Big Tech Earnings Face $600B AI Reality Check Today

1 min ago

Generac stock is in focus in early market trading on 29 April 2026, ahead of a first-quarter earnings report that could fundamentally rewrite the company narrative. Analysts had anticipated moderate, steady growth heading into the pre-market release. However, the actual top and bottom-line figures revealed an operation successfully capitalising on the unprecedented power demands of artificial intelligence and data centre infrastructure.

The immediate market reaction reflects a repricing of the business model from a consumer hardware manufacturer to an enterprise power provider. This analysis provides a clear breakdown of the financial metrics that drove the morning rally and the mechanics behind the rapidly expanding commercial backlog. It also examines what the upgraded full-year guidance means for long-term investors tracking the transition toward commercial infrastructure.

Total first-quarter revenues are expected to reach the $1.05 billion Wall Street consensus forecast. This performance represents a 12 percent year-over-year revenue expansion compared to the $942 million recorded in Q1 2025. Generating this level of top-line growth signals accelerating operational momentum across the core business divisions.

Early financial coverage analysing Generac’s earnings beat confirms this strong revenue performance, cementing the narrative that commercial infrastructure demand is successfully replacing legacy consumer sales.

The primary catalyst for the stock surge was a substantial $0.45 outperformance on adjusted per-share profits. The company is expected to report adjusted earnings per share meeting the projected $1.33 Wall Street estimate. Investors needed to see exactly how much the company outperformed expectations to determine if the morning trading movement was fundamentally justified.

The magnitude of this profit beat delivers a hard financial reality that validates the aggressive equity purchasing. Delivering an earnings beat of this size demonstrates that the shift toward higher-margin commercial contracts is already yielding tangible bottom-line results. Early trading equity valuations jumped nearly 14 percent as institutional capital adjusted to the accelerated profitability timeline.

| Metric | Q1 2026 Actuals | Wall Street Consensus | Q1 2025 Actuals | Year-Over-Year Growth |

|---|---|---|---|---|

| Adjusted Earnings Per Share | $1.80 | $1.33 | N/A | Beat by $0.45 |

| Total Revenue | $1.06B | $1.05B | $942M | +12% |

This level of profitability indicates that fixed costs are being effectively absorbed by higher production volumes. The combination of double-digit revenue expansion and a massive earnings beat provides the fundamental justification for the equity repricing.

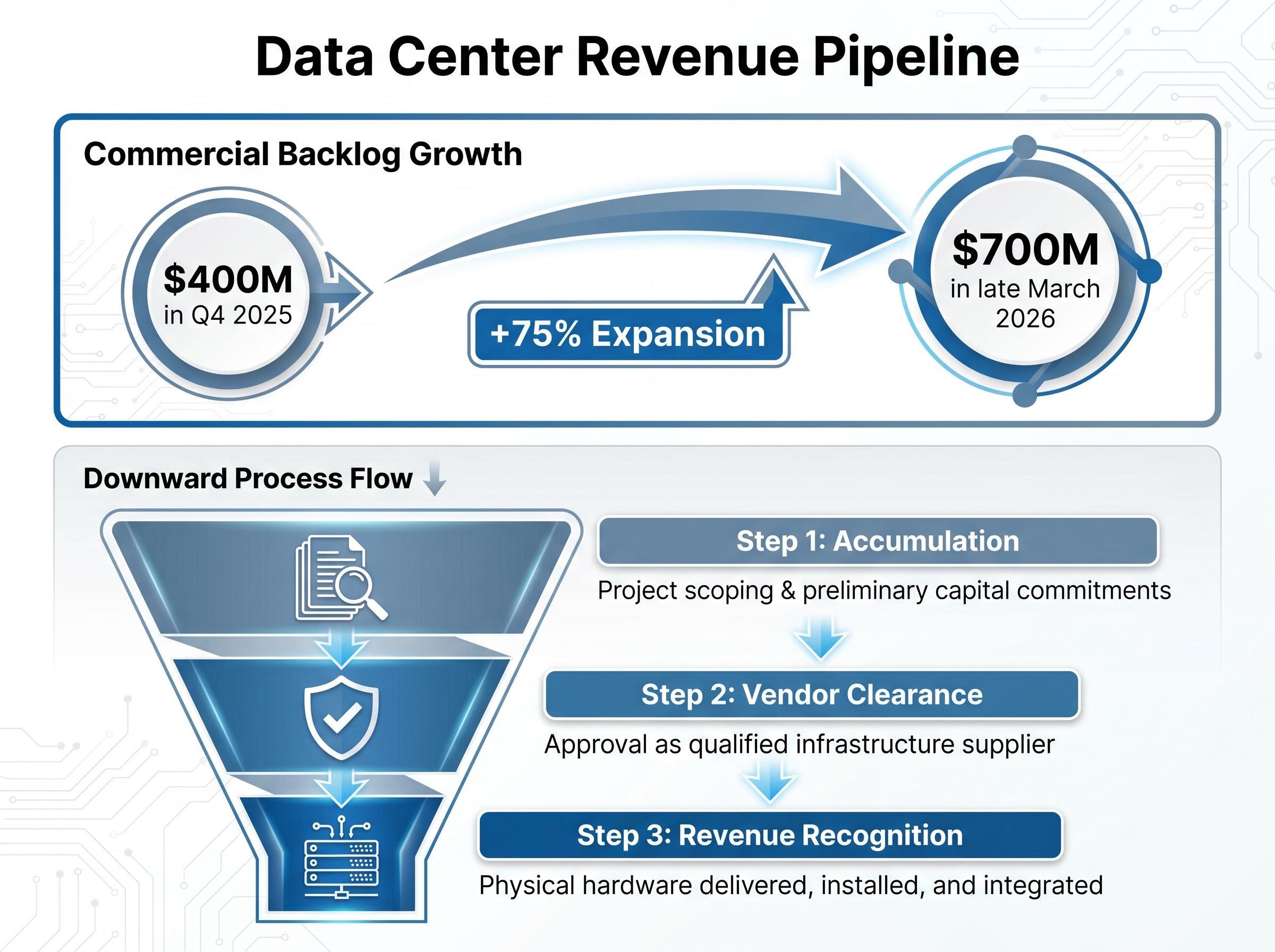

The focus now shifts from raw historical numbers to the mechanics of infrastructure growth. Late-stage vendor clearance processes with large-scale data centre clients serve as a critical driver of future earnings visibility. Retail investors tracking this sector must understand why navigating these clearance processes dictates future revenue flow.

In the context of hyperscale facilities, late-stage vendor clearance means an equipment provider has passed rigorous technical audits and is approved to bid on final procurement contracts. These enterprise-level technology clients require exact specifications for uninterrupted power generation. Becoming an approved supplier for these operators transforms prospective discussions into tangible, executable contracts.

The International Energy Agency projects global data center power demand to more than double by 2030, creating a massive total addressable market for infrastructure providers that can meet these rigorous AI-driven specifications.

Pre-earnings data showed the commercial backlog expanded by approximately 75 percent over a single quarter. This specific pipeline rose from $400 million in Q4 2025 to $700 million by late March 2026. Translating this massive backlog into recognised revenue typically follows a distinct three-step progression:

This progression clarifies the complex corporate terminology, showing exactly how the current backlog secures future revenue streams.

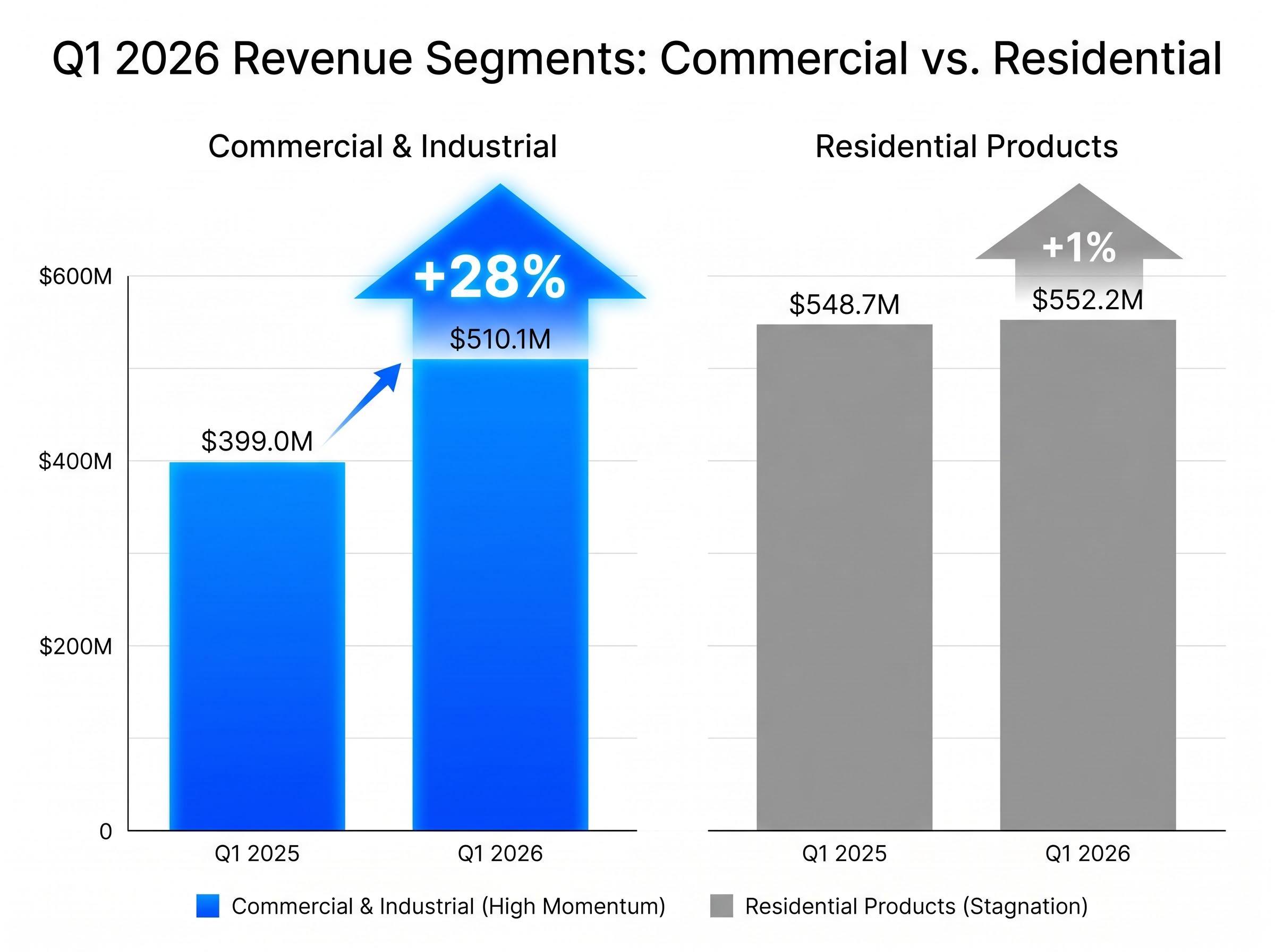

The stark divergence in growth rates between the business-facing and consumer-facing divisions illustrates a fundamental rewiring of the corporate model. Commercial and industrial segment revenues surged roughly 28 percent to $510.1 million, up from $399.0 million in the prior year. This industrial division is now the undeniable growth engine for the entire operation.

Conversely, the residential product category increased a marginal 1 percent to $552.2 million, compared to the $548.7 million prior-year baseline. This near-flat performance in the residential category is not a critical failure, but rather a sign of successful operational diversification. The company is no longer solely dependent on severe weather events driving unpredictable home generator sales.

“Our first-quarter results demonstrate the successful diversification of our operational structure, allowing us to capture demand in enterprise power markets while maintaining our residential market share,” management noted regarding the strategic shift.

This context shows investors that the firm is now a vital industrial infrastructure play capable of offsetting consumer market stagnation.

| Segment | Q1 2026 Revenue | Q1 2025 Revenue | Percentage Change |

|---|---|---|---|

| Commercial and Industrial | $510.1M | $399.0M | +28% |

| Residential Products | $552.2M | $548.7M | +1% |

The data confirms that the commercial segment will soon outpace the legacy residential business if current adoption rates hold. This transition fundamentally lowers revenue volatility, replacing weather-dependent sales spikes with predictable, large-scale infrastructure contracts.

For readers evaluating broader risks to commercial capital expenditures, our deep-dive into escalating US recession risks explores how surging global crude prices and tightening economic conditions could impact future corporate infrastructure budgets.

The first-quarter beat is part of an accelerating operational trajectory supported by strategic mergers and acquisitions. Management detailed specific upward revisions to the full-year 2026 financial guidance. Anticipated full-year sales expansion reiterates earlier mid-teens projections.

Leadership connected the upcoming Enercon Engineering integration directly to these strengthened forward-looking expectations. The addition of Enercon is expected to yield integration efficiencies that directly fund the newly upgraded margin targets. Adjusted EBITDA margin expectations have increased to a range of 18.5 to 19.5 percent.

Expanding custom power engineering capabilities through rapid strategic integrations allows the firm to capture more lucrative segments of the enterprise supply chain.

The specific before-and-after metrics of the full-year 2026 guidance upgrade include:

Projected overall net sales expansion upgraded from mid-teens to mid-to-high teens. The adjusted EBITDA margin expectation floor raised to 18.5 percent, with a ceiling of 19.5 percent. * A new targeted median EBITDA margin of 19.0 percent, replacing the previously projected 18.5 percent benchmark.

The Enercon transaction is expected to officially close in the second quarter of 2026. Once finalised, the acquisition will provide specific EBITDA margin benefits driven by improved volume absorption in the switchgear market. Switchgear systems are critical for controlling and protecting electrical equipment in high-capacity environments.

Securing this supply chain allows the firm to deliver complete, integrated power solutions to data centre operators. This capability directly accelerates the conversion of the commercial backlog into recognised revenue.

The massive first-quarter results validate the strategic pivot toward industrial power solutions. The 14 percent market reaction reflects a clear repricing of the stock based on commercial data centre demand rather than legacy residential sales cycles. Institutional capital is now modelling the firm as an infrastructure provider tied to artificial intelligence expansion.

This crucial positioning provides a definitive advantage as persistent data storage hardware constraints and widespread component shortages continue to bottleneck facility buildouts across the tech sector.

Investors should closely monitor the finalisation of the Enercon acquisition in the second quarter of 2026. Completing this integration is the next necessary step to ensure the company has the physical capacity to service its $700 million commercial backlog.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

Past performance does not guarantee future results. Financial projections and statements regarding acquisitions are speculative and subject to market conditions, regulatory approvals, and company performance.

Generac stock rallied 14 percent due to substantial earnings per share outperformance and strong revenue growth, signaling a successful strategic pivot toward high-margin commercial power solutions for data centers and AI infrastructure.

The Q1 2026 results show Generac transitioning from a consumer hardware manufacturer to an enterprise power provider, with commercial and industrial segment revenues surging 28 percent while residential growth remained marginal.

Generac's commercial backlog expanded 75 percent to $700 million, securing future revenue streams, while the upcoming Enercon Engineering acquisition is expected to boost EBITDA margins and enhance switchgear capabilities crucial for fulfilling data center contracts.

Late-stage vendor clearance means Generac has passed rigorous technical audits and is approved to bid on final procurement contracts with hyperscale data center clients, turning prospective discussions into tangible, executable agreements.