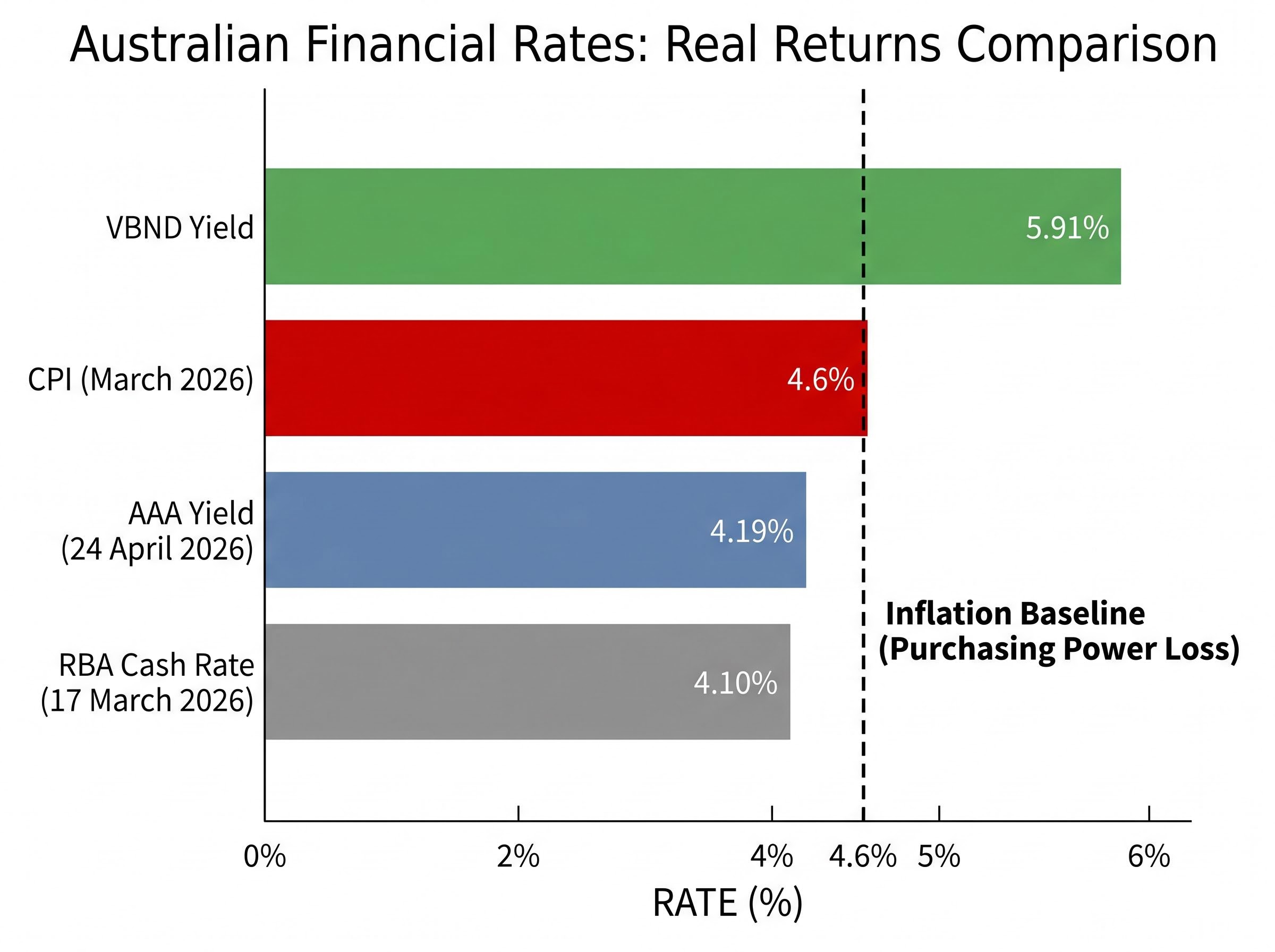

Australia’s headline Consumer Price Index (CPI) hit 4.6% annually as of the March 2026 release, and with Brent crude at $113.77 per barrel and the Reserve Bank of Australia (RBA) cash rate sitting at 4.10%, the real return on a standard savings account is now negative. That gap, between what inflation takes and what cash earns, is where investing for inflation in Australia begins. The Iran conflict has introduced a new layer of energy-driven cost-push inflation into the economy, with Reuters flagging stagflation risk as recently as 14 April 2026. The ASX 200 closed April at 8,631 points with elevated volatility, and the RBA lifted rates to 4.10% on 17 March 2026 in direct response to sustained price pressure. This is not a theoretical concern. This guide explains how to position an ASX ETF portfolio to generate real income, maintain global diversification, and protect capital when inflation is running above the cash rate, covering specific ETFs, the logic behind each, and how to combine them into a coherent inflation-aware strategy.

What inflation actually does to your portfolio (and why 4.6% changes the calculus)

A portfolio returning 4% in nominal terms while inflation runs at 4.6% is not standing still. It is losing purchasing power with every quarter that passes. The loss is silent, invisible on a brokerage statement, and compounding.

The ABS CPI data for March 2026 confirmed the headline rate at 4.6% annually, with housing, food, and transport costs among the primary contributors driving the broad-based nature of the current inflationary episode.

How inflation inflicts that damage depends on what type of inflation is present. Demand-pull inflation, driven by strong employment and consumer spending, tends to lift corporate revenues alongside prices, partially shielding equities. Cost-push inflation, the type currently driven by the Iran-related Brent crude surge to $113.77 per barrel, compresses margins for businesses that cannot pass input costs through to customers. It punishes without compensating.

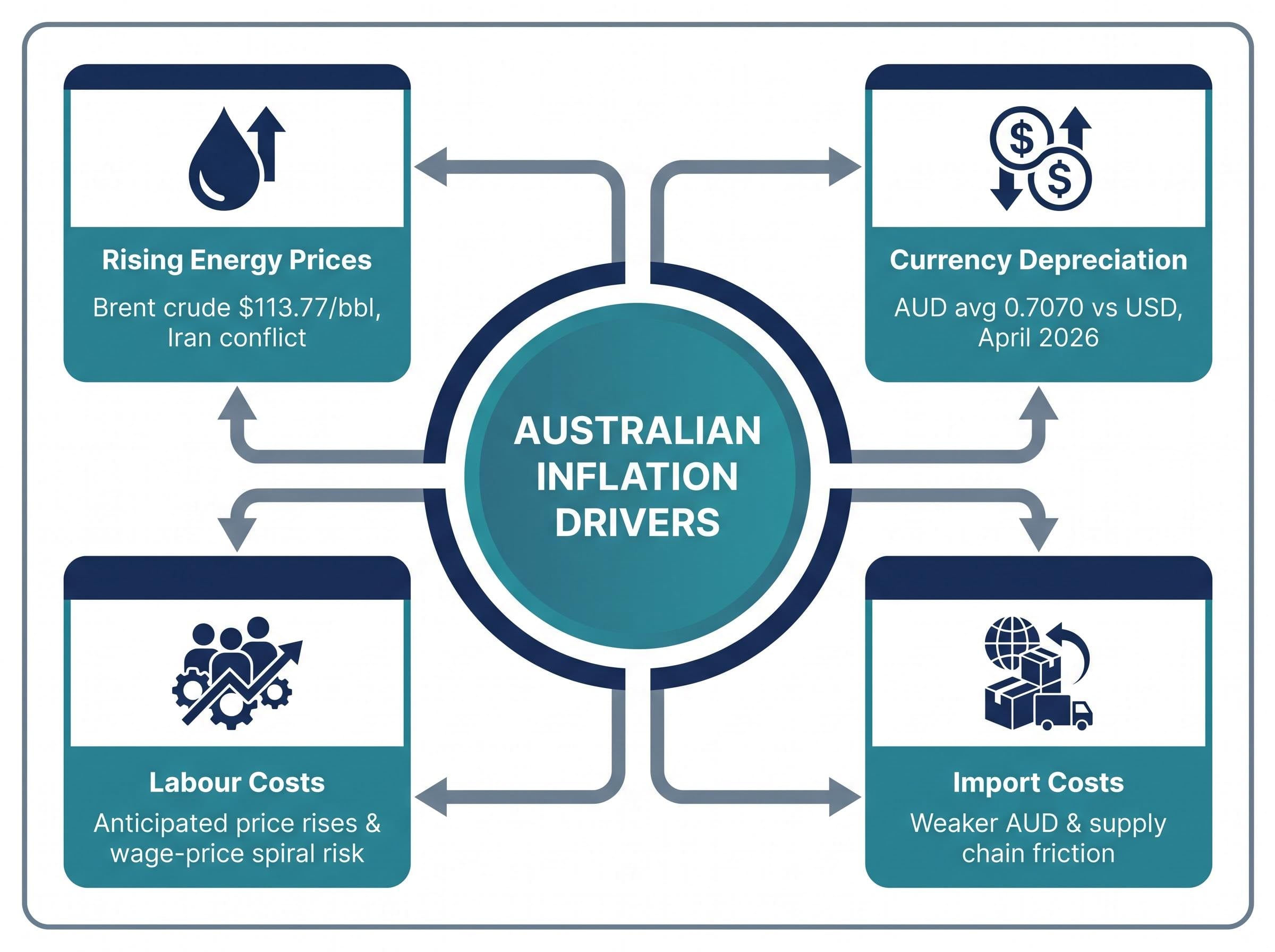

Four forces are driving the current Australian inflationary episode:

- Rising energy prices flowing from the Iran conflict and elevated global crude benchmarks

- Currency depreciation, with the AUD averaging 0.7070 against the USD in April 2026

- Labour costs, as workers seek higher pay in anticipation of further price rises, risking a wage-price spiral

- Import costs, amplified by the weaker Australian dollar and global supply chain friction

With CPI at 4.6% and the RBA cash rate at 4.10%, real rates are marginally negative. Even the central bank’s benchmark is not keeping pace with prices. Research from the International Monetary Fund indicates that each additional percentage point of inflation beyond 3% is associated with a 0.1-0.2% reduction in real GDP growth, a drag that compounds if inflation persists.

Reuters, 14 April 2026: “Australia Inc starts to feel Iran war fallout, raising stagflation risk”

Understanding the mechanics of this inflationary episode, not just its existence, is what separates reactive investors from positioned ones. Every ETF recommendation that follows is built on this foundation.

For investors who want to understand the full framework behind supply-side stagflation, our deep-dive into stagflation investing strategies examines how the Strait of Hormuz closure is structurally different from demand-driven inflation cycles, why conventional monetary easing cannot resolve a physical supply shock, and what terminal rate scenarios the RBA is navigating as it attempts to engineer demand destruction without triggering a recession.

When big ASX news breaks, our subscribers know first

Why bond yields are your friend when inflation peaks (and how to read the current moment)

Rising interest rates punish existing bondholders. That much is widely understood. What receives less attention is the opportunity embedded in the same dynamic: as bond prices fall, the income yield available to new buyers improves. For an investor entering the bond market today rather than twelve months ago, the maths has shifted meaningfully in their favour.

The question is whether rates will continue climbing or have reached a level where the next move is sideways or down. Two historical paths have ended inflationary episodes:

- Engineered economic contraction, where central banks raise rates aggressively enough to suppress demand (the US Federal Reserve’s 1980-1982 cycle reduced inflation from approximately 14% to 3%, but triggered unemployment exceeding 10%)

- Supply constraints easing organically, where the underlying cause of inflation, such as an energy supply disruption, resolves and price pressures moderate without a deep recession

The Taylor Rule, a framework for assessing whether policy rates are genuinely restrictive, implies that central banks need to raise rates approximately 1.5 percentage points per 1 percentage point of excess inflation. With CPI at 4.6% and the cash rate at 4.10%, the RBA’s current setting is restrictive only if inflation falls toward target. Further hikes or a sustained plateau remain plausible before cuts arrive.

The RBA March 2026 rate decision noted persistent upside risks to the inflation outlook alongside signs of underlying moderation, a mixed signal that leaves the door open to further tightening if price pressures do not ease as projected.

What backwardation in oil futures is telling investors right now

Oil futures markets offer a signal worth reading. Backwardation, a condition where near-term futures contracts trade at a premium to longer-dated ones, indicates that buyers are paying more for immediate delivery than for oil six or twelve months from now. This pricing structure suggests markets view the current supply disruption as transitory rather than permanent.

Historically, oil supply shocks have resolved within six to twelve months, with rate cuts following as growth headwinds dominate the policy outlook. If the current backwardation signal holds, it would be consistent with that pattern: elevated rates today, but a path toward easing within the next year. That forward-looking context is what shapes the duration decision in any fixed-income allocation.

Oil futures backwardation, where near-term contracts trade at a premium to longer-dated delivery prices, has historically been one of the more reliable signals that an energy supply shock is being priced as transitory rather than structural, and that distinction carries direct consequences for how long the RBA needs to hold rates at their current level.

Capital preservation tools when volatility is elevated: AAA and ISEC

Holding cash in an inflationary environment can feel like a concession. It is not. A cash allocation earning 4.19% is not dead money; it is a tactical reservoir that enables the moves other investors cannot make when prices dislocate.

BetaShares Australian High Interest Cash ETF (AAA) holds Australian dollar bank deposit accounts, offers daily liquidity, and delivers a running yield of 4.19% as of 24 April 2026. That tracks closely to the RBA cash rate of 4.10%, making AAA a competitive alternative to a standard savings account with the added convenience of sitting inside a brokerage account.

iShares Enhanced Cash ETF (ISEC) allocates to liquid short-term money market instruments and short-duration corporate bonds, targeting modestly higher yields than standard deposit ETFs. The trade-off is marginally less liquidity and slightly more credit exposure than a pure cash product like AAA.

| ETF | Issuer | Running Yield | Underlying Instruments |

|---|---|---|---|

| AAA | BetaShares | 4.19% | Bank deposit accounts |

| ISEC | iShares (BlackRock) | Modestly above AAA | Short-term money market and short-duration corporate bonds |

Three scenarios make a cash ETF allocation strategically valuable:

- As a pre-deployment buffer while building positions in higher-conviction holdings over time

- As a rebalancing reserve, allowing quarterly portfolio adjustments without selling existing positions at unfavourable prices

- As an opportunistic buying fund, enabling increased contributions precisely when market dislocations create depressed entry points

In a volatile, inflation-elevated environment, knowing where to park capital that is not yet deployed is as important as knowing what to buy.

Global equity ETFs for diversification and inflation resilience

Distribution yields of 1.69% and 1.73% on international equity ETFs look modest next to a bond fund paying 5.91%. That comparison misses the point. Equity ETFs are not in the portfolio for income. They are there for capital growth and geographic diversification, both of which serve a distinct purpose when inflation is concentrated in a single economy.

Vanguard MSCI Index International Shares ETF (VGS) provides exposure to over 1,000 large-cap companies across developed markets excluding Australia, with a dividend yield of 1.69%. As a core holding, VGS reduces concentration in AUD-denominated assets and ASX sector risks. With AUD/USD averaging 0.7070 in April 2026 (reaching a high of 0.7193 on 27 April), international equity ETFs also carry implicit currency diversification, which can act as a partial inflation hedge if the Australian dollar weakens further.

VGS vs QUAL: which does what in an inflation-aware portfolio

VanEck MSCI International Quality ETF (QUAL) occupies a different role. Rather than broad market coverage, QUAL selects for a specific factor: quality. Its selection criteria filter for companies with characteristics that tend to protect margins when input costs rise:

- High return on equity

- Low leverage

- Earnings stability

- Sufficient pricing power to pass costs through to customers

QUAL’s dividend yield of 1.73% (as of 22 April 2026, per Morningstar Australia) is comparable to VGS, but its concentrated quality tilt is the differentiator. In a stagflationary domestic scenario, where Australian GDP growth slows while prices remain elevated, quality factor companies with global revenue streams are structurally better positioned than the broad market.

The quality factor that QUAL selects for internationally has a domestic equivalent: pricing power on the ASX, which tends to be concentrated in companies with low debt, high return on equity, and revenue streams that are not easily compressed by rising input costs.

VGS provides the breadth. QUAL provides the resilience filter. Both serve the diversification function, but they do it differently.

Fixed income ETFs for income in a high-rate environment

Two ASX-listed bond ETFs occupy distinct positions on the fixed-income spectrum, and understanding how they differ determines whether an allocation is diversified or duplicated.

Vanguard Australian Bond ETF (VBND) offers globally diversified, currency-hedged bond exposure with an annual distribution yield of 5.91%. For an investor seeking broad, high-quality fixed-income income that currently exceeds both the RBA cash rate and the CPI reading, VBND provides that in a single holding.

BetaShares Australian Investment Grade Corporate Bond ETF (CRED) concentrates on senior fixed-rate bonds from domestic investment-grade issuers. The focus on Australian corporate credit means CRED carries a different risk profile: narrower issuer diversification, but direct exposure to the Australian corporate bond market with the potential for capital appreciation if rates peak and bond prices recover.

VBND’s 5.91% yield versus 4.6% CPI represents a positive real yield in investment-grade bonds, a condition that has not been available to Australian investors for several years.

Both ETFs carry duration risk. If the RBA continues raising rates beyond 4.10%, capital values in these funds will face downward pressure. Investors should size fixed-income allocations relative to their rate outlook and time horizon rather than chasing yield alone.

| ETF | Issuer | Yield | Underlying Exposure | Currency Hedged |

|---|---|---|---|---|

| VBND | Vanguard | 5.91% | Global diversified bonds | Yes |

| CRED | BetaShares | See fund page | Australian investment-grade corporate bonds | N/A (AUD-denominated) |

Owning both is a yield diversification decision: VBND provides global breadth, CRED provides domestic corporate credit concentration. They complement rather than duplicate.

Putting it together: contribution discipline and portfolio structure when inflation is running hot

The six ETFs discussed above serve three distinct roles within a coherent inflation-aware portfolio structure.

| Portfolio Role | ETF(s) | Function in an Inflationary Environment |

|---|---|---|

| Income | VBND, CRED | Generate yields above CPI, providing positive real income from investment-grade bonds |

| Global Diversification | VGS, QUAL | Reduce AUD concentration, access quality companies with pricing power across developed markets |

| Capital Preservation | AAA, ISEC | Earn competitive yields on liquid reserves while maintaining dry powder for opportunistic deployment |

Structure alone is not enough. Behaviour during volatile markets determines long-term outcomes more than ETF selection does. Dollar-cost averaging, specifically the discipline of investing regular amounts regardless of market conditions, is suited to the current environment. The enhanced version of this approach, investing above-normal amounts during significant market drawdowns, has historically produced better long-term results by reducing average cost basis.

Four contribution discipline steps apply in this environment:

- Set a regular contribution schedule (fortnightly or monthly) and maintain it regardless of headlines

- Identify a drawdown threshold (for example, a 10% decline in the ASX 200 from recent highs) that triggers above-normal contributions from the cash ETF buffer

- Review and rebalance quarterly to ensure allocations have not drifted materially from target weights

- Retain a cash ETF buffer (AAA or ISEC) specifically earmarked for opportunistic deployment, separate from the regular contribution schedule

With the ASX 200 at 8,631 points as of 30 April 2026, volatility is elevated but the market has not broken down. Historical patterns indicate that supply-driven oil price shocks resolve within approximately six to twelve months, with market recovery following as rate pressures ease. A disciplined positioning approach, rather than a defensive exit, is warranted.

Inflation is not the end of portfolio returns; it is the stress test that reveals whether your structure is right

The combination described in this guide, income-generating fixed-income ETFs yielding above CPI, quality-tilted international equity exposure, and liquid capital reserves, is precisely the structure designed to perform relative to inflation rather than be eroded by it.

The inflation-aware structure: income above CPI + global diversification + liquid reserves. These three elements, working together, position a portfolio to generate real returns in a high-inflation environment rather than merely preserve nominal value.

Genuine risks remain. If the RBA continues hiking beyond 4.10%, duration risk in VBND and CRED will pressure capital values. If the Iran conflict escalates further, equity volatility may intensify before it resolves. These are not hypothetical concerns.

The historical perspective offers context without guarantees. Supply shocks, including the 1970s oil crisis and the 2022 Ukraine-driven energy spike, have resolved, and investors who maintained discipline through them captured the subsequent recovery. Disinflationary forces remain in play: AI-driven productivity gains, moderating wage growth in some sectors, and downward price pressure from redirected Chinese goods all suggest the current inflationary episode has a shelf life.

Inflation is a condition to position for, not flee from. The tools to do it are available on the ASX today.

For investors wanting to extend the framework beyond ASX-listed ETFs into assets such as Treasury Inflation-Protected Securities, infrastructure REITs, and physical gold, our full explainer on tactical inflation allocation covers how each asset class behaves across the four quadrants of the inflation cycle and how to size positions relative to a 10-15% cash buffer strategy.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

—