The US software market has suffered its most severe wealth destruction event in two decades, yet institutional capital is actively accelerating its deployment. A staggering $2 trillion in market capitalisation evaporated from legacy software equities in early 2026, colliding with a massive $1.2 trillion wave of merger and acquisition activity. The sheer velocity of this capital rotation has fractured traditional valuation models across the technology sector.

The gap between these metrics reveals how the AI disruption in tech is actively reallocating enterprise value rather than simply destroying it. Capital is rapidly migrating away from bloated headcount-dependent platforms and flowing directly toward highly efficient synthetic infrastructure. For US investors, this historic divergence demands a structural reassessment of software portfolios to separate durable platforms from fundamentally obsolete models.

The Great Repricing and the New Reality of Software Markets

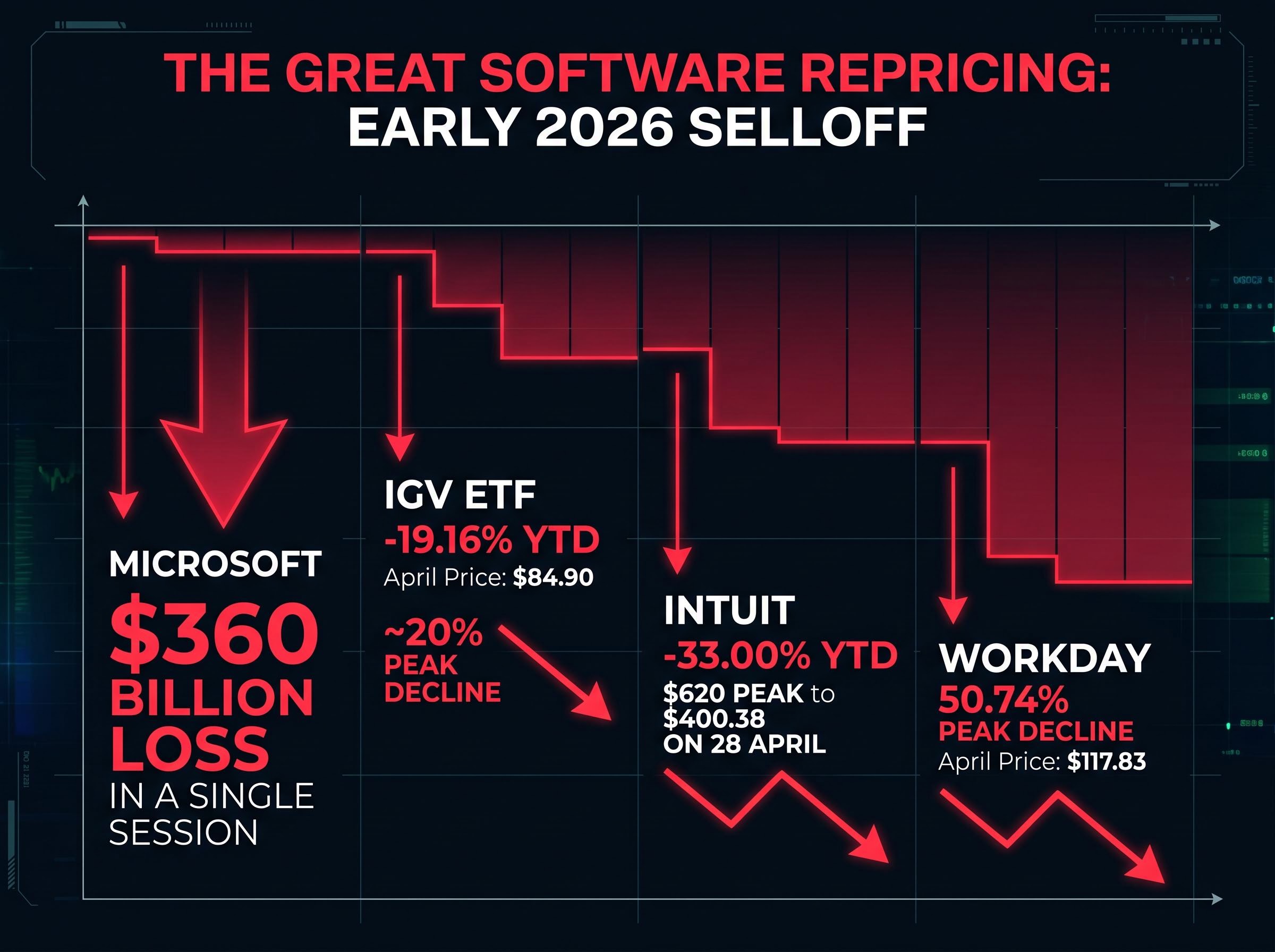

The velocity of the early 2026 market shift shattered conventional valuation metrics across the technology sector. In just 30 days, $2 trillion was wiped out across the software ecosystem, catching many institutional portfolios entirely off guard.

The destruction was heavily concentrated at the top, punctuated by Microsoft shedding $360 billion in a single trading session. This was not a standard macroeconomic pullback driven by interest rates, but a targeted repricing of legacy software-as-a-service models.

The iShares Expanded Tech-Software ETF (IGV) captures this precise dynamic. The fund sits at a negative 19.16% year-to-date return as of 27 April 2026, reflecting deep sector-wide capitulation.

| Asset | Year-to-Date Performance | April 2026 Price | Peak Decline |

|---|---|---|---|

| IGV ETF | -19.16% | $84.90 | ~20% (below 200-day MA) |

| Intuit | -33.00% | $400.38 | 35-40% |

| Workday | 24% decline from early February 2026 peaks | $117.83 | 50.74% |

Major Casualties in the US Equity Selloff

The timeline of individual equity declines illustrates the severity of the institutional rotation away from legacy vendors. Intuit collapsed from its early 2026 peaks near $620 to close at $400.38 on 28 April 2026. Workday followed a similar downward trajectory, losing 50.74% of its value over the past year, with cumulative losses from its all-time high exceeding 50% as deployment fears accelerated.

These steep selloffs mirror historical sector corrections in their speed and severity. By mid-March, the IGV had dropped roughly 20% below its 200-day moving average. Market analysts note this represents the widest technical gap since the 2000 dot-com crash, underscoring the permanent structural repricing US investors are currently facing.

For investors exploring the broader macro triggers behind these severe pullbacks, our detailed coverage of market correction risks examines how ongoing geopolitical tensions and automated trading algorithms are actively distorting global equity valuations.

When big ASX news breaks, our subscribers know first

Decoding Seat Compression and the Commoditisation of Code

The collapse of legacy technology valuations traces back to a fundamental breakdown in how enterprise software generates revenue. For two decades, software-as-a-service companies scaled their operations by charging per human employee, a system commonly known as the seat-based model. This established revenue structure is now fracturing under the rapid acceleration of seat compression.

Seat compression occurs when autonomous digital agents replace human operators, immediately destroying the enterprise requirement for multiple paid user licences. Goldman Sachs data reveals that over 10,000 venture-backed startups are currently targeting the $400 billion global software market with these highly automated solutions. As artificial intelligence handles complex corporate workflows natively, businesses simply need significantly fewer human operators to achieve the same output.

The NBER research on AI agents models this exact macroeconomic shift, demonstrating how synthetic operators fundamentally alter organizational design and reduce traditional workforce licensing requirements.

This transition represents a permanent structural change in global digital consumption. AllianceBernstein tracked the MSCI World Software and Services Index, noting it dropped over 20% by the end of February 2026. Their analysis attributed this decline entirely to widespread institutional fears surrounding autonomous agent deployments.

The distinction between legacy systems and emerging models dictates future investment viability:

Legacy per-user licensing: Revenue scales linearly with corporate headcount, making platforms highly vulnerable to workforce automation and efficiency gains. Emerging consumption-based models: Revenue scales directly with compute usage and data volume, aligning costs securely with actual platform utility. * Agent-driven frameworks: Value is derived strictly from completed automated tasks rather than the amount of time human operators spend navigating inside an interface.

By understanding the mechanics of seat compression, investors can accurately identify which technology companies possess resilient pricing architectures. Legacy vendors relying on bloated headcount metrics are structurally exposed to ongoing value destruction.

The Incumbent Survival Strategy Through Mega-Acquisitions

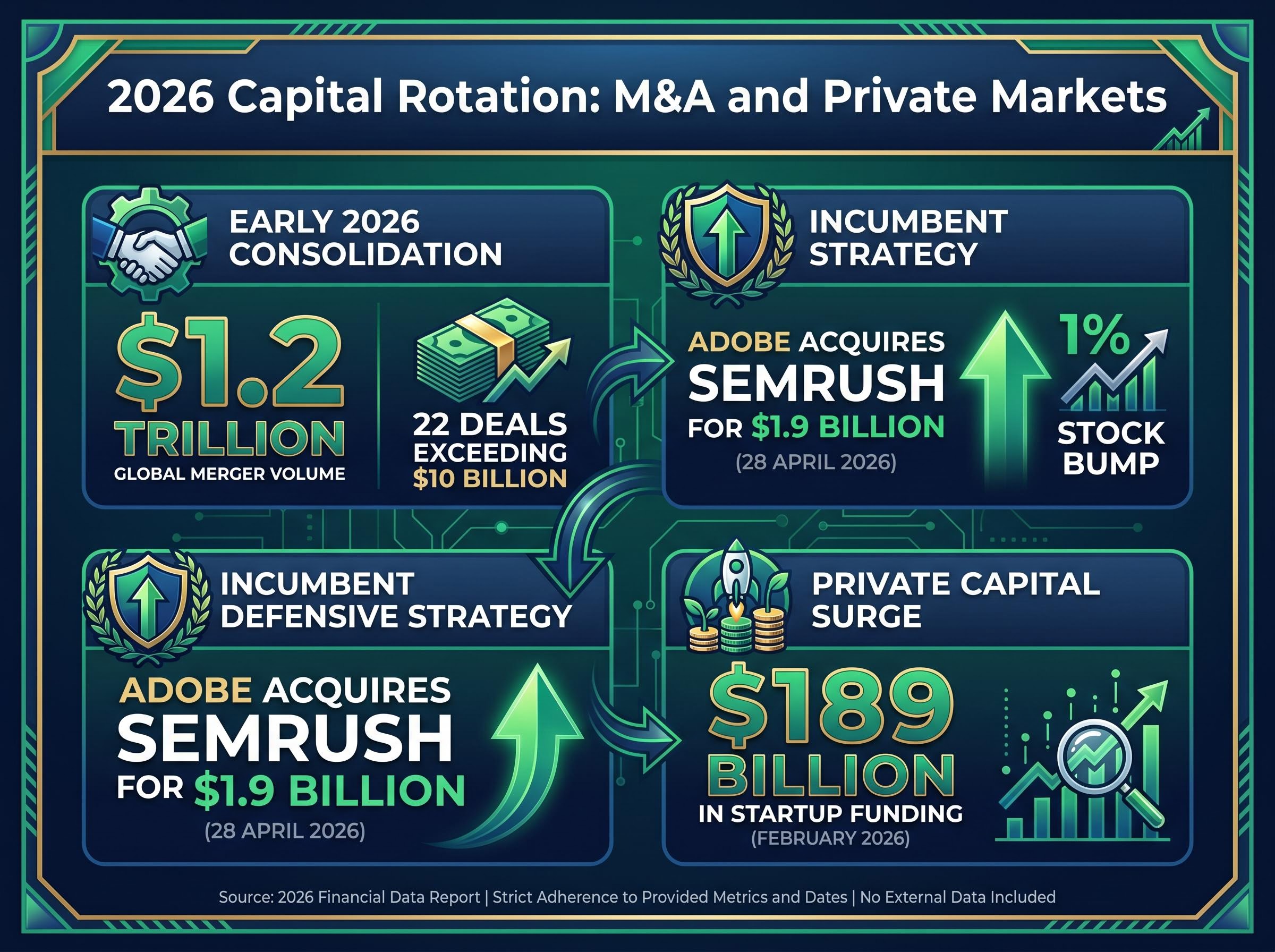

While the broader software index bled capital, legacy technology giants leveraged their massive balance sheets to acquire their way out of obsolescence. Global merger volume hit $1.2 trillion in early 2026, driven almost entirely by aggressive sector consolidation. The market recorded 22 massive deals exceeding $10 billion, explicitly tied to foundational technology acquisitions.

Adobe provides the clearest real-time blueprint for this defensive survival strategy among software incumbents. The company completed a $1.9 billion acquisition of Semrush yesterday, on 28 April 2026. This transaction was strategically engineered to integrate advanced data capabilities and protect the company against the rapid commoditisation of legacy digital marketing workflows.

Analytical Perspective on Defensive Acquisitions “The Adobe transaction demonstrates how incumbent giants are mitigating algorithmic risk by acquiring established data pipelines. This represents a necessary fortification against foundational models bypassing traditional search interfaces entirely.”

The market reaction to these aggressive corporate manoeuvres serves as a strong signal of institutional approval. Adobe received an immediate 1% stock bump following the transaction closure, validating the underlying defensive logic. Tracking these legacy buyout patterns reveals massive commercial opportunities across the broader technology ecosystem. Investors positioned in specialised, data-rich acquisition targets can capture significant premiums as legacy giants race to adapt their core architectures.

Private Capital and the Rise of Native Platforms

The capital fleeing legacy software platforms has not exited the broader technology sector entirely. Instead, it has forcefully rotated into unconstrained private ventures building synthetic intelligence infrastructure from the ground up. In February 2026 alone, private markets recorded a staggering $189 billion in startup funding, highlighting a massive institutional reallocation of risk capital.

Early 2026 PitchBook venture capital data confirms this reallocation is heavily concentrated in native artificial intelligence infrastructure, validating the institutional shift away from legacy application development.

This wave of institutional funding is aggressively targeting organisations that operate completely free of legacy technical debt. Smart money is actively pivoting away from generic cloud analytics applications. Capital is now moving decisively toward synthesised, automated corporate infrastructure platforms that demonstrate immediate utility.

Valuation Milestones in the New Infrastructure

The financial trajectories of specific private entities illustrate exactly where Wall Street is placing its long-term architectural bets. Profound was involved in notable recent strategic transactions. Concurrently, data infrastructure provider Hightouch offers a compelling operational case study in calculated growth dynamics.

Hightouch recently secured funding in its latest funding round. The company deliberately deferred profitability for two years to capture early market share. This strategy intentionally prioritised product innovation and raw technical dominance over immediate margin expansion.

Key financial milestones defining the Hightouch expansion strategy include:

* Securing top-tier institutional backing that explicitly validates the strategy of prioritising architectural dominance over short-term cash flow metrics.

Monitoring these private venture flows highlights the next generation of potential initial public offerings. It reveals precisely how institutional capital currently evaluates the structural efficiency of native platforms against legacy benchmarks.

Institutional Playbooks for Capital Allocation

The sheer volume of recent market data requires a disciplined framework to separate genuine investment signals from macroeconomic noise. Major US financial institutions have updated their guidance to help investors evaluate software investments moving forward. These frameworks focus almost exclusively on technical defensibility and architectural rebirth.

Morgan Stanley analysts recently identified a $100 billion revenue opportunity specifically reserved for highly resilient software incumbents. They argue that the recent selloffs represent a stark overreaction for companies possessing deeply embedded enterprise workflows. Similarly, AllianceBernstein advises clients to distinguish carefully between structurally exposed firms and durable businesses that command true pricing power.

Goldman Sachs provides the most aggressive forward outlook, viewing the entire software sector as undergoing a structural rebirth. They recommend focusing institutional capital on the total re-architecture of legacy systems using advanced language models. The sustained outperformance of foundational infrastructural providers like NVIDIA and Palantir confirms that markets will heavily reward raw computational utility.

This relentless institutional demand for computational utility has fueled a historic semiconductor supercycle, with hyperscalers deploying massive capital directly toward physical hardware and data centre construction.

The institutional consensus strategy for capital rotation follows a specific sequential framework:

- Assess portfolio vulnerability by identifying companies strictly reliant on traditional per-user licensing models.

- Rotate capital toward foundational infrastructural providers that profit from aggregate computing volume regardless of the specific software winner.

- Target durable incumbents demonstrating aggressive, defensive acquisition strategies designed to protect existing market share.

- Monitor private market valuations to identify consumption-based pricing models that represent the definitive future standard of enterprise software.

- Deploy capital into firms exhibiting clear technical defensibility rather than catching falling knives in indiscriminate sector selloffs.

Navigating the Next Phase of Technological Evolution

The unprecedented repricing of US equities highlights a fundamental shift from traditional software-as-a-service to consumption-based synthetic networks. Capital is emphatically not leaving the technology sector. It is ruthlessly rotating to reward structural efficiency while severely penalising legacy corporate bloat.

The sheer scale of the $1.2 trillion merger volume recorded in early 2026 serves as a vital leading indicator for future market movements. Investors should expect this aggressive acquisition activity to persist at high velocity through the remainder of the year. Incumbents will continue scrambling to acquire native capabilities before their core business models become entirely obsolete.

However, the aggressive pursuit of these physical hardware capabilities faces severe supply chain bottlenecks, prompting Wall Street to increasingly scrutinise the delayed commercial monetisation of such massive capital outlays.

By focusing on infrastructural resilience and consumption-based pricing models, market participants can successfully navigate this volatile environment.

This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions. Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors.