple’s Q2 2026 earnings release confirms the $100 billion share repurchase authorisation alongside the headline financial figures, making it the primary source for investors verifying the simultaneity of the buyback announcement and the record revenue and EPS results.

| Metric | Result | Analyst Estimate | Year-over-Year Change |

|---|---|---|---|

| Total Revenue | $111.18B | $108.92B | +17% |

| Diluted EPS | $2.01 | $1.93 | +22% |

| Net Income | $29.6B |

Every section that follows builds on this scorecard. The records are the foundation; the story is what they did and did not resolve.

When big ASX news breaks, our subscribers know first

iPhone’s historic run: how Apple claimed the global smartphone crown

Apple ranked first globally in smartphone shipments during Q1 of a calendar year for the first time on record, according to Counterpoint Research. The milestone confirmed what the revenue figures already suggested: iPhone is not simply selling well, it is outpacing every competitor at the top of the market.

Counterpoint Research global smartphone shipments data for Q1 2026 placed Apple at 21% market share, the first time the company has led calendar-year first-quarter rankings, a milestone that reinforces the structural rather than seasonal nature of the iPhone demand surge.

Three factors underpin the surge:

- Demand concentration in the iPhone 17 Pro lineup, where average selling prices are highest

- Sustained multi-quarter momentum, with the prior fiscal quarter already described as the best iPhone sales performance in over four years

- Global shipment leadership, marking a structural shift rather than a seasonal spike

iPhone revenue reached $56.99 billion in the quarter, a 22% year-over-year increase. The growth rate is significant because it is not being driven by unit volume alone. Consumer purchasing is skewing toward Pro models, which carry wider margins and deeper ecosystem integration.

What is driving iPhone demand at the high end

The Pro lineup concentration is the thread that connects the revenue beat to Apple’s broader services thesis. Higher-end devices tend to generate stronger attachment rates for subscriptions, cloud storage, and accessory ecosystems. That connection matters for the AI monetisation debate covered in the next section.

What is Apple Intelligence and why it remains the unresolved question for investors

Apple Intelligence is Apple’s suite of artificial intelligence features integrated across iPhone, iPad, and Mac. The system combines on-device processing with cloud-connected models to personalise the operating system, from writing assistance and photo editing to contextual notifications and search. In practical terms, it is Apple’s bet that AI woven into existing products will deepen ecosystem engagement rather than requiring users to adopt a standalone AI service.

The investment thesis rests on two claims:

- AI features accelerate iPhone upgrade cycles by making newer hardware functionally superior

- Deeper ecosystem engagement increases services attachment rates, expanding the company’s highest-margin revenue stream

What Apple Intelligence has not yet demonstrated:

- A verified revenue contribution directly attributable to AI features

- Regulatory clearance in all target markets, with analyst commentary flagging compliance headwinds as a risk to execution timelines

Analysts have characterised Apple Intelligence as “a key monetisation driver” for the services segment, while noting that regulatory headwinds could complicate deployment timelines.

The services segment remains a high-margin growth driver, and management cited AI integration as central to its trajectory on the earnings call. The gap between that narrative and measurable financial proof is the single largest open question heading into the next quarter.

The divergence in market reactions to AI monetisation across Big Tech became the defining story of the same earnings window: Alphabet surged more than 7% to an all-time high on 81% net income growth, while Meta fell more than 9% despite 33% revenue growth, exposing a market that is now pricing each company’s spending-to-revenue conversion speed individually rather than treating AI deployment as a single unified trade.

Cook to chairman, Ternus to CEO: reading the succession through the earnings lens

The sequencing is worth noting. Apple announced its leadership transition on approximately 20 April 2026, ten days before delivering a record quarter. That is not accidental. A blowout earnings report arriving days after a surprise succession announcement functions as a statement: the business is performing, and the handover happens from strength.

The key facts, in order:

- Leadership transition announced approximately 20 April 2026

- Effective date: 1 September 2026

- Tim Cook moves to Executive Chairman

- John Ternus becomes CEO and joins the board of directors

Analyst reception has been broadly constructive. The phrases “smooth handover” and “handover from strength” appeared across post-earnings commentary, reflecting a consensus that Cook’s tenure produced the financial foundation for the transition to proceed without operational disruption.

Measured concerns remain. Some analyst commentary flagged Apple’s AI competitive positioning under new leadership as an ongoing question, particularly given the pace at which rivals are deploying their own AI ecosystems. The earnings results partially addressed the initial investor unease that followed the surprise announcement, but the longer-term test arrives after 1 September, when Ternus takes operational control.

Tariffs, memory chips, and the supply chain risks Apple is navigating

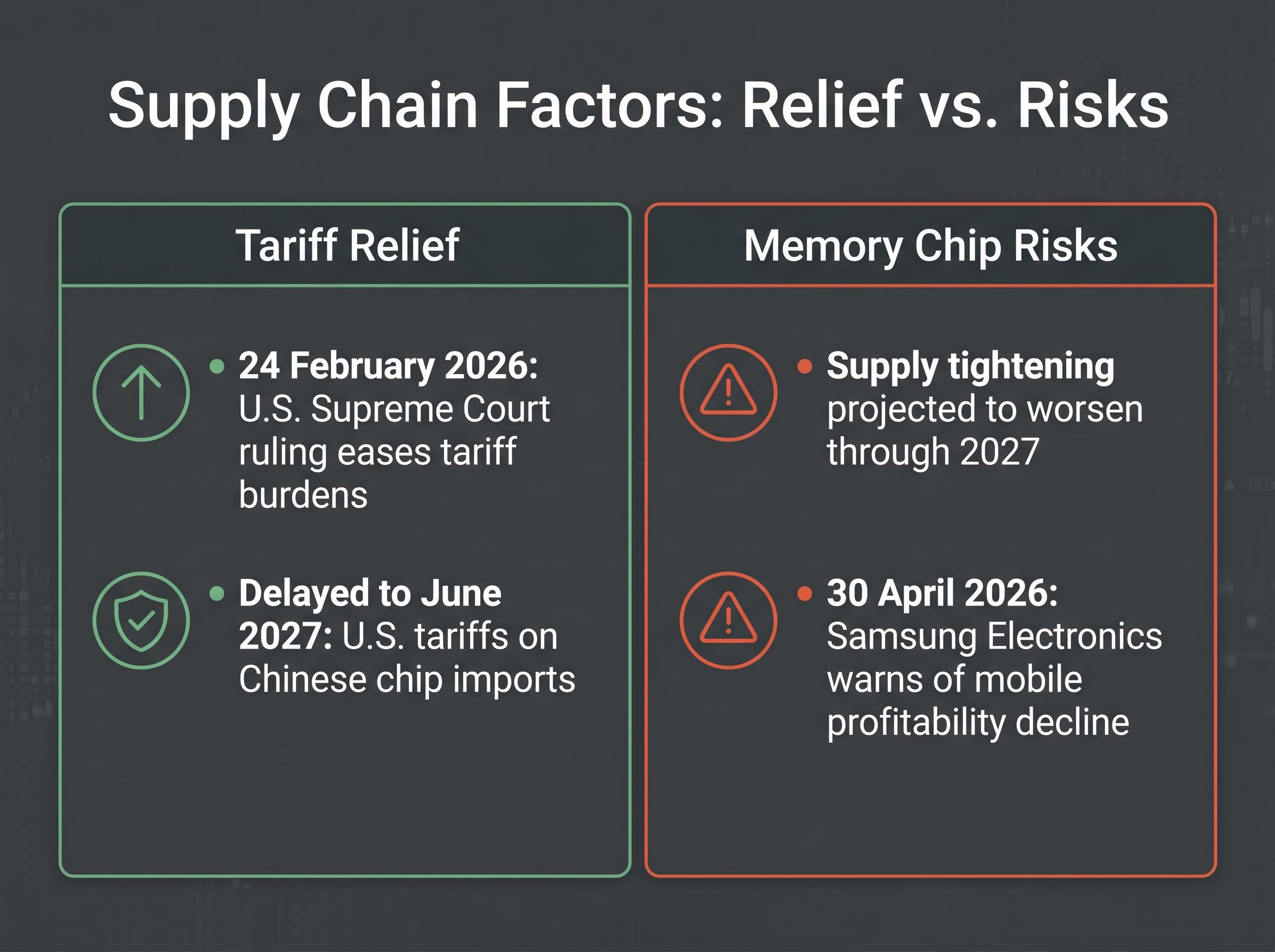

A record quarter does not exist in isolation from its supply chain. Two near-term developments reduced Apple’s worst-case tariff exposure:

- A U.S. Supreme Court ruling on 24 February 2026 eased some of Apple’s tariff burdens

- Steep U.S. tariffs on Chinese chip imports were delayed until June 2027, removing an immediate cost headwind

Two ongoing risks complicate the forward picture:

- Memory chip supply tightening across the sector, with conditions projected to worsen through 2027

- Persistent U.S.-China trade tension requiring continued supply chain diversification

Samsung Electronics warned on 30 April 2026 that its mobile division profitability is projected to decline, citing a memory supply shortage expected to worsen through 2027.

That warning arrived on the same day Apple reported earnings. Samsung’s acknowledgement of the supply constraint validates it as a sector-wide pressure rather than a company-specific concern. Management addressed the issue on the earnings call, citing supply chain resilience as a strategic priority and pointing to ongoing diversification efforts as the structural response.

Memory supply constraints are not an Apple-specific concern: the same physical bottlenecks restricting chip availability across the sector are documented across hyperscaler earnings commentary, with physical supply chain limitations, including memory shortages and grid power limits, now identified as the binding constraint on how quickly approved AI budgets can be deployed.

The stock fell on a record quarter: what the market is actually pricing in

Apple shares ticked higher in after-hours trading immediately following the 30 April release, then reversed, finishing the extended session down approximately 1.3%. On 1 May, the stock closed at $271.35, with an intraday range of $268.14 to $276.00 on volume of 91.8 million shares. After-hours trading on 1 May showed a subsequent recovery to $278.25, up $6.90 (+2.54%).

The initial selling reflected three investor concerns embedded in the reaction:

- AI monetisation timeline: Record results proved hardware and services execution but did not close the gap between AI deployment and AI revenue

- Leadership transition risk: The September handoff remains an unknown variable for long-term positioning

- Valuation: A record quarter may already have been priced into the stock ahead of the report

The $100 billion buyback authorisation serves as the board’s counter-signal, a direct statement that management views the stock as undervalued relative to its earnings power.

Q3 FY2026 gross margin guidance: 47.5-48.5%, the concrete forward indicator management offered alongside the buyback.

The post-earnings dip is not irrational. It is the market separating what the quarter proved (execution is strong, demand is real, margins are expanding) from what it did not prove (that AI will monetise, that the leadership transition will be seamless, and that there is still upside left in the valuation).

Record results, unresolved questions, and what comes next for Apple investors

Apple’s fiscal Q2 2026 confirmed that the hardware and services engine is operating at peak capacity. It did not confirm that Apple Intelligence can convert deployment into revenue, or that the transition from Cook to Ternus will proceed without strategic disruption. Three near-term milestones will shape the next chapter: Q3 FY2026 results, the deployment of the $100 billion buyback, and the 1 September CEO handoff.

The record quarter settled the execution question. It left the growth question open.

Investors exploring the bear case in more depth will find our deep-dive into AI hardware valuation risks, which examines derivative market complacency, the profitability economics of generative AI inference, and what a deceleration in hyperscaler capital deployment would mean for semiconductor valuations and the broader tech sector through 2027.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.