A 3-Layer Portfolio Strategy for Volatile ASX Markets

2 mins ago

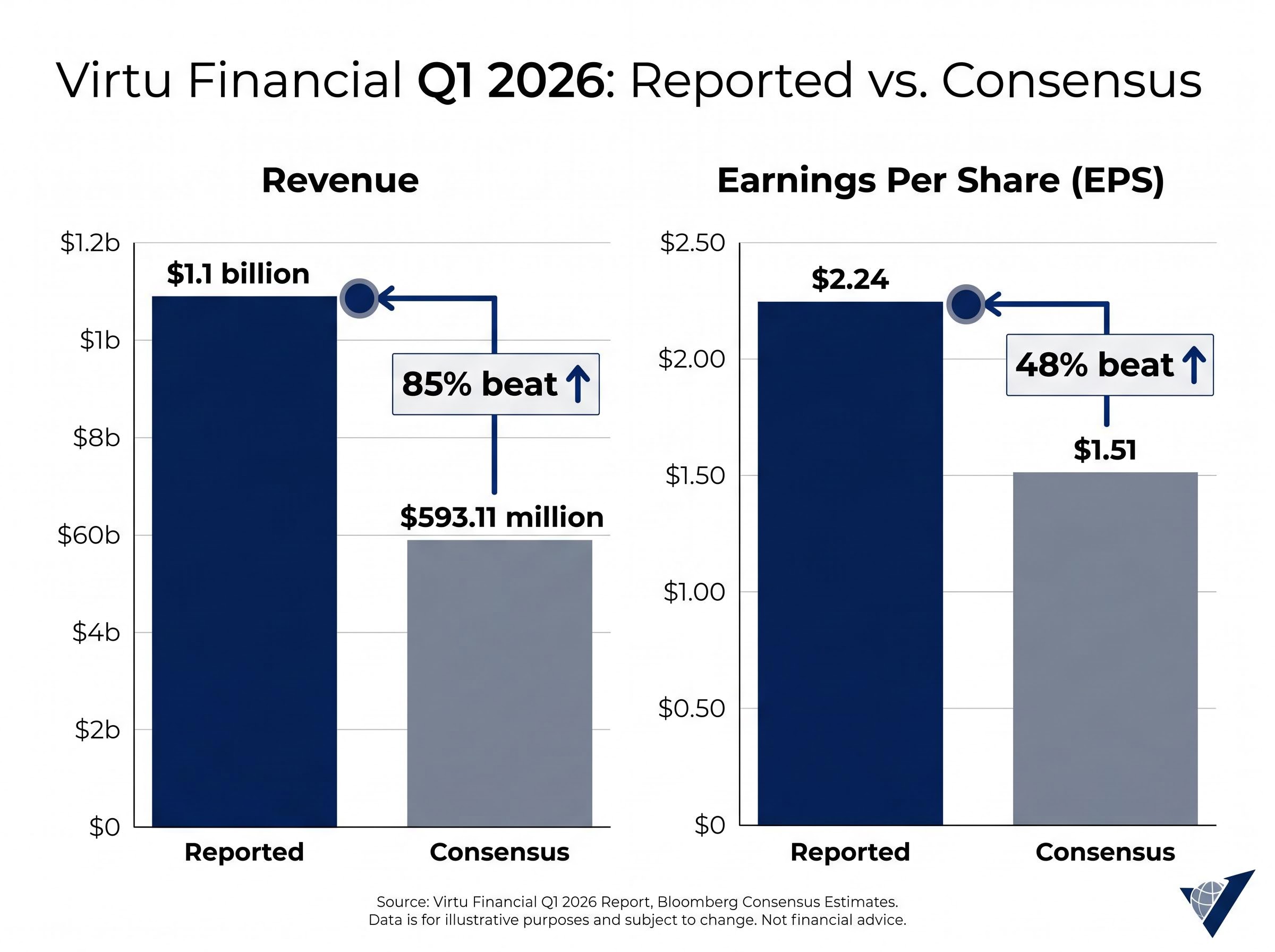

Virtu Financial just reported adjusted earnings per share of $2.24, beating the $1.51 consensus estimate by 48 percent, and yet the most important question for investors is not what just happened but whether a stock that has already climbed 48 percent year-to-date has anything left to give.

The 29 April 2026 earnings release arrived during a period of elevated cross-asset volatility that is structurally favourable for market-making firms. Shares surged nearly 6 percent in pre-market trading toward the 52-week high of $52.21. That backdrop makes the valuation question both urgent and genuinely contested: the consensus analyst price target of $48.86 sits below the current trading range, while at least one prominent platform rates the stock a Strong Buy.

What follows works through the earnings numbers, the competing valuation frameworks, the macro tailwind, and Virtu’s forward strategy to give retail investors a clear picture of what they are paying for at current prices, and whether the risk-reward remains compelling.

The headline numbers are striking even by Virtu’s own standards. Total revenue came in at $1.1 billion against a consensus estimate of $593.11 million, an 85 percent beat. Adjusted net income reached $521 million. Record aggregate daily adjusted net trading proceeds hit $787 million for the quarter, translating to a daily average of $12.9 million.

The outperformance was not concentrated in a single line. The market-making division delivered a daily average of $10.4 million, while execution services contributed $2.5 million per day. Both divisions produced at levels that suggest the quarter’s strength was broad-based rather than a one-off anomaly.

| Metric | Reported | Consensus Estimate |

|---|---|---|

| Revenue | $1.1 billion | $593.11 million |

| Adjusted EPS | $2.24 | $1.51 |

| EBITDA Margin | 66% | N/A |

EBITDA margin of 66 percent: For context, EBITDA margin measures the share of revenue retained after operating expenses. A 66 percent reading is exceptionally high for a financial services firm and reflects the degree to which Virtu’s technology infrastructure converts trading volume into profit with minimal incremental cost.

The scale of the beat matters because it signals that Virtu’s business is not merely benefiting from volatility at the margin. It is structurally positioned to convert volatile market conditions into outsized earnings, and that conversion efficiency is the core thesis investors need to weigh at current prices.

Interpreting the Q1 result requires understanding the mechanism that produced it. Virtu is an electronic market maker, meaning the firm provides continuous buy and sell quotes across thousands of instruments, earning the difference between the bid and ask prices on each transaction. The business operates across equities, fixed income, currencies, and commodities, and its technology platform is designed to execute this function at scale with minimal human intervention.

The SEC market maker obligations framework establishes that firms providing continuous quotes across listed securities must maintain fair and orderly markets, a regulatory baseline that shapes the compliance environment within which Virtu and its peers operate at scale.

Two divisions drive the economics. Each has a distinct role and a distinct earnings profile.

The current macro environment amplifies both divisions. Rate volatility, bond market dislocation, political risk, and persistent inflation concerns have created cross-asset volatility conditions that multiple institutional strategists, including those at PNC, State Street, and Morgan Stanley, have identified as likely to persist through mid-2026.

Retail investors who treat Virtu as a generic financial stock miss the distinction: this business is engineered to profit from market stress events, not endure them.

The high frequency trading economics that produced Virtu’s outsized margins are built on a fixed-cost infrastructure model: co-located servers, custom execution platforms, and quantitative systems that run at near-zero marginal cost per additional transaction, meaning every incremental dollar of trading volume flows through to earnings at a conversion rate most industries cannot approach.

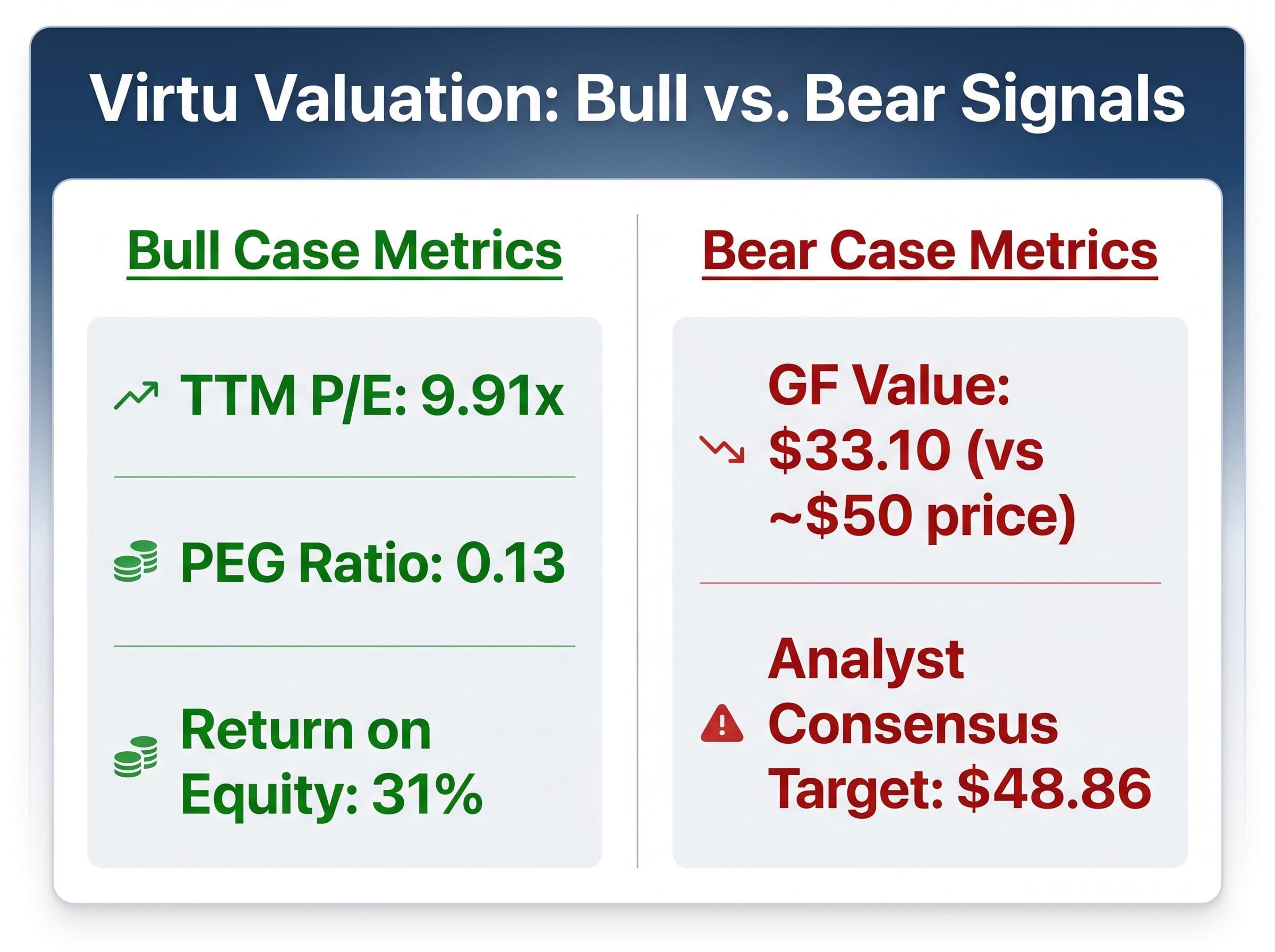

The valuation picture contains a genuine contradiction, and investors who flatten it into a single conclusion risk mispricing the stock in either direction.

The bull case rests on earnings power relative to price. The trailing twelve-month P/E ratio sits at 9.91x, historically low in absolute terms for a business generating 66 percent EBITDA margins and a 31 percent return on equity. The PEG ratio, which measures the P/E relative to expected earnings growth, stands at 0.13. A PEG below 1.0 is typically interpreted as a signal that the market has not fully priced in the forward earnings trajectory; at 0.13, the gap is unusually wide. At least six analysts raised their full-year 2026 EPS estimates following the earnings release, pushing the consensus to $10.16.

The bear case rests on intrinsic value models. GuruFocus assigns a GF Value of $33.10 against a current price near $50, implying roughly 35 percent downside. The average analyst price target of $48.86 sits below the current trading range, suggesting limited near-term upside even in the consensus view. The 52-week range of $31.55 to $52.21 places the stock near its upper bound, with the pre-market surge on 30 April 2026 pushing shares to $51.75.

| Metric | Value | Signal |

|---|---|---|

| TTM P/E | 9.91x | Bull |

| PEG Ratio | 0.13 | Bull |

| Return on Equity | 31% | Bull |

| GF Value vs. Price | $33.10 vs. ~$50 | Bear |

| Analyst Consensus Target | $48.86 | Bear |

Forward EPS estimate: $10.16. If Virtu delivers on the revised consensus for full-year 2026, the implied forward P/E at a $50 share price falls to approximately 4.9x, a level that would be difficult to sustain for a profitable, growing business unless the market is pricing in a sharp earnings reversion.

The disagreement here is not noise. It reflects a methodological tension: intrinsic value models may struggle to capture a business whose earnings are structurally tied to a volatility regime that is itself difficult to model. Investors who understand this distinction are better equipped to size a position appropriately.

A single quarter of exceptional results at one firm could be an anomaly. When the closest listed peer reports a similar pattern, the signal sharpens.

Flow Traders, the Amsterdam-listed electronic market maker and the most relevant public comparable for Virtu, reported its own Q1 2026 results:

Citadel Securities and IMC, two other major electronic market-making firms, are privately held and do not disclose comparable public metrics. Flow Traders is therefore the best available cross-validation point for listed investors.

When the best-available peer also shows double-digit year-over-year income growth and record capital deployment, Virtu’s Q1 looks like sector outperformance within a rising tide rather than a single outlier. The inference is meaningful: it suggests the earnings environment for electronic market makers is broadly favourable and may have duration beyond a single quarter.

Cross-asset volatility driven by stagflation concerns and geopolitical uncertainty has been extensively documented in 2026 market reporting, providing independent corroboration that the macro conditions underpinning Virtu’s record quarter are not a firm-specific artefact but a broadly observable market phenomenon.

The comparison has limits. Virtu operates at significantly greater scale and has a different geographic and asset-class mix. But for retail investors assessing whether the macro tailwind is real, Flow Traders provides independent corroboration that it is.

Backward-looking earnings tell investors what happened. Capital allocation and headcount decisions tell them what management expects to happen next.

Three forward-looking signals emerged from the Q1 disclosure, listed in order of their informational weight:

Virtu’s approach to talent strategy as competitive moat is more deliberate than a typical hiring expansion: the firm restricts generative AI to internal productivity tools and relies on specialist quantitative analysts and C++ engineers for core execution systems, a calculated stance that trades potential automation gains for lower systemic risk in live trading environments.

Management outlook: In commentary accompanying the Q1 release, Virtu’s leadership indicated plans to expand hiring and deploy additional capital into trading capacity through the remainder of 2026, citing the favourable volatility environment and the firm’s ability to capitalise on wider opportunity sets across asset classes.

The compensation ratio provides a check on the hiring narrative. At 22 percent for Q1 2026, labour costs remain within historical norms despite the talent acquisition push. The quarterly dividend of $0.24 per share, unchanged from prior periods, signals capital discipline alongside growth investment.

When hiring, capital deployment, and the compensation ratio all point in the same direction, the signal is that management believes the current earnings environment is durable.

The stock has appreciated 48 percent year-to-date and 44 percent over the trailing six months. It trades near $50, within reach of its 52-week high of $52.21. The consensus analyst target of $48.86 already sits roughly 2 percent below the current price.

Against those figures, the forward P/E implied by the $10.16 consensus EPS estimate is approximately 4.9x at a $50 share price. That is an unusually low multiple for a business with this margin and return profile, which is why the bull-bear debate remains live despite the run-up.

Conditions that support the bull case:

Conditions that support the bear case:

The burden of proof for a new position at $50 is higher than it was at $35. Investors considering an entry at current levels need a view on whether the volatility regime has duration, not merely whether the last quarter was strong.

Regulatory scrutiny and margin risks represent the structural headwinds that valuation models must price alongside the earnings power argument: prolonged periods of low volatility, tightening oversight of algorithmic trading practices, and escalating talent acquisition costs each have the capacity to compress the compensation ratio above the current 22 percent threshold without a proportionate revenue offset.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.

Virtu’s Q1 2026 results were genuinely exceptional: $1.1 billion in revenue, a 66 percent EBITDA margin, and a $2.24 adjusted EPS that exceeded consensus by nearly half. The business model performed exactly as designed during a period of elevated cross-asset volatility, and Flow Traders’ results confirm the tailwind was sector-wide.

The tension sits in what comes next. The stock trades near its 52-week high with the consensus price target already behind it, yet the implied forward P/E of approximately 4.9x on $10.16 in consensus earnings suggests the market is pricing in a significant earnings reversion. The most actionable consideration for investors is whether that reversion materialises.

The next catalyst is Q2 2026 earnings. The metric to watch is whether average daily net trading income remains near the record $12.9 million level or reverts as volatility conditions normalise. That single data point will do more to resolve the valuation debate than any model can.

Virtu Financial is an electronic market maker that earns revenue by providing continuous buy and sell quotes across thousands of financial instruments, profiting from the bid-ask spread on each transaction across equities, fixed income, currencies, and commodities.

Virtu reported adjusted EPS of $2.24, beating the $1.51 consensus estimate by 48 percent, with total revenue of $1.1 billion against a consensus of $593 million, driven by elevated cross-asset volatility that boosted both trading volumes and bid-ask spreads.

The forward P/E of approximately 4.9x based on the $10.16 consensus EPS estimate suggests potential undervaluation, but the consensus analyst price target of $48.86 sits below the current trading range, meaning investors must weigh whether elevated volatility conditions will persist through H2 2026.

Key metrics include a trailing P/E of 9.91x, a PEG ratio of 0.13 (well below the 1.0 threshold), a 31 percent return on equity, and a GF Value of $33.10 from GuruFocus, which implies significant downside from current prices near $50.

The primary risks include a sharp normalisation in cross-asset volatility that would compress both trading volumes and bid-ask spreads, diminishing returns on the $500 million capital injection, and a rising compensation ratio if the planned hiring push outpaces revenue growth.