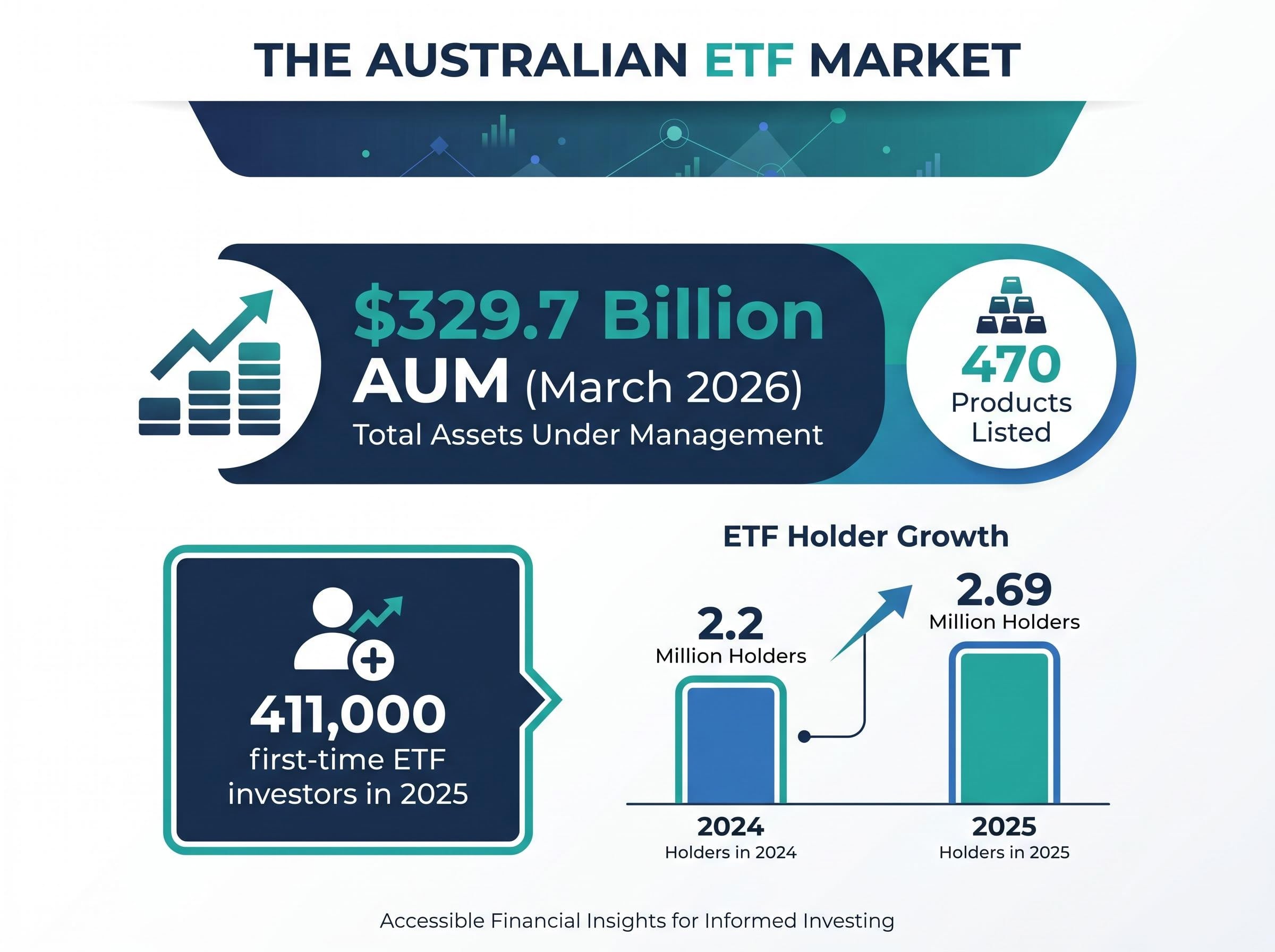

The Australian ETF market hit $329.7 billion in assets under management across approximately 470 products as of March 2026. In 2025 alone, 411,000 Australians made their first-ever ETF investment, pushing the total number of holders to 2.69 million. ETFs are no longer a niche product for self-directed traders; they have become the default entry point for Australian retail investors building long-term portfolios. Yet many buyers purchase their first ETF without understanding the structural decisions involved: which product type fits their objective, what costs are actually deducted from returns, how distributions are taxed, and whether the price on screen reflects fair value. Those gaps lead to suboptimal outcomes even with a well-chosen fund. This guide covers the full picture in one place: how ETFs work on the ASX, what types are available, how fees compare to managed funds, Australian tax treatment, investor protections, and how to execute a trade well. It is designed for first-time buyers and for investors reviewing existing holdings.

What an ETF actually is and how it works on the ASX

An exchange-traded fund is an open-ended investment fund that holds a portfolio of underlying assets and trades on a stock exchange like an ordinary share. That combination gives investors the diversification of a managed fund with the ability to buy and sell at a live market price during trading hours.

Market Scale: The Australian ETF market reached $329.7 billion in total AUM as of March 2026, with approximately 470 products listed on the ASX.

Four characteristics define the structure:

- Portfolio of underlying assets: Each ETF holds a basket of securities (shares, bonds, commodities, or other instruments) rather than a single stock

- Intraday trading: Units trade continuously on the ASX during market hours, with prices updating in real time

- NAV anchoring via authorised participants: Large institutional participants can create or redeem ETF units directly with the issuer, which keeps the market price close to the fund’s net asset value

- Open-ended structure: New units can be created and existing units redeemed as demand shifts, so the fund is not constrained by a fixed number of shares

The creation and redemption mechanism is worth understanding because it explains a structural advantage. When the market price drifts above the fund’s net asset value (NAV), authorised participants can create new units at NAV and sell them on the exchange at the higher price, pocketing the difference. When the price falls below NAV, they can buy units on market and redeem them with the issuer. This arbitrage keeps the two prices closely aligned and provides a liquidity backstop that extends well beyond what on-screen trading volume might suggest.

Investors transact at the market price, not the NAV directly. The two can diverge temporarily, particularly during the first and last minutes of the trading session when spreads widen. The ASX remains the primary exchange, though CBOE Australia also lists over 20 ETFs from 14 issuers as of 2026, which some brokers can access.

The investor base has expanded rapidly. An estimated 2.69 million Australians held ETFs as of 2025, up from approximately 2.2 million the prior year.

When big ASX news breaks, our subscribers know first

The eight main types of ETFs listed on the ASX

Eight primary categories cover the breadth of what is available to Australian investors on the ASX. The table below summarises each with a specific listed product and its management expense ratio.

| Category | Example ASX Code | Product Name | MER |

|---|---|---|---|

| Australian equities | A200 | Betashares Australia 200 ETF | 0.04% |

| International equities | NDQ | BetaShares NASDAQ 100 ETF | 0.48% |

| Fixed income | IAF | iShares Core Composite Bond ETF | 0.15% |

| Cash | BILL | iShares Core Cash ETF | 0.07% |

| Commodities / Resources | QRE | BetaShares Australian Resources Sector ETF | ~0.34% |

| Digital assets | iShares Bitcoin ETF | iShares Bitcoin ETF | See PDS |

| Diversified (multi-asset) | VGS | Vanguard MSCI Index International Shares ETF | ~0.18% |

| Property securities | VAP | Vanguard Australian Property Securities Index ETF | See PDS |

Other notable domestic equity options include IOZ (0.05%), VAS (0.07%), and A300 (0.04%). For resources, MVR (VanEck Australian Resources ETF) sits at approximately 0.34%-0.35%.

Two structural distinctions matter when navigating these categories:

- Physical ETFs hold the actual underlying securities. Most products listed on the ASX are physical. Synthetic ETFs use derivatives such as futures or swaps to replicate exposure, and Australian naming rules require the word “synthetic” to appear in parentheses in the fund name.

- Geared or leveraged products are technically classified as managed funds rather than ETFs under Australian regulation, despite trading on an exchange. Investors should not assume they carry the same risk profile as standard ETFs.

The digital asset category expanded meaningfully when the iShares Bitcoin ETF launched on the ASX in November 2025, becoming one of the first spot Bitcoin ETFs available to Australian retail investors. The Corporations Amendment (Digital Assets Framework) Bill 2025, which passed Parliament in April 2026, established a new regulatory framework for digital asset products going forward.

Active, ESG, and thematic ETFs: a growing part of the landscape

Active ETFs employ professional managers who aim to outperform a benchmark rather than simply replicate it. Unlike passive ETFs, active products typically do not publish daily holdings to protect their trading strategies.

Fee competition in this space has intensified. MQAE (Macquarie Core Australian Equity Active ETF) carries a MER of just 0.03%, and MQEG (Macquarie Core Global Equity Active ETF) charges 0.08%, both competitive with or below some passive products. ESG ETFs apply exclusion screens or ESG scoring to standard index methodologies: E200 charges 0.05% and IESG charges 0.09%, carrying modest premiums over equivalent non-screened products.

The SPIVA Australia Year-End 2025 scorecard from S&P Global remains the most current independent dataset on active versus passive outcomes. Its consistent long-term finding is that the majority of active funds underperform their benchmark after fees over medium-to-long time horizons.

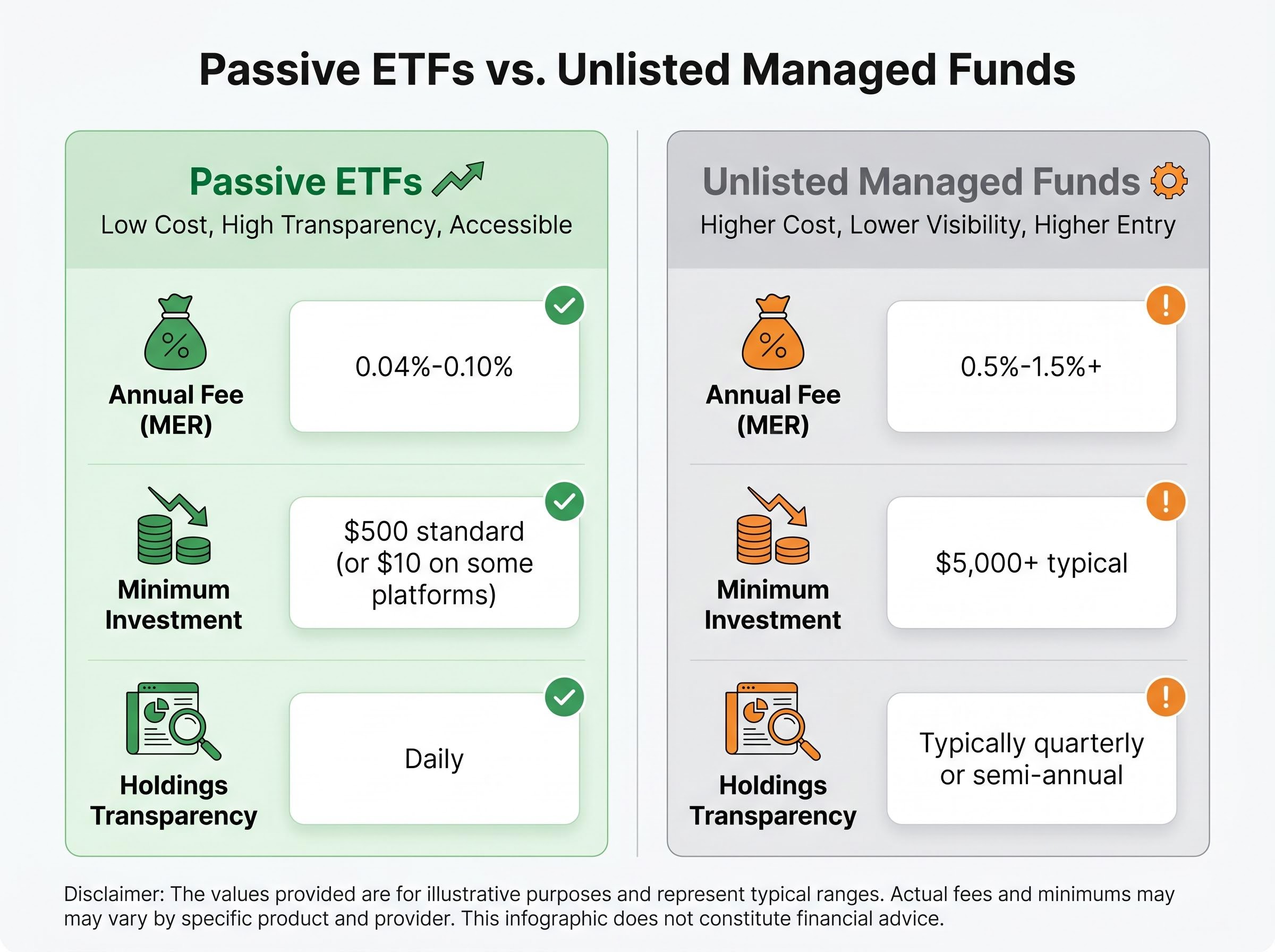

What ETFs actually cost: fees, spreads, and the comparison to managed funds

The Management Expense Ratio (MER) is the annual fee deducted directly from the fund’s assets before returns reach investors. There is no separate invoice; the cost is embedded in performance. A fund with a 0.07% MER deducts that proportion of assets each year, reducing the NAV and, by extension, the return the investor receives.

Fee Comparison: Broad passive ETFs charge 0.04%-0.10% per annum. Traditional Australian actively managed funds commonly charge 0.5%-1.5% per annum.

The named anchors make the gap concrete. A200 charges 0.04%, IOZ charges 0.05%, and A300 charges 0.04%. An actively managed Australian equities fund charging 1.0% costs roughly 20 times more per dollar invested than those products for exposure to a similar underlying market.

| Dimension | Passive ETFs | Unlisted Managed Funds |

|---|---|---|

| Annual fee (MER) | 0.04%-0.10% | 0.5%-1.5%+ |

| Minimum investment | $500 standard; $10 on some platforms | $5,000+ typical |

| Brokerage | Per-trade fee (varies by broker; zero on some platforms for own products) | Nil (buy/sell spread instead) |

| Holdings transparency | Daily (passive); periodic (active) | Typically quarterly or semi-annual |

Brokerage commissions and bid-ask spreads are transaction costs that sit on top of the MER and vary by platform and ETF liquidity. Some platforms, such as Betashares Direct, offer zero brokerage on their own products.

The minimum investment barrier is also lower. Most standard brokerage accounts set $500 as the minimum ETF purchase, while some platforms allow investment from as little as $10. Unlisted managed funds typically require $5,000 or more to open, with further minimum top-up amounts.

Over a 20-year investment horizon, the gap between a 0.07% MER and a 1.0% MER on the same underlying return compounds into a material difference in terminal wealth. The numbers speak for themselves.

For investors weighing whether to use an ETF or an actively managed fund for part of their portfolio, our comprehensive walkthrough of managed fund due diligence covers the specific PDS sections that carry the most decision weight, how to verify an AFS licence on ASIC Connect, and the fee compounding calculations that make a 1% annual cost difference worth roughly $32,000 on a $50,000 investment over 20 years.

How Australian tax applies to ETF distributions and capital gains

A common misconception is that ETFs are entirely “set and forget” from a tax perspective. In practice, two distinct tax events apply:

- Distributions received during the holding period, paid by the ETF to unitholders (typically quarterly or semi-annually)

- A capital gains tax (CGT) event on disposal, triggered when units are sold

Distributions can include several components, each with different tax treatment in the investor’s hands:

- Ordinary dividends or interest income

- Franking credits passed through from Australian equities holdings

- Capital gains realised inside the fund from portfolio rebalancing

Franking credits attached to dividends from Australian companies reduce the investor’s tax liability, functioning as a credit for corporate tax already paid. Interest income and unfranked dividends are added to assessable income at the investor’s marginal rate.

Capital gains tax on disposal works as follows: the cost base equals the original purchase price plus transaction costs such as brokerage. Sale proceeds minus cost base equals the capital gain (or capital loss) that forms a CGT event.

ETF issuers publish annual tax statements, including AMIT (Attribution Managed Investment Trust) member annual statements, which investors or their accountants use when lodging returns. Australian-listed ETFs are structured as regulated unit trusts under the same legal framework as traditional managed funds.

The 12-month CGT discount rule and what it means in practice

The 50% CGT discount is one of the most valuable structural advantages available to Australian investors. ETF units held for at least 12 months qualify, meaning only half the net capital gain is added to assessable income.

The discount applies to individuals and trusts (including SMSFs at concessional rates), not to companies. It applies to the net capital gain after offsetting any capital losses from other investments in the same financial year.

For SMSF investors in accumulation phase, the effective tax rate on capital gains is 15%. On assets held for more than 12 months, the rate drops to 10%, making ETFs a particularly tax-efficient vehicle within super.

Hidden superannuation costs extend the fee comparison beyond headline MER figures: pooled trust structures can transfer capital gains tax liabilities from exiting members to remaining members, and some options marketed as low-fee index strategies embed a financing spread cost through swap contracts that never appears as a line item in any fee disclosure document.

The ATO guidance on calculating CGT confirms that the 50% discount applies to individuals and trusts on assets held for at least 12 months, while complying superannuation funds receive a one-third discount rather than the full 50% available to individual investors.

Understanding this rule directly affects the optimal holding strategy. Selling ETF units one day before the 12-month threshold means forgoing a discount that could halve the tax on the gain. Many first-time buyers are unaware of this mechanic.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Tax outcomes depend on the investor’s total income, entity structure (individual, SMSF, company), and holding period. A qualified tax adviser should be consulted for individual circumstances.

Investor protections and how ETF assets are kept safe

ETF assets are held on trust for unitholders in a legally separate structure from the issuer’s own business. The fund’s holdings sit outside the issuer’s balance sheet and would not be accessible to the issuer’s creditors in an insolvency event.

Structural Protection: ETF assets are not included in the issuer’s balance sheet and would not be available to the issuer’s creditors.

Three layers of protection apply:

- Unit trust legal separation: The fund exists as a distinct legal entity from the ETF provider

- Third-party custodian: An independent custodian (appointed by the issuer) holds the underlying assets, adding further separation from operational risk at the issuer level

- Corporations Act regulated product framework: Australian-listed ETFs are structured as regulated unit trusts, carrying the highest tier of investor protection regulation available for retail investment products in Australia

For synthetic ETFs, the protection profile differs because they use derivative instruments rather than holding physical assets. Counterparty risk becomes relevant, and investors should review the Product Disclosure Statement (PDS) to understand what collateral or other mechanisms are in place. ASIC naming conventions require the word “synthetic” to appear in parentheses in the fund name.

ASIC Regulatory Guide RG 282 establishes the naming conventions and disclosure obligations that govern how ETPs are classified and marketed to Australian retail investors, including the requirement that synthetic ETFs display that description in parentheses within the fund name.

The Corporations Amendment (Digital Assets Framework) Bill 2025, which passed in April 2026, is relevant to investor protections for digital asset ETFs going forward, establishing a new regulated product category for these instruments.

Australian-domiciled ETFs also avoid the administrative requirement of completing US W-8BEN forms that applies when investing in US-domiciled funds directly. This is a practical benefit that simplifies tax reporting for Australian holders.

Executing an ETF trade: platforms, order types, and best practices

Choosing between an online broker, full-service broker, or financial adviser

Three purchasing pathways are available, each with a different cost and service trade-off:

- Online broker: Lowest cost, self-directed, suitable for straightforward ETF purchases. Most platforms set a minimum of $500 per trade, though some allow purchases from $10.

- Full-service broker: Higher cost, with access to research, IPO allocations, and estate or SMSF guidance. Suitable for investors with more complex portfolios or those seeking advisory support.

- Financial adviser: Highest cost, with managed portfolio construction, ongoing monitoring, and tax guidance. Appropriate for those wanting professional asset allocation. ETF uptake among financial planning firms has been growing, making adviser-managed ETF portfolios increasingly mainstream.

For the majority of first-time ETF buyers, an online brokerage account is the most practical starting point. The steps below outline the process.

How to execute an ETF purchase online:

- Open a brokerage account with a platform that provides access to ASX-listed ETFs

- Transfer funds into the account (allow time for settlement)

- Search the ASX ticker code of the ETF (e.g., A200, IOZ, VGS)

- Check the indicative NAV (iNAV) published by the issuer and compare it to the current market price

- Review the bid-ask spread; a tighter spread indicates better liquidity

- Place a limit order at a price close to the iNAV rather than a market order

- Confirm the order and note that settlement in Australia is T+2 (two business days after the trade date)

The distinction between order types matters. A market order executes immediately at the best available price, which on a less liquid ETF may be materially different from the last traded price. A limit order executes only at the specified price or better, giving the investor control over execution quality.

Execution practices that protect returns:

- Use limit orders for all ETF transactions to ensure execution near NAV

- Avoid trading in the first and last 10 minutes of the ASX session (10:00-10:10 am and 3:50-4:00 pm AEST) when bid-ask spreads widen and price volatility increases during open and close auctions

- Check the iNAV before placing an order to confirm the market price reflects fair value

- Consider dollar-cost averaging: investing a fixed dollar amount at regular intervals (monthly or quarterly) rather than attempting to time the market, a strategy well-suited to low-minimum platforms

Designing an ETF portfolio: aligning strategy with objectives

Selecting a well-regarded ETF solves one problem. Placing it within a portfolio structure that matches the investor’s objectives, time horizon, and risk tolerance solves the larger one.

The core-satellite framework is a widely used approach. The core consists of one or two broadly diversified, low-cost ETFs held for the long term. Satellites are smaller positions in sector, thematic, or asset class ETFs that reflect specific views or needs.

- Core examples: A200, VAS, or IOZ for domestic equity; VGS for broad international developed markets

- Satellite examples: NDQ for US technology exposure; IAF for fixed income; BILL for cash management; QRE or MVR for resources sector tilts; E200 or IESG for ESG-screened allocations

Diversification beyond equities matters. Including fixed income ETFs, cash ETFs, and property ETFs can reduce portfolio volatility and improve income stability, particularly as investors approach the drawdown phase of their investment timeline.

Inflation-aware portfolio construction adds another lens to the core-satellite framework: with Australia’s annual CPI at 4.6% in March 2026 and the RBA cash rate at 4.10%, fixed income ETFs like CRED (5.2% distribution yield) and cash ETFs like AAA and ISEC (yielding roughly 3.90%-4.24%) can serve a dual role as both income generators and tactical reserves while equity positioning is assessed.

ETFs are eligible for SMSF holding on the same basis as individual shares, making them a natural building block in self-managed super portfolios. They also fit within standard brokerage accounts and managed account structures.

Six questions to ask before buying any ETF

Before purchasing any ETF, work through this selection checklist:

- What index or strategy does this ETF track, and is the methodology transparent? Reputable index providers include S&P, Nasdaq, and Solactive.

- What is the total cost including MER and typical bid-ask spread? A low MER combined with a wide spread may not deliver the cost advantage it appears to on paper.

- Is this a physical or synthetic structure, and what does that mean for risk? Physical ETFs hold the underlying assets directly; synthetic ETFs introduce counterparty risk.

- What is the fund’s AUM and trading liquidity on the ASX? Higher AUM generally correlates with tighter spreads and more efficient pricing.

- Is this ETF Australian-domiciled, and what are the tax reporting implications? Australian-domiciled products simplify tax reporting and avoid US W-8BEN requirements.

- Have I read the PDS and do I understand the specific risks for this asset class? The Product Disclosure Statement is the authoritative document for fees, risks, and distribution policy.

Betashares AUM exceeded $50 billion with more than 1 million Australian investors, providing one benchmark for assessing provider scale and credibility. MQAE recorded a one-year return of +13.51% as of 1 April 2026, though any active return should be assessed against the relevant benchmark for a meaningful comparison.

The PDS for each ETF contains the authoritative information on all of the above and should be read before investing.

The long-term case for ETFs in Australia is built on structure, not hype

The structural advantages covered throughout this guide explain why adoption continues to accelerate:

- Cost efficiency: MERs as low as 0.03%-0.07% for broad market exposure

- Intraday liquidity: Buy and sell during market hours at live prices anchored to NAV

- Transparent holdings: Daily disclosure for passive products

- Investor protection: Assets held in a legally separate unit trust with an independent custodian, regulated under the Corporations Act

- Accessibility: Entry from as little as $10 on some platforms

The growth trajectory reinforces the point. From approximately 2.2 million holders in 2024 to 2.69 million in 2025, with an estimated 300,000 additional Australians intending to begin ETF investing within the next 12 months, this reflects a structural shift in how Australians invest rather than a cyclical trend. 411,000 first-time investors entered the market in 2025 alone.

ETFs do not remove market risk. They require a deliberate portfolio construction approach to achieve genuine diversification, and tax outcomes depend on individual circumstances that benefit from professional advice.

The practical next steps are straightforward: review the six-question selection checklist, read the PDS for any ETF under consideration, and execute with a limit order during core market hours.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.