Barclays Warns of Prolonged Market Volatility Under New Fed Reality

21 hrs ago

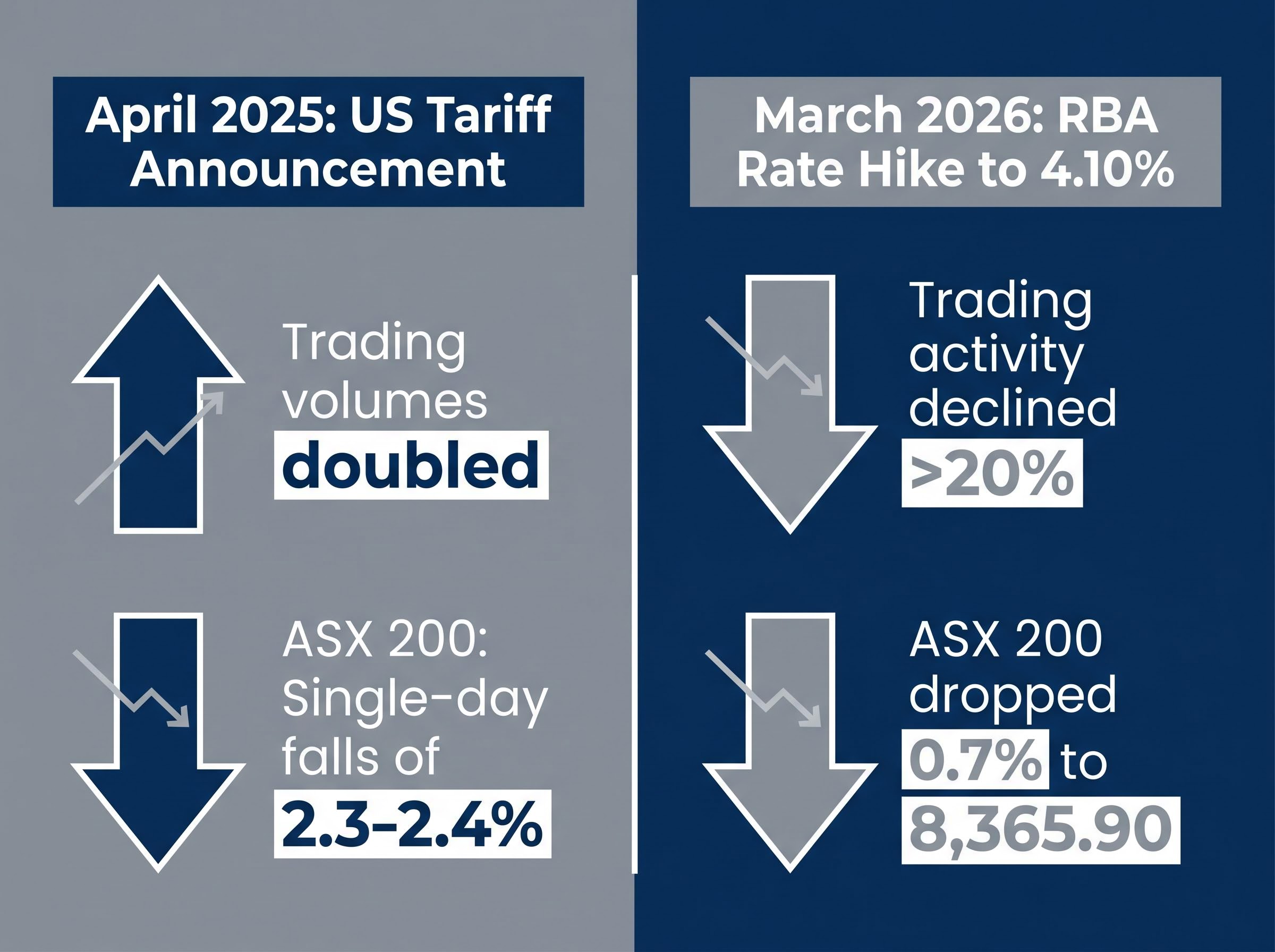

Platform data from April 2026 reveals a pattern Australian retail investors may find uncomfortable. Trading volumes on the Selfwealth by Syfe platform doubled during the US tariff announcement in April 2025, then fell more than 20% after the RBA’s March 2026 rate hike. Two macroeconomic events, two opposite reactions, one consistent thread: investors are moving faster than the market warrants. The Selfwealth by Syfe Quarterly Investor Pulse Index for Q1 2026 offers a rare, granular look at how Australian retail investors actually behave when headlines arrive, not how they intend to behave. This data lands at a moment when ASX trading volumes are running 32% above Q1 2025 levels and when the speed at which news moves markets has structurally accelerated. What follows is an examination of what the volume data reveals about the cost of reactive investing, why the psychological pull toward action is so difficult to resist, and which specific strategies can help Australian investors build the kind of disciplined system that outperforms headline-chasing over time.

The contrast is stark. When US tariff announcements hit in April 2025, trading volumes on the Selfwealth by Syfe platform doubled. The ASX 200 fell approximately 2.3-2.4% in single-day drops, and investors rushed to act. When the RBA raised the cash rate to 4.10% on 17 March 2026, the opposite occurred: trading activity declined more than 20%, and the ASX 200 drifted to 8,365.90 on 22 March 2026, its lowest close since May 2025.

One event triggered panic trading. The other triggered paralysis. Neither response served the investors who acted on it.

| Attribute | US tariff announcement (April 2025) | RBA rate hike (March 2026) |

|---|---|---|

| Volume response | Doubled on platform | Declined more than 20% |

| ASX 200 market move | Single-day falls of 2.3-2.4% | Dropped 0.7% to 8,365.90 |

| Typical outcome for reactive traders | Sold into fear; missed relatively swift recovery | Froze; missed rebalancing opportunity during weakness |

The broader context reinforces the pattern. ASX Q1 2026 trading volumes ran 32% above Q1 2025 and 23% above Q4 2025, confirming that elevated reactivity is structural, not a one-off spike. The problem is not the direction of the response. It is the reflex itself: letting macro headlines determine portfolio decisions regardless of whether the headline calls for action at all.

Platform data finding: Market-moving news is now reflected in trading activity almost immediately rather than over days or weeks, compressing the window in which emotional decisions are made.

The speed of the reactive response is not accidental. Several structural forces have converged to make it almost inevitable:

The compression of the information-to-trade window is not merely a platform feature; retail investor behaviour in Australia now exhibits zero execution lag, with capital rotating toward defensive positions within hours of a macro announcement rather than across the days or weeks that characterised earlier market cycles.

Morningstar’s 2025 Australian ETF flows review confirmed net inflows of AUD 48.3 billion for the year, a marked acceleration from 2024 levels that illustrates how the scale of passive investment in Australia has reached a point where large fund flows are now capable of concentrating and amplifying single-day price movements.

Each of these forces would increase reactivity on its own. Together, they have created a feedback loop: faster information produces faster trades, which amplifies short-term volatility, which generates more headlines, which triggers more trades.

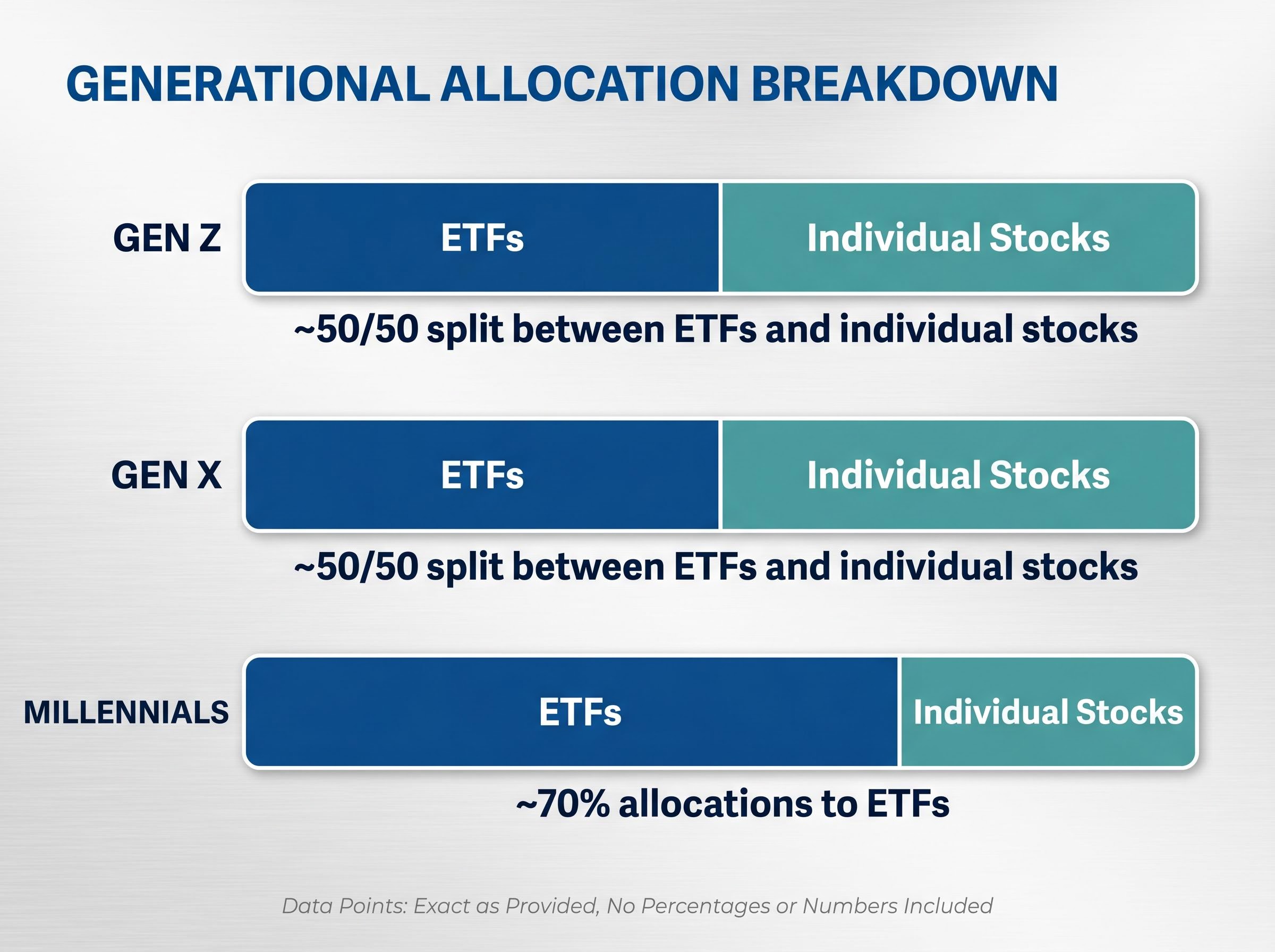

The composition of who is investing adds another layer. Platform data shows Gen Z and Gen X investors maintain an approximately 50/50 split between ETFs and individual stocks, while Millennials direct roughly 70% of allocations to ETFs. International ETFs overtook domestic ETFs as the most purchased category on the Selfwealth by Syfe platform in Q1 2026.

Younger investors show a higher propensity for active trading responses to news. Yet even older cohorts are becoming more reactive than prior generations, a convergence driven by the same platform accessibility and information speed that shapes the younger demographic. The market did not simply get noisier; the feedback loop between news and retail action genuinely tightened.

Reactive trading is not a character flaw. It is a well-documented psychological mechanism, and it follows a predictable sequence:

The mechanism at the core of this sequence is loss aversion: investors feel losses approximately twice as acutely as equivalent gains, according to foundational behavioural finance research. When the ASX 200 fell 2.3-2.4% in a single day on tariff headlines in April 2025, the loss felt urgent and personal. The recovery, which followed relatively quickly, felt abstract and uncertain. Investors who exited during the fear locked in real losses while the index went on to deliver a 6.8% full-year gain for 2025, despite the intra-year volatility.

The financial penalty for reactive trading extends beyond missed recovery sessions: Australia’s 50% CGT discount for assets held longer than 12 months functions as a structural tax incentive to hold through volatility, meaning investors who sold during the April 2025 tariff spike not only forfeited index gains but also forfeited a government-sanctioned reduction in their eventual tax burden.

Kahneman and Tversky’s prospect theory established the foundational evidence that losses loom approximately twice as large as equivalent gains in investor decision-making, a finding that directly explains why a single-day ASX fall of 2.3-2.4% produces a trading response disproportionate to its long-term portfolio significance.

The asymmetry cuts deeper than most investors realise. Missing even a handful of the strongest recovery days in a calendar year can substantially reduce annual returns. The tariff episodes of 2025 demonstrated this with uncomfortable clarity: the sharpest rebounds came within days of the sharpest falls, and investors who had already sold were not positioned to capture them.

Northcape Capital’s 2026 outlook positions disciplined investing in quality companies as demonstrably superior to reactive, macro-news-driven trading, particularly amid volatility generated by passive fund flows and sector-level extremes.

This is not merely a theoretical argument. The Australian market data from 2025-2026 provides a real-time case study in the cost of acting on headlines rather than maintaining a long-term position.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

If the problem is structural, the solution needs to be systematic. Three specific mechanisms can neutralise different dimensions of the reactivity problem:

The mechanism is straightforward: a fixed periodic investment regardless of market price averages out entry cost over time. During the April 2025 tariff volatility, an investor with a scheduled fortnightly purchase would have bought into the weakness automatically, capturing the lower prices that reactive sellers were fleeing. The purchase happened because it was pre-committed, not because the investor made a calm, rational decision under pressure.

Two implementation models exist: calendar-driven (quarterly or semi-annual review) and threshold-driven (rebalance when any allocation drifts beyond a set percentage). Both enforce discipline during drawdowns. After the March 2026 RBA hike pushed the ASX 200 to its lowest close since May 2025, a threshold-triggered rebalance would have directed capital toward equities at a relative discount, the opposite of the paralysis that platform data recorded.

The Selfwealth by Syfe platform’s auto-invest feature enables scheduled recurring purchases on existing holdings. This is the system-level implementation of the behavioural insight: if the decision to invest is made once and automated, the emotional spike that accompanies a rate hike or tariff announcement cannot override it. The mechanism works precisely because it removes discretion at the moment discretion is most dangerous.

One encouraging signal already exists in the data. Gold-related buying declined below 70% of total trades on the platform in Q1 2026, down from a late-2025 peak. This suggests some investors are exercising more calibrated judgement, moving away from a purely defensive posture as immediate fears moderated, rather than maintaining a reactive position indefinitely.

The structural forces driving reactivity, platform accessibility, information speed, and the sheer scale of passive flows approaching $52 billion annually, are features of the modern Australian market, not temporary conditions. The RBA cash rate sits at 4.10%, and the central bank’s own projections indicate inflation may not return to the midpoint of the target band until mid-2028. Macro-driven headline events are likely to continue throughout this period.

The investor paralysis recorded after the March 2026 rate hike assumes the current tightening cycle will extend as projected, but oil futures backwardation and historical supply shock cycles suggest an RBA policy pivot may arrive within a 6-12 month window of the shock’s peak, well ahead of the mid-2028 inflation normalisation timeline currently framing investor caution.

Yet the same generation of investors demonstrating reactive volume spikes are also building genuinely diversified portfolios. Millennials directing approximately 70% of allocations to ETFs, and the shift toward international ETFs as the most purchased category, represent systematic diversification already underway among the most reactive cohorts.

Reacting to market speed with equivalent trading frequency is potentially counterproductive to long-term returns. The goal is not to feel nothing when a headline hits; it is to build systems that ensure the feeling does not become a trade.

The capacity for disciplined behaviour exists alongside the reactive impulse. The question is which one an investor’s system activates first.

Australian retail investor behaviour has become structurally more reactive. The two Selfwealth by Syfe data points from 2025-2026, volumes doubling on tariff fears then collapsing after a rate hike, represent a measurable cost, not a neutral trait. The pattern is consistent, the behavioural mechanisms are well understood, and the asymmetric penalty for acting on headlines rather than holding through them is supported by the market data.

Three strategies offer a practical response: dollar-cost averaging removes the timing decision, periodic rebalancing enforces discipline during drawdowns, and auto-investing eliminates the human decision point when emotional pressure peaks. With the RBA’s inflation timeline extending to mid-2028 and ongoing global macro uncertainty, the conditions that triggered 2025-2026 reactivity are not fading. Systematic discipline is not a one-off correction; it is a compounding structural advantage.

Investors ready to move from diagnosis to portfolio construction will find our comprehensive walkthrough of systematic investing strategies for 2026 covers how dollar-cost averaging into diversified index products, geographic diversification across global equity ETFs, and threshold-based rebalancing work together as a combined framework, with data on capital rotation patterns and platform-specific implementation steps.

Investors may find it worth reviewing their current investment cadence, considering whether their last three portfolio decisions were triggered by a scheduled review or by a headline, and exploring whether auto-investing or rebalancing tools are available on their current platform.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Reactive investing means making portfolio decisions in direct response to headlines or macro events rather than a pre-set plan. Data from the Selfwealth by Syfe platform shows this pattern cost investors returns in 2025, with those who sold during the April tariff scare missing a 6.8% full-year ASX gain.

Trading volumes on the Selfwealth by Syfe platform fell more than 20% following the RBA's March 2026 rate hike to 4.10%, with the ASX 200 drifting to 8,365.90, its lowest close since May 2025. This paralysis meant many investors missed a rebalancing opportunity during the period of relative market weakness.

Dollar-cost averaging involves investing a fixed amount at regular intervals regardless of market conditions, removing the need to time the market. During the April 2025 tariff volatility, investors with pre-scheduled fortnightly purchases automatically bought into market weakness without needing to make a calm decision under emotional pressure.

Australian ETF net inflows reached AUD 48.3 billion in 2025 and are on track for approximately AUD 52 billion annualised in 2026, meaning large passive fund flows are now concentrating and amplifying single-day price moves. This amplification triggers more reactive individual trading responses, creating a feedback loop between headlines and short-term market swings.

Three systematic strategies can reduce reactive trading: dollar-cost averaging via fixed periodic investments, calendar or threshold-based portfolio rebalancing, and using platform-level auto-invest tools to schedule recurring purchases. These mechanisms remove the human decision point at the moment of maximum emotional pressure, which is when discretion is most dangerous.