AI Disruption in Tech: the $2T Legacy Software Repricing

5 mins ago

Evaluating an investment in Latour stock currently requires reconciling a jarring contrast between market sentiment and historical reliability. Following the release of its first-quarter financial update in late April 2026, aggregated data initially pointed to a near 20% market plunge, testing the patience of shareholders accustomed to an unbroken 19-year history of continuous dividend payouts. The broader market reacted negatively to lagging benchmark comparisons and foreign exchange fears.

Beneath this turbulent surface, the underlying commercial demand tells a completely different story. This analysis delivers a clear, data-driven evaluation of the recent valuation drop. It determines whether the current pricing represents a fundamental breakdown in the business model or a temporary commercial buying opportunity.

The initial shock of the steep stock decline commanded immediate market attention. Over the initial trading sessions following the earnings release, the stock valuation remained stable without dramatic drops, before live market data confirmed stabilising closing prices near 215 SEK. According to company data, this headline retreat mirrored a reported drop in net asset valuation (NAV), which fell 5.9% year-over-year to 203 SEK per share.

Analysts reviewing the Investment Latour earnings report have noted that this pullback created a rare market discount relative to net asset value, a highly unusual scenario for a holding company that typically trades at a significant premium.

However, severe foreign exchange conversion obstacles heavily masked the company’s actual operational momentum. Unfavourable currency translations negatively impacted quarterly corporate revenue by approximately 6%. When isolating the core markets from these monetary fluctuations, the baseline expansion showed a solid 5% increase in incoming requests.

The wholly-owned industrial divisions also secured a 4% advance in invoiced merchandise during the same period. This positive non-acquired expansion proves the fundamental business continues to grow, even as exchange rates obscure the top-line figures.

| Metric Category | Market Headline Figure | Underlying Operational Reality |

|---|---|---|

| Stock Valuation Impact | 19.73% initial drop | Prices stabilised near 215 SEK |

| Net Asset Value (NAV) | 5.9% decline to 203 SEK | Negative translation effect only |

| Corporate Revenue | Impacted by 6% currency drag | Invoiced merchandise advanced 4% |

| Forward Demand | Overshadowed by NAV drop | Incoming requests increased 5% |

Understanding why resilient industrial groups can appear weak on paper requires examining the structural realities of international holding companies. A Swedish entity with global operations is uniquely vulnerable to Swedish Krona (SEK) fluctuations. When the local currency appreciates, international revenues translate into fewer local dollars, creating paper losses even when local operations remain highly profitable.

This dynamic explains the stark difference between reported net asset value declines and the actual cash flow generation within the proprietary divisions. The underlying business engines are accelerating, but the translation math temporarily penalises the consolidated balance sheet. According to company data, total consolidated debt obligations sit at 15.3 billion SEK, representing an 11% ratio against total investment market worth.

This low debt ratio and the purely translational nature of the revenue hit explain why analyst consensus largely maintains Hold or Buy ratings despite the initial market panic.

Broader ING macroeconomic currency forecasts support this optimistic consensus, noting that the disruptive phase of Swedish Krona appreciation should moderate throughout the remainder of the year.

Macroeconomic Currency Outlook Macroeconomic forecasts from CIBC and ING suggest the current exchange rate headwinds are temporary. Analysis predicts slower SEK appreciation and underlying stabilisation heading into early 2026, potentially relieving the translational pressure on international earnings.

The reality of the operational floor provides a stark contrast to the broader market apprehension. Specific subsidiary wins demonstrate divergent outcomes across manufacturing divisions, explicitly contrasting massive gains in fastening and logistics against softer construction environments. The wholly-owned industrial groups maintained impressive profit margins despite global turbulence.

Strategic expansion moves, including the Alstor integration for forestry equipment and key European ventilation buyouts, further fortified the portfolio. According to company data, these newly integrated enterprises will add roughly 500 million SEK to annualised turnover.

| Subsidiary Name | Order Surge | Revenue Expansion | Operating Margin | Operating Profit |

|---|---|---|---|---|

| Nord-Lock | 30% | 17% | 29.4% | 166 million SEK |

| Caljan | 34% | 44% | 16.5% | Not disclosed |

| Innovalift | Stable volume | Consistent growth | 9.0% | 70 million SEK |

Modified operating profits across all proprietary divisions reached 886 million SEK, retaining a highly competitive 30.2% profitability ratio. The internal engines of the business are accelerating rather than stalling.

Structural demographic shifts are aggressively driving the accessibility and vertical mobility segment. According to company data, this division generates 3.4 billion SEK annually, manufacturing a massive scale of 10,000 yearly systems. It maintains a solid 9% margin, yielding 70 million SEK in quarterly profit.

Management formally acknowledged this momentum through the April 2026 formation of a new business area within Innovalift. This strategic reorganisation signals future consolidation potential and long-term capacity expansion.

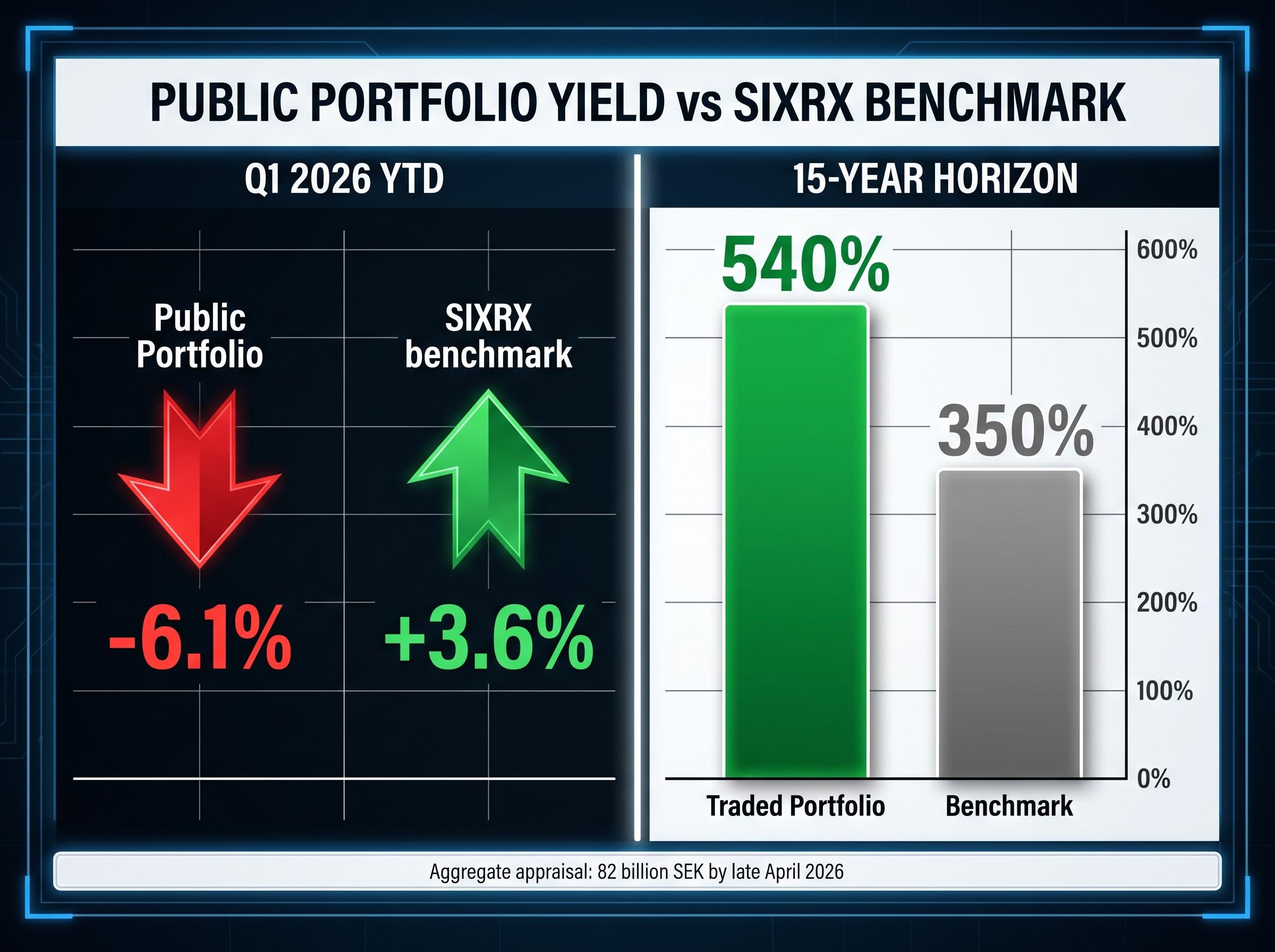

The primary culprits of the valuation drag reside squarely within the publicly traded assets. According to company data, publicly traded asset valuations retreated by 9% in the first quarter of 2026, dropping to an aggregate appraisal of 82 billion SEK by late April 2026. The year-to-date aggregate yield for these listed assets was negative 6.1%, severely lagging the 3.6% advance of the broader SIXRX benchmark.

The earnings report from Tomra Systems ASA disproportionately impacted the broader portfolio perception. Tomra experienced a confirmed 19.3% stock plunge on 24 April 2026 following margin pressures and guidance expecting zero growth for the rest of the year. This specific weakness pulled down the consolidated holding company metrics.

However, this short-term negative yield must be contrasted against massive historical outperformance. According to company data, over a 15-year horizon, the traded portfolio generated a 540% aggregate yield compared to the benchmark’s 350% gain.

The public entities currently face three specific headwinds: Exchange rate disadvantages impacting international revenue conversions Sluggish consumer segments delaying capital expenditure cycles * Mature sector stagnation limiting near-term organic growth opportunities

For investors evaluating the impact of these specific market pressures, our detailed coverage of Latour’s listed portfolio drag examines the negative benchmark comparisons and the strategic acquisitions management is using to offset this volatility.

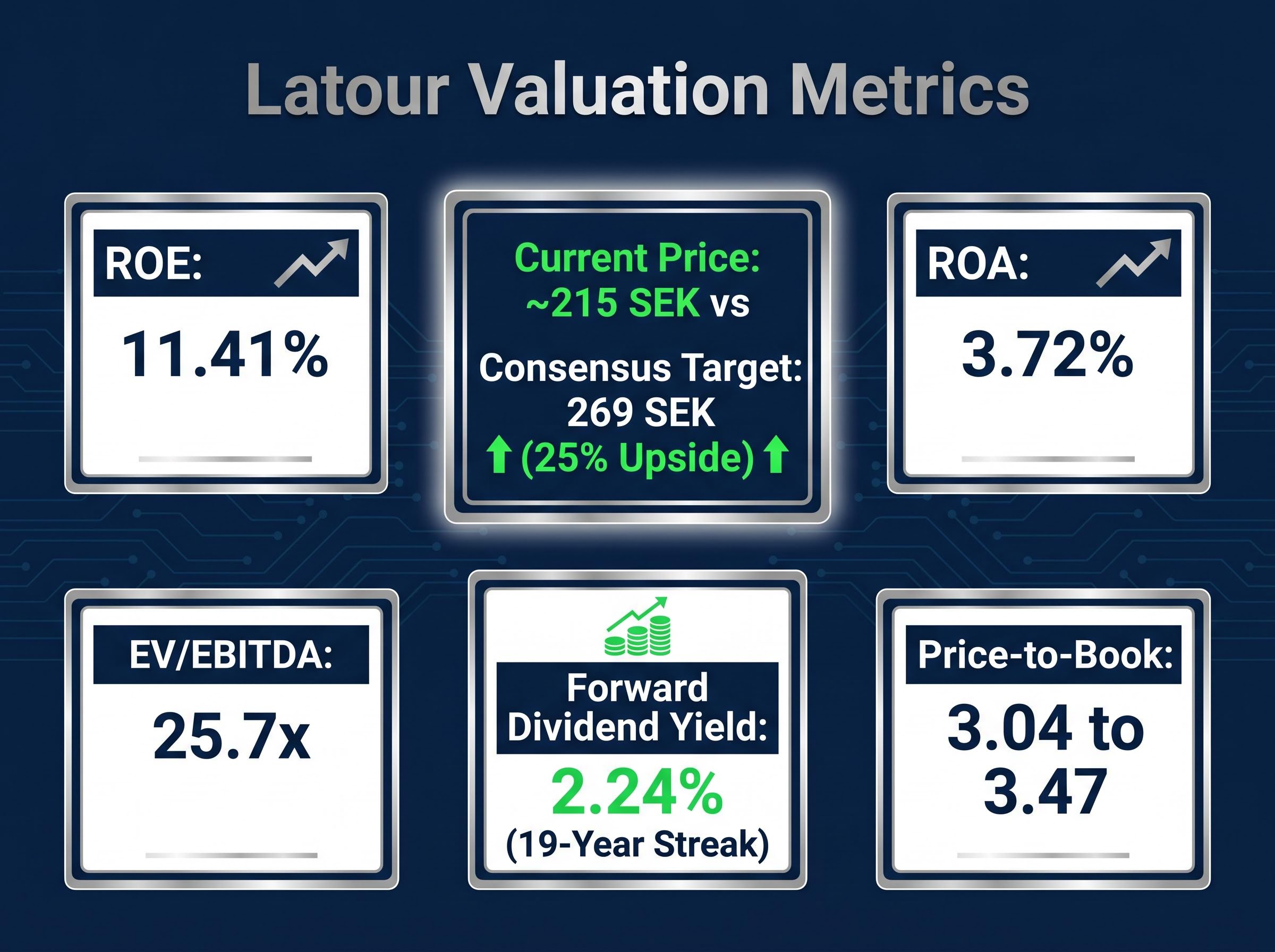

Synthesising these metrics reveals a mathematical gap between the current trading price and consensus target prices. Average consensus target prices sit around 269 SEK, implying a 25% upside from the late April trading levels of roughly 215 SEK. This premium valuation is fundamentally supported by a Return on Equity (ROE) of 11.41% and a Return on Assets (ROA) of 3.72%.

For income-focused investors, the underlying dividend reliability remains a central pillar of the long-term investment thesis. The stock currently offers a forward dividend yield of 2.24%, backed by a 19-year continuous distribution streak. The enterprise valuation to EBITDA ratio (EV/EBITDA) stands at 25.7x, with a Price-to-Book range of 3.04 to 3.47.

First-quarter earnings call transcript details from corporate leadership reinforced that sustaining this multi-decade distribution history remains a core operational mandate despite temporary exchange rate turbulence.

Management’s forward-looking projections for 2026 and 2027 reflect confidence in weathering these cyclical pressures. They expect softening foreign exchange pressures in the second quarter, allowing the underlying operational growth to reflect more accurately in the financials.

Management has identified several primary organisational threats to monitor:

The market reaction in early 2026 was largely a currency and public portfolio-driven event, while the proprietary industrial core remains highly resilient. Management’s long-term holding strategy is designed specifically to weather these cyclical currency storms while capturing market share during industry downturns.

Investors should closely monitor Swedish Krona stabilisation and subsidiary order flow in the upcoming second-quarter reports to verify this recovery thesis. While short-term volatility persists, the underlying manufacturing assets continue to generate reliable cash flows.

Past performance does not guarantee future results. Financial projections are subject to market conditions and various risk factors. These statements are speculative and subject to change based on market developments and company performance. This article is for informational purposes only and should not be considered financial advice. Investors should conduct their own research and consult with financial professionals before making investment decisions.

The recent decline in Investment Latour stock was primarily driven by unfavorable foreign exchange rates impacting reported revenue and a significant drop in its publicly traded assets, particularly Tomra Systems ASA. However, underlying operational growth in its proprietary industrial divisions remained strong.

Yes, Investment Latour stock offers a forward dividend yield of 2.24%, backed by an impressive 19-year history of continuous dividend distributions. Management has reinforced that sustaining this distribution streak is a core operational mandate.

Unfavorable currency translations negatively impacted Latour's Q1 2026 corporate revenue by approximately 6%, masking a solid 5% increase in incoming requests from core markets. This was a translational effect, not a fundamental operational decline.

Latour trading below its net asset value, with NAV falling 5.9% to 203 SEK per share, is highly unusual for this holding company, which typically trades at a significant premium. This creates a rare market discount that investors are currently evaluating.

Latour's proprietary industrial businesses, including Nord-Lock, Caljan, and Innovalift, demonstrated robust growth and high profit margins in Q1 2026. Management remains confident in their performance, with strategic expansions and new business area formations signaling continued momentum.