Thematic ETFs Returned 233%, but Investors Lost 35%

2 hrs ago

Resources and energy ETFs delivered triple-digit returns in the twelve months to early 2026. XMET, tracking energy transition metals, gained approximately 123.72%. MNRS, the currency-hedged global gold miners fund, returned approximately 100.83%. At the same time, technology-themed ETFs faced drawdowns of up to 25% as a software valuation reset worked through the sector.

The divergence is one of the sharpest sector rotation events Australian investors have experienced this decade, and it carried material consequences. The Australian ETF market now holds more than $14 billion in technology-themed products, meaning concentrated thematic positioning was not a niche problem but a widespread one. What follows examines what the 2026 rotation reveals about the structural limitations of thematic ETF investing, why diversified alternatives are designed to absorb exactly this kind of shift, and what practical options exist for investors who still want thematic exposure without bearing its full concentration risk.

The rotation arrived as a sequence, not a single event. Through the first months of 2026, capital moved decisively out of technology and software positions and into resources, energy, and commodity-linked equities. The shift was visible across both retail ETF flows and institutional positioning.

Scale of exposure: ASX-listed technology-themed ETFs collectively hold more than $14 billion in investor capital, meaning the drawdown affected a substantial cohort of Australian retail investors and growth-oriented active managers alike.

Several prominent Australian active growth managers who had accumulated software positions during the technology boom also experienced significant drawdowns, widening the rotation’s impact beyond retail ETF holders. Funds concentrated in names benefiting from AI and cloud computing themes found themselves on the wrong side of a valuation reset that adviser commentary, cited by Livewire Markets, characterised as a repricing rather than a sector collapse.

The result was a dual problem. Investors concentrated in technology-themed ETFs experienced the drawdown in their holdings and missed the resource and energy gains entirely. They did not merely underperform; they had zero participation in the sectors generating the strongest returns of the period.

| ETF Ticker | Theme | Issuer | Approx. 12-Month Return | Primary Driver |

|---|---|---|---|---|

| XMET | Energy transition metals | BetaShares | +123.72% | Clean energy infrastructure demand |

| MNRS | Global gold miners (hedged) | BetaShares | +100.83% | Central bank buying, commodity surge |

| Tech-themed ETFs | Technology / software | Various | Up to -25% | Software valuation reset |

The 2026 rotation was not a freak event. It was a symptom of a structural feature that applies to all thematic ETFs: concentration around a single investment narrative inherently excludes entire categories of the market.

A technology-themed mandate, by design, carries minimal or no exposure to:

This means a thematic ETF investor is not simply overweight one sector. They are implicitly short every sector the theme excludes. When leadership rotates, the portfolio has no mechanism to capture the new winners.

Technology-themed ETF positioning after a valuation reset carries a different risk profile than entering at peak sentiment; VTEK, which launched on the ASX in late March 2026 tracking 300 global technology companies through a capped index structure at 0.23% per annum, illustrates how within-sector concentration controls can reduce single-name risk without providing the cross-sector diversification that a broad market mandate delivers.

The deeper problem is one of expectations pricing. Chris Brycki, founder of Stockspot, has noted that when a sector is widely held and priced for strong future performance, the bar for delivering positive returns becomes extremely high. The theme itself may prove correct; the companies within it may grow revenue and expand their markets. But if the share prices already reflect that optimism, investors who bought at peak enthusiasm need the sector to exceed already-elevated expectations to generate a return.

The inverse also holds. Undervalued sectors, where expectations are modest, can deliver strong returns on only marginal improvement. This asymmetry is the mechanism that makes forecasting which theme will lead, and whether that leadership is already priced in, consistently difficult. Adviser commentary from Livewire Markets supports this framing, characterising 2026’s rotation as a valuation reset rather than a technology collapse.

Beyond market structure, there is a second cost to thematic investing that rarely appears in fund marketing: the gap between reported fund returns and the returns investors actually receive.

The distinction matters. A fund’s reported return (its time-weighted return) measures what a dollar invested at inception and left untouched would have earned. The money-weighted return measures what investors collectively experienced, accounting for the timing and size of their actual inflows and outflows. For thematic ETFs, which attract the bulk of their capital after periods of strong performance, the gap between these two figures is structurally wider than for diversified alternatives.

Morningstar’s Mind the Gap study, which tracks the difference between reported fund returns and actual investor returns across fund categories, finds the gap is consistently largest in sector and thematic equity funds, where performance chasing and peak-inflow timing are most pronounced.

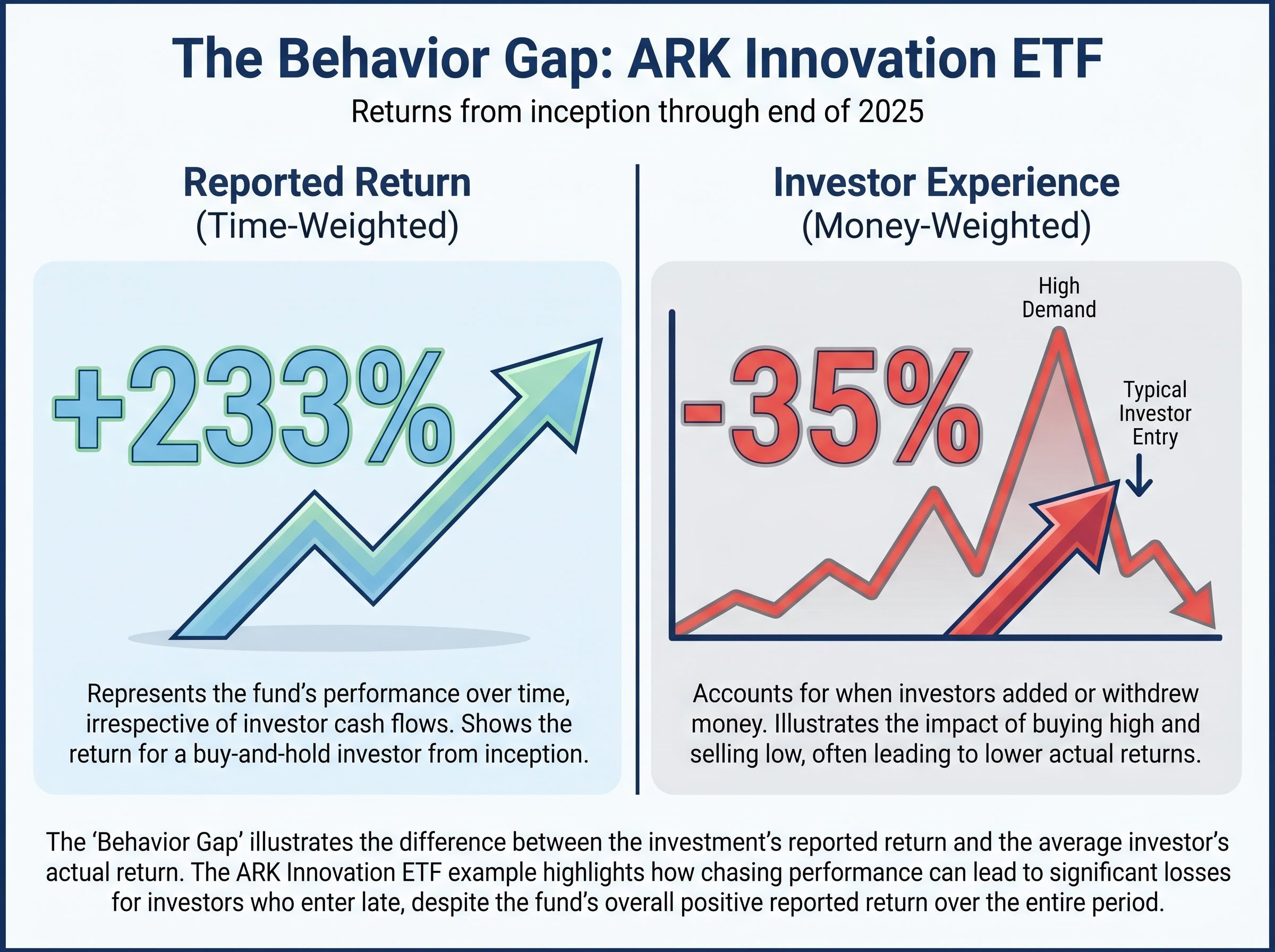

The ARK case study: ARK Innovation ETF reported a time-weighted return of approximately 233% from inception through the end of 2025, slightly exceeding the S&P 500 over the same period. The estimated money-weighted return experienced by investors was approximately negative 35%. The fund’s headline performance was strong; the typical investor lost money.

Chris Brycki’s analysis of the ARK case identifies the causal mechanism clearly. The pattern follows three steps:

The same inflow-after-peak pattern is observable in Australian thematic funds, where investor capital tends to arrive following strong performance periods. A fund can report attractive headline returns while the typical investor in that fund experiences a materially different outcome.

Diversification is not a consolation prize for investors who cannot identify winning themes. It is the only mechanism that reliably captures rotating sector leadership without requiring the investor to forecast which sector will lead next.

A broad market ETF holds exposure across technology, financials, energy, resources, and consumer sectors simultaneously. When capital rotated from technology into resources in 2026, a diversified ETF investor participated in both the resource and energy gains and retained their technology exposure for any future recovery.

Index concentration risk operates at a level that many passive investors do not fully appreciate; the Magnificent Seven group represented nearly 33.7% of the S&P 500 by April 2026, meaning that even a diversified broad market index carries meaningful single-sector exposure when the largest constituents are heavily weighted toward one industry.

A technology-themed ETF investor experienced the drawdown with no offsetting participation in the sectors delivering the strongest returns.

Market-cap-weighted broad market ETFs naturally shift their sector weightings as prices move. When energy and resource stocks rise, their weight in the index increases automatically. When technology stocks decline, their weight decreases. This rebalancing happens without requiring the investor to make active allocation decisions or timing calls. It is the specific mechanism that allows a diversified portfolio to participate in rotation passively.

Stockspot’s recommended core ETF portfolio approach reflects this diversified-first methodology in the Australian context. The broader market supports the direction: the Australian ETF industry grew 31.7% year-over-year to March 2026, with $5.6 billion in total inflows in March 2026 alone. Adviser commentary from Michael Wayne of Medallion Financial and Adam Dawes of Shaw and Partners points to selectivity and real asset exposure as the dominant investment approach expected for 2026, reinforcing the case for broad positioning over narrow thematic bets.

The Betashares Australian ETF Review for March 2026 records the industry’s 31.7% year-over-year growth and the $5.6 billion in monthly inflows, figures that contextualise just how much retail capital was concentrated in thematic products when the rotation landed.

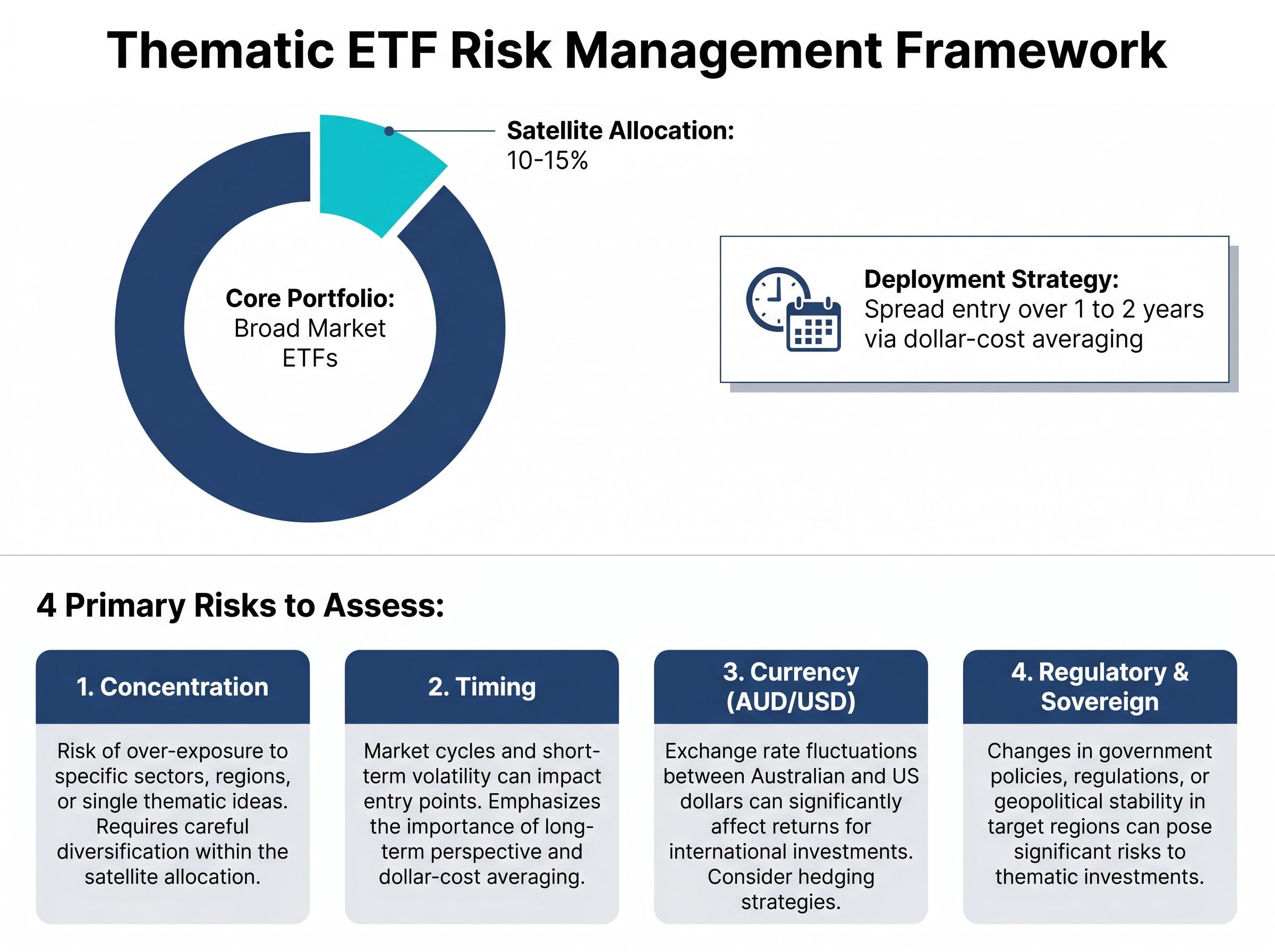

For investors who find a specific thematic ETF compelling, the following framework addresses the principal risks of timing and concentration without requiring complete avoidance of thematic exposure.

For investors who want to understand the full cost case for dollar-cost averaging before applying it to a thematic satellite position, our dedicated guide to dollar-cost averaging and reactive trading costs walks through four compounding cost mechanisms, including CGT drag, transaction costs, and opportunity cost from mis-timed exits, with hard data from Australian retail trading patterns in the March to April 2026 volatility period.

The four primary risk categories for ASX-listed thematic ETFs are:

The 2026 rotation is not an isolated event. It is an illustration of a recurring market dynamic in which leadership shifts between sectors in ways that are consistently difficult to forecast. Technology dominated equity market returns from 2020 onward, creating the conditions for the 2026 reset. This pattern of dominance followed by rotation is a historical recurring feature of equity markets, and there is no reason to expect the cycle has ended.

Adviser commentary characterises 2026 as a valuation reset rather than a structural technology decline. Technology leadership may resume, but the timing remains uncertain. The continued emphasis on selectivity and real-asset orientation across Australian advisory firms suggests the rotation may have further to run.

The appropriate response to this reality is not more sophisticated thematic selection. It is a portfolio structure that does not require correct thematic selection in the first place. The investor who holds a diversified ETF does not need to know when the next rotation will happen, which sector it will favour, or how long it will last.

As Chris Brycki’s analysis underscores, structural diversification eliminates the need to predict sector leadership. The advantage is not in better forecasting; it is in making the forecast irrelevant.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results.

Thematic ETFs concentrate their holdings around a single investment narrative or sector, such as technology or clean energy, while broad market ETFs hold exposure across multiple sectors simultaneously. This concentration means thematic ETFs have no mechanism to participate in returns from sectors outside their mandate when market leadership rotates.

Technology-themed ETFs fell by up to 25% during a software valuation reset in early 2026, while investors in those funds had zero exposure to resources and energy ETFs like XMET and MNRS, which returned 123.72% and 100.83% respectively over the same twelve-month period. Concentrated thematic positioning left investors unable to participate in the sectors generating the strongest returns.

The behaviour gap is the difference between a fund's reported time-weighted return and the money-weighted return that investors actually experience, which accounts for the timing of real inflows and outflows. Thematic ETFs are particularly prone to a wide behaviour gap because most investor capital flows in after strong performance, meaning the average investor buys near peak valuations and experiences worse returns than the fund's headline figure suggests.

Australian financial advisers generally recommend sizing thematic ETFs as satellite allocations of around 10-15% of a portfolio, with broad market ETFs forming the core foundation. Spreading entry over one to two years via dollar-cost averaging can also reduce the risk of deploying capital at peak sentiment and elevated valuations.

Market-cap-weighted broad market ETFs naturally shift their sector weightings as prices move, so when energy and resource stocks rise their index weight increases automatically and when technology stocks decline their weight decreases. This means a diversified investor participates in rotating sector leadership without needing to forecast which sector will lead next.