RBC Raises S&P 500 Target to 8,150, Warns of 10% Pullback Risk

1 hr ago

With the fee gap between Australia’s three cheapest broad-market share ETFs now just 0.01 percentage points, choosing the right Australian share ETF in 2026 is no longer simply a cost decision. VAS, A200, IOZ, STW, and MVW collectively hold more than A$50 billion in assets and attract billions in annual inflows from Australian retail investors. These five funds track similar but not identical indices, carry meaningfully different liquidity profiles, and have delivered returns that diverged more than their overlapping structures might suggest. The Australian ETF market pulled in A$13.3 billion in net inflows in the 12 months to December 2025, confirming that passive index investing via ASX-listed ETFs is now mainstream for Australian retail portfolios.

Australian ETF market growth has been running at a five-year compound annual rate of 26.3%, with total assets estimated at A$340-350 billion as of April 2026 and Betashares forecasting the industry will surpass A$500 billion by end-2028, a trajectory that is reshaping how retail investors think about passive index allocation.

This analysis compares all five ETFs across fund size, management fees, bid-ask spreads, daily liquidity, five-year returns, and index methodology, using ASX data as at 31 March 2026, to give readers a structured framework for matching the right fund to their individual priorities.

Most investors treat these five funds as interchangeable. They are not. The distinction starts at the index level, and it embeds a philosophical decision about how the Australian market should be represented in a portfolio.

Each ETF tracks a different benchmark:

A200’s Solactive index differs from the S&P/ASX 200 in brand, but the composition is nearly identical in practice. That distinction is largely academic. VAS’s S&P/ASX 300 coverage, however, adds genuine exposure to mid- and small-cap names absent from the ASX 200 funds, a modest but substantive diversification difference.

The most structurally significant outlier is MVW. Its equal-weight methodology redistributes portfolio weight away from the big banks and miners that dominate every market-cap-weighted fund in this group.

Sector concentration note: Financials (30.43%) and Materials (20.36%) alone account for more than 50% of the S&P/ASX 200 as at 29 April 2026. Health Care follows at 10.07%. Every market-cap-weighted ETF in this comparison carries that same concentration.

For investors already overweight large Australian banks and miners through superannuation, the equal-weight or broader-index options may warrant specific consideration before the fee comparison begins.

Home bias in Australian portfolios has historically been reinforced by the franking credit system, which rewards domestic equity income in ways that international funds cannot replicate, but that structural incentive has not prevented a measurable shift toward international ETFs as the top purchase category on major platforms in Q1 2026.

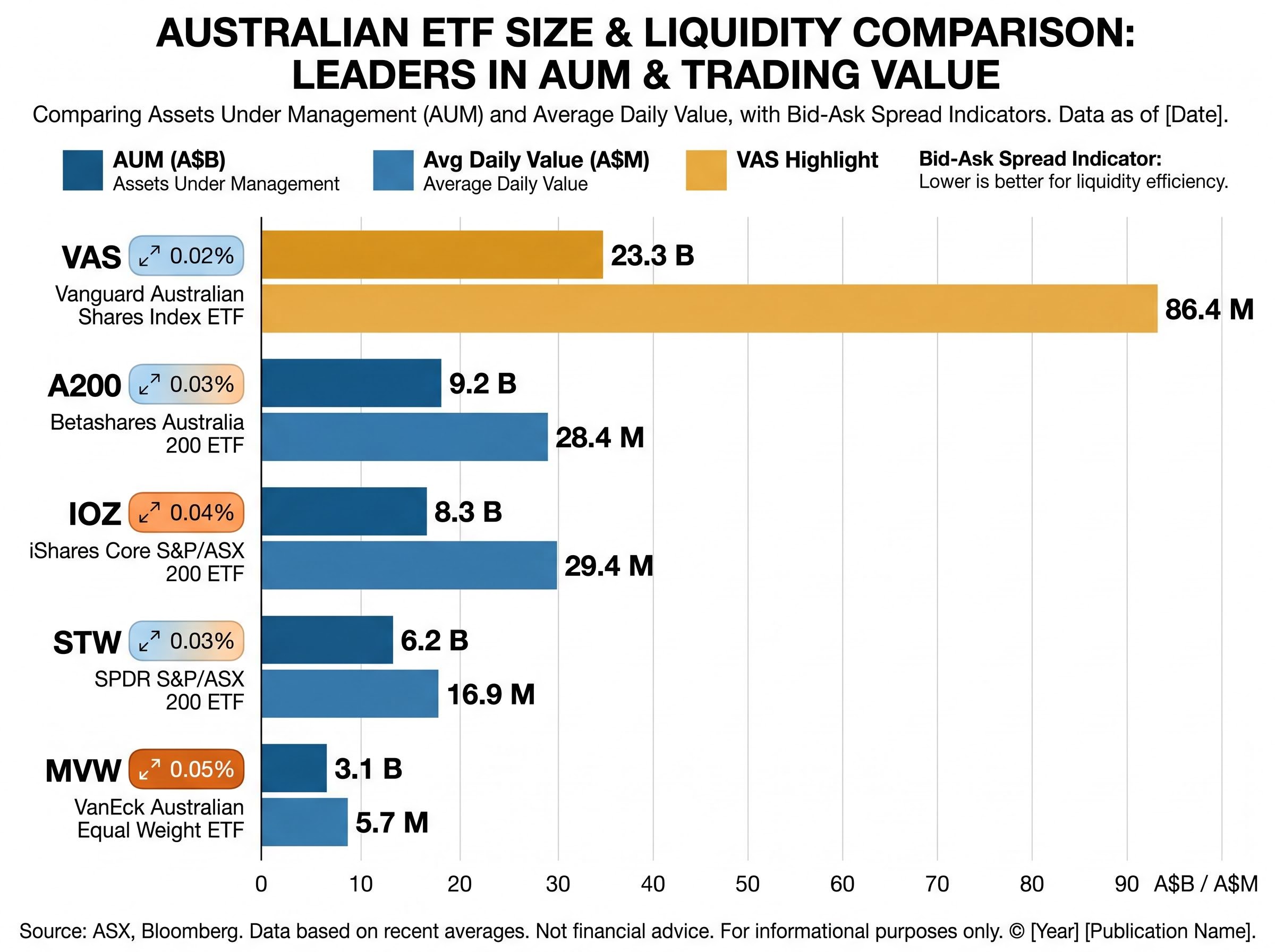

The hierarchy here is not close. VAS holds A$23.3 billion in assets under management, more than double A200 at A$9.2 billion and nearly three times IOZ at A$8.3 billion. STW sits at A$6.2 billion, and MVW trails at A$3.1 billion.

But AUM alone is not the most operationally relevant measure. For investors making regular contributions or executing large lump-sum trades, daily traded value determines how easily a position can be built or unwound without moving the price.

| ETF | AUM (A$B) | Avg daily value (A$M) | Bid-ask spread (%) |

|---|---|---|---|

| VAS | 23.3 | 86.4 | 0.02 |

| IOZ | 8.3 | 29.4 | 0.04 |

| A200 | 9.2 | 28.4 | 0.03 |

| STW | 6.2 | 16.9 | 0.03 |

| MVW | 3.1 | 5.7 | 0.05 |

VAS trades A$86.4 million per day on average, roughly three times the volume of its nearest peers. IOZ recorded the strongest ETF inflows among all Australian share ETFs in February 2026, signalling growing retail preference, but its daily volume still sits well behind VAS.

MVW’s position warrants attention for a different reason. Its AUM declined by A$158.5 million between Q4 2025 and Q1 2026, making it the only fund in the group to record a decline. Sustained outflows create commercial sustainability questions for any fund.

The bid-ask spread is the difference between the price a buyer pays and the price a seller receives. It applies on both sides of every trade, making it an implicit transaction cost that compounds for frequent investors.

VAS offers the tightest spread at 0.02%, followed by A200 and STW at 0.03%, IOZ at 0.04%, and MVW at 0.05%. VAS’s dominance in both AUM and spread reflects a virtuous cycle: larger funds attract more market makers, which compresses spreads further, which attracts more capital. For investors who dollar-cost average monthly, this recurring per-trade cost may matter more than a one-basis-point MER difference.

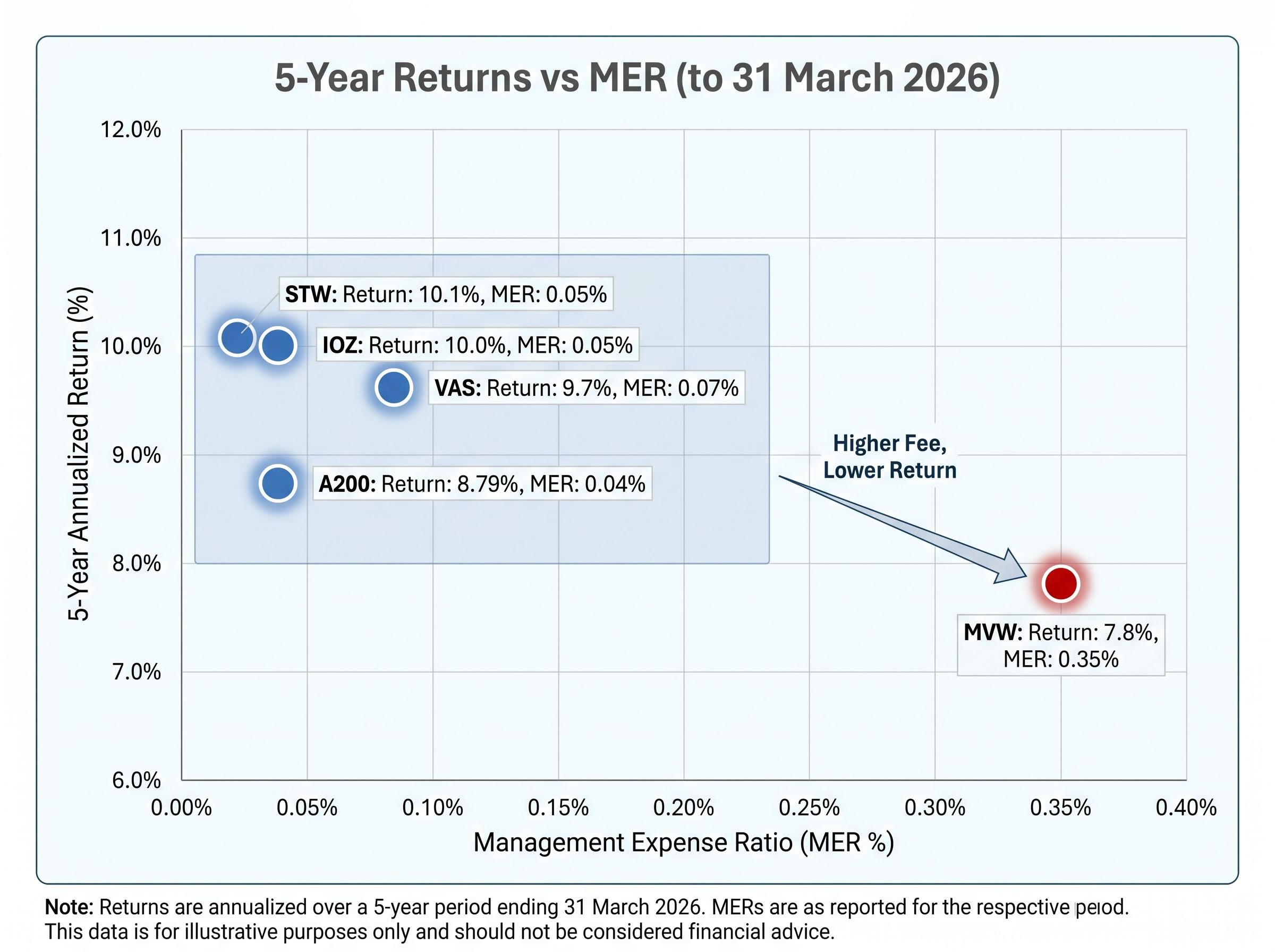

A200 holds the lowest management expense ratio (MER) in the category at 0.04%, a position it established when Betashares cut the fee from 0.07% in March 2023. IOZ and STW sit at 0.05%, VAS at 0.07%, and MVW at 0.35%.

| ETF | MER (%) | Est. annual fee revenue (A$M) |

|---|---|---|

| A200 | 0.04 | 3.7 |

| IOZ | 0.05 | — |

| STW | 0.05 | 3.1 |

| VAS | 0.07 | 16.3 |

| MVW | 0.35 | 10.9 |

On a A$50,000 holding, the difference between A200 (0.04%) and VAS (0.07%) is A$15 per year. Over a decade, that gap amounts to A$150 before compounding, a real but modest sum relative to the liquidity and diversification differences between the two funds.

The 0.01% gap between A200, IOZ, and STW is even smaller. In dollar terms, it is negligible for most retail portfolios.

MVW’s 0.35% MER stands apart. At roughly 8.75 times A200’s fee per dollar invested, it generates an estimated A$10.9 million in annual fee revenue despite being the smallest fund in the group. That premium reflects the higher cost of maintaining an equal-weight strategy, but it requires performance to justify it. STW’s fee history shows competitive pressure at work: State Street cut the fee from 0.29% to 0.19% in December 2015, with further reductions since.

Among the four market-cap-weighted funds, fee differences alone are unlikely to determine which ETF best suits an individual investor.

Four of the five funds sit in a tight band. STW delivered 10.1% annualised over five years to 31 March 2026, and A200 delivered 8.79%, followed by IOZ at 10.0% and VAS at 9.7%. Index methodology and fees have not produced dramatically different outcomes among market-cap-weighted peers over this period.

VAS’s slightly lower figure reflects its broader index exposure. The S&P/ASX 300’s small- and mid-cap tail modestly diluted returns compared to ASX 200-focused funds over the measured period.

Then there is MVW, at 7.8% annualised.

MVW trailed the top-ranked ETFs by approximately 2.3 percentage points per annum over five years, a gap that compounds significantly over a long holding period.

| ETF | 5-year annualised return (%) | 1-year return (%) | MER (%) |

|---|---|---|---|

| STW | 10.1 | 16.45 (to 29 Apr 2026) | 0.05 |

| A200 | 8.79 | 11.93 (to 31 Mar 2026) | 0.04 |

| IOZ | 10.0 | — | 0.05 |

| VAS | 9.7 | — | 0.07 |

| MVW | 7.8 | — | 0.35 |

MVW’s underperformance is structural rather than cyclical. The equal-weight approach underweights large-cap financials and miners during periods when those sectors outperform, which they have done consistently over the past five years. The variability is telling: MVW ranked second best among the group at the end of Q1 2025, then fell to worst performer by the end of Q1 2026. That swing is not random noise. It is a predictable consequence of an equal-weight structure that amplifies sector rotation effects.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. Still, MVW’s return profile warrants scrutiny because its variability is a feature of the methodology, not a temporary dislocation.

The preceding data supports a matching exercise rather than a universal ranking. Three investor archetypes map to distinct fund strengths:

IOZ and STW fill situational roles. IOZ suits investors who prefer BlackRock’s infrastructure and the accessibility of its lower unit price (approximately $34.89) for regular contributions. Its strong February 2026 inflows reflect growing retail preference. STW offers the longest continuous trading history on the ASX but carries a slightly higher fee than A200 for no meaningful structural benefit.

Inflation-aware ETF allocation has become a live portfolio consideration for Australian investors in 2026, with the RBA cash rate at 4.10% and annual CPI running at 4.6%, factors that affect the real return calculation for broad market share ETFs alongside their headline distribution yields.

All five ETFs pay quarterly distributions. Approximate cash yields as at April 2026: IOZ at 3.56%, VAS at approximately 3.5%, STW at 3.30%, and A200 at 3.2%.

Franking credits improve effective after-tax yields for Australian resident investors. A200’s gross yield (including franking credits) is higher than its 3.2% cash figure suggests, improving its competitiveness with higher-yielding peers on a post-tax basis. No 2026 tax or regulatory changes affect franking credit treatment for these funds.

When fees between the three cheapest options are separated by just 0.01%, the decision framework shifts from cost optimisation to fit optimisation. VAS leads for scale and liquidity. A200 leads for lowest cost. IOZ offers accessibility and BlackRock infrastructure. STW provides historical continuity. MVW requires a deliberate equal-weight thesis to justify its fee.

As Australia’s ETF market deepens, AUM growth in IOZ and A200 will likely continue to close the liquidity gap with VAS, potentially making the choice among the top three even more interchangeable in the years ahead.

For investors who have settled on a core domestic share ETF and want to build out a broader multi-fund structure around it, our dedicated guide to building a quality ASX ETF portfolio covers how QUAL, IVV, and AQLT each occupy a distinct portfolio role, including the CGT discount mechanics that reward holding periods beyond 12 months.

Readers should verify current figures on ETF provider websites and ASX monthly investment product reports before making any investment decision. All data in this analysis reflects 31 March 2026 figures unless otherwise noted.

The ASX monthly investment product reports publish comprehensive fund flow, AUM, and trading activity statistics for all ASX-listed ETFs, providing the official benchmark data against which provider-reported figures can be independently verified.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The five leading Australian share ETFs by assets are VAS, A200, IOZ, STW, and MVW, which collectively hold more than A$50 billion. VAS leads on liquidity and scale, A200 leads on the lowest fee at 0.04%, while MVW takes a distinct equal-weight approach that suits a specific investor thesis.

VAS tracks the S&P/ASX 300 with approximately 300 holdings and charges a 0.07% MER, while A200 tracks the Solactive Australia 200 with approximately 200 holdings at a lower 0.04% MER. VAS also trades around A$86.4 million per day, nearly three times A200's daily volume, making it stronger for investors who trade frequently or in large amounts.

A200 from Betashares has the lowest management expense ratio at 0.04%, after a fee cut from 0.07% in March 2023. On a A$50,000 holding, the difference between A200 and VAS (at 0.07%) amounts to just A$15 per year.

STW delivered the highest five-year annualised return at 10.1% to 31 March 2026, followed by IOZ at 10.0%, VAS at 9.7%, and A200 at 8.79%. MVW, the equal-weight fund, trailed the group at 7.8% annualised over the same period.

MVW uses an equal-weight methodology that reduces concentration in the big banks and miners that dominate market-cap-weighted funds, but it charges a 0.35% MER and delivered a five-year annualised return of 7.8%, trailing its peers by approximately 2.3 percentage points per year. It suits investors with a deliberate conviction about reducing large-cap concentration risk, not those optimising for cost or returns alone.