The most consequential day of the big tech earnings season has arrived, carrying a staggering derivatives pricing setup that indicates a potential $750 billion valuation swing pending the 4:00 PM EST bell today. On 29 April 2026, the simultaneous financial reports of Alphabet, Amazon, Meta, and Microsoft will dictate immediate market direction. Wall Street is looking far beyond headline revenue figures to expose the underlying infrastructure anxieties currently driving institutional sentiment.

Investors require a clear breakdown of capital expenditure metrics and artificial intelligence monetisation timelines. These detailed disclosures will determine if the sector’s recent spending phase remains sustainable.

Extreme Options Market Volatility Setup

Options market pricing translates abstract derivatives mathematics into immediate market fragility. Traders are pricing in post-earnings price movements of 5% to 7% across all four technology companies. While no verified pricing explicitly confirms the rumoured $750 billion figure, the mathematics align perfectly with a 5% to 7% swing across their combined market capitalisations.

Such dramatic pricing often precedes an implied volatility crush that collapses option premiums immediately following the earnings call, regardless of whether the stock moves in the anticipated direction.

The immediate trading context reveals significant divergence in year-to-date momentum. Alphabet stock has surged 118.65% over the past year, while Microsoft is down 11.97% year-to-date. Technology-focused index futures increased prior to regular trading hours, establishing a tense atmosphere ahead of the closing bell.

This setup explains exactly how much volatility the market expects today, allowing investors to categorise sudden post-market price movements.

| Company | Year-to-Date Performance | Options-Implied Move |

|---|---|---|

| Alphabet | +12.0% | 5% to 7% |

| Amazon | +13.13% | 5% to 7% |

| Meta | +2.89% | 5% to 7% |

| Microsoft | -11.97% | 5% to 7% |

When big ASX news breaks, our subscribers know first

Understanding the Artificial Intelligence Capital Expenditure Reality

Wall Street anxiety stems directly from the physical reality of data centres and the sheer cost of purchasing advanced computing power. The scale of required infrastructure investment is testing investor patience across the technology sector. Sustaining an artificial intelligence infrastructure advantage is increasingly viewed by analysts as a potential liability rather than a guaranteed asset.

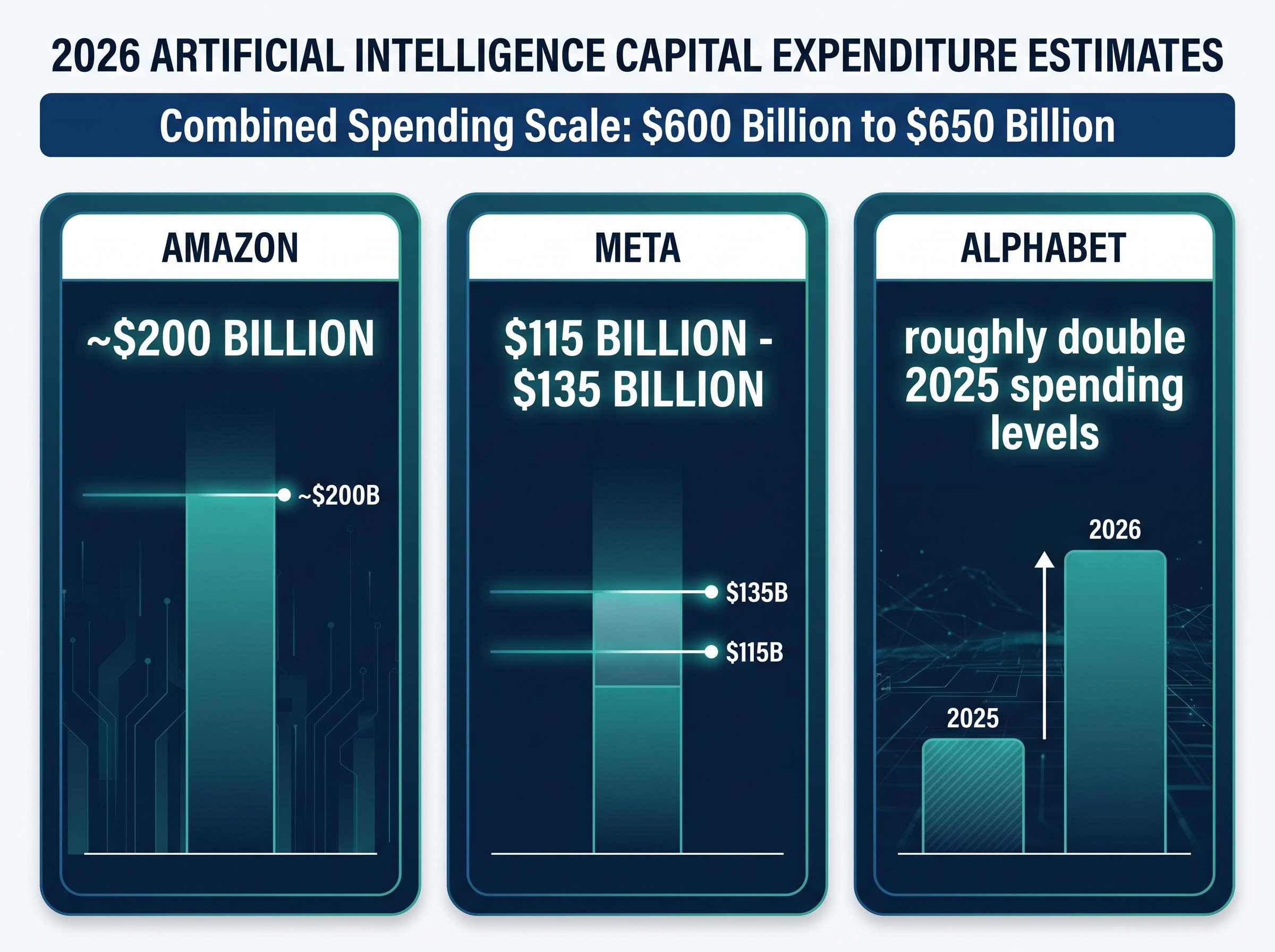

Combined Spending Scale Analysts estimate the combined 2026 capital expenditures for these four companies will reach between $600 billion and $650 billion.

Meta has set its 2026 spending guidance between $115 billion and $135 billion, representing a massive 67% to 97% increase from 2025. Amazon expects capital expenditures of approximately $200 billion. Alphabet is guiding to roughly double its 2025 spending levels.

The Return on Investment Timeline

A growing disconnect exists between when these funds are spent and when companies recognise the resulting revenue. Wall Street analysts are increasingly demanding concrete proof of commercial returns to justify the historic outlay.

This massive capital allocation translates abstract financial metrics into a clear risk factor. The current data shows why record-breaking spending might punish stock prices if immediate monetisation remains unproven.

For readers wanting to track how quickly these investments convert to revenue, our deep-dive into cloud service monetization timelines examines early enterprise adoption rates across major platforms like Amazon Web Services and Google Cloud.

OpenAI Concentration and Microsoft Earnings Vulnerability

The current earnings cycle positions Microsoft as the ultimate test case for the broader artificial intelligence revenue narrative. The company faces unique exposure due to its heavy reliance on OpenAI achieving its commercial goals. In prior quarters, Microsoft stock fell despite overall revenue growth, directly reacting to escalating infrastructure costs that dragged on profit margins.

Today’s earnings call serves as the bellwether for the entire technology sector. The market will judge whether a fundamentally strong enterprise can avoid a sell-off while aggressively expanding its computing capacity.

This aggressive capacity expansion introduces a software monetization lag where application revenue struggles to keep pace with the massive hardware deployment costs hitting the balance sheet.

Specific headwinds facing Microsoft today include: First-quarter capital expenditures reaching $36.2 billion A 45% commercial remaining performance obligations concentration risk Target market demands for 37-38% Azure cloud growth Recent industry reports indicating OpenAI is missing internal commercial and engagement targets

This specific concentration risk highlights exactly what metrics will determine the company’s valuation trajectory this afternoon.

Core Business Lifelines for Alphabet, Amazon, and Meta

Traditional core operations continue to generate massive cash flow, acting as a release valve for infrastructure anxieties. Resilient retail and advertising environments are effectively subsidising the generational pivot to new technologies. Positive core business results in e-commerce and search could offset institutional concerns regarding computing investments.

These underlying business models remain highly profitable, providing the financial foundation necessary to fund continued expansion.

Ranked by expected total revenue growth, the specific core drivers for each company include:

- Alphabet is projecting 19% year-over-year growth to $107 billion in total sales, driven by an expected jump in cloud revenues.

- Microsoft consensus estimates project 17% earnings per share growth, heavily dependent on traditional software and Azure cloud adoption.

- Amazon targets consensus revenue between $173 billion and $178 billion, relying on its cloud division targeting annual growth.

- Meta anticipates first-quarter sales beating consensus estimates of $55.56 billion on the back of sustained advertising strength.

The Semiconductor Systemic Risk Factor

The spending plans of these four mega-cap companies connect directly to semiconductor valuations, establishing a clear cause-and-effect relationship across the broader market. Even investors who do not own these specific technology names hold heavy portfolio exposure through chipmakers. Any reduction in forward infrastructure guidance from today’s reports will disproportionately punish semiconductor manufacturers.

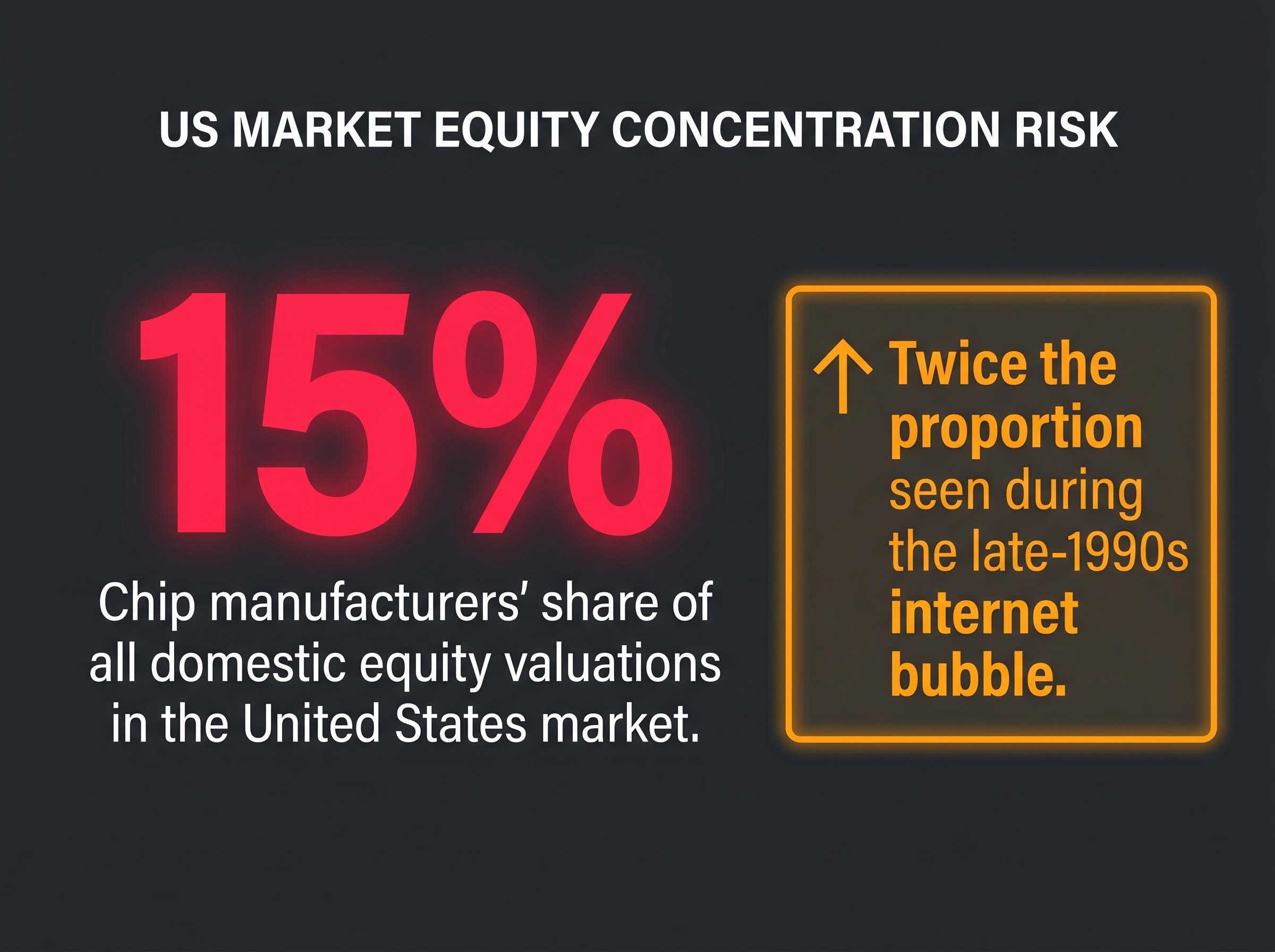

Historical Bubble Comparisons

According to market data, chip manufacturers currently comprise almost 15% of all domestic equity valuations in the United States market. This concentration represents twice the proportion seen during the peak of the historical late-1990s internet bubble. Market strategists warn that the current upward market rally is highly vulnerable to a sharp retracement if technology spending slows.

Analysts note that escalating inference costs continue to challenge the profitability of generative applications, a structural flaw that could force hyperscalers to drastically reduce future equipment orders.

A miss by Meta or Microsoft could easily trigger a broader market correction. This interconnected relationship reveals the hidden leverage currently built into the financial system.

What to Watch After the Closing Bell

When the reports drop at 4:00 PM EST, the immediate market reaction will focus on forward-looking projections. Guidance for the second quarter will dictate price action far more than any first-quarter beats or misses.

This afternoon will serve as the ultimate test of durability for the current technology rally. Investors must monitor capital expenditure forecasts closely, as they provide the clearest signal of future corporate strategy.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.